Change in the Us Automobile Industry

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

April 2021 VALVE CHATTER

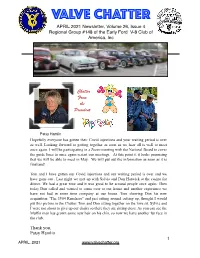

VALVE CHATTER APRIL 2021 Newsletter, Volume 26, Issue 4 Regional Group #148 of the Early Ford V-8 Club of America, Inc Chatter From the President Patsy Hamlin Hopefully everyone has gotten their Covid injections and your waiting period is over as well. Looking forward to getting together as soon as we hear all is well to meet once again. I will be participating in a Zoom meeting with the National Board to cover the guide lines to once again restart our meetings. At this point it it looks promising that we will be able to meet in May. We will put out the information as soon as it is finalized! Tom and I have gotten our Covid injections and our waiting period is over and we have gone out . Last night we met up with Sylvia and Don Harwick at the casino for dinner. We had a great time and it was good to be around people once again. Then today Don called and wanted to come over to our house and another experience we have not had in some time company at our house. Tom showing Don his new acquisition “The 1964 Ranchero” and just sitting around cutting up, thought I would put this picture in the Chatter. Tom and Don sitting together on the love sit. Sylvia and I were not about to give up our chairs so there they are sitting close. As you can see the Muffin man has grown some new hair on his chin, so now we have another fur face in the club. -

Cleveland All Stars Homecoming Car Show of Cleveland and Northeast Ohio Built Vehicles

Cleveland All Stars Homecoming Car Show of Cleveland and Northeast Ohio Built Vehicles June 23 – 25, 2017 APPLICATION FOR PARTICIPATION Presented by the Crawford Auto-Aviation Museum of the Western Reserve Historical Society Show LocationLocation: Cleveland History Center | 10825 East Boulevard, Cleveland, OH 44106 Please seeseesee reverse side forforfor aaa full listlistlist ofofof accepted vehicles. *If applying with a coach-built vehicle from Cleveland/Northern Ohio, please supply evidence of your vehicle’s Cleveland/Northern Ohio provenance if it is not a Northern Ohio marque. Please include a photo of the coachbuilder’s tag or other documentation related to the regional production. All applications will be reviewed by the Cleveland All Stars Homecoming Car Show committee and final acceptance of vehicles will be determined by the committee. Vehicle year: _______________________ Make, Model, and Body Style: ______________________________________ Has this vehicle been modified from new in anyway? [ ] YES [ ] NO If yes, please explain: _______________________________________________________________________________ Name of Owner: ____________________________________ Address: _______________________________________ City: ________________________________________ State: _____________________ Zip Code: _________________ Home/Cell Phone: _____________________________Email Address: ________________________________________ Insurance carrier and policy number: ___________________________________________________________________ Will be trailering -

RINDEX50 Rev 2017

Restorer Index Volume 1 through 50 – 1956-2005 Model A Ford Club of America "The Restorer" Volume 1 Issue 1 to Volume 50 Issue 6 Combined Index Release 7 — March 28, 2017 Edited by Rick Black © Model A Ford Club of America, Inc. 2006 1928 Events of the year, Jul-Aug 1956 (1-2) p 12 1928 (EARLY A'S) Kalinka, "Doc." "The early birds," illus., -Sep-Oct 1967 (12-3) p 11-14 Mar-Apr 1968 (12-6) p 7 Nov-Dec 1968 (13-4) p 24-28 Early Fordor interior. photo, Jan-Feb 1974 (18-5) p 19 Photo, Jul-Aug 1976 (21-2) p 37 1928 FIFTY PLUS FIVE The 1928 Fords, a pictorial essay, Nov-Dec 1983 (28-4) p 16-21 1928 FORD BROCHURE "Introducing the Model A," illus., Nov-Dec 1977 (22-4) p 15-26, back cover 1928 OWNER QUESTIONNAIRE Jan-Feb 1966 (10-5) p 32 1930 ANNIVERSARY LETTERS Mar-Apr 1980 (24-6) p 14-21,26 1930 EARLY MODEL A's Worsham, Bill, "The early 30's," illus., Jul-Aug 1980 (25-2) p 20 1930 MODEL A FORDS Moline, Mary, "Model A Ford in 1930," illus., Jul-Aug 1971 (16-2) p 13-16 Pictorial essay, Mar-Apr 1980 (24-6) covers, p 13-21, 26 1930 SALES BROCHURE Featuring the 1930 "new" models, Jan-Feb 1980 (24-5) p 5-12 20 MILLIONTH FORD "MAFCA Members To View Model A History – Twenty Millionth Ford Enhances Riverside National Convention, " photo, Jul-Aug 2002 (47-2) p 42 "A-1" Tudor (55-A), 1927 (first Model A), photo, Mar-Apr 1963 (7-6) p 17 "A-400" See Convertible Sedan (400-A), 1931 Car Clubs and Special Interest Groups A-BONEYARD Ben Nazenic owner, photo, Jul-Aug 1957 (2-2) p 12 "A" CANADIAN BUILT See also Canadian Model A's Comparison and body part names, discussion of the Canadian built Model A in Brickell, R. -

