TVA PILOT Annual Report to the General Assembly

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Watauga River Water Quality Management Plan (2002)

WATAUGA RIVER WATERSHED (06010103) OF THE TENNESSEE RIVER BASIN WATER QUALITY MANAGEMENT PLAN TENNESSEE DEPARTMENT OF ENVIRONMENT AND CONSERVATION DIVISION OF WATER POLLUTION CONTROL WATERSHED MANAGEMENT SECTION August 13, 2002 WATAUGA RIVER WATERSHED WATER QUALITY MANAGEMENT PLAN TABLE OF CONTENTS Glossary Chapter 1. Watershed Approach to Water Quality Chapter 2. Description of the Watauga River Watershed Chapter 3. Water Quality Assessment of the Watauga River Watershed Chapter 4. Point and Nonpoint Source Characterization of the Watauga River Watershed Chapter 5. Water Quality Partnerships in the Watauga River Watershed Chapter 6. Future Plans Appendix I Appendix II Appendix III Appendix IV Appendix V Glossary GLOSSARY 1Q20. The lowest average 1 consecutive days flow with average recurrence frequency of once every 20 years. 30Q2. The lowest average 3 consecutive days flow with average recurrence frequency of once every 2 years. 7Q10. The lowest average 7 consecutive days flow with average recurrence frequency of once every 10 years. 303(d). The section of the federal Clean Water Act that requires a listing by states, territories, and authorized tribes of impaired waters, which do not meet the water quality standards that states, territories, and authorized tribes have set for them, even after point sources of pollution have installed the minimum required levels of pollution control technology. 305(b). The section of the federal Clean Water Act that requires EPA to assemble and submit a report to Congress on the condition of all water bodies across the Country as determined by a biennial collection of data and other information by States and Tribes. AFO. Animal Feeding Operation. -

Some Dam – Hydro Newstm

11/20/2015 Some Dam – Hydro News TM And Other Stuff i Quote of Note: “Remember, te Ark was built by amaturs, te Titanic by professionals.” – Unknown Some Dam - Hydro News Newsletter Archive for Back Issues and Search http://npdp.stanford.edu/ Click on Link (Some Dam - Hydro News) Bottom Right - Under Perspectives “Good wine is a necessity of life.” - -Thomas Jefferson Ron’s wine pick of the week: 2012 Cameron Hughes Cabernet Sauvignon "CAM Collection" “ No nation was ever drunk when wine was cheap. ” - - Thomas Jefferson Dams: (TVA’s Boone Dam headache just got bigger.) TVA: Separate underground water near Boone Dam a “potential problem” By Josh Smith, November 4, 2015, wjhl.com BOONE LAKE (WJHL) – The Tennessee Valley Authority is closely monitoring a second area of water moving underground near Boone Dam. That’s according to a newly released report on the plan to stop a separate area of water movement under and through Boone Dam, something the utility says would have jeopardized the safety of communities downstream if unaddressed. A year ago, TVA rapidly dropped the level of Boone Dam after discovering a sinkhole and water seeping 1 Copy obtained from the National Performance of Dams Program: http://npdp.stanford.edu out of an embankment near the base of the dam. This past summer, TVA announced its plan to spend 5 to 7 years and as much as $300 million on the repair. “What we believe is that this proposed repair project that we have laid out for Boone Dam will take care of all of this issue,” said Jim Hopson, TVA spokesman. -

