Applying the Doctrine of Revocation by Divorce to Life Insurance Policies Alan S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Petition for Marriage Permission Or Dispensation

Form M2 Revised 9/2009 DIOCESE OF SPOKANE PETITION FOR MARRIAGE PERMISSION OR DISPENSATION GROOM BRIDE Name Name Address Address City, State City, State Date of Birth Date of Birth RELIGION Catholic Catholic Parish: Parish: Place: Place: Baptized non-Catholic Baptized non-Catholic Denomination: Denomination: Unbaptized Unbaptized Scheduled date and place for marriage: The following dispensation and permissions may be granted by the pastor for marriages celebrated within the territory his parish. Otherwise, the petition is submitted to the Local Ordinary. A. Disparity of Cult (C. 1086, a Catholic and a non-baptized person). See reverse side. B. Mixed Religion (and, if necessary, disparity of cult, C. 1124). See reverse side. C. Natural obligations from a prior union (C. 1071 3°). Marriage is permitted only when the pastor or competent authority is sure that these obligations are being fulfilled. D. Permission to marry when conditions are attached to a declaration of nullity—granted only if these stipulations have been fulfilled. (Cf. C. 1684) By virtue of the faculties granted to pastors of the Diocese of Spokane, I hereby grant the above indicated permissions/dispensation. Pastor: Date: (This document is retained in the prenuptial file) See p. 2 of this form for dispensations and permissions reserved to the Local Ordinary (Diocesan bishop, Vicar General or their delegate). Page 1 of 2 Form M2 In cases of Mixed Religion (Catholic and a baptized non-Catholic) or Disparity of Cult, the Catholic party is to make the following promise in writing or orally: “I reaffirm my faith in Jesus Christ and, with God’s help, intend to continue living that faith in the Catholic Church. -

Suspension and Revocation Chapter 23 Major Offenses

MRS Title 29-A, Chapter 23. MAJOR OFFENSES - SUSPENSION AND REVOCATION CHAPTER 23 MAJOR OFFENSES - SUSPENSION AND REVOCATION SUBCHAPTER 1 GENERAL PROVISIONS §2401. Definitions As used in this chapter, unless the context otherwise indicates, the following terms have the following meanings. [PL 1993, c. 683, Pt. A, §2 (NEW); PL 1993, c. 683, Pt. B, §5 (AFF).] 1. Alcohol and drug program. "Alcohol and drug program" means the alcohol and other drug education, evaluation and treatment program administered by the Department of Health and Human Services under Title 5, chapter 521, subchapter 5. [PL 2011, c. 657, Pt. AA, §77 (AMD).] 2. Alcohol level. "Alcohol level" means either grams of alcohol per 100 milliliters of blood or grams of alcohol per 210 liters of breath. [PL 2009, c. 447, §32 (AMD).] 3. Chemical test or test. "Chemical test" or "test" means a test or tests used to determine alcohol level or the presence of a drug or drug metabolite by analysis of blood, breath or urine. [PL 2013, c. 459, §1 (AMD).] 4. Drugs. "Drugs" means scheduled drugs as defined under Title 17‑A, section 1101. The term "drugs" includes any natural or artificial chemical substance that, when taken into the human body, can impair the ability of the person to safely operate a motor vehicle. [PL 1995, c. 145, §1 (AMD).] 5. Failure to submit to a test, fails to submit to a test or failed to submit to a test. "Failure to submit to a test," "fails to submit to a test" or "failed to submit to a test" means failure to comply with the duty to submit to and complete a chemical test under section 2521 or 2525. -

