Keynes, Hayek and the Great Recession

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Against Regulatory Stimulus

University of Colorado Law School Colorado Law Scholarly Commons Articles Colorado Law Faculty Scholarship 2020 Against Regulatory Stimulus Erik F. Gerding University of Colorado Law School Follow this and additional works at: https://scholar.law.colorado.edu/articles Part of the Administrative Law Commons, Banking and Finance Law Commons, Law and Economics Commons, and the Legislation Commons Citation Information Erik F. Gerding, Against Regulatory Stimulus, 83 LAW & CONTEMP. PROBS. 49 (2020), available at https://scholar.law.colorado.edu/articles/1268. Copyright Statement Copyright protected. Use of materials from this collection beyond the exceptions provided for in the Fair Use and Educational Use clauses of the U.S. Copyright Law may violate federal law. Permission to publish or reproduce is required. This Article is brought to you for free and open access by the Colorado Law Faculty Scholarship at Colorado Law Scholarly Commons. It has been accepted for inclusion in Articles by an authorized administrator of Colorado Law Scholarly Commons. For more information, please contact [email protected]. BOOK PROOF -G ERDING (DO NOT DELETE) 3/1/2020 10:34 PM AGAINST REGULATORY STIMULUS ERIK F. GERDING* I INTRODUCTION The 2012 JOBS Act1 deserves close scrutiny not only because of its impact on federal securities laws, but because it represented an attempt by Congress to use deregulation as a macroeconomic tool to jumpstart growth. When enacted in 2012, the U.S. economy was still struggling to recover from the global financial crisis. After the crisis, traditional macroeconomic tools were either rendered ineffective or appeared politically infeasible. Interest rates were already close to zero, and fears grew that global economies had entered a “liquidity trap.”2 Meanwhile, the Republican-controlled House of Representatives consistently blocked Democrats’ fiscal spending initiatives. -

Quantitative Easing and Inequality: QE Impacts on Wealth and Income Distribution in the United States After the Great Recession

University of Puget Sound Sound Ideas Economics Theses Economics, Department of Fall 2019 Quantitative Easing and Inequality: QE impacts on wealth and income distribution in the United States after the Great Recession Emily Davis Follow this and additional works at: https://soundideas.pugetsound.edu/economics_theses Part of the Finance Commons, Income Distribution Commons, Macroeconomics Commons, Political Economy Commons, and the Public Economics Commons Recommended Citation Davis, Emily, "Quantitative Easing and Inequality: QE impacts on wealth and income distribution in the United States after the Great Recession" (2019). Economics Theses. 108. https://soundideas.pugetsound.edu/economics_theses/108 This Dissertation/Thesis is brought to you for free and open access by the Economics, Department of at Sound Ideas. It has been accepted for inclusion in Economics Theses by an authorized administrator of Sound Ideas. For more information, please contact [email protected]. Quantitative Easing and Inequality: QE impacts on wealth and income distribution in the United States after the Great Recession Emily Davis Abstract In response to Great Recession, the Federal Reserve implemented quantitative easing. Quantitative easing (QE) aided stabilization of the economy and reduction of the liquidity trap. This research evaluates the correlation between QE implementation and increased inequality through the recovery of the Great Recession. The paper begins with an evaluation of the literature focused on QE impacts on financial markets, wages, and debt. Then, the paper conducts an analysis of QE impacts on income, household wealth, corporations and the housing market. The analysis found that the changes in wealth distribution had a significant impact on increasing inequality. Changes in wages were not the prominent cause of changes in GINI post-recession so changes in existing wealth appeared to be a contributing factor. -