Boone Dam Seepage Remediation

Boone Dam Seepage Remediation FINAL ENVIRONMENTAL ASSESSMENT JANUARY 2016 TENNESSEE VALLEY AUTHORITY This page intentionally left blank. Document Type: EA-Administrative Record Index Field: Final Environmental Assessment Project Name: Boone Dam Seepage Remediation Project Number: 2015- 15 Boone Dam Seepage Remediation Final Environmental Assessment January 2016 For Information Contact: Matthew Higdon, NEPA Specialist Tennessee Valley Authority 400 West Summit Hill Drive, WT 11D Knoxville, Tennessee 37902-1499 Phone: 865-632-8051 Email: [email protected] Boone Dam Seepage Remediation Table Of Contents TABLE OF CONTENTS 1.0 INTRODUCTION ............................................................................................... 1-1 1.1 PROJECT LOCATION AND DESCRIPTION ..................................................... 1-1 1.2 BACKGROUND .................................................................................................. 1-7 1.2.1 Prior Related Activities and NEPA Compliance ...................................... 1-7 1.3 PURPOSE AND NEED FOR ACTION ............................................................... 1-9 1.4 SCOPE OF THIS ENVIRONMENTAL ASSESSMENT ...................................... 1-9 1.5 SIMILAR AND CONNECTED ACTIONS .......................................................... 1-10 1.5.1 Related Actions to Address Near-Term Needs ..................................... 1-10 1.5.2 Related Actions to Address Long-Term Needs .................................... 1-11 1.6 RELATED ENVIRONMENTAL REVIEWS ...................................................... -

Tennessee Fish and Wildlife Commisssion Proclamation 19-06 Bait

Page 1 of 5 TENNESSEE FISH AND WILDLIFE COMMISSSION PROCLAMATION 19-06 BAIT Pursuant to the authority granted by Title 70, Tennessee Code Annotated, Section 70-4-107, the Tennessee Fish and Wildlife Commission (TFWC) proclaims the following regulations effective March 1, 2020. SECTION I. GENERAL REGULATIONS 1. Definitions. a. For the purposes of this proclamation, "bait" means any fish, crayfish, or salamander species, that is not identified by the TFWC as endangered, threatened, or in need of management or specifically regulated in this proclamation. b. For the purposes of this proclamation, "sport angler" means anyone who takes, kills, injures, captures, or catches any sport fish; attempts to take, kill, injure, capture, or catch any sport fish; and every act of assistance thereof. c. For the purposes of this proclamation, "bait dealer" means one who engages in the business of capturing legal species of fish or other aquatic life for the purpose of sale, or one who sells legal species of fish and other aquatic life for bait. 2. All bait dealers must purchase a type 118 (resident) or 116 (nonresident) license annually and make all necessary reports as required to the Tennessee Wildlife Resources Agency. Only commercial fishers and bait dealers may harvest bait for sale. The harvest and use of bait by commercial fishers shall be regulated in the commercial fishing proclamation. 3. Under no circumstance shall live bait be intentionally released into Tennessee waters unless released into the waters from which the bait were harvested. 4. A licensed sport angler (with all required licenses and permits) can harvest game fish (including rainbow trout and sunfish) for use as bait from the wild using legal sport fishing methods. -

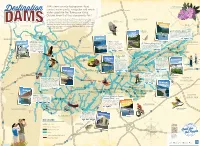

TVA's Dams Provide Hydropower, Flood Control, Water Quality, Navigation

TVA’s dams provide hydropower, ood Catawba Rhododendron (Rhododendron catawbiense) control, water quality, navigation and ample Lexington Destination water supply for the Tennessee Valley. Did you know that they also provide fun? Come summer, TVA operates its dams to ll the reservoirs for recreation. Boating, shing, swimming, rafting and blueway paddling are all supported Bald Eagle KENTUCKY by TVA with boat ramps, swim beaches and put ins. There are plenty of hiking (Haliaeetus leucocephalus) and biking trails, picnic pavilions, playgrounds, campsites, scenic overlooks SOUTH and other day-use areas, too. So plan a TVA vacation this year—you’re sure HO W.V. ILLINOIS LSTON 77 to have a dam good time. o R i v i e Rainbow Trout South Holston Dam - 1951 h r (Oncorhynchus mykiss) Because of its depth and clarity, South Holston Lake is a O FORT premier destination for inland scuba diving. The aerating Paducah PATRICK weir below the dam has many benets—among them NRY creating an oxygen-rich environment that’s fostered a HE world-class trout shery. ORRIS 75 MISSOURI N Hopkinsville 65 Kentucky – 1944 24 Norris - 1936 CKY Norris Dam—the rst built by a newly VIRGINIA KENTU Around Kentucky Lake there are Ft. Patrick Henry - 1953 55 formed TVA—is known for its many Fort Patrick Henry Dam is an ideal shing over 12,000 acres of state wildlife hiking and biking trails. The Norris River management areas, that offer small destination. The reservoir is stocked with rainbow Bluff Trail is a must-see destination for trout each year, and is also good for hooking and large game and waterfowl wildower enthusiasts each spring. -

