February 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

February 2019

UNITED STATES – February 2019 Contents USA - THE PROBLEM WITH PROPERTY TAXES......................................................................................................... 3 USA - LESSONS FROM AMAZON'S DECISION TO CANCEL NEW YORK CITY HEADQUARTERS ................................... 4 USA - SANDERS’ ESTATE TAX PLAN WON’T LIKELY RAISE THE REVENUE INTENDED ............................................... 6 USA - HOW BIG-BOX STORES BILK LOCAL GOVERNMENTS ..................................................................................... 6 USA - THESE MAJOR U.S. CITIES ARE SEEING PROPERTY TAX INCREASES THIS YEAR .............................................. 8 USA - THUNE LEADS COLLEAGUES IN REINTRODUCING A PERMANENT REPEAL TO THE ESTATE TAX ..................... 9 USA - SANDERS PROPOSES ESTATE TAX OF UP TO 77 PERCENT FOR BILLIONAIRES ................................................ 9 USA - THE SELF-STORAGE PROPERTY-TAX CONUNDRUM: ALTERNATIVES TO BETTER OUR COMMUNITIES ........ 10 CALIFORNIA ................................................................................................................................................................. 12 PROP 13 SPLIT-ROLL TAX INCREASE WOULD HURT BUSINESS, AND AFFORDABLE HOUSING EFFORTS ................. 12 CALIFORNIA BUSINESSES SHOULD REJECT EFFORTS LEVERAGING THREAT OF SPLIT ROLL FOR OTHER TAX HIKES 13 CHANGING PROP. 13 COULD WORSEN CALIFORNIA’S HOUSING CRISIS. HERE’S HOW ......................................... 14 HAWAII ....................................................................................................................................................................... -

Paul Bettencourt an Open Letter to the Citizens of Senate District 7

T E X A S S T A T E S E N A T O R Paul Bettencourt An Open Letter to the Citizens of Senate District 7 COMMITTEES: CAPITOL ADDRESS INTERGOVERNMENTAL RELATIONS - VICE-CHAIR P.O. BOX 12068 EDUCATION AUSTIN, TEXAS 78711-2068 FINANCE (512) 463-0107 HIGHER EDUCATION FAX: (512) 463-8810 SENATOR PAUL BETTENCOURT DISTRICT 7 Dear Friends and Neighbors, It is my privilege to represent you in the Texas Senate. The interim since the 84th Texas Legislature adjourned last session has been busy, as the Lieutenant Governor assigned the Senate nearly 100 interim public policy charges to study prior to the upcoming session. One of them was, of course, property tax reform and relief. I wanted to update you on what we accomplished in the last session as well as during the interim, and give you an overview of some of the priorities we will be addressing in the upcoming session. During my first legislative session in 2014, I served as chief Senate sponsor on 25 bills which gained legislative approval, earning me the distinction of “Freshman of the Year” by Capitol Inside. This legislation included passage of the Andrea Sloan “Right to Try” bill, allowing terminally ill Texas patients access to drugs still in the FDA’s approval pipeline. In fact, Houston physician Ebrahim S. Delpassand stated before the United States Senate Committee on Homeland Security and Governmental Affairs that he is using the state’s “Right to Try” Act to successfully treat about 80 patients. I also added an amendment to SB 1760 requiring a 60% supermajority within a taxing jurisdiction to increase property taxes over the effective rate. -

Salado What Does It Mean to Be from Salado?

Salado Villageillage Voiceoice VOL. XLI, NUMBER 44 VTHURSDAY, FEBRUARY 14, 2019 254/947-5321 V SALADOviLLAGEVOICE.COM 50¢ SISD trustees approve contracts for bond BY TIM FLEISCHER concession stands and mov- wastewater to the campus EDitOR-in-CHIEF ing a 200-seat section of is $1.15 million, which will stands from the home side to leave about $800,000 in con- Salado school trustees the visitors’ side of the stadi- tingency in the $49.4 million awarded bids at their Feb. um. Also bidding were STR bond budget. 11 meeting to Chaney-Cox Construction at $2.7 million In other business, trustees construction for construc- and Built Wright at $2.6 mil- approved $99,336 for the ad- tion of the Thomas Arnold lion. Chaney-Cox was also dition of 449 stadium seats Elementary corridor and the top qualified bidder ac- for the home side of the Eagle football stadium work and to cording to the ranking com- stadium. This will expand Lee Lewis Construction for mittee. Trustees approved the stadium by 249 seats on construction of the Middle an additional $28,000 in al- the home side (because 200 School and baseball and ternates for construction of seats are being moved to the softball fields on Williams a covered vestibule for the visitor side) and 200 seats on Rd. TAE Corridor. the visitor side of the stadi- Darrell Street gave the Trustees also approved um. This will come from the motion to select Lee Lewis add-ons for the work. The bond budget as well. This Construction as the contrac- board approved $1.7 mil- proposal comes through the tor and authorize the super- lion in additional work at the BuyBoard program. -

