Interim Paper on Aviation , File Type

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

People, Places and Policy

People, Places and Policy Set within the context of UK devolution and constitutional change, People, Places and Policy offers important and interesting insights into ‘place-making’ and ‘locality-making’ in contemporary Wales. Combining policy research with policy-maker and stakeholder interviews at various spatial scales (local, regional, national), it examines the historical processes and working practices that have produced the complex political geography of Wales. This book looks at the economic, social and political geographies of Wales, which in the context of devolution and public service governance are hotly debated. It offers a novel ‘new localities’ theoretical framework for capturing the dynamics of locality-making, to go beyond the obsession with boundaries and coterminous geog- raphies expressed by policy-makers and politicians. Three localities – Heads of the Valleys (north of Cardiff), central and west coast regions (Ceredigion, Pembrokeshire and the former district of Montgomeryshire in Powys) and the A55 corridor (from Wrexham to Holyhead) – are discussed in detail to illustrate this and also reveal the geographical tensions of devolution in contemporary Wales. This book is an original statement on the making of contemporary Wales from the Wales Institute of Social and Economic Research, Data and Methods (WISERD) researchers. It deploys a novel ‘new localities’ theoretical framework and innovative mapping techniques to represent spatial patterns in data. This allows the timely uncovering of both unbounded and fuzzy relational policy geographies, and the more bounded administrative concerns, which come together to produce and reproduce over time Wales’ regional geography. The Open Access version of this book, available at www.tandfebooks.com, has been made available under a Creative Commons Attribution-Non Commercial-No Derivatives 3.0 license. -

4R Bus Time Schedule & Line Route

4R bus time schedule & line map 4R Bangor - Holyhead View In Website Mode The 4R bus line (Bangor - Holyhead) has 2 routes. For regular weekdays, their operation hours are: (1) Holyhead: 9:08 AM - 9:18 PM (2) Llangefni: 5:00 AM - 10:15 PM Use the Moovit App to ƒnd the closest 4R bus station near you and ƒnd out when is the next 4R bus arriving. Direction: Holyhead 4R bus Time Schedule 56 stops Holyhead Route Timetable: VIEW LINE SCHEDULE Sunday 9:00 AM - 4:45 PM Monday 9:08 AM - 9:18 PM Ysgol Y Bont, Llangefni Tuesday 9:08 AM - 9:18 PM Library, Llangefni Wednesday 9:08 AM - 9:18 PM Ysgol, Llangefni Thursday 9:08 AM - 9:18 PM Cildwrn Road, Llangefni Friday 9:08 AM - 9:18 PM Ffordd Corn Hir, Llangefni Saturday 9:08 AM - 9:18 PM Bodelis, Llangefni Cae Mawr, Rhostrehwfa Tan Rallt, Rhostrehwfa 4R bus Info Direction: Holyhead Penrhiw, Rhostrehwfa Stops: 56 Trip Duration: 46 min Gorwel Deg, Rhostrehwfa Line Summary: Ysgol Y Bont, Llangefni, Library, Llangefni, Ysgol, Llangefni, Ffordd Corn Hir, Gorwel Deg, Llangristiolus Community Llangefni, Bodelis, Llangefni, Cae Mawr, Rhostrehwfa, Tan Rallt, Rhostrehwfa, Penrhiw, Capel Cana, Rhostrehwfa Rhostrehwfa, Gorwel Deg, Rhostrehwfa, Capel Cana, Stad Tŷ Gwyn, Llangristiolus Community Rhostrehwfa, Cefn Cwmwd, Rhostrehwfa, Afhendre Fawr, Rhostrehwfa, Mona Isaf, Rhostrehwfa, Cefn Cwmwd, Rhostrehwfa Bodffordd Turn, Heneglwys, Anglesey Show Ground, Gwalchmai Uchaf, Old Toll House, Gwalchmai Uchaf, Afhendre Fawr, Rhostrehwfa Waverley, Gwalchmai Uchaf, Clock, Gwalchmai Uchaf, Rhosneigir Turn, Engedi, Ty-Hen -