Auction Results Hershey

Auction Results Hershey Lot Year - Make / Model Chassis # Price Sold 107 1912 Auto-Carrier Delivery Box Van 1683 $49,500.00 Sold 108 1911 Brasier 11/15 HP Runabout 284 $44,000.00 Sold 109 1930 Cadillac V-16 Roadster $1,100,000.00 Sold 110 1900 De Dion-Bouton Vis-à-Vis 585 $96,250.00 Sold 111 1911 E-M-F Model 30 Speedster 43364 $30,250.00 Sold 112 1933 Ford V-8 Station Wagon $82,500.00 Sold 113 1914 G.N. Cyclecar 208 $110,000.00 Sold 114 1953 HRG 1500 WS Roadster WS.222 $60,500.00 Sold 115 1901 International Charette Double Phaeton $77,000.00 Sold 116 1928 Jowett 7/17 Sports Racer 823147 $38,500.00 Sold 117 1911 Kelsey Model M Motorette $49,500.00 Sold 118 1934 Lancia Augusta Special Tourer 34-1078 $143,000.00 Sold 119 1926 Morgan Aero Three-Wheeler 14423 $55,000.00 Sold 120 1953 Nash-Healey Sports Roadster 2347 $71,500.00 Sold 121 1904 Orient Buckboard $30,250.00 Sold 122 1937 Packard Six Station Wagon $170,500.00 Sold 123 1905 Queen Model B Runabout 401 $52,250.00 Sold 124 1931 Rolls-Royce 20/25 Drophead Coupe GFT31 $66,000.00 Sold 125 1913 Spacke Cyclecar Prototype $38,500.00 Sold 126 1958 Triumph TR3A Roadster TS 34495 L $22,000.00 Sold 127 1911 Unic GS Roi-des-Belges 7184 $30,250.00 Sold 128 1956 Volkswagen Type 1 Beetle 1075984 $4,950.00 Sold 129 1921 Wolseley Ten Coupe 51961 $13,750.00 Sold 130 1999 Xanthos 23B $41,250.00 Sold 131 1923 Yellow Cab Model A-2 Brougham Taxi 12757 $33,000.00 Sold 132 1910 Zebra Type A Runabout 1213 $24,750.00 Sold 133 1984 Zoe Zipper $13,200.00 Sold 134 1975 AC Invacar $4,400.00 Sold 135 1926 AC 12/24 -

The Evolution of the US Automotive Industry

The Evolution of the U.S. Automotive Industry Course No: D05-004 Credit: 5 PDH Robert P. Tata, P.E. Continuing Education and Development, Inc. 22 Stonewall Court Woodcliff Lake, NJ 07677 P: (877) 322-5800 [email protected] The Evolution of the U.S. Automotive Industry Copyright 2013 Robert Tata, B.M.S.E., P.E. All Rights Reserved Introduction The author, a licensed Professional Engineer, has also been employed in an engineering capacity by all “Big Three” automakers; GM, Ford, & Chrysler. Here he has sought to investigate the series of events that made Detroit, Michigan the automotive capital of the world. Detroit, Michigan is a place, off the beaten path, in an isolated glove-shape piece of land thrust up between two lakes, with sometimes very inclement weather. Ohio and Indiana, who were also active in the creation of the auto industry in the U.S., are in the same general area of the country as Michigan and share the same climate. How did the industry get its start in this three-state area. One would think that other parts of the country would be more conducive to the formation of such an important part of the history of this nation. Michigan, Ohio, and Indiana were not members of the original 13 states and therefore have to be considered less developed territories than the original thirteen states around the turn of the 19th century when the American gasoline powered automobile was invented. Read how the author has searched for the answers to these somewhat perplexing questions surrounding why Detroit became “The Motor City”. -

