Our Annual Results for the Year Ended 31 March 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

March 29 2016 NEWS RELEASE PALOMA SELECTS ST DAVID's

March 29 2016 NEWS RELEASE PALOMA SELECTS ST DAVID’S FOR ITS WELSH DEBUT The St David’s Partnership, owners of St David’s in Cardiff, one of the UK’s premier retail and leisure destinations, has today announced that Paloma, the independent Italian fashion brand, has opened its first store in Wales at the centre. The 2,000 sq ft Paloma boutique is located on St David’s Grand Arcade, opposite The White Company, and officially launched on March 25. Designed by an in-house team, the store will feature Paloma’s trademark Italian designer womenswear and accessory collections. Currently trading from a store in Brighton, St David’s marks the beginning of an expansion plan for the brand, as it targets key locations in the UK to create a select number of flagship stores. This follows a successful year for the St David’s Partnership, a joint venture between intu and Land Securities, which secured over 90,000 sq ft of lettings and a number of key store openings last year, including the largest H&M store in the UK. Speaking on behalf of the St David’s Partnership, Colin Flinn, regional director at intu, said: “Paloma is a very strong addition to St David’s line-up, adding to the mix of independent retailers that complement the major high street brands. Our strategy of developing St David’s mix in this way ensures the centre remains not only the number one retail and leisure destination in Wales, but one of the most in-demand centres in the country.” Mandhir Shukla, operations director of Paloma added: “St David’s, Cardiff is a fantastic opportunity for Paloma. -

Download Our Operating and Portfolio Review

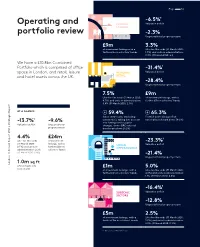

Page 36 -6.5%1 Operating and CENTRAL Valuation deficit LONDON portfolio review -2.3% Ungeared total property return £9m 3.3% of investment lettings with a Like-for-like voids (31 March 2020: further £1m in solicitors’ hands 1.3%) and units in administration: 0.3% (31 March 2020: nil) We have a £10.8bn Combined Portfolio which is comprised of office -31.4%1 space in London, and retail, leisure REGIONAL Valuation deficit and hotel assets across the UK. RETAIL -28.4% Ungeared total property return 7.5% £9m Like-for-like voids (31 March 2020: of investment lettings, with a 4.7%) and units in administration: further £7m in solicitors’ hands 5.8% (31 March 2020: 2.1%) AT A GLANCE 59.4% 65.3% Same centre sales (excluding Footfall down (ShopperTrak ¹ automotive), taking into account national benchmark down 58.2%) -13.7% -9.6% new lettings and occupier Valuation deficit Ungeared total changes, down (BRC national » Strategic Report property return benchmark down 29.2%) 4.4% £24m Like-for-like voids of investment -23.3%1 (31 March 2020: lettings, with a URBAN Valuation deficit 2.5%) and units in further £12m in OPPORTUNITIES administration: 2.2% solicitors’ hands (31 March 2020: 0.8%) -21.4% Ungeared total property return 1.0m sq ft Landsec // AnnualLandsec Report // 2021 of developments £1m 5.0% now on site of investment lettings, with a Like-for-like voids (31 March 2020: further £1m in solicitors’ hands 4.8%) and units in administration: 1.1% (31 March 2020: 0.4%) -16.4%1 SUBSCALE Valuation deficit SECTORS -12.8% Ungeared total property return £5m 2.5% of investment lettings, with a Like-for-like voids (31 March 2020: further £3m in solicitors’ hands 2.0%) and units in administration: 2.9% (31 March 2020: 0.9%) 1. -

