(Net)I Fell -16.30%

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Investor Presentation

Ross Stores, Inc. Investor Overview March 2020 Disclosure of Risk Factors Forward-Looking Statements: This presentation contains forward-looking statements regarding expected sales, earnings levels, new store growth opportunity, and other financial results in future periods that are subject to risks and uncertainties which could cause our actual results to differ materially from management’s current expectations. The words “plan,” “expect,” “target,” “anticipate,” “estimate,” “believe,” “forecast,” “projected,” “guidance,” “outlook,” “looking ahead,” and similar expressions identify forward-looking statements. Risk factors for Ross Dress for Less® (“Ross”) and dd’s DISCOUNTS® include without limitation, competitive pressures in the apparel or home-related merchandise retailing industry; changes in the level of consumer spending on or preferences for apparel and home-related merchandise; market availability, quantity, and quality of attractive brand name merchandise at desirable discounts and our buyers’ ability to purchase merchandise that enables us to offer customers a wide assortment of merchandise at competitive prices; impacts from the macro-economic environment, financial and credit markets, geopolitical conditions, or public health issues (such as pandemics); our ability to continually attract, train, and retain associates to execute our off-price strategies; unseasonable weather that may affect shopping patterns and consumer demand for seasonal apparel and other merchandise, and may result in temporary store closures and disruptions -

Ross Stores, Inc. Corporate Social Responsibility Table of Contents

Ross Stores, Inc. Corporate Social Responsibility Table of Contents Corporate Social Responsibility ............................................................................................................................... 3 Empowering Our Associates ....................................................................................................................................... 4 Training and Development Programs ...................................................................................................................................... 5 Advancement Opportunities ........................................................................................................................................................... 5 A Commitment to Diversity .............................................................................................................................................................. 6 Volunteering in the Community .................................................................................................................................................... 6 A Scholarship Program for Associates and Their Dependents ............................................................................... 7 Competitive Benefits and Total Rewards Package ......................................................................................................... 7 Providing a Safe Work Environment ........................................................................................................................................ -

Schedule 14A

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant [X] Filed by a Party other than the Registrant [ ] Check the appropriate box: [ ] Preliminary Proxy Statement [ ] Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) [X] Definitive Proxy Statement [ ] Definitive Additional Materials [ ] Soliciting Material Pursuant to §240.14a-12 ROSS STORES, INC. (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): [X] No fee required. [ ] Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. 1 Title of each class of securities to which transaction applies: 2 Aggregate number of securities to which transaction applies: Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing 3 fee is calculated and state how it was determined): 4 Proposed maximum aggregate value of transaction: 5 Total fee paid: [ ] Fee paid previously with preliminary materials. [ ] Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. 1 Amount Previously Paid: 2 Form, Schedule or Registration Statement No.: 3 Filing Party: 4 Date Filed: April 9, 2019 Dear Stockholder: You are cordially invited to attend the 2019 Ross Stores, Inc. -

P-Card Transparency Report

Company Name SC SPARTANBURG SCH DIS 7 Post Date Between 2020-07-28 00:00:00 and 2020-08-27 00:00:00 P-card Transparency Report - Report Owner Blanton, Shannon Final Report Time 2020-09-29 14:26:00 Transaction Type One of: Cash advance or Misc Credit or Misc Debit or Purchase or Payment Purchase Date Amount Vendor Name MCC Description 07/27/2020 3.96 LOWES #02548 HOME SUPPLY WAREHOUSE STORES 07/27/2020 180.28 UNITED REFRIG INC 490 COMMERCIAL EQUIPMENT, NOT ELSEWHERE CLAS 07/27/2020 6.03 NAPA STORE 1074025 AUTOMOTIVE PARTS, ACCESSORIES STORES 07/27/2020 194.55 TUCKER MATERIALS INC LUMBER AND BUILDING MATERIALS STORES 07/27/2020 5.50 NAPA STORE 1074025 AUTOMOTIVE PARTS, ACCESSORIES STORES 07/27/2020 681.60 GRAPHIC PRODUCTS INC DURABLE GOODS,NOT ELSEWHERE CLASSIFIED 07/27/2020 42.03 LOWES #02548 HOME SUPPLY WAREHOUSE STORES 07/27/2020 74.02 LOWES #02548 HOME SUPPLY WAREHOUSE STORES 07/27/2020 245.51 SMITH TURF & IRRIGATION - COMMERCIAL EQUIPMENT, NOT ELSEWHERE CLAS 07/28/2020 58.19 UNITED REFRIG INC 490 COMMERCIAL EQUIPMENT, NOT ELSEWHERE CLAS 07/28/2020 12.71 WM SUPERCENTER #1281 GROCERY STORES, SUPERMARKETS 07/28/2020 27.78 O'REILLY AUTO PARTS 1940 AUTOMOTIVE PARTS, ACCESSORIES STORES 07/28/2020 20.01 8160 ALL-PHASE ELECTRICAL PARTS AND EQUIPMENT 07/28/2020 52.23 UNITED REFRIG INC 490 COMMERCIAL EQUIPMENT, NOT ELSEWHERE CLAS 07/28/2020 38.86 LOWES #02548 HOME SUPPLY WAREHOUSE STORES 07/28/2020 21.85 LOWES #02548 HOME SUPPLY WAREHOUSE STORES 07/28/2020 53.49 GOOGLE YouTube TV DIGITAL GOODS - APPS (EXCLUDES GAMES) 07/28/2020 277.28 O'REILLY -