QE Equivalence to Interest Rate Policy: Implications for Exit

QE Equivalence to Interest Rate Policy: Implications for Exit Samuel Reynard∗ Preliminary Draft - January 13, 2015 Abstract A negative policy interest rate of about 4 percentage points equivalent to the Federal Reserve QE programs is estimated in a framework that accounts for the broad money supply of the central bank and commercial banks. This provides a quantitative estimate of how much higher (relative to pre-QE) the interbank interest rate will have to be set during the exit, for a given central bank’s balance sheet, to obtain a desired monetary policy stance. JEL classification: E52; E58; E51; E41; E43 Keywords: Quantitative Easing; Negative Interest Rate; Exit; Monetary policy transmission; Money Supply; Banking ∗Swiss National Bank. Email: [email protected]. The views expressed in this paper do not necessarily reflect those of the Swiss National Bank. I am thankful to Romain Baeriswyl, Marvin Goodfriend, and seminar participants at the BIS, Dallas Fed and SNB for helpful discussions and comments. 1 1. Introduction This paper presents and estimates a monetary policy transmission framework to jointly analyze central banks (CBs)’ asset purchase and interest rate policies. The negative policy interest rate equivalent to QE is estimated in a framework that ac- counts for the broad money supply of the CB and commercial banks. The framework characterises how standard monetary policy, setting an interbank market interest rate or interest on reserves (IOR), has to be adjusted to account for the effects of the CB’s broad money injection. It provides a quantitative estimate of how much higher (rel- ative to pre-QE) the interbank interest rate will have to be set during the exit, for a given central bank’s balance sheet, to obtain a desired monetary policy stance. -

HOW DID QUANTITATIVE EASING REALLY WORK? a New Methodology for Measuring the Fed’S Impact on Financial Markets

HOW DID QUANTITATIVE EASING REALLY WORK? A New Methodology for Measuring the Fed’s Impact on Financial Markets Ramin Toloui Stanford Institute for Economic Policy Research [email protected] SIEPR Working Paper No. 19-032 November 2019 ABSTRACT This paper introduces a new methodology for measuring the impact of unconventional policies. Specifically, the paper examines how such policies reshaped market perceptions of how the Fed would behave in the future—not merely the expected path for policy rates, but how the central bank would adjust that path in response to different combinations of future inflation and growth. In short, it studies how quantitative easing affected investor beliefs about the future policy reaction function. The paper (1) proposes a novel model of market expectations for the central bank’s future policy reaction function based on the Taylor Rule; (2) shows that empirical estimates of the model exhibit structural breaks that coincide with innovations in unconventional policies; and (3) finds that such policy innovations were associated with regime shifts in the behavior of 10-year U.S. Treasury yields, as well as unusual performance in risk assets such as credit spreads and equities. These findings provide evidence that a key causal channel for unconventional policies was via their impact on market expectations for the Fed’s future policy reaction function. These shifts in expectations, in turn, appear to have had larger, more persistent, and more pervasive effects across financial markets than found in previous studies. Monetary economics today is obsessed with balance sheets—and rightfully so. More than ten years after the global financial crisis, policy interest rates remain exceptionally low in much of the industrialized world. -

Working Paper

WP 2020-12 December 2020 Working Paper Charles H. Dyson School of Applied Economics and Management Cornell University, Ithaca, New York 14853-7801 USA Social Externalities and Economic Analysis Marc Fleurbaey, Ravi Kanbur, and Brody Viney It is the Policy of Cornell University actively to support equality of educational and employment opportunity. No person shall be denied admission to any educational program or activity or be denied employmen t on the basis of any legally prohibited discrimination involving, but not limited to, such factors as race, color, creed, religion, national or ethnic origin, sex, age or handicap. The University is committed to the maintenance of affirmative action prog rams which will assure the continuation of such equality of opportunity. 2 Social Externalities and Economic Analysis Marc Fleurbaey, Ravi Kanbur, Brody Viney ThisThis version: versio Augustn: Aug 6,us 2020t 6, 20201 Abstract This paper considers and assesses the concept of social externalities through human interdependence, in relation to the economic analysis of externalities in the tradition of Pigou and Arrow, including the analysis of the commons. It argues that there are limits to economic analysis. Our proposal is to enlarge the perspective and start thinking about a broader framework in which any pattern of influence of an agent or a group of agents over a third party, which is not mediated by any economic, social, or psychological mechanism guaranteeing the alignment of the marginal net private benefit with marginal net social benefit, can be attached the “externality” label and be scrutinized for the likely negative consequences that result from the divergence .These consequences may be significant given the many interactions between the social and economic realms, and the scope for spillovers and feedback loops to emerge. -

How Would Modern Macroeconomic Schools of Thought Respond to the Recent Economic Crisis?