TRVSC Itinerary

Tennessee River Valley EXPLORE MORE Stewardship Council America’s Tennessee River Valley W.V. IL. 77 o R i v i e h r KENTUCKY 81 O Paducah 77 75 VIRGINIA Kentucky 24 MISSOURI Dam & Lock Hopkinsville 65 Clear Creek Dam Beaver Creek Dam 55 LAND BETWEEN THE LAKES r NATIONAL RECREATION AREA Ft. Patrick Henry Dam South e Holston Dam v Boone Dam C Doakes Wilbur Dam i u 81 m Creek Dam R b Watauga e Dam ARK. r i Nashville l Norris Dam a Cherokee n Nolichucky p Dam d Dam R 40 p 155 i v e i r Douglas 26 Melton Dam s Hill DamKnoxville GREAT SMOKY MOUNTAINS s & Lock NATIONAL PARK i Cedar Ft. Loudoun Dam & Lock Dam TENNESSEE 40 s Tellico 40 NORTH Pin Oak Dam Great Falls Dam Dam s Beech Dam Redbud Dam i Dogwood Dam Watts Bar CAROLINA Dam & Lock M Pine Dam Lost Creek Dam Sycamore Dam 75 Fontana Dam Asheville Charlotte 40 Normandy Dam 26 24 R i v e r Apalachia 65 Dam SHILOH NATIONAL Hiwassee Dam MILITARY PARK Tims Ford Dam Ocoee #1 Dam Memphis Chickamauga Dam & Lock Ocoee #2 Dam Chatuge Dam Pickwick Landing Dam & Lock Nickajack Dam & Lock Chattanooga Ocoee #3 Dam Raccoon Nottely Dam Wheeler Mountain SOUTH Dam & Lock Pumped Blue Ridge Dam Storage CAROLINA Plant Muscle Wilson Dam Shoals & Lock Huntsville 75 e Cedar Creek Dam e 26 b Guntersville g Little Bear Creek Dam i Dam & Lock b Tupelo m y Bear Creek Dam T e n n e s s e e o a 85 T w - r e e GEORGIA e t s a s Upper Bear Creek Dam W e n 59 n e MISSISSIPPI T 55 Atlanta ALABAMA 20 20 Where River s andBirmingham Mount ains Meet | www. -

Finding of No Significant Impact Tennessee Valley Authority

Document Type: EA-Administrative Record Index Field: Finding of No Significant Impact (FONSI) Project Name: Boone Dam Seepage Remediation Project Number: 2015-15 FINDING OF NO SIGNIFICANT IMPACT TENNESSEE VALLEY AUTHORITY BOONE DAM SEEPAGE REMEDIATION The Tennessee Valley Authority (TVA) proposes to construct a composite seepage barrier to remediate seepage beneath the Boone Dam in Sullivan County, Tennessee. In October 2014, a small sinkhole and seepage was discovered at the base of the dam that indicates a potential risk to the integrity of a section of the dam’s earthen embankment. TVA responded to the discovery by taking immediate interim risk reduction measures (IRRMs) for the protection of public safety. These measures included repairing the small sinkhole, constructing a tailrace filter to minimize further deterioration of the dam, closing the dam reservation (areas managed for the purpose of supporting operation and maintenance of the dam and associated infrastructure) to the public, installing a network of sensors to monitor the dam, and lowering the pool elevation to between 1,350 and 1,355 feet mean sea level (msl), which is approximately 10 feet below normal winter pool levels. As part of the IRRMs, TVA also began Interim Operations at Boone Dam that included lower reservoir levels, limited seasonal reservoir pool fluctuation, modified releases into the tailwater for hydropower generation, 24-hour inspection, and modified flood control operations. After extensive investigation, TVA developed a proposal to remediate the seepage and prepared an environmental assessment (EA) to consider its potential environmental impacts. Proposed Action As described in detail in the EA, TVA proposes to remediate the seepage of water and sediment under Boone Dam by constructing a composite seepage barrier from the crest of the dam embankment downward into the foundations soils, weathered bedrock, and underlying bedrock beneath the dam. -