DCC ECRM Supervision Supervision Process Revocation.Pdf

Electronic Case Reference Manual > Supervision > DCC Supervision > Supervision Process > Revocations Investigation/Decision Pre-Preliminary Hearing Waived Hearings Preliminary Hearings Post-Preliminary Hearing Final Revocation Hearing Appeals Revocation and Reinstatement Orders Special Revocation Procedures Legal Rules, Aids & Guidelines INVESTIGATION/DECISION .01 AUTHORITY Wisconsin Administrative Code Sections HA 2 Wisconsin Administrative Code DOC 331 Wisconsin Statutes 302.11 .02 GENERAL STATEMENT An offender's supervision may be revoked if the offender violates a rule or condition of supervision. When supervision is revoked, the offender is either: returned to court for sentencing, or transported to a correctional facility to begin serving the sentence indicated by the Court. Protection of the public is the primary consideration in any revocation decision. .03 TIME FRAMES These time frames only apply to cases where an Order to Detain (DOC-212) has been authorized by the Department. Electronic Case Reference Manual > Supervision > DCC Supervision > Supervision Process > Revocations If the offender is in custody, the offender should be interviewed within 3 working days. The original 3 working day detention for investigation can be extended by completing a Detention Extension Request (DOC-212). The supervisor may extend detention for 3 working days. The Regional Chief may extend for an additional 5 working days. If further extension is necessary, the Administrator or designee may approve any additional time in increments of five days. Once a decision to revoke has been made, the Notice of Violation and Hearing Rights (DOC-414) shall be served within 2 working days. If revocation will proceed and an ATR is not likely at the time of issuance of the DOC-414, the Revocation Notification to Victim (DOC-2938) along with a Revocation Proceeding Fact Sheet for Victims shall be sent to the victim. -

HOUSE BILL No. 2038

{As Amended by Senate Committee of the Whole} Session of 2019 HOUSE BILL No. 2038 By Committee on Judiciary 1-17 1 AN ACT concerning inheritance rights; relating to revocation upon 2 divorce. 3 4 Be it enacted by the Legislature of the State of Kansas: 5 Section 1. (a) As used in this section: 6 (1) "Disposition or appointment of property" includes a transfer of an 7 item of property or any other benefit to a beneficiary designated in a 8 governing instrument. 9 (2) "Divorce or annulment" means any divorce or annulment, or any 10 dissolution or declaration of invalidity of a marriage that would exclude 11 the spouse as a surviving spouse. A decree of separation that does not 12 terminate the parties' marital status is not a divorce for purposes of this 13 section. 14 (3) "Divorced individual" includes an individual whose marriage has 15 been annulled. 16 (4) "Governing instrument" means a document executed by the 17 divorced individual before the divorce or annulment of such individual's 18 marriage to such individual's former spouse. 19 (5) "Relative of the divorced individual's former spouse" means an 20 individual who is related to the divorced individual's former spouse by 21 blood, adoption or affinity and who, after the divorce or annulment, is not 22 related to the divorced individual by blood, adoption or affinity. 23 (6) "Revocable," with respect to a disposition, appointment, provision 24 or nomination, means one under which the divorced individual, at the time 25 of the divorce or annulment, was alone empowered, by law or under the 26 governing instrument, to cancel the designation in favor of such 27 individual's former spouse or former spouse's relative, whether or not the 28 divorced individual was then empowered to designate such individual's 29 self in place of such individual's former spouse or in place of such 30 individual's former spouse's relative and whether or not the divorced 31 individual then had the capacity to exercise the power. -