Costar Regional Sales Director – Seattle, WA

Real Estate Career Opportunities After many years in the corporate real estate business, we are networked well to learn of new career opportunities that arise. Clients of ours use our network to learn of jobs available in the real estate industry and to help spread the word when they have positions open. This is a service open only to clients or prospective clients. On a regular basis we update job listings we are aware of. Become a client or prospective client and we’ll keep you updated on terrific real estate career opportunities in the U.S. and internationally. Call us for more information. Eddie Bauer Director of Real Estate – Bellevue, WA King County Real Estate Services Section Manager – Seattle, WA CoStar Regional Sales Director – Seattle, WA CoStar Account Executive – Seattle, WA Microsoft Area Portfolio Manager – Redmond, WA Hopelink Associate Director of Facilities – Redmond, WA T-Mobile Director, Programs & Services (CRE) – Bellevue, WA SKB Companies Asset Manager – Portland, OR Harsch Investment Properties Real Estate Development Manager – Portland, OR CoStar Regional Sales Director – Portland, OR Callan Associates Real Asset Associate – San Francisco, CA Digital Realty Trust Director of Global Sales Operations – San Francisco, CA Holliday Fenoglio Fowler, LP Real Estate Analyst – San Francisco, CA Level 3 RE Business Development Specialist – San Francisco, CA Levi Director, Americas Store Design – San Francisco, CA Prudential Director - Asset Manager, CRE – San Francisco, CA Robert Half International RE Operations Manager -

National Chains & Retailers

National Chains & Retailers - Santee, CA Feb. 2021 Inventory of National Chains- by industry category [168 total] Apparel & Accessories Bus Svcs Supl (cont.) Electronics/Ent. (cont) Hotels & Hosp. Svcs. ▪DSW ▪Postal Annex [2] ▪Cox Communications ▪Best Western ▪Famous Footwear ▪RE/MAX ▪Gamestop ▪Rodeway Inn ▪Old Navy ▪SERVPRO ▪Radio Shack Express ▪WoodSpring Suites [coming] ▪Skechers ▪Sharp Business Syst. ▪T Mobile ▪Tilly's ▪State Farm Insurance ▪uBreakiFix Specialty Retail & Services ▪The UPS Store ▪Verizon ▪Banfield Pet Hosp Automotive ▪Barnes & Noble ▪76 / Conoco Phillips Childcare/Educ. Enrichmt. General Merchandise ▪BevMo ▪Arco ▪KinderCare Learning ▪99¢ Only ▪HobbyTown ▪Auto Zone ▪Mathnasium ▪Costco Wholesale ▪Michael's Arts & Crafts ▪Budget Truck Rental ▪Montessori Charter Sch. ▪Dollar Tree [2] ▪Molly Maid ▪Bumper Doc ▪Tutor Time Learning ▪Kohl's ▪Party City ▪Chevron ▪Ross Stores ▪Petco ▪Discount Tire Dining & Food Specialties ▪Target ▪PetSmart ▪Enterprise Rent-A-Car ▪Baskin Robbins ▪T.J. Maxx ▪Thrive Vet Care ▪ExxonMobil ▪Buffalo Wild Wings ▪Walmart ▪Firestone Auto Care ▪Carl's Jr. Restaurant ▪Hertz Rent-A-Car ▪Chick-fil-A Grocers & Pharmacies ▪O'Reilly Auto Parts ▪Chili's ▪7-Eleven [6] National Chains ▪Penske Truck Rental ▪Chipotle Mexican Grill ▪Circle K Added Since 2015 - - ▪Pep Boys ▪Cold Stone Creamery ▪CVS Pharmacy ▪Service King ▪Dairy Queen ▪Food 4 Less/Kroger ♦Club Pilates ▪Sparks Cmp. Car Care ▪Del Taco ▪Grocery Outlet ♦Eyeglass World ▪Tire Choice ▪Denny's Restaurant ▪Smart & Final Extra ♦Lumber Liquidators ▪Toyota Certified Center ▪Domino's Pizza ▪Sprouts Market ♦Grocery Outlet ▪U-Haul ▪Einstein Bros. Bagels ▪Vons ♦Baskin Robbins ▪USA Gasoline ▪El Pollo Loco ▪Walgreens ♦Movement Mortgage ▪Handel's Ice Crm [coming] ♦CosmoProf Banks & Credit Unions ▪In N Out Health & Fitness ♦Smart & Final Extra ▪Bank of America ▪Int. -