Stakeholder Briefing Document, Intercity West Coast Re-Franchising

Stakeholder Briefing Document, InterCity West Coast Re-Franchising MAY 2011 1 Consultation Process The Department is grateful to all the organisations and individuals who took the time and effort to respond to this consultation, and to those who attended the consultation events. Their valuable comments and suggestions have been considered and are summarised in this report. The Department has endeavoured, in good faith, to produce a synopsis of each response received. These are tabulated at Appendix B. Any significant omission or incorrect emphasis is entirely unintentional. Bidders for the franchise will have access to all consultation responses submitted. The consultation document for the proposed InterCity West Coast franchise was issued by the Department on the 19th of January 2011, and closed on the 21st of April 2011. The consultation gave details of the proposed specification for the new franchise, and posed a number of questions to consultees. The closed consultation document can be found at: http://www.dft.gov.uk/consultations/closed/ 325 local authorities, agencies (such as the Office of Rail Regulation), user groups and rail industry stakeholders (including Passenger Focus) were formally consulted and were sent electronic copies of the consultation document. No formal ‘hard copy’ document was produced for this consultation exercise as part of the Department’s overall drive for efficiency savings. In addition the document was posted on the DfT website and a press notice released. All MPs with one or more stations in their Constituency served by the current franchise were also sent a copy of the consultation document and copies were also placed in the House of Commons library. -

GENERAL AVIATION REPORT GUIDANCE – December 2013

GENERAL AVIATION REPORT GUIDANCE – December 2013 Changes from November 2013 version Annex C – Wick Airport updated to reflect that it is approved for 3rd country aircraft imports No other changes to November version Introduction These instructions have been produced by Border Force are designed and published for General Aviation1 pilots, operators and owners of aircraft. They help you to complete and submit a General Aviation Report (GAR) and inform you about the types of airport you can use to make your journey. The instructions explain: - What a General Aviation Report (GAR) is What powers are used to require a report Where aircraft can land and take off When you are asked to submit a General Aviation Report (GAR); When, how and where to send the GAR How to complete the GAR How GAR information is used Custom requirements when travelling to the UK The immigration and documentation requirements to enter the UK What to do if you see something suspicious What is a General Aviation Report (GAR)? General Aviation pilots, operators and owners of aircraft making Common Travel Area2 and international journeys in some circumstances are required to report their expected journey to the Police and/or the Border Force command of the Home Office. Border Force and the Police request that the report is made using a GAR. The GAR helps Border Force and the Police in securing the UK border and preventing crime and terrorism. What powers are used to require a report? An operator or pilot of a general aviation aircraft is required to report in relation to international or Channel Islands journeys to or from the UK, unless they are travelling outbound directly from the UK to a destination in the European Union as specified under Sections 35 and 64 of the Customs & 1 The term General Aviation describes any aircraft not operating to a specific and published schedule 2 The Common Travel Area is comprised of Great Britain, Northern Ireland, Ireland, the Isle of Man and the Channel Islands Excise Management Act 1979. -

General Aviation Report (GAR) Guidance – January 2021

General Aviation Report (GAR) Guidance – January 2021 Changes to the 2019 version of this guidance: • Updated Annex C (CoA list of airports) Submitting a General Aviation Report to Border Force under the Customs & Excise Management Act 1979 and to the Police under the Terrorism Act 2000. Introduction These instructions are for General Aviation (GA) pilots, operators and owners of aircraft. They provide information about completing and submitting a GAR and inform you about the types of airport you can use to make your journey. The instructions explain: 1. What is General Aviation Report (GAR) 2. Powers used to require a report 3. Where aircraft can land and take off 4. When, how and where to send the GAR 5. How to submit a GAR 6. How to complete the GAR 7. How GAR information is used 8. Customs requirements when travelling to the UK 9. Immigration and documentation requirements to enter the UK 10. What to do if you see something suspicious 1. General Aviation Report (GAR) GA pilots, operators and owners of aircraft making Common Travel Area1 and international journeys in some circumstances are required to report or provide notification of their expected journey to UK authorities. The information provided is used by Border Force and the Police to facilitate the smooth passage of legitimate persons and goods across the border and prevent crime and terrorism. 2. Powers used to require a report An operator or pilot of a GA aircraft is required to report in relation to international or Channel Island journeys to or from the UK under Sections 35 and 64 of the Customs & Excise Management Act 1979. -