Revocation of Trusts by Consent of the Beneficiaries

Indiana Law Journal Volume 36 Issue 1 Article 4 Fall 1960 Revocation of Trusts by Consent of the Beneficiaries Follow this and additional works at: https://www.repository.law.indiana.edu/ilj Part of the Estates and Trusts Commons Recommended Citation (1960) "Revocation of Trusts by Consent of the Beneficiaries," Indiana Law Journal: Vol. 36 : Iss. 1 , Article 4. Available at: https://www.repository.law.indiana.edu/ilj/vol36/iss1/4 This Note is brought to you for free and open access by the Law School Journals at Digital Repository @ Maurer Law. It has been accepted for inclusion in Indiana Law Journal by an authorized editor of Digital Repository @ Maurer Law. For more information, please contact [email protected]. NOTES REVOCATION OF TRUSTS BY CONSENT OF THE BENEFICIARIES The settlor of an inter vivos trust generally cannot revoke it unless he has reserved in the trust instrument a power of revocation.' A well recognized exception occurs, however, where all persons who have a "beneficial interest" in the trust give their consent that the settlor can revoke the trust even though the instrument declares that the trust shall be irrevocable.' This exception, called the consent rule, is derived from the English common-law and has been adopted throughout most of the United States3 whenever the question of revocation of a trust by the con- sent of the beneficiaries has arisen. Generally, when a settlor has granted property rights he cannot resume his former status merely because he later decides his disposition was unwise.4 But if the settlor and all the beneficiaries no longer wish the trust to be continued, there is no reason for the court to insist that its terms be carried out.5 The rule is simple enough as stated, but courts have experienced con- siderable difficulty in determining who are persons beneficially interested. -

Revocation of "Irrevocable" Trusts

Fordham Law Review Volume 6 Issue 2 Article 5 1937 Revocation of "Irrevocable" Trusts Follow this and additional works at: https://ir.lawnet.fordham.edu/flr Part of the Law Commons Recommended Citation Revocation of "Irrevocable" Trusts, 6 Fordham L. Rev. 242 (1937). Available at: https://ir.lawnet.fordham.edu/flr/vol6/iss2/5 This Article is brought to you for free and open access by FLASH: The Fordham Law Archive of Scholarship and History. It has been accepted for inclusion in Fordham Law Review by an authorized editor of FLASH: The Fordham Law Archive of Scholarship and History. For more information, please contact [email protected]. COMMENTS REVOCATION OF "IRREvOCABLE" TRuSvs.-Every period of economic depres- sion serves to accentuate the already perplexing problems of the law. Coinci- dental with the last of these periods, the situation became acute in relation to the problem of revocation of the so-called irrevocable trusts, that is, trusts wherein the right of revocation has not been expressly reserved. This well recognized though paradoxical description of the problem arises from the single exception to the rule that such trusts are irrevocable, which permits revocation of a living trust upon the consent of all persons beneficially interested therein. No state fails to make the exception and New York has codified it.' Applica- tion of the pertinent rules to any particular case involves, at the outset, the de- termination, first, of the character of the estates created by the disposition made of the corpus of the trust in the trust deed and, second, in many instances, re- quires the ascertainment of the nature and quality of the interest which, under the exception, will constitute a beneficial interest. -

Revoking Rights

University of Colorado Law School Colorado Law Scholarly Commons Articles Colorado Law Faculty Scholarship 2015 Revoking Rights Craig J. Konnoth University of Colorado Law School Follow this and additional works at: https://scholar.law.colorado.edu/articles Part of the Civil Rights and Discrimination Commons, Constitutional Law Commons, Human Rights Law Commons, Law and Race Commons, Legal History Commons, Sexuality and the Law Commons, and the Social Welfare Law Commons Citation Information Craig J. Konnoth, Revoking Rights, 66 HASTINGS L.J. 1365 (2015), available at https://scholar.law.colorado.edu/articles/711. Copyright Statement Copyright protected. Use of materials from this collection beyond the exceptions provided for in the Fair Use and Educational Use clauses of the U.S. Copyright Law may violate federal law. Permission to publish or reproduce is required. This Article is brought to you for free and open access by the Colorado Law Faculty Scholarship at Colorado Law Scholarly Commons. It has been accepted for inclusion in Articles by an authorized administrator of Colorado Law Scholarly Commons. For more information, please contact [email protected]. +(,121/,1( Citation: 66 Hastings L.J. 1365 2014-2015 Provided by: William A. Wise Law Library Content downloaded/printed from HeinOnline Thu Jul 20 19:14:11 2017 -- Your use of this HeinOnline PDF indicates your acceptance of HeinOnline's Terms and Conditions of the license agreement available at http://heinonline.org/HOL/License -- The search text of this PDF is generated from uncorrected OCR text. -- To obtain permission to use this article beyond the scope of your HeinOnline license, please use: Copyright Information Revoking Rights CRAIG J. -