® Economic Information Newsletter Liber8 Brought to You by the Research Library of the Federal Reserve Bank of St. Louis November 2009 How Would Modern Macroeconomic Schools of Thought Respond to the Recent Economic Crisis? “Would financial markets and the economy have been better off if the Fed pursued a policy of quantitative easing sooner?” —Daniel L. Thornton, Vice President and Economic Adviser, Federal Reserve Bank of St. Louis, Economic Synopses The government and the Federal Reserve’s response to the current recession continues to be hotly de bated. Several questions arise: Was a $780 billion economic stimulus bill appropriate? Was the Troubled Asset Re lief Program (TARP) beneficial? Should the Fed have increased the money supply sooner? Should Lehman Brothers have been allowed to fail? Some answers to these questions lie in economic theory, and whether prudent decisions were made depends on whom you ask. This article examines three modern schools of economic thought and how each school would advise was the best way to respond to the most recent crisis. The New Keynesian Approach New Keynesian economics, the “new” version of the school based on the works of the early twentieth- century economist John Maynard Keynes, is founded on two major assumptions. First, people are forward looking; that is, they use available information today (interest rates, stock prices, gas prices, and so on) to form expectations about the future. Second, prices and wages are “sticky,” meaning they adjust gradually. One example of “stickiness” is a union-negotiated contract, which is fixed for a definite period of time. Menus are also an example of price stickiness: The cost associated with reprinting menus causes a restaurant owner to be reluctant about replacing them. -

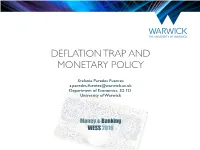

04 Deflation Trap and Unconventional Mon

DEFLATION TRAP AND MONETARY POLICY Stefania Paredes Fuentes [email protected] Department of Economics, S2.121 University of Warwick Money & Banking WESS 2016 DEFLATION TRAP • CB adjusts the nominal interest rate in order to affect the real interest rate - It must take into account expected inflation i = r + πe • Nominal interest rate cannot be below zero - Zero lower bound (ZLB) min r πe ≥− Stefania Paredes Fuentes Money and Banking WESS 2016 THE 3-EQUATION MODEL AND MACROECONOMIC POLICY 2009 2011 Inflation in Industrialised Economies 2000-2015 Stefania Paredes Fuentes Money and Banking WESS 2016 DEFLATION TRAP r A r =re IS π y PC(πE= 2%) π =2% A MR ye y Stefania Paredes Fuentes Money and Banking WESS 2016 DEFLATION TRAP r Large permanent negative AD shock B A r =re y IS’ IS π PC(πE= 2%) π =2% A ye y MR Stefania Paredes Fuentes Money and Banking WESS 2016 DEFLATION TRAP Large permanent r negative AD shock B A rs i = r + πE y r’0 C’ i = rs - 0.5% IS IS’ min r ≥ - πE π PC(πE= 2%) E PC(π 1= 0.5%) π =2% A C’ ye π0 = -0.5% B MR Stefania Paredes Fuentes Money and Banking WESS 2016 DEFLATION TRAP Large permanent r negative AD shock i = r + πE B A min r ≥ - πE rs C min r = r0 = -0.5% y1 y’1 y r’0 C’ IS IS’ π PC(πE= 2%) E PC(π 1= π0) π =2% A C’ ye y π0 B MR π1 C Stefania Paredes Fuentes Money and Banking WESS 2016 DEFLATION TRAP Large permanent r negative AD shock i = r + πE B A E rs min r ≥ - π X r’s C min r = r0 = -0.5% y1 y’1 y r’0 C’ IS IS’ π PC(πE= 2%) E PC(π 1= π0) π =2% A C’ ye y π0 B MR π1 C Stefania Paredes Fuentes Money and -

Chapter 28 | Monetary Policy and Bank Regulation 635 28 | Monetary Policy and Bank Regulation