Location Indicators by Indicator

ECCAIRS 4.2.6 Data Definition Standard Location Indicators by indicator The ECCAIRS 4 location indicators are based on ICAO's ADREP 2000 taxonomy. They have been organised at two hierarchical levels. 12 January 2006 Page 1 of 251 ECCAIRS 4 Location Indicators by Indicator Data Definition Standard OAAD OAAD : Amdar 1001 Afghanistan OAAK OAAK : Andkhoi 1002 Afghanistan OAAS OAAS : Asmar 1003 Afghanistan OABG OABG : Baghlan 1004 Afghanistan OABR OABR : Bamar 1005 Afghanistan OABN OABN : Bamyan 1006 Afghanistan OABK OABK : Bandkamalkhan 1007 Afghanistan OABD OABD : Behsood 1008 Afghanistan OABT OABT : Bost 1009 Afghanistan OACC OACC : Chakhcharan 1010 Afghanistan OACB OACB : Charburjak 1011 Afghanistan OADF OADF : Darra-I-Soof 1012 Afghanistan OADZ OADZ : Darwaz 1013 Afghanistan OADD OADD : Dawlatabad 1014 Afghanistan OAOO OAOO : Deshoo 1015 Afghanistan OADV OADV : Devar 1016 Afghanistan OARM OARM : Dilaram 1017 Afghanistan OAEM OAEM : Eshkashem 1018 Afghanistan OAFZ OAFZ : Faizabad 1019 Afghanistan OAFR OAFR : Farah 1020 Afghanistan OAGD OAGD : Gader 1021 Afghanistan OAGZ OAGZ : Gardez 1022 Afghanistan OAGS OAGS : Gasar 1023 Afghanistan OAGA OAGA : Ghaziabad 1024 Afghanistan OAGN OAGN : Ghazni 1025 Afghanistan OAGM OAGM : Ghelmeen 1026 Afghanistan OAGL OAGL : Gulistan 1027 Afghanistan OAHJ OAHJ : Hajigak 1028 Afghanistan OAHE OAHE : Hazrat eman 1029 Afghanistan OAHR OAHR : Herat 1030 Afghanistan OAEQ OAEQ : Islam qala 1031 Afghanistan OAJS OAJS : Jabul saraj 1032 Afghanistan OAJL OAJL : Jalalabad 1033 Afghanistan OAJW OAJW : Jawand 1034 -

SWANSEA Road, Rail and Sea Connectivity to LET Close Proximity to Swansea City Centre Warehousing / Office / and M4 Motorway (Junction 42) Open Storage Opportunities

SWANSEA Road, rail and sea connectivity TO LET Close proximity to Swansea city centre Warehousing / Office / and M4 motorway (Junction 42) Open Storage Opportunities Port of Swansea, SA1 1QR Situated in a top tier (‘A’) grant assisted area and within the Swansea Bay City Region Available Property Swansea City Centre A483 M4 SA1 Swansea Waterfront J42 - 4.8 km / 3 mi Delivering Property Solutions Swansea, Available Property Sat Nav: SA1 1QR Opportunity M4 J45 J47 J46 Our available sites, warehousing and office accommodation are situated within the secure confines of the Port of Swansea, located M4 J44 less than 2 miles from Swansea city centre. J47 12.8 km A48 A4067 Over recent years the Port has benefitted from major investment and offers opportunity M4 for port-related users to take advantage of both available quayside access and port J43 J45 12.8 km Winch Wen handling services, together with non-port related commercial occupiers seeking well A483 M4 located and secure storage land, existing warehousing and development plots for J42 the design and construction of bespoke business accommodation. Cockett Swansea Location Port Services St Thomas M4 Swansea A483 A4118 City Centre J42 4.8 km The Port of Swansea is conveniently located ABP’s most westerly positioned Port in South Wales providing ABP Port 3 miles, via the A483 dual carriageway, to shorter sailing times for vessels trading in/out of the West of of Swansea the west of Junction 42 of the M4 motorway, UK. The docks provides deep sea accessibility (Length: 200m, A4067 offering excellent road connectivity. -

Flying Clubs and Schools

A P 3 IR A PR CR 1 IC A G E FT E S, , YOUR COMPLE TE GUI DE C CO S O U N R TA S C ES TO UK AND OVERSEAS UK clubs TS , and schools Choose your region, county and read down for the page number FLYING CLUBS Bedfordshire . 34 Berkshire . 38 Buckinghamshire . 39 Cambridgeshire . 35 Cheshire . 51 Cornwall . 44 AND SCHOOLS Co Durham . 53 Cumbria . 51 Derbyshire . 48 elcome to your new-look Devon . 44 Dorset . 45 Where To Fly Guide listing for Essex . 35 2009. Whatever your reason Gloucestershire . 46 Wfor flying, this is the place to Hampshire . 40 Herefordshire . 48 start. We’ve made it easier to find a Lochs and Hertfordshire . 37 school and club by colour coding mountains in Isle of Wight . 40 regions and then listing by county – Scotland Kent . 40 Grampian Lancashire . 52 simply use the map opposite to find PAGE 55 Highlands Leicestershire . 48 the page number that corresponds Lincolnshire . 48 to you. Clubs and schools from Greater London . 42 Merseyside . 53 abroad are also listed. Flying rates Tayside Norfolk . 38 are quoted by the hour and we asked Northamptonshire . 49 Northumberland . 54 the schools to include fuel, VAT and base Fife Nottinghamshire . 49 landing fees unless indicated. Central Hills and Dales Oxfordshire . 42 Also listed are courses, specialist training Lothian of the Shropshire . 50 and PPL ratings – everything you could North East Somerset . 47 Strathclyde Staffordshire . 50 Borders want from flying in 2009 is here! PAGE 53 Suffolk . 38 Surrey . 42 Dumfries Northumberland Sussex . 43 The luscious & Galloway Warwickshire . -