March 2016 Newsletter

March 2016 ATVG Newsletter EPA Set to Declare Memphis Area in Compliance With Smog Standards In a move that would give a boost to local economic-development efforts, the U.S. Environmental Protection Agency appears poised to declare the Memphis area in compliance with federal air-pollution standards. EPA recently published proposals to reclassify Crittenden County and part of DeSoto County as being in attainment, or compliance, with the standard for ground-level ozone pollution. The two counties encompass the Arkansas and Mississippi portions of the local area that has categorized as nonattainment, or in violation of the standard. The federal agency also has signaled its intention to reclassify the Tennessee portion of the nonattainment area, Shelby County, as being in compliance with pollution rules. "EPA is proposing to determine that the Memphis, TN-MS-AR area is attaining the 2008 8-hour ozone national ambient air quality standards," the agency said in a public notice published February 11th in the Federal Register. The proposals are subject to public comment periods ending in March. Should the reclassification become final, the Memphis area will be much more attractive to industries seeking sites for new plants, said Bob Rogers, pollution-control manager for the Health Department. In areas that violate air standards, new and expanding industries face greater difficulty getting environmental permits. They are also subject to much more rigorous and costly pollution-control standards on air emissions. "It's a very big deal. When we're in attainment, we get on more lists for expansions and businesses to move here," Rogers said. -

In 1996, the Tennessee Valley Authority (TVA) Completed a Five

OVERVIEW OF RESERVOIR RELEASE IMPROVEMENTS AT 20 TVA DAMS By John M. Higgins,1 Member, ASCE, and W. Gary Brock2 ABSTRACT: In 1987, the Tennessee Valley Authority (TVA) authorized a com- prehensive review of reservoir operating priorities that had been followed since 1933. The purpose was to ensure optimum operation of the reservoir system, rec- ognizing that needs, demands, and values change over time. The review resulted in a ®ve-year, $50 million program to improve the quantity and quality of releases from 20 dams in the Tennessee Valley. TVA worked with state and federal resource agencies to de®ne minimum ¯ow and dissolved oxygen targets for each tailwater. Facilities and operating procedures were designed and installed to meet the target conditions. This paper describes the facilities, operating procedures, and perfor- mance of the reservoir release improvements. Alternative approaches, monitoring requirements, operational problems, and costs are discussed. Results from four years of operation are presented. INTRODUCTION In 1996, the Tennessee Valley Authority (TVA) completed a ®ve-year, $50 million program to improve the quantity and quality of releases from 20 dams in the Tennessee Valley. Prior to the program, over 500 km of tailwaters were being adversely impacted by reservoir releases. Hydropower operations re- sulted in periods of zero ¯ow below some dams. Thermal reservoir strati®- cation resulted in the release of water low in dissolved oxygen (DO), affecting downstream water quality, aquatic habitat, recreation, and waste assimilation. To improve the releases, TVA worked with resource agencies and nongov- ernmental organizations to de®ne minimum ¯ow and dissolved oxygen tar- gets. -

TVA Boone Dam PBL

TVA Boone Dam PBL Created By: Wendy Courtney Topic: Earth and Human Activity and Grade Level: Middle Grades Forces as it Relates to Dam and Embankment Building Science Standards: ● Science and Engineering Practice: Asking questions (for science) and defining problems (for engineering) Students define design problems, invoking scientific background knowledge to define multiple criteria and constraints for solutions. ● Develop and use models. ● Evaluate design constraints on solutions for maintaining ecosystems and biodiversity. ● Evaluate and interpret that for every force exerted on an object there is an equal force exerted in the opposite direction. ● Interpret data to explain that earth’s groundwater resources are unevenly distributed as a result of geologic processes. Math Standards: ● Summarize numerical data sets in relation to their context. ● Using mathematics and computational thinking ELA & Other Content Area Standards: ● Integrate information presented in different media or formats, such as in tables, images, diagrams, and words to develop a coherent understanding of a topic or issue. ● Include multimedia components and visual displays in presentations to clarify information. Unit Summary: Write a few sentences describing this PBL Multi-Dimensional Question/Driving Question: Think of unit. a relevant problem with multiple solutions that will drive student learning. Background information: In October 2014, a sinkhole was discovered near the base of the embankment at Boone Dam, How can we as civil engineers build a geotechnical wall that and water and sediment was found seeping from the will prevent the seepage of groundwater from causing riverbank below. While sinkhole occurrence in East internal erosion and damaging the existing Boone Dam. Stu Tennessee is common, the locations of the sinkhole and the TSIN PBL Template | www.tsin.org | Page 1 muddy discharge were indicators of potential issues with the safety of the dam. -