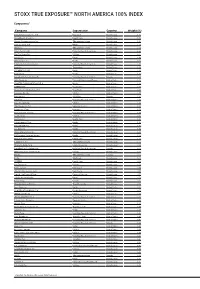

Stoxx True Exposure™ North America 100% Index

STOXX TRUE EXPOSURE™ NORTH AMERICA 100% INDEX Components1 Company Supersector Country Weight (%) Berkshire Hathaway Inc. Cl B Insurance United States 4.96 UnitedHealth Group Inc. Health Care United States 4.79 Verizon Communications Inc. Telecommunications United States 4.10 Comcast Corp. Cl A Media United States 3.38 AT&T Inc. Telecommunications United States 3.08 Union Pacific Corp. Industrial Goods & Services United States 2.22 NextEra Energy Inc. Utilities United States 2.22 Lowe's Cos. Retail United States 1.86 Wells Fargo & Co. Banks United States 1.56 Fidelity National Information Industrial Goods & Services United States 1.49 Intuit Inc. Technology United States 1.28 CVS HEALTH CORP. Retail United States 1.28 Target Corp. Retail United States 1.24 Canadian National Railway Co. Industrial Goods & Services Canada 1.23 Altria Group Inc. Personal & Household Goods United States 1.21 CHARTER COMMUNICATIONS CL.A Media United States 1.20 ANTHEM INC Health Care United States 1.09 Crown Castle International Cor Real Estate United States 1.09 Dominion Energy Utilities United States 1.07 Enbridge Inc. Oil & Gas Canada 1.01 CSX Corp. Industrial Goods & Services United States 1.00 Duke Energy Corp. Utilities United States 1.00 CME Group Inc. Cl A Financial Services United States 0.99 Progressive Corp. Insurance United States 0.93 Norfolk Southern Corp. Industrial Goods & Services United States 0.93 Southern Co. Utilities United States 0.92 Humana Inc. Health Care United States 0.87 Truist Financial Corp Banks United States 0.87 DOLLAR GENERAL Retail United States 0.86 U.S. -

Ross Dress for Less Leasehold Interest OFFERING MEMORANDUM San Jose, California (San Francisco Bay Area) E