Uk Aircraft Maintenance Companies

UK AIRCRAFT MAINTENANCE COMPANIES CAREERS CENTRE Please do not reproduce without permission from RAeS Careers Centre AAR International AEM Limited World Business Centre Taylor's End 120 Newall Road Stansted Airport Heathrow Airport STANSTED Middlesex Essex London CM24 1RB TW6 2RE Tel: +44 (0) 1279 682332 Tel: +44 (0) 208 990 6700 Web: www.aem.co.uk Web: www.aarcorp.com Air Contractors Engineering Airline Services Unit 5, Rankine Square Canberra House Deans Industrial Estate Robeson Way Livingston Sharston Green Business Park West Lothian Manchester EH54 8SH M22 4SX Tel: +44 (0) 131 339 8880 Tel: +44 (0) 161 495 6900 Web: www.aircontractorsengineering.co.uk Web: www.airline-services.com A J Walter Aviation Apple Aviation Viscount House Cedar House, Sutton Quays Business Park Partridge Green Clifton Road West Sussex Sutton Weaver RH13 8RA Cheshire, WA7 3EH Tel: +44 (0) 1403 798 000 Tel: +44 (0) 7955 028 542 Web: www.ajw-aviation.com Web: www.appleaviation.com ATC Lasham Airtime Aviation Lasham Airfield Hangar 103 Lasham Aviation Park West Hampshire Bournemouth International Airport GU34 5SP Christchurch Tel: +44 (0) 1256 825100 Dorset, BH23 6NW Web: www.atclasham.co.uk Tel: +44 (0) 1202 580 676 Web: www.airtimeaviation.com Avia Technique Air Atlanta Aviaservices Unit 1 Fishponds Estate Unit 2, Meadowbrook Fishponds Road Industrial Estate Wokingham Maxwell Way Berkshire Crawley RG41 2QJ West Sussex, RH10 9SA Tel: +44 (0) 118 978 9789 Tel: +44 (0) 1293 223 500 Web: www.aviatechnique.co.uk Web: www.aviaservices.com 4 Hamilton Place London W1J 7BQ Tel +44(0)20 7670 4300 Fax +44(0)20 7670 4309 Email [email protected] Web www.careersinaerospace.com www.aerosociety.com REGISTERED CHARITY NO. -

Review of the Intra Wales Air Service

Monitoring of the Cardiff/Ynys Môn Air Service Final Report October 2008 Welsh Assembly Government Evaluation of the Cardiff/Ynys Môn Air Service Final Report Contents Amendment Record This report has been issued and amended as follows: Issue Revision Description Date Signed 1 0 Draft Report Jun 08 EC 1 1 2nd Draft Report Jul 08 EC 1 2 3rd Draft Report Jul 08 EC 1 3 4th Draft Report Aug 08 EC 1 4 Final Report Oct 08 EC Halcrow Group Limited One Kingsway Cardiff CF10 3AN Wales Tel +44 (0)29 2072 0920 Fax +44 (0)29 2072 0880 www.halcrow.com Contents Executive Summary Crynodeb Gweithredol 1 Introduction 1 1.1 The Study 1 1.2 Background 1 1.3 Aims & Objectives 2 1.4 Approach to the Study 2 1.5 Structure of Report 3 2 Existing Conditions 4 2.1 Introduction 4 2.2 Demand for Air Travel 4 2.3 Demand for Travel between North and South W ales 6 2.4 Reasons for Travel (Journey Purpose) 7 2.5 Length of Stay 8 2.6 Service Reliability 10 2.7 Key Findings 11 3 Reasons for Mode Choice 12 3.1 Introduction 12 3.2 Journey Time 14 3.3 Journey Cost 15 3.4 Comfort 19 3.5 Departure/Arrival Locations 21 3.6 Frequency of Service 24 3.7 Environmental Considerations 26 3.8 Other Influences 27 3.9 Key Findings 27 4 Social Inclusion 29 4.1 Introduction 29 4.2 Social Inclusion Impacts 29 4.3 Access to Transport services 30 4.4 Additional Needs 31 4.5 Conclusions 31 Doc No 1 Rev: - Date: June 2008 U:\CUC\PROJECTS\Live Projects\WAG Framework 2007\Lot 1\Projects\Air PSO (CTCADZ)\Reports\Final Report\Final Evaluation Report_No options Mar 09.doc 5 Economic Activity 33 -