Chapter 28 | Monetary Policy and Bank Regulation 635 28 | Monetary Policy and Bank Regulation Figure 28.1 Marriner S. Eccles Federal Reserve Headquarters, Washington D.C. Some of the most influential decisions regarding monetary policy in the United States are made behind these doors. (Credit: modification of work by “squirrel83”/Flickr Creative Commons) The Problem of the Zero Percent Interest Rate Lower Bound Most economists believe that monetary policy (the manipulation of interest rates and credit conditions by a nation’s central bank) has a powerful influence on a nation’s economy. Monetary policy works when the central bank reduces interest rates and makes credit more available. As a result, business investment and other types of spending increase, causing GDP and employment to grow. But what if the interest rates banks pay are close to zero already? They cannot be made negative, can they? That would mean that lenders pay borrowers for the privilege of taking their money. Yet, this was the situation the U.S. Federal Reserve found itself in at the end of the 2008–2009 recession. The federal funds rate, which is the interest rate for banks that the Federal Reserve targets with its monetary policy, was slightly above 5% in 2007. By 2009, it had fallen to 0.16%. The Federal Reserve’s situation was further complicated because fiscal policy, the other major tool for managing the economy, was constrained by fears that the federal budget deficit and the public debt were already too high. What were the Federal Reserve’s options? How could monetary policy be used to stimulate the economy? The answer, as we will see in this chapter, was to change the rules of the game. -

Inflation and Other Risks of Unsound Money

Inflation and Other Risks of Unsound Money Prepared by Martin Hickling Presented to the Actuaries Institute Actuaries Summit 20-21 May 2013 Sydney This paper has been prepared for Actuaries Institute 2013 Actuaries Summit. The Institute Council wishes it to be understood that opinions put forward herein are not necessarily those of the Institute and the Council is not responsible for those opinions. copyright Martin Hickling The Institute will ensure that all reproductions of the paper acknowledge the Author/s as the author/s, and include the above copyright statement. Institute of Actuaries of Australia ABN 69 000 423 656 Level 7, 4 Martin Place, Sydney NSW Australia 2000 t +61 (0) 2 9233 3466 f +61 (0) 2 9233 3446 e [email protected] w www.actuaries.asn.au Inflation and Other Risks of Unsound Money Purpose of paper To investigate Austrian economic literature and explain to an actuarial audience the concepts of ‘sound money’ (normally a commodity based medium of exchange) and the risks, including inflation, of the current ‘unsound’ government-issued fiat based money system. Abstract No form of money is perfect. Even gold suffers from new supply – although it is quite difficult and costly to mine. Austrian economic theory helps us to understand the distortions and ultimate consequences of injections of government fiat paper money. As the new money is created it dilutes purchasing power of the holders of money - in a free market this is the people who have produced more than they have consumed - and reduces the real value of holders of nominal debts. -

How QE Works: Evidence on the Refinancing Channel

How Quantitative Easing Works: Evidence on the Refinancing Channel⇤ § Marco Di Maggio† Amir Kermani‡ Christopher J. Palmer August 2019 Abstract We document the transmission of large-scale asset purchases by the Federal Reserve to the real economy using rich borrower-linked mortgage-market data and an identifica- tion strategy based on mortgage market segmentation. We find that central bank QE1 MBS purchases substantially increased refinancing activity, reduced interest payments for refinancing households, led to a boom in equity extraction, and increased aggre- gate consumption. Relative to QE-ineligible jumbo mortgages, QE-eligible conforming mortgage interest rates fell by an additional 40 bp and refinancing volumes increased by an additional 56% during QE1. We estimate that households refinancing during QE1 increased their durable consumption by 12%. Our results highlight that the transmis- sion of unconventional monetary policy to the real economy depends crucially on the composition of assets purchased and the degree of segmentation in the market. ⇤Apreviousversionofthispaperwascirculatedunderthetitle,“UnconventionalMonetaryPolicyand the Allocation of Credit.” For helpful comments, we thank our discussants, Florian Heider, Anil Kashyap, Deborah Lucas, Alexi Savov, Philipp Schnabl, and Felipe Severino; Adam Ashcraft, Andreas Fuster, Nicola Gennaioli, Robin Greenwood, Sam Hanson, Arvind Krishnamurthy, Stephan Luck, Michael Johannes, David Romer, David Scharfstein, Andrei Shleifer, Jeremy Stein, Johannes Stroebel, Stijn Van Nieuwerburgh, An- nette Vissing-Jørgensen, Nancy Wallace, and Paul Willen; seminar, conference, and workshop participants at Berkeley, Chicago Fed, Columbia, NBER Monetary, NBER Corporate Finance, Econometric Society, EEA, Fed Board, HEC Paris, MIT, Northwestern, NYU, NY Fed/NYU Stern Conference on Financial Intermedi- ation, Paul Woolley Conference at LSE, Penn State, San Francisco Fed, Stanford, St. -