Lewisham Town Centre Local Plan Submission Version

Lewisham local plan Lewisham town centre local plan Submission version September 2012 PLEASE NOTE: The maps and figures within this document will be professionally altered for the final publication version. Contents 1 The plan and context 3 1.1 Lewisham town centre and the Local Plan 4 1.2 Key characteristics of Lewisham town centre 6 1.3 Summary of issues and challenges for the town centre 11 1.4 How does the LTC Local Plan relate to other policy? 12 1.5 Sustainability Appraisal and Equalities Analysis Assessment 15 2 Vision and objectives 16 2.1 The vision 17 2.2 The objectives 18 2.3 From issues to objectives 20 3 Presumption in favour of sustainable development 22 4 The spatial strategy 24 4.1 The plan boundaries 25 4.2 Introducing policy areas and sites 27 4.3 Creating a cohesive and complete town centre experience 32 5 Policy Areas and sites 37 5.1 Lewisham Gateway Policy Area 37 5.2 Loampit Vale Policy Area 41 5.3 Conington Road Policy Area 46 5.4 Lee High Road Policy Area 51 5.5 Ladywell Policy Area 55 5.6 Central Policy Area 60 6 Area-wide policies 66 6.1 Growing the local economy 67 6.1.1 Employment 69 6.1.2 Housing 73 6.1.3 Shopping 76 6.2 Building a sustainable community 84 6.2.1 Urban design 85 Lewisham TCLP Adoption Version Contents 6.2.2 Sustainable movement 89 6.2.3 Community 95 6.3 Environmental management 100 7 Implementation, monitoring and risk 106 7.1 Implementation 107 7.2 Monitoring 111 7.3 Risk 113 8 Appendix 1 - Policy, guidance and evidence base linkages 115 9 Appendix 2 - Heritage assets 122 10 Appendix 3 - Delivery strategy and monitoring framework 125 11 Appendix 4 - Lewisham town centre infrastructure schedule 134 12 Appendix 5 - UDP proposals replaced by the LTCLP 143 13 Glossary 144 Lewisham TCLP Adoption Version The plan and context 1 Section 1 of the Lewisham Town Centre Local Plan (LTCLP) firstly introduces Lewisham town centre, its strengths, weaknesses and the opportunities for it to develop and improve in the next five to ten years. -

1. Entering Into a Competition Or Promotion Hosted by Us

PRIVACY & COOKIES POLICY This Privacy Notice may vary from time to time so please check it regularly. This Notice describes the types of information collected, how that information is used and disclosed, and how you can access, modify, or delete your information. Land Securities Properties Limited (company number 961477) whose registered office is at 100 Victoria Street London SW1E 5JL (“we”, “us” or “our”) is the ‘data controller’ for the personal data we collect. We are registered with the Information Commissioner’s Office with registration number Z5806812. 1. WIFI IN OUR CENTRES Please see (wifi Link) 2. MARKETING AND GUEST SERVICES HOW DO WE COLLECT INFORMATION ABOUT YOU? 1. Entering into a competition or promotion hosted by us or our third parties: You may provide us with personal data when you subscribe to these services either online or through a physical form. 2. Enrolling for a loyalty card or a club run at our centres: you will typically provide us with your name and contact details when you enrol for a loyalty card either online or through a physical form. 3. Feedback: providing feedback to us through our online surveys where you may provide your contact details and subscribe to receiving marketing information. Our main supplier for this service is Privacy Shield accredited and based in the United States so your data will be transferred securely and legally outside of the UK. You can also provide us feedback through writing to or emailing the centre with any comments, complaints or suggestions. 4. Website usage: We may also collect information from you automatically when you access and use our Online Services, including the time and duration of your visit, the referring URL, your Internet Protocol (IP) or MAC address, the type of device you use and its operating system. -

Limited and Guild Realisations Limited (Formerly Republic (Retail) Limited) - Both in Administration (Together ‘The Companies’)

Ernst & Young LLP 1 Bridgewater Place, Water Lane Leeds LS11 5QR T el: 0113 298 2200 Fax: 0113 298 2201 www.ey.com/uk TO ALL KNOWN CREDITORS 8 April 2013 Ref: RHK/JPS/TRJ/AE/PCF11.1 Direct line: 0113 298 2496 Direct fax: 0113 298 2206 Email: [email protected] Dear Sirs Republic (UK) Limited and Guild Realisations Limited (formerly Republic (Retail) Limited) - both in Administration (together ‘the Companies’) Further to my appointment as Joint Administrator of the Companies, I attach a copy of my statement of proposals in accordance with paragraph 49 of Schedule B1 to the Insolvency Act 1986. As you will note from the proposals, there is no prospect of any funds becoming available to unsecured creditors of either of the Companies other than by virtue of the prescribed part. As a consequence, I do not propose to summon meetings of creditors. If, however, creditors whose debts amount to at least 10% of total debts of either of the Companies make a request in the prescribed form within 8 business days of these proposals being sent out, a meeting will be held in that company. Copies of the prescribed form (Form 2.21B) are enclosed in case you wish to request a meeting. I would draw your attention to the provisions of Rule 2.37 of the Insolvency Rules 1986 which provide that if a meeting is requested, it will only be held if the expenses of summoning and holding such a meeting are paid by the creditor or creditors making the request and if security is first deposited with me for payment. -