Ross Dress For Less Leasehold Interest OFFERING MEMORANDUM San Jose, California (San Francisco Bay Area) E. Capitol Expressway Location Net Lease Investment Services CUSHMAN & WAKEFIELD Andrew Bogardus Christopher Sheldon 201 California Street, Suite 800 +1 415 677 0421 +1 415 677 0441 San Francisco, CA 94111 [email protected] [email protected] Lic #00913825 Lic #01806345 www.thinknnn.com Net Lease Investment Services Disclaimer The information contained in this marketing brochure (“Materials”) is The information contained in the Materials has been obtained by proprietary and confidential. It is intended to be reviewed only by the Agent from sources believed to be reliable; however, no representation person or entity receiving the Materials from Cushman & Wakefield or warranty is made regarding the accuracy or completeness of the (“Agent”). The Materials are intended to be used for the sole purpose of Materials. Agent makes no representation or warranty regarding the preliminary evaluation of the subject property/properties (“Property”) Property, including but not limited to income, expenses, or financial for potential purchase. performance (past, present, or future); size, square footage, condition, or quality of the land and improvements; presence or absence of The Materials have been prepared to provide unverified summary contaminating substances (PCB’s, asbestos, mold, etc.); compliance with financial, property, and market information to a prospective purchaser laws and regulations (local, state, and federal); or, financial condition to enable it to establish a preliminary level of interest in potential or business prospects of any tenant (tenants’ intentions regarding purchase of the Property. The Materials are not to be considered continued occupancy, payment of rent, etc). -

O'reilly Automotive, Inc 2008 Proxy Statement

March 23, 2012 Dear Shareholder: You are cordially invited to attend the 2012 Annual Meeting of Shareholders of O’Reilly Automotive, Inc. to be held at the Doubletree Hotel Springfield, 2431 North Glenstone Avenue, Springfield, Missouri 65803, on Tuesday, May 8, 2012, at 10:00 a.m. central time. Details of the business to be conducted at the Annual Meeting are given in the attached Notice of Annual Meeting of Shareholders and Proxy Statement. In addition to the specific matters to be acted upon, there will be a report on the progress of the Company and an opportunity for questions of general interest to the shareholders. It is important that your shares be represented at the meeting. Whether or not you plan to attend in person, please complete, sign, date and return the enclosed proxy card in the envelope provided at your earliest convenience or vote via telephone or Internet using the instructions on the proxy card. If you attend the meeting, you may vote your shares in person even if you have previously signed and returned your proxy. In order to assist us in preparing for the Annual Meeting, please let us know if you plan to attend by contacting Tricia Headley, our Corporate Secretary, at 233 South Patterson Avenue, Springfield, Missouri 65802, (417) 874-7161. We look forward to seeing you at the Annual Meeting. David E. O’Reilly Chairman of the Board O’REILLY AUTOMOTIVE, INC. 233 South Patterson Avenue Springfield, Missouri 65802 NOTICE OF ANNUAL MEETING OF SHAREHOLDERS To be held on May 8, 2012 Springfield, Missouri March 23, 2012 The Annual Meeting of Shareholders (“Annual Meeting”) of O’Reilly Automotive, Inc. -

California-Based Most Penalized Parent Companies.Xlsx

parent_name ownership stock ticker major_industry Penalty Rank Total Penalties Number of Cases Wells Fargo publicly traded WFC financial services 4 $205,403,723 24 Oracle publicly traded ORCL information technology 20 $92,268,000 10 24 Hour Fitness privately held miscellaneous services 31 $55,448,500 2 Electronic Arts publicly traded EA entertainment 48 $31,285,000 3 Kaiser Permanente non-profit healthcare services 57 $27,757,368 9 Smart & Final Stores publicly traded SFS retailing 58 $27,400,000 3 Children's Hospital Los Angeles non-profit healthcare services 59 $27,000,000 1 Leonard Green & Partners privately held private equity (including portfolio companies) 60 $26,082,979 11 Robert Half International publicly traded RHI business services 76 $19,615,000 2 PG&E Corp. publicly traded PCG utilities and power generation 90 $17,327,748 2 Jack in the Box Inc. publicly traded JACK restaurants and foodservice 92 $17,300,000 2 Ares Management publicly traded ARES private equity (including portfolio companies) 106 $15,182,970 11 KPC Healthcare privately held healthcare services 113 $14,500,000 1 Alphabet Inc. publicly traded GOOG information technology 135 $11,543,907 4 Shippers Transport Express privately held freight and logistics 138 $11,040,000 1 Uber Technologies privately held miscellaneous services 141 $10,750,000 2 Alorica privately held business services 152 $9,991,901 4 CalAmp publicly traded CAMP information technology 186 $8,100,000 1 AECOM publicly traded ACM construction and engineering 189 $7,964,334 26 Rubio's Restaurants privately held restaurants and foodservice 205 $7,500,000 1 Golden Gate Capital privately held private equity (including portfolio companies) 209 $7,188,000 3 Cisco Systems publicly traded CSCO electrical and electronic equipment 218 $6,700,000 1 Giumarra Vineyards privately held beverages 234 $6,110,368 2 AHMC Healthcare privately held healthcare services 235 $6,000,000 1 Hewlett Packard Enterprise publicly traded HPE information technology 257 $5,500,000 1 Gap Inc. -