Petitioners Brief

No. 16-1432 IN THE Supreme Court of the United States _________ ASHLEY SVEEN AND ANTONE SVEEN, Petitioners, v. KAYE MELIN, Respondent. ________ On Writ of Certiorari to the United States Court of Appeals for the Eighth Circuit ________ BRIEF OF PETITIONERS ________ DANIEL DODA ADAM G. UNIKOWSKY DODA MCGEENEY Counsel of Record 975 34th Ave. NW JAMES T. DAWSON* Suite 400 JENNER & BLOCK LLP Rochester, MN 55901 1099 New York Ave., NW, Suite 900 Washington, DC 20001 (202) 639-6000 [email protected] CLIFFORD W. BERLOW JENNER & BLOCK LLP 353 North Clark St. Chicago, IL 60654 * Not admitted in Washington, D.C. Only admitted in Texas. i QUESTION PRESENTED In 2002, Minnesota enacted legislation providing, in relevant part, that “the dissolution or annulment of a marriage revokes any revocable … beneficiary designation … made by an individual to the individual’s former spouse.” Minn. Stat. § 524.2-804, subd. 1. Thus, if a person designates a spouse as a life insurance beneficiary and later gets divorced, Minnesota law provides that the beneficiary designation is automatically revoked. At least twenty-eight other states have enacted similar revocation-on-divorce statutes. The question presented is: Does the application of a revocation-on-divorce statute to a contract signed before the statute’s enactment violate the Contracts Clause? ii TABLE OF CONTENTS QUESTION PRESENTED .............................................. i TABLE OF AUTHORITIES ......................................... vi OPINIONS BELOW ........................................................ -

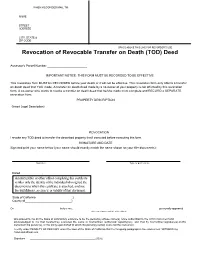

Revocation of Revocable Transfer on Death (TOD) Deed

WHEN RECORDED MAIL TO: NAME STREET ADDRESS CITY, STATE & ZIP CODE SPACE ABOVE THIS LINE FOR RECORDER’S USE Revocation of Revocable Transfer on Death (TOD) Deed Assessor's Parcel Number:_______________________ IMPORTANT NOTICE: THIS FORM MUST BE RECORDED TO BE EFFECTIVE This revocation form MUST be RECORDED before your death or it will not be effective. This revocation form only affects a transfer on death deed that YOU made. A transfer on death deed made by a co-owner of your property is not affected by this revocation form. A co-owner who wants to revoke a transfer on death deed that he/she made must complete and RECORD a SEPARATE revocation form. PROPERTY DESCRIPTION REVOCATION I revoke any TOD deed to transfer the described property that I executed before executing this form. SIGNATURE AND DATE Sign and print your name below (your name should exactly match the name shown on your title documents): Signature Type or print name Dated , . A notary public or other officer completing this certificate verifies only the identity of the individual who signed the document to which this certificate is attached, and not the truthfulness, accuracy, or validity of that document. State of California } County of } On before me, personally appeared (here insert name and title of the officer) , who proved to me on the basis of satisfactory evidence to be the person(s) whose name(s) is/are subscribed to the within instrument and acknowledged to me that he/she/they executed the same in his/her/their authorized capacity(ies), and that by his/her/their signature(s) on the instrument the person(s), or the entity upon behalf of which the person(s) acted, executed the instrument. -