Leeds BID Feasibility Study

Leeds BID Feasibility Study Detailed Report February 2014 Leeds Business Improvement District Feasibility Study 11 1.0 Introduction and Executive 2.0 Business Improvement Districts Summary Detailed report 2.0 Business Improvement Districts “The growth rate of BIDs continues to rise and the ballot success rate remains high at 84% overall, and 3.0 Leeds City Centre 91% for renewal ballots demonstrating that this is a tool that the business community is seeing real value 4.0 Consultation from. The scale and reach of BIDs is now significant with close to 70,000 businesses paying levies across 5.0 BID Boundary and Levy options the country and a total investment in BID areas 6.0 Recommendations and of almost £100 million annually”. – British BIDs 2013 Nationwide Survey next steps 7.0 Risks and issues Appendices History of BIDs 22 *BIDs around the world BIDs in the UK and Ireland . BIDs were first established in North America in the mid-1960s . In 2004 legislation for the creation of BIDs was . Since then more than 1,500 BIDs have been introduced in England, and later in Scotland, adopted in many countries around the world Wales and Ireland including: . Since then more than 170 BIDs have been created including those in London, Birmingham, – 450 United States Manchester and Edinburgh – 350 Canada – 185 Australia . Each BID proposal is different depending on – 140 New Zealand local needs and priorities, but usually focus on: – 260 Japan – 40 South Africa – Safety and security – 225 European countries – Cleaning and maintenance – Events and marketing – Retail and evening economy – Access and signage *source www.britishbids.info How BIDs work 33 A BID is defined by a geographical area where partners pull together to create a better place to live and work. -

Tall Buildings Study Draft

LEWISHAM TALL BUILDINGS STUDY DRAFT LONDON BOROUGH OF LEWISHAM Allies and Morrison Urban Practitioners February 2021 D R A F T D R A F T CONTENTS 1 INTRODUCTION AND CONTEXT 5 4 SENSITIVITY ASSESSMENT 53 1.1 Introduction, Purpose and Structure of the Study 5 4.1 Introduction 53 1.2 Introduction to The Borough 6 4.2 Assessment of Sensitivity 54 1.3 Tall Building Policy Context 7 4.3 World Heritage Sites 56 1.4 Other Relevant Guidance 10 4.4 Conservation Areas and Special Local Character 58 4.5 Listed Buildings 60 2 DEFINING WHAT IS TALL 15 4.6 Strategic and Local Views And Landmarks 62 2.1 Lewisham Borough Definition for Tall Buildings 15 4.7 Areas Characterised by Consistent Building Heights 64 2.2 Lewisham Borough Definition for Taller Buildings 15 4.8 Topography 66 2.3 Building Heights 16 4.9 Tall Building Sensitivity Map 68 2.4 Existing and Proposed Tall Buildings 18 4.10 Site Allocations 70 2.5 Average Building Heights by Area 20 2.6 Average Building Heights by Neighbourhood 22 2.7 Average Building Heights Area Analysis 24 2.8 Building Height Variance 25 2.9 Prevailing Heights 26 2.10 What is Tall 26 3 SUITABILITY ASSESSMENT 29 3.1 Introduction 29 3.2 Assessment of Suitability 30 3.3 High PTAL 32 3.4 Bakerloo Line Extension 34 3.5 Town Centres 36 3.6 Opportunity Areas 38 3.7 Growth Areas 40 3.8 Building Heights and Tall Building Clusters 42 3.9 Tall Building Suitability Map 44 3.10 Green, Open Space and Rivers 46 3.11 Cycling Transport Accessibility Level (CTAL) 48 3.12 Site Allocations 50 D R A F T D R A F T DRAFT LB LEWISHAM TALL -