2019-2020 PAC Contributions

2019-2020 Election Cycle Contributions State Candidate or Committee Name Party -District Total Amount ALABAMA Sen. Candidate Thomas Tuberville R $5,000 Rep. Candidate Jerry Carl R-01 $2,500 Rep. Michael Rogers R-03 $1,500 Rep. Gary Palmer R-06 $1,500 Rep. Terri Sewell D-07 $10,000 ALASKA Sen. Dan Sullivan R $3,800 Rep. Donald Young R-At-Large $7,500 ARIZONA Sen. Martha McSally R $10,000 Rep. Andy Biggs R-05 $5,000 Rep. David Schweikert R-06 $6,500 ARKANSAS Sen. Thomas Cotton R $7,500 Rep. Rick Crawford R-01 $2,500 Rep. French Hill R-02 $9,000 Rep. Steve Womack R-03 $2,500 Rep. Bruce Westerman R-04 $7,500 St. Sen. Ben Hester R-01 $750 St. Sen. Jim Hendren R-02 $750 St. Sen. Lance Eads R-07 $750 St. Sen. Milton Hickey R-11 $1,500 St. Sen. Bruce Maloch D-12 $750 St. Sen. Alan Clark R-13 $750 St. Sen. Breanne Davis R-16 $500 St. Sen. John Cooper R-21 $750 St. Sen. David Wallace R-22 $500 St. Sen. Ronald Caldwell R-23 $750 St. Sen. Stephanie Flowers D-25 $750 St. Sen. Eddie Cheatham D-26 $750 St. Sen. Trent Garner R-27 $750 St. Sen. Ricky Hill R-29 $500 St. Sen. Jane English R-34 $1,500 St. Rep. Lane Jean R-02 $500 St. Rep. Danny Watson R-03 $500 St. Rep. DeAnn Vaught R-04 $500 St. Rep. David Fielding D-05 $500 St. Rep. Matthew Shepherd R-06 $1,000 St. -

Senate Criminal Justice Committee (84Th)

2904 Floyd, Suite A | Dallas, TX 74204 | 214-442-1672 | www.texprotects.org Senate Criminal Justice Committee (84th) Clerk: Jessie Cox Phone: 512-463-0345 Room: SBH 470 Name Party Room Number Phone Number (top is Other Committees capitol number and bottom is district number) Chair Sen. John D CAP 1E.13 (512)-463-0115 Business & Commerce; Whitmire (Houston) (713)-864-8701 Finance Vice Chair Sen. Joan R CAP 1E.15 (512)-463-0117 Finance; State Affairs (Vice Huffman (Houston) (218)-980-3500 Chair) Sen. Konnie Burton R CAP GE.7 (512)-463-0110 Higher Education; Nominations; Veteran Affairs & Military Installations (Vice Chair) Sen. Brandon R EXT E1.606 (512)-463-0104 Agriculture, Water & Rural Creighton Affairs; Business & Commerce (Vice Chair); State Affairs Sen. Juan Hinojosa D CAP 3E.10 (512)-463-0120 Agriculture, Water & Rural (McAllen) (956)-972-1841 Affairs; Finance (Vice Chair); Natural Resources & Economic Development Sen. Charles Perry R EXT E1.810 (512)-463-0128 Agriculture, Water & Rural (Lubbock) (806)-783-9934 Affairs (Chair); Health & Human Services; Higher Education Sen. Leticia Van de D CAP 3S.3 (512)-463-0126 Higher Education; Putte (San Antonio) (210)-733-6604 Intergovernmental Relations Senate Education Committee (84th) Clerk: Holly Mabry McCoy Phone: 512-463-0355 Room: SBH 440 Name Party Room Number Phone Number Other Committees Sen. Larry Taylor R CAP GE.5 512-463-0111 Business & Commerce; Finance; (Pearland) 281-485-9800 Intergovernmental Relations Vice Chair Sen. Eddie D CAP 3S.5 512-463-0127 Intergovernmental Relations Lucio, Jr (Brownsville) 956-548-0227 (Chair); Natural Resources & Economic Development; Veteran Affairs & Military Installations; Veteran Affairs & Military Installations-S/C Border Security Sen. -

IDEOLOGY and PARTISANSHIP in the 87Th (2021) REGULAR SESSION of the TEXAS LEGISLATURE