Accenture Anheuser-Busch ARCADIS, Inc. Bank of America

Employers Who Held Employer-Hosted Events (2019-2020) Accenture Northrop Grumman Anheuser-Busch NorthStar Home ARCADIS, Inc. Parker Hannifin Corporation Bank of America Paylocity Booz Allen Hamilton Procter & Gamble (P&G) Brooks Rehabilitation PwC Camp Starlight Raytheon Citi Schlumberger Cooper & Cooper Real Estate Southern Company Deloitte Consulting Southwestern Advantage Disney Parks and Resorts Synovus Duke Energy Target Edwards Lifesciences Teach For America ExxonMobil Triage Consulting Group Facebook Trillium Trading Fidelity Investments TripAdvisor Flagship Pioneering United Technologies Corporation FlipSetter Collaborate Veeva Systems Gartner Verizon General Electric Visa Inc. Georgia Tech - MS in Quantitative & Volunteer Eco Students Abroad World Fuel Services Computational Finance Program Goldman Sachs Google Harvard Business School Intel Corporation johnson & johnson Kittelson & Associates, Inc. KPMG Kraft Foods Oscar Mayer Foods Division L3Harris Technologies LOCKHEED MARTIN Manhattan Associates McIntire School of Commerce- UVA Minor League Baseball Employers Who Hosted On-Campus Interviews (2019-2020) Abercrombie & Fitch NextEra Energy, Inc. Accenture Nielsen Analog Devices Northrop Grumman Corporation B&R Industrial Automation Corp. OneTrust BDO USA LLP Oracle Corporation Bloomberg LP Parametric Solutions Inc. Chevron Corporation PepsiCo Chewy Pratt & Whitney Precision Castparts Corp. Citrix Procter & Gamble (P&G) Crowe LLP Protiviti Danaher Corporation Raytheon Deloitte S&ME, Inc. E&J Gallo Winery Schlumberger ExxonMobil -

Rockefeller Sent the Letter to the Following Fortune 500 Companies (Listed Below in Alphabetical Order)

Rockefeller sent the letter to the following Fortune 500 companies (listed below in alphabetical order): 3M Becton Dickinson Consolidated Edison Abbot Laboratories Bed Bath & Beyond Con-Way Advance Auto Parts Bemis Core-Mark Holding Advanced Micro Devices Berkshire Hathaway Corn Products International AECOM Technology Best Buy Corning AES Big Lots Costco Wholesale Aetna Biogen Idec Coventry Health Care Aflac BlackRock Crown Holdings AGCO Boeing CSX Agilent Technologies Booz Allen Hamilton Holding Cummins Air Products and Chemicals BorgWarner CVR Energy AK Steel Holding Boston Scientific CVS Caremark Alcoa BrightPoint Dana Holding Aleris Bristol-Myers Squibb Danaher Allegheny Technologies Broadcom Darden Restaurants Allergan C.H. Robinson Worldwide DaVita Alliant Techsystems Cablevision Systems Dean Foods Allstate Caesars Entertainment Deere Ally Financial Calpine Dell Alpha Natural Resources Cameron International Delta Air Lines Altria Group Campbell Soup Devon Energy Amazon.com Capital One Financial Dick's Sporting Goods Ameren Cardinal Health Dillard's American Electric Power CarMax DirecTV American Express Casey's General Stores Discover Financial Services American Family Insurance Catalyst Health Solutions DISH Network Group Caterpillar Dole Food American International Group CBRE Group Dollar General Amerigroup CBS Dollar Tree Ameriprise Financial CC Media Holdings Dominion Resources AmerisourceBergen CDW Domtar Amgen Celanese Dover AMR Celgene Dow Chemical Anadarko Petroleum Centene Dr Pepper Snapple Group Anixter International CenterPoint