View Results

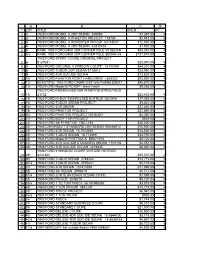

A B C D 1 LOT TITLE SOLD CC 2 1r 1928 FORD MODEL A 4DR SEDAN 369984 $7,357.50 4 3 2r 1929 FORD MODEL A PHAETON PROJECT 136784 $2,943.00 6 4 3r 1929 FORD MODEL A ROADSTER PICKUP A2143047 $12,535.00 4 5 4r 1930 FORD MODEL A 2DR SEDAN A2912453 $7,902.50 4 6 5r RARE 1932 FORD B400 2DR CONVERTIBLE V8 SEDAN $55,045.00 4 7 5ra RARE 1932 FORD B400 2DR CONVERTIBLE SEDAN V8 $107,910.00 4 1932 FORD SPORT COUPE ORIGINAL PROJECT 8 6r 5127651 $35,970.00 5 9 7r 1932 FORD ORIGINAL 5 WINDOW COUPE 18107009 $64,310.00 4 10 8r 1932 FORD TUDOR-2DR SEDAN 5118612 $23,980.00 4 11 9r 1932 FORD 4DR SUICIDE SEDAN $13,625.00 5 12 10r 1932 FORD PHAETON RIGHT HAND DRIVE cb02232 $22,890.00 4 13 11r BEAUTIFUL 1932 FORD CABRIOLET with RUMBLESEAT $46,870.00 3 14 12r 1932 FORD Model B PICKUP - Barn Fresh $9,265.00 5 1932 FORD FIBERGLASS 4DR PHAETON STREETROD 15 13r 23732 $23,435.00 4 16 14r 1932 FORD HI-BOY FIBERGLASS HOTROD 1821940 $17,985.00 4 17 15r 1932 FORD TUDOR SEDAN PROJECT $9,537.50 6 18 16r 1932 FORD 4DR SEDAN $22,345.00 4 19 18r 1932 FORD PHAETON PROJECT $22,890.00 6 20 20r 1932 FORD PHAETON PROJECT NO BODY $4,360.00 6 21 21r 1941 FORD BODY FOR PROJECT $545.00 6 22 22r 1933 FORD 4dr PHAETON 750L1235 $30,520.00 4 23 23r 1935 CHEVROLET STANDARD 2DR SEDAN M5486912 $10,900.00 5 24 24r 1934 FORD 4DR SEDAN 18-1023662 $18,530.00 5 25 25r 1934 FORD TUDOR SEDAN 18-713869 $33,790.00 4 26 26r 1934 FORD Model B FIRETRUCK BB871918 $8,720.00 4 27 27r 1935 FORD 4DR SUICIDE STANDARD SEDAN 1914194 $4,087.50 5 28 28r 1936 FORD 4DR SUICIDE SEDAN 2479435 $5,450.00 5 1936 FORD 5 -

WHEELS: the HORSELESS CARRIAGE – Part 1

PRESENTS WHEELS: THE HORSELESS CARRIAGE – Part 1 Researched and Compiled by William John Cummings BRIEF CHRONOLOGY OF THE EVOLUTION OF THE MODERN AUTOMOBILE – 1 A Frenchman named Etienne Lenoir In August, 1888, William Steinway, patented the first practical gas engine in owner of Steinway & Sons piano factory, Paris in 1860 and drove a car based on the talked to Gottlieb Daimler about U.S. design from Paris to Joinville in 1862. manufacturing right and by September had a deal. By 1891 the Daimler Motor In 1862, Alphonse Bear de Rochas Company, owned by Steinway, was figured out how to compress the gas in the producing petrol engines for tramway same cylinder in which it was to burn. cars, carriages, quadricycles, fire engines This process of bringing the gas into the and boats in a plant in Hartford, cylinder, compressing it, combusting the Connecticut. compressed mixture, then exhausting it is known as the Otto cycle, or four cycle engine. Siegfried Marcus, of Mecklenburg, Germany, built a car in 1868 and showed one at the Vienna Exhibition of 1873. In 1876, Nokolaus Otto patented the Otto cycle engine which de Rochas had neglected to do. Daimler-Phoenix Automobile – 1899-1902 BRIEF CHRONOLOGY OF THE EVOLUTION OF THE MODERN AUTOMOBILE – 2 In 1871, Dr. J.W. Carhart, professor of Thirteen Duryeas of the same design physics at Wisconsin State University, and were produced in 1896, making it the the J.I. Case Company built a working first production car. In 1898 the brothers steam car. It was practical enough to went their separate ways and the Duryea inspire the State of Wisconsin to offer a Motor Wagon Company was closed. -