How Quantitative Easing Works: Evidence on the Refinancing Channel

Harvard | Business | School Project onThe Behavioral Behavioral Finance Finance and and Financial Financial Stabilities Stability Project Project How Quantitative Easing Works: Evidence on the Refinancing Channel Marco Di Maggio Amir Kermani Christopher Palmer Working Paper 2016-08 How Quantitative Easing Works: Evidence on the Refinancing Channel⇤ § Marco Di Maggio† Amir Kermani‡ Christopher Palmer December 2016 Abstract Despite massive large-scale asset purchases (LSAPs) by central banks around the world since the global financial crisis, there is a lack of empirical evidence on whether and how these pro- grams affect the real economy. Using rich borrower-linked mortgage-market data, we document that there is a “flypaper effect” of LSAPs, where the transmission of unconventional monetary policy to interest rates and (more importantly) origination volumes depends crucially on the assets purchased and degree of segmentation in the market. For example, QE1, which involved significant purchases of GSE-guaranteed mortgages, increased GSE-eligible mortgage origina- tions significantly more than the origination of GSE-ineligible mortgages. In contrast, QE2’s focus on purchasing Treasuries did not have such differential effects. We find that the Fed’s purchase of MBS (rather than exclusively Treasuries) during QE1 resulted in an additional $600 billion of refinancing, substantially reducing interest payments for refinancing households, lead- ing to a boom in equity extraction, and increasing consumption by an additional $76 billion. This de facto allocation of credit across mortgage market segments, combined with sharp bunch- ing around GSE eligibility cutoffs, establishes an important complementarity between monetary policy and macroprudential housing policy. Our counterfactual simulations estimate that re- laxing GSE eligibility requirements would have significantly increased refinancing activity in response to QE1, including a 35% increase in equity extraction by households. -

Revisiting Stimulus and the Great Recession

The Daily Dish Revisiting Stimulus and the Great Recession DOUGLAS HOLTZ-EAKIN | OCTOBER 21, 2020 Eakinomics: Revisiting Stimulus and the Great Recession There has been a steady drumbeat of calls for additional “stimulus” to counter the fallout of the COVID-19 recession. I want to stipulate that I think the case can be made for an appropriately structured fiscal bill, but the case is not being made in a compelling fashion. A key part of the argument has been that stimulus got cut off after the 2008-09 recession and doomed the economy to slow growth. A New York Times article, entitled “ Why the U.S. Risks Repeating 2009’s Economic Stimulus Mistakes,” is typical. “‘The initial response was good, but we need more,’ said Karen Dynan, who was chief economist at the Treasury Department in the Obama administration and now teaches at Harvard. The decision to pull back on spending a decade ago, she said, ‘really prolonged the period of weakness after the great recession.’” (This argument is most often made by former Obama Administration officials.) Maybe. But maybe there is another lesson from that era. The first is that if you are going to do fiscal stimulus, do fiscal stimulus. The American Recovery and Reinvestment Act (ARRA) contained some tax cuts and social safety net transfers of the typical stimulus ilk. But it contained a slew of provisions – e.g., health services information technologies and green investments – that were transformative in nature and core parts of the Obama domestic agenda. Transformation is not stimulus, which is just putting back in place what was previously there.