IDEOLOGY AND PARTISANSHIP IN THE 87th (2021) REGULAR SESSION OF THE TEXAS LEGISLATURE Mark P. Jones, Ph.D. Fellow in Political Science, Rice University’s Baker Institute for Public Policy July 2021 © 2021 Rice University’s Baker Institute for Public Policy This material may be quoted or reproduced without prior permission, provided appropriate credit is given to the author and the Baker Institute for Public Policy. Wherever feasible, papers are reviewed by outside experts before they are released. However, the research and views expressed in this paper are those of the individual researcher(s) and do not necessarily represent the views of the Baker Institute. Mark P. Jones, Ph.D. “Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature” https://doi.org/10.25613/HP57-BF70 Ideology and Partisanship in the 87th (2021) Regular Session of the Texas Legislature Executive Summary This report utilizes roll call vote data to improve our understanding of the ideological and partisan dynamics of the Texas Legislature’s 87th regular session. The first section examines the location of the members of the Texas Senate and of the Texas House on the liberal-conservative dimension along which legislative politics takes place in Austin. In both chambers, every Republican is more conservative than every Democrat and every Democrat is more liberal than every Republican. There does, however, exist substantial ideological diversity within the respective Democratic and Republican delegations in each chamber. The second section explores the extent to which each senator and each representative was on the winning side of the non-lopsided final passage votes (FPVs) on which they voted. -

MICROCOMP Output File

S. HRG. 105±819 ESTUARY RESTORATION AND COASTAL WATER CONSERVATION LEGISLATION HEARING BEFORE THE COMMITTEE ON ENVIRONMENT AND PUBLIC WORKS UNITED STATES SENATE ONE HUNDRED FIFTH CONGRESS SECOND SESSION JULY 9, 1998 ON S. 1222 A BILL TO CATALYZE RESTORATION OF ESTUARY HABITAT THROUGH MORE EFFICIENT FINANCING OF PROJECTS AND ENHANCED COORDI- NATION OF FEDERAL AND NON-FEDERAL RESTORATION PROGRAMS, AND FOR OTHER PURPOSES S. 1321 A BILL TO AMEND THE FEDERAL WATER POLLUTION CONTROL ACT TO PERMIT GRANTS FOR THE NATIONAL ESTUARY PROGRAM TO BE USED FOR THE DEVELOPMENT AND IMPLEMENTATION OF A COMPREHENSIVE CONSERVATION AND MANAGEMENT PLAN, TO REAUTHORIZE APPROPROPRIATIONS TO CARRY OUT THE PROGRAM, AND FOR OTHER PURPOSES H.R. 2207 AN ACT TO AMEND THE FEDERAL WATER POLLUTION CONTROL ACT CONCERNING A PROPOSAL TO CONSTRUCT A DEEP OCEAN OUTFALL OFF THE COAST OF MAYAGUEZ, PUERTO RICO ( U.S. GOVERNMENT PRINTING OFFICE 52±625 CC WASHINGTON : 1999 For sale by the U.S. Government Printing Office Superintendent of Documents, Congressional Sales Office, Washington DC 20402 COMMITTEE ON ENVIRONMENT AND PUBLIC WORKS ONE HUNDRED FIFTH CONGRESS JOHN H. CHAFEE, Rhode Island, Chairman JOHN W. WARNER, Virginia MAX BAUCUS, Montana ROBERT SMITH, New Hampshire DANIEL PATRICK MOYNIHAN, New York DIRK KEMPTHORNE, Idaho FRANK R. LAUTENBERG, New Jersey JAMES M. INHOFE, Oklahoma HARRY REID, Nevada CRAIG THOMAS, Wyoming BOB GRAHAM, Florida CHRISTOPHER S. BOND, Missouri JOSEPH I. LIEBERMAN, Connecticut TIM HUTCHINSON, Arkansas BARBARA BOXER, California WAYNE ALLARD, Colorado RON WYDEN, Oregon JEFF SESSIONS, Alabama JIMMIE POWELL, Staff Director J. THOMAS SLITER, Minority Staff Director (II) CONTENTS Page JULY 9, 1998 OPENING STATEMENTS Chafee, Hon. -