LOT TITLE VIN T Or BOS SOLD 309R CHRYSLER AIRFLOW PRESSED

A B C D E 1 LOT TITLE VIN T or BOS SOLD 2 309R CHRYSLER AIRFLOW PRESSED TIN TOY 3 309RA POT METAL PROJECT TOY TRUCK 4 310R 1930'S POTMETAL PROJECT TOY 5 501R AMF PEDAL CAR FOR RESTORE 6 502R PEDAL CAR FOR RESTORE 7 1000R 1970 SUZUKI T250 MOTORCYCLE T250-26251 BOS 8 1001R 1975 HONDA XL250 MOTORCYCLE XL250-4001919 T 9 1002R 1971 HONDA MINI TRAIL MOTORCYCLE Z50A-334815 BOS 10 1002RA LATE 1970'S BATAVUS STARFLITE MOPED BOS 11 1003R MINIATURE STEAM TRACTION TRACTOR 12 1003RB NOVO Upright Stationary Steam Engine on Cart 13 300R 1932 FORD ORIGINAL GRILL 14 301R 1932 FORD ORIGINAL GRILL 15 302R 1932 FORD ORIGINAL GRILL 16 303R 1932 FORD ORIGINAL GRILL 17 304R 1932 FORD ORIGINAL GRILL 18 17R 1932 FORD 2DR SEDAN PROJECT 19 305R 1932 FORD ORIGINAL GRILL 20 311R RARE 1930'S FORD FACTORY ACCESSORY RADIO 21 314R NOS 1932 FORD REAR FENDER 22 315R SHARP ALUMINUM TRI-POWER INTAKE 23 317R 1932 FORD GLOVEBOX DOOR WITH CLOCK 24 1R 1928 FORD MODEL A 4DR SEDAN A369984 T 25 2R 1929 FORD MODEL A PHAETON PROJECT 136784 BOS 26 3R 1929 FORD MODEL A ROADSTER PICKUP A2143047 CAP6276 T 27 4R 1930 FORD MODEL A 2DR SEDAN A2912453 T RARE 1932 FORD B400 2DR CONVERTIBLE V8 28 5R SEDAN 50952(V) T RARE 1932 FORD B400 2DR CONVERTIBLE 29 5RA SEDAN V8 55813 B400B713 T 30 6R 1932 FORD SPORT COUPE ORIGINAL PROJECT 5127651 T 31 7R 1932 FORD ORIGINAL 5 WINDOW COUPE 18-I07009 T 32 8R 1932 FORD TUDOR-2DR SEDAN 5118612 T A B C D E 33 9R 1932 FORD 4DR SUICIDE SEDAN 34 10R 1932 FORD PHAETON RIGHT HAND DRIVE C18PF3609 T BEAUTIFUL 1932 FORD CABRIOLET with 35 11R RUMBLESEAT T 36 12R 1932 -

Introduction to R&C Database Compilation & Index

Introduction to R&C Database Compilation & Index I have a long history and fondness for Rod & Custom magazine. This is the first magazine I purchased at age 10, and I’ve been hooked ever since. I often refer back to my collection, but find it hard to quickly lay my hands on a given article. This is for fellow HAMB members who share a love for this little magazine. This Index covers Rod & Custom Magazine from May 1953 through May 1974. I stopped at 1974 since R&C went out of print then. R&C was restarted in December 1988 and lasted until October 2014. This index is created for general reference, technical reference, research, tracing automobile histories, and genealogy. I have attempted to use a consistent categorization or article grouping scheme across all 20+ years, even though editors or previous compilations may not have used this convention. This index contains the following specific information: Title of each article along with a descriptive supplement such as club affiliation, noted customizers, past owners, professions, etc. The author’s and/or photographer’s name where space allowed. Featured vehicle year, make, model, & engine and/or engine displacement where available or where space allowed. Vehicle owner name, city and state. Where the country is other than the United States, I listed the country Product manufacturer name, city and state. Address may be included if space allowed. The month and page number of each feature article or photograph. The index is sorted by year, and a title at the top of each page indicates which year. -