96 Lewisham High Street, Lewisham London SE13 5JH

www.acuitus.co.uk lot 2 96 Lewisham High Street, Lewisham London SE13 5JH Rent Freehold Retail Investment • Entirely let to RAL Limited (t/a Quicksilver) • Nearby occupiers include Vodafone, £44,500 until 2028 Barclays Bank, Subway and Greggs per annum • Recently re-geared lease • 40 metres from Lewisham Shopping Centre exclusive • Prominent town centre position • Six Week Completion Available Ref: 4407/GT/WH PA: AS Location Description Miles: 1.4 miles south of Greenwich The property comprises a ground floor retail unit with office/storage 2 miles west of Blackheath Village accommodation on the first and second floors and a third floor attic 6 miles south-east of the City of London area which is currently unuseable. N Roads: A20, A21 Rail: Lewisham Rail (direct to Charing Cross & Cannon Street), Tenure Lewisham DLR (19 minutes to Canary Wharf) Freehold. Air: London City Airport VAT Situation VAT is not applicable to this lot. The property is situated in a prominent position on the western side of the pedestrianised High Street, close to its junction with Lee High Road. The property is situated 40 metres from an entrance to Lewisham Shopping Centre which houses retailers including Marks & Spencer, TK Maxx, BHS, H & M, Next, New Look and Boots Chemist. Other nearby occupiers include Vodafone, Barclays Bank, Subway and Greggs. Tenancy and accommodation Floor Use Floor Areas (Approx) Tenant Term Rent p.a.x. Reviews Ground Retail 118.64 sq m (1,277 sq ft) RAL LIMITED (1) 16 years and 17 days from £44,500 29/05/2017 First Office/Storage 48.62 sq m (523 sq ft) (t/a Quicksilver) 29/05/2012 until 14/06/2028 on a and LEWISHAM SHOPPING CENTRE Second Office 21.34 sq m (230 sq ft) full repairing and insuring lease 29/05/2022 Third Not Measured Totals 188.60 sq m (2,030 sq ft) £44,500 (1) As of 19th January 2012, RAL Ltd have a Dun & Bradstreet Rating of 4A1, showing minimum risk. -

Lewisham Local Plan Site Allocations – Central Area

Draft Lewisham Local Plan Site Allocations – Central area Regulation 18 stage ‘Preferred Approach’ Document Lewisham Gateway Site address: Lewisham Gateway Site, Lewisham High Street, London, SE13 Site details: Site size (ha): 5.52, Setting: Central, PTAL: In 2015: 6b, In 2021: 6b, In 2031: 6b, Ownership: Mixed public and private, Current use: Transport interchange How site was Lewisham Core Strategy (2011) and London SHLAA (2017) identified: Planning Opportunity Area, adjacent to Conservation Area, Critical Drainage Area, designations Flood Zones 1 and 2 and site constraints: Planning Full application DC/06/062375 granted in May 2009. Various reserved matters and Status: s73 minor material amendment granted April 2013 – February 2019. Started construction and development is partially complete. Timeframe for 2020/21 – 2024/25 2025/26 – 2029/30 2030/31 – 2034/35 2035/36 – 3039/40 delivery: Yes Indicative Net residential units: Non-residential floorspace: development 607 Town centre: 2,550 capacity: 1 Employment: 17,500 Existing planning consent DC/06/062375 - The comprehensive mixed use redevelopment of the Lewisham Gateway Site, SE13 (land between Rennell Street and Lewisham Railway Station) for 100000m² comprising retail (A1, A2, A3, A4 and A5), offices (B1), hotel (C1), residential (C3), education/health (D1) and leisure (D2) with parking and associated infrastructure, as well as open space and water features as follows: up to 57,000 m² residential (C3) up to 12,000 m² shops, financial & professional services (A1 & A2) up to 17,500 m² offices (B1) / education (D1) up to 5,000 m² leisure (D2) up to 4,000 m² restaurants & cafés and drinking establishments (A3 & A4) up to 3,000 m² hotel (C1) up to 1,000 m² hot food takeaways (A5) 500m² health (D1) provision of up to 500 car parking spaces revised road alignment of (part of) Lewisham High Street, Rennell Street, Molesworth Street and Loampit Vale and works to Lewisham Road. -