Boone Dam Seepage Remediation Supplemental Environmental Assessment

Document Type: EA-Administrative Record Index Field: Supplemental Environmental Assessment Project Name: Boone Dam Seepage Remediation Project Number: 2015-15 Boone Dam Seepage Remediation Vegetation Management – Herbicide Use Supplemental Environmental Assessment June 2020 For Information Contact: Matthew Higdon NEPA Specialist Tennessee Valley Authority 400 West Summit Hill Drive, WT11B Knoxville, Tennessee 37902-1499 Email: [email protected] This page intentionally left blank. TABLE OF CONTENTS 1.0 INTRODUCTION .................................................................................................. 1 1.1 BACKGROUND .................................................................................................. 2 1.2 PURPOSE AND NEED FOR ACTION ................................................................ 3 1.3 RELATED ENVIRONMENTAL REVIEWS........................................................... 3 1.4 SCOPE OF THIS ENVIRONMENTAL ASSESSMENT ........................................ 4 1.5 CONSULTATION REQUIREMENTS AND NECESSARY PERMITS................... 5 1.6 PUBLIC NOTIFICATION ..................................................................................... 5 2.0 DESCRIPTION OF ALTERNATIVES CONSIDERED .......................................... 6 2.1 NO ACTION ALTERNATIVE ............................................................................... 6 2.2 TVA’S PROPOSED ACTION – HERBICIDE USE FOR VEGETATION MANAGEMENT ................................................................................................. -

June, 2017 (Revised) 1 RULES of TENNESSEE WILDLIFE

RULES OF TENNESSEE WILDLIFE RESOURCES AGENCY BOATING CHAPTER 1660-02-07 RULES AND REGULATIONS GOVERNING OPERATIONS OF VESSELS TABLE OF CONTENTS 1660-02-07-.01 Repealed 1660-02-07-.20 Repealed 1660-02-07-.02 AEDC Lake 1660-02-07-.21 Boone Lake 1660-02-07-.03 Repealed 1660-02-07-.22 Kentucky Lake 1660-02-07-.04 Old Hickory Lake 1660-02-07-.23 Watts Bar Lake 1660-02-07-.05 Percy Priest Reservoir 1660-02-07-.24 Ocoee River 1660-02-07-.06 Pickwick Lake 1660-02-07-.25 Cherokee Reservoir (Cherokee Dam) 1660-02-07-.07 Center Hill Lake 1660-02-07-.26 Melton Hill Reservoir 1660-02-07-.08 Beech River Watershed Lakes 1660-02-07-.27 Douglas Lake 1660-02-07-.09 Watauga Lake 1660-02-07-.28 Norris Reservoir 1660-02-07-.10 Tims Ford lake 1660-02-07-.29 South Holston Lake 1660-02-07-.11 Special Areas 1660-02-07-.30 Parksville Lake 1660-02-07-.12 Normandy Reservoir 1660-02-07-.31 Fort Patrick Henry Reservoir 1660-02-07-.13 Cold Creek 1660-02-07-.32 Cordell Hull Lake 1660-02-07-.14 Fort Loudoun Lake 1660-02-07-.33 Lake Barkley 1660-02-07-.15 Chickamauga Lake 1660-02-07-.34 Dale Hollow Lake 1660-02-07-.16 Land Between the Lakes 1660-02-07-.35 Wolf River Embayment (Mud Island 1660-02-07-.17 Cheatham Reservoir Harbor) 1660-02-07-.18 Tellico Reservoir 1660-02-07-.36 Public Facilities 1660-02-07-.19 Nickajack Reservoir 1660-02-07-.37 Repealed 1660-02-07-.01 REPEALED.