June, 2018 TSCRIPT NEWS Newspage 1

SCRIPJune, 2018 TSCRIPT NEWS NEWSPage 1 Published by the Script “A” Region, MARC June, 2018 Dad, need a little help here? - Sacramento Capitol A’s Johnathan asked his young son, “Greg, do you think I’m a bad father?” “My name is Andrew,” replied his son. - Bob Davies Page 2 SCRIPT NEWS June, 2018 Script “A” Region, Model A Restorers Club http://www.script-a-region.org President Steve Burton 9173 Circle Lake Dr., Grand Blanc, 48439 810-223-4905 or 810-655-6750 [email protected] Doc’s Dribble Vice-President Nora Petriches 1430 Amy St., Burton 48509 810-962-2146 A Message from the President [email protected] Secretary Bob Davies 493 Hut West, Flushing 48433 810-624-0278 t is June already. I hope everybody tions of rain so come prepared for sun. [email protected] I has plans to get their cars on the I have been working hard on plan- Treasurer Jerry Purtell 1691 N. Garfield Rd., Linwood, 48634 road soon before it gets cold. I have ning my trip to Branson in my Sport 989-879-4265 been working to get my car ready for Coupe. I have been pouring over maps Board Cheryl Roy the National Meet in Branson. I am for weeks now looking for the shortest, Members 810-653-8254 Ted Metiva making good progress. All the tires easiest route. My plan so far is to turn 989-777-0964 have air, the horn is tuned and the left at the first and second stop signs Dottie Eckert windshield is clean. -

Bulb Horn Subject Index January 1980

Bulb Horn Subject Index January 1980 – December 1989 For corrections or omissions, please send a message to [email protected] (Note: Regional and Chapter News and Reports are included in most issues as submitted by Regional personnel and edited by the Bulb Horn Editor. Only those Regional reports detailing a specific Regional tour are indexed individually.) Adria Adria of Batavia, The. Marvin, Keith. 1985 Apr-Jun 46 (2). 34-37 American Underslung 1912 American" Underslung". MacIlvain, Walter O.. 1989 Oct-Dec 50 (4). 10-11 Artzberger Foster/Artzberger Steamer, The. Artzberger, Bill. 1984 Apr-Jun 45 (2). 41-43 Austin Auld Austin, The. Connors, J. P.. 1984 Jan-Mar 45 (1). 8-11 Automobile Advertising Auto Clipping Collection Donated to VMCCA. MacIlvain, Walter O. Editor. 1985 Jan- Mar 46 (1). 20-21 Brief History of Packard Advertising, A. Ruddock, Ken. 1989 Jan-Mar 50 (1). 26-30 Automobile Bodies Coachwork to Oder. MacIlvain, Walter O.. 1989 Jul-Sep 50 (3). 10-13 Origin of the Skiff Body, The. Ulmann, Alec. 1984 Jul-Sep 45 (3). 24-25 Automotive Books and magazines Automobile Restorer's Source List: First Annual Edition. Smith, Tom. 1984 Oct-Dec 45 (4). 57-58 Condensed Roster, Listing by Names, Dates and Sites, the Motor Vehicles Commercially Produced in Saginaw County Michigan. Putz, Ronald J.. 1984 Oct-Dec 45 (4). 23-25 Managing Editor's Survey of Automotive Periodicals Published in the United States. Saal, Tom. 1980 Oct-Dec 41 (4). 57-59 Tom Saal's A-Z Survey of U. S. Automotive Periodicals. Saal, Tom. 1981 Apr-Jun 42 (2). -

FORD ( Model "K," 6-Cylinder Touring- Car

SOMETIMES I WAKE UP in indicate the horsepower or number of the middle of the night, get by Dave Cole cylinders or something, but with Ford, up to test the plumbing, and go the first cars were just called Model A. back to bed, but I don't drop off to Within five years, Ford had worked its way sleep right away. The older I get, the more through the alphabet clear up to the Model S! S is the often this happens. As I drift back to sleep, my mind 19th letter in the alphabet, but this doesn't mean that wanders through all sorts of things—solutions to Ford had built 19 models by 1908. The Model S was the world's problems, things I should have done and only Ford's ninth model. They had skipped about didn't, or things I did I shouldn't have and that sort half of the letters on the way to S. of thing—but one night, I got to thinking how Henry In their first five years, Ford had brought out Ford really should have kept going through the al their phabet with his model designations, right up through • Model A, a 2-cylinder, 8-horsepower car, built in 1937. It would have made much better sense than 1903 and '04, what he did. It's really kind of interesting to consider • Model B, a 4-cylinder, 24-horsepower car, built in what he could've done, should've done, and didn't. 1904 and '05, I'll admit that by 1938, the proliferation of mod • Model C, a 2-cylinder, 10-horsepower job, built els had gotten to the point where a new system was from late 1904 thru '05, called for, and that part makes good sense.