Cold Weather Payments 7 Dec 2010

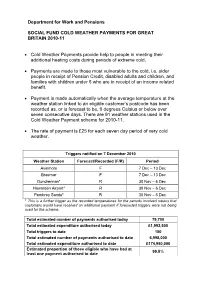

Department for Work and Pensions SOCIAL FUND COLD WEATHER PAYMENTS FOR GREAT BRITAIN 2010-11 • Cold Weather Payments provide help to people in meeting their additional heating costs during periods of extreme cold. • Payments are made to those most vulnerable to the cold, i.e. older people in receipt of Pension Credit, disabled adults and children, and families with children under 5 who are in receipt of an income related benefit. • Payment is made automatically when the average temperature at the weather station linked to an eligible customer’s postcode has been recorded as, or is forecast to be, 0 degrees Celsius or below over seven consecutive days. There are 91 weather stations used in the Cold Weather Payment scheme for 2010-11. • The rate of payment is £25 for each seven day period of very cold weather. Triggers notified on 7 December 2010 Weather Station Forecast/Recorded (F/R) Period Aviemore F 7 Dec – 13 Dec Braemar F 7 Dec – 13 Dec Dundrennan* R 30 Nov – 6 Dec Hawarden Airport* R 30 Nov – 6 Dec Pembrey Sands* R 30 Nov – 6 Dec * This is a further trigger as the recorded temperatures for the periods involved means that customers would have received an additional payment if forecasted triggers were not being used for the scheme. Total estimated number of payments authorised today 79,700 Total estimated expenditure authorised today £1,992,500 Total triggers to date 150 Total estimated number of payments authorised to date 6,998,000 Total estimated expenditure authorised to date £174,950,000 Estimated proportion of those eligible who have had at 99.8% least one payment authorised to date Note: The data above is based on the estimated number of benefit units linked to each weather station which are eligible for Cold Weather Payments. -

Organisations Approved in Accordance with Part M, Subpart G Published 04 September 2018 That Have ARC Privileges

Organisations approved in accordance with Part M, Subpart G Published 04 September 2018 that have ARC privileges Approval Address Aircraft Type Reference UK.MG.0231 2 Excel Aviation Limited Extra EA200/300 Series The Tiger House Sywell Aerodrome Piper PA31 AOC No GB2299 Sywell Beech 200 Series Northamptonshire NN6 0BN Boeing 727 Tel: 01778 590448 Eurocopter EC135 Series Email: [email protected] Boeing 737 300/400/500 Regional Office: Shared Service Centre UK.MG.0661 A2B Aero Limited EUROCOPTER AS355 SERIES Hangar 4S Oxford Airport SIKORSKY S76 SERIES AOC No Kidlington BELL 429 SERIES Oxfordshire OX5 1RA EUROCOPTER AS365 SERIES Tel: 01844 352239 / 07777 236 0123 EUROCOPTER EC135 SERIES Email: [email protected] SINGLE TURBINE ENGINE HELICOPTERS NOT E AGUSTA WESTLAND AW139 Regional Office: Shared Service Centre EUROCOPTER BO105 EUROCOPTER DEUTSCHLAND MBB-BK 117 SERI EUROCOPTER EC155 SERIES MD HELICOPTERS 902 ROBINSON R22/R44 AGUSTA AW109 SERIES BELL 212/AGUSTA AB212 BELL 412/AGUSTA AB412 AIRBUS HELICOPTERS EC225 AIRBUS HELICOPTERS AS332 UK.MG.0494 Acropolis Aviation Limited AIRBUS A319-100 SERIES Business Aviation Centre Farnborough AOC No 2363 Airport Farnborough Hampshire GU14 6XA Tel: 01458 241112 Email: aidan.murphy@acropolis- aviation.com Regional Office: Shared Service Centre UK.MG.0385 ACS Aviation Limited SINGLE TURBOPROP AEROPLANES NOT EXCEED Hangar 4 Perth Airport PISTON ENGINE AEROPLANES - METAL STRUCT AOC No Scone PISTON ENGINE AEROPLANES - COMPOSITE ST Perthshire PH2 6PL PISTON ENGINE AEROPLANES - WOODEN STRU