Writing the State Budget: 87Th Legislature

March 8, 2021 No. 87-1 FOCUS on State Finance Initial budget development 1 Writing the state budget Writing and passing a biennial budget 2 Writing a budget is one of the Texas Legislature’s main tasks. The state’s budget is written General appropriations and implemented in a two-year cycle that includes development of the budget, passage of the bill 4 general appropriations act, actions by the comptroller and governor, and interim monitoring. During the 2021 regular session, the 87th Legislature will consider a budget for fiscal 2022- Legislative action 5 23, the two-year period from September 1, 2021, through August 31, 2023. Action after final passage 7 Initial budget development Interim budget action 7 Developing the budget begins with state agencies receiving instructions for submitting budget requests. Agencies then submit their budget proposals, and hearings are held on Restrictions on spending 8 their requests. Next, the Legislative Budget Board (LBB) adopts a growth rate that limits appropriations, the comptroller issues an estimate of available revenue, and preliminary budgets are drafted. Pre-session budget instructions and hearings. State agencies are required in even- numbered years to develop five-year strategic plans (Government Code sec. 2056.002) that include agency goals, strategies for accomplishing those goals, and performance measures. Before a regular legislative session begins, agencies submit funding requests to the governor’s budget office and the LBB. These requests are called Legislative Appropriations Requests, or LARs. The LARs have two parts: the base-level request and requests for exceptional items beyond the baseline. In August 2020, state agencies were instructed to submit spending requests with base funding equal to their adjusted fiscal 2020-21 base. -

Member-Directory.Pdf

2018 – 2019 MEMBER DIRECTORY P.O. Box 16550 Sugar Land, TX 77496-6550 1650 Highway 6, Suite 460 Sugar Land, TX 77478 (281) 980-3434 Fax: (281) 980-2608 [email protected] www.houstoncardealers.com Open to the public January 23 - January 27, 2019 www.houstonautoshow.com TABLE OF CONTENTS NATIONAL, STATE & METRO ASSOCIATIONS ......................................................................... 2 HADA STAFF...................................................................................................................... 3 BOARD OF DIRECTORS - OFFICERS ............................................................................. 4 BOARD OF DIRECTORS - DIRECTORS .......................................................................... 5 HADA PAST CHAIRMEN ................................................................................................... 6 MEMBER SERVICES ......................................................................................................... 7 HADA PICTURES ............................................................................................................... 14 DEALER MEMBER LISTING ............................................................................................. 19 DEALER MEMBERS BY MANUFACTURER .................................................................... 51 ASSOCIATE MEMBER LISTING ....................................................................................... 60 ASSOCIATE MEMBERS BY PRODUCTS OR SERVICES .............................................. -

Legislative Staff: 87Th Legislature

HRO HOUSE RESEARCH ORGANIZATION Texas House of Representatives Legislative Staff 87th Legislature 2021 Focus Report No. 87-2 House Research Organization Page 2 Table of Contents House of Representatives ....................................3 House Committees ..............................................15 Senate ...................................................................18 Senate Committees .............................................22 Other State Numbers...........................................24 Cover design by Robert Inks House Research Organization Page 3 House of Representatives ALLEN, Alma A. GW.5 BELL, Cecil Jr. E2.708 Phone: (512) 463-0744 Phone: (512) 463-0650 Fax: (512) 463-0761 Fax: (512) 463-0575 Chief of staff ...........................................Anneliese Vogel Chief of staff .............................................. Ariane Marion Legislative director ................................. Adoneca Fortier Legislative aide......................................Joshua Chandler Legislative aide.................................... Sarah Hutchinson BELL, Keith E2.414 ALLISON, Steve E1.512 Phone: (512) 463-0458 Phone: (512) 463-0686 Fax: (512) 463-2040 Chief of staff .................................................Rocky Gage Chief of staff .................................... Georgeanne Palmer Legislative director/scheduler ...................German Lopez Legislative director ....................................Reed Johnson Legislative aide........................................ Rebecca Brady ANCHÍA, Rafael 1N.5 -

Texas House of Representatives Contact Information - 2017 Representative District Email Address (512) Phone Alma A

Texas House of Representatives Contact Information - 2017 Representative District Email Address (512) Phone Alma A. Allen (D) 131 [email protected] (512) 463-0744 Roberto R. Alonzo (D) 104 [email protected] (512) 463-0408 Carol Alvarado (D) 145 [email protected] (512) 463-0732 Rafael Anchia (D) 103 [email protected] (512) 463-0746 Charles "Doc" Anderson (R) 56 [email protected] (512) 463-0135 Rodney Anderson (R) 105 [email protected] (512) 463-0641 Diana Arévalo (D) 116 [email protected] (512) 463-0616 Trent Ashby (R) 57 [email protected] (512) 463-0508 Ernest Bailes (R) 18 [email protected] (512) 463-0570 Cecil Bell (R) 3 [email protected] (512) 463-0650 Diego Bernal (D) 123 [email protected] (512) 463-0532 Kyle Biedermann (R) 