Clerical Opposition in Habsburg Castile

02_EHQ 31/3 articles 3/7/01 10:13 am Page 323 Sean T. Perrone Clerical Opposition in Habsburg Castile Introduction The emergence of the new monarchies at the end of the fifteenth century and the beginning of the sixteenth century has often been considered a watershed mark in the development of the modern state. Historians and social scientists have argued that this transition led to greater royal control over society, including the clergy. John Thomson, for example, notes that in the fifteenth century princes gradually wrested from the papacy the right of appointment to ecclesiastical benefices, the right to tax the clergy, and greater jurisdictional rights over the national Church.1 According to the state-building paradigm, then, the new monarchies brought an end to the universalist claims of the popes and brought the national clergy more thoroughly under royal control. This suggests, however, a sharp discontinuity with the medieval past, which was full of struggles between Church and State. A few of the most notable examples include: the ‘investiture con- flict’ in Germany, which led Henry IV (1056–1106) to prostrate himself before the gates of Castile Canossa for three consecutive days seeking papal absolution (1077);2 the struggles in England over the status of Church courts and law, and the subsequent murder of Archbishop Thomas à Becket in Canterbury Cathedral (1170); and the conflicts between Philip the Fair (1285–1314) and Boniface VIII (1294–1303) over ecclesiastical taxation and immunity, which were only resolved when Philip arrested Boniface VIII (1303). Could the contentious popes, bishops, and priests of the Middle Ages really have been subdued and trans- formed so rapidly? No. -

LOVE, POWER, and SUFFERING: SALVATION in GHANAIAN PENTECOSTALISM and ROMANS 8:35-39 Kirsten Jeffery, Graduate Nazarene Theological College, Manchester

1 LOVE, POWER, AND SUFFERING: SALVATION IN GHANAIAN PENTECOSTALISM AND ROMANS 8:35-39 Kirsten Jeffery, Graduate Nazarene Theological College, Manchester Finding Favour Neno Evangelism Centre in Nairobi, Kenya is one of the largest in the city. Its charismatic leader, James Ng’ang’a, preached to a packed building and a television audience on the day my husband and I visited for a Sunday service in October 2012. The high point of the service was the offering, which came after the pastor had given a short message assuring people that God wanted to bless them financially. But the blessing depended on faith, and faith could be demonstrated by giving money to God, even if it was all the money they had. During the offering, we watched hundreds of people throw money onto the stage, blanketing the carpet around the preacher. I met one of the worshippers outside afterwards. She lived in a slum outside Nairobi and had two young children. She was unemployed and barely survived day to day. She said she came to the church because the pastor had an anointing of divine favour which brought blessing. She hoped that, by spending time near him, she would catch some of that favour to transform her own circumstances. Christians claim that the life, death, and resurrection of Christ has changed the world. God has definitively shown his love for his creation and his intention to bring it from death to life. When, and how, will God do that for this woman? How does the love of God act in our world? These questions are raised by hardship of all kinds in all situations. -

Revocation by Dissolution of Marriage

REVOCATION BY DISSOLUTION OF MARRIAGE. Subdivision 1. Revocation upon dissolution. Except as provided by the express terms of a governing instrument, a dissolution of marriage revokes any revocable: (a) disposition or appointment of property in a governing instrument made by a divorced individual to or for the benefit of the divorced individual's former spouse or a relative of the divorced individual’s former spouse1; (b) provision in a governing instrument conferring a general or nongeneral power of appointment on a former spouse or on a relative of an individual’s former spouse; and (c) nomination in a governing instrument, nominating an individual's former spouse or a relative of the individual’s former spouse to serve in any fiduciary or representative capacity, including as a personal representative, executor, trustee, conservator, agent, or guardian. Subd. 2. Effect of revocation.2 Provisions of a governing instrument are given effect as if the former spouse and relatives of the former spouse died immediately before the dissolution of marriage. Subd. 3. Revival if dissolution nullified. Provisions of a governing instrument revoked solely by this section are revived by the divorced individual's remarriage to the former spouse or by a nullification of the dissolution of marriage. Subd. 4. No revocation for other change of circumstances. No change of circumstances other than as described in this section and in § 45a- 4473 effects a revocation. 1 We should consider amending C.G.S. § 45a-257(c) (Marriage of testator terminated after execution of will. Provisions of will re former spouse revoked) to also include relatives.