June 2018 • £8.00 Tipping Point for Landfill

SHOPPINGCENTREThe business of retail destinations www.shopping-centre.co.uk June 2018 • £8.00 Tipping point for landfill Technology diverts food waste from landfill 10 Development 12 Sustainability 17 Parking Intu Watford Centres face food Global tech alliance nears completion waste challenge to streamline parking The Highcross Beacons, @HXBeacons Creative LED solutions to make spaces and places memorable. ADI design content-driven experiences and exceptional digital installations that deliver the unexpected. We combine giant LED platforms with larger-than-life creative to drive large scale IRKEKIQIRXERHMRXIVEGXMSR8SƼRHSYX more visit www.adi.tv/shoppingcentre For more information visit www.adi.tv/shoppingcentre 0800 592 346 | [email protected] | www.adi.tv CONTENTS Editor’s letter Editor Graham Parker 07956 231 078 Fraser is widely forecast to be Wolfson has complained that [email protected] next, with as many as 30 stores a two-tier market is emerging Editorial Assistant earmarked for closure. with retailers paying widely dif- Iain Hoey However the CVA is a form ferent rents for adjacent stores 07757 946 414 of insolvency and the question depending on whether or not [email protected] has to be asked whether these they have been through a CVA. Sales Manager businesses are in fact insolvent. He’s now inserting CVA clauses Trudy Whiston In the end that’s a decision for into leases allowing Next to 01293 416 090 [email protected] lawyers and accountants and claim a rent cut if a neighbour- not magazine editors, but the ing brand wins one through a Database Manager At last there are signs that land- suspicion is that companies CVA. -

REGISTER of MEMBERS' FINANCIAL INTERESTS As at 6

REGISTER OF MEMBERS’ FINANCIAL INTERESTS as at 6 June 2016 _________________ Abbott, Ms Diane (Hackney North and Stoke Newington) 1. Employment and earnings Fees received for co-presenting BBC’s ‘This Week’ TV programme. Address: BBC Broadcasting House, Portland Place, London W1A 1AA. (Registered 04 November 2013) 14 May 2015, received £700. Hours: 3 hrs. (Registered 03 June 2015) 4 June 2015, received £700. Hours: 3 hrs. (Registered 01 July 2015) 18 June 2015, received £700. Hours: 3 hrs. (Registered 01 July 2015) 16 July 2015, received £700. Hours: 3 hrs. (Registered 07 August 2015) 8 January 2016, received £700 for an appearance on 17 December 2015. Hours: 3 hrs. (Registered 14 January 2016) 28 July 2015, received £4,000 for taking part in Grant Thornton’s panel at the JLA/FD Intelligence Post-election event. Address: JLA, 14 Berners Street, London W1T 3LJ. Hours: 5 hrs. (Registered 07 August 2015) 23rd October 2015, received £1,500 for co-presenting BBC’s “Have I Got News for You” TV programme. Address: Hat Trick Productions, 33 Oval Road Camden, London NW1 7EA. Hours: 5 hrs. (Registered 26 October 2015) 10 October 2015, received £1,400 for taking part in a talk at the New Wolsey Theatre in Ipswich. Address: Clive Conway Productions, 32 Grove St, Oxford OX2 7JT. Hours: 5 hrs. (Registered 26 October 2015) 21 March 2016, received £4,000 via Speakers Corner (London) Ltd, Unit 31, Highbury Studios, 10 Hornsey Street, London N7 8EL, from Thompson Reuters, Canary Wharf, London E14 5EP, for speaking and consulting on a panel. -

Immersive Experiences the Future of the Shopping Centre Retailweek Connect Reports

RetailWeek CONNECT In association with REPORTS Immersive experiences The future of the shopping centre RetailWeek CONNECT REPORTS RETAIL WEEK FOREWORD JameS KNOWLES HEAD OF COMMERCIAL CONTENT OPERATIONS oday’s consumer buys into new set of criteria; does this centre offer experiences. Not just within the the immersive experience the modern stores they visit, but also from customer wants? Retailers have to base retail destinations themselves. Understanding this is key. What store openings on a TAs a result UK shopping centres do today’s consumers expect from the are rising to the challenge by giving experience shopping centres provide? new set of criteria consumers more reasons than just retail And how will these expectations evolve? to pay a visit. What are centres doing, and what can they – does this centre Look no further than intu. The do, to meet these demands? offer the experience shopping centre operator will open its To find out, this Retail Week report, first Nickelodeon park at intu Lakeside, produced in association with intu, has consumers expect? strengthening its appeal to the family- surveyed a nationally representative pool day-out market. of 2,000 UK consumers to find out. This is a clear indication that shopping Over the coming pages we will reveal centres are about much more than simply how the shopping centre landscape has shopping. changed, bringing you the exclusive While not every centre is going to insights from our survey, identifying feature an all-singing, all-dancing fun examples of centres leading the way, and park, it does mean retailers now have to arming retailers with key takeaways on base store-opening decisions on a whole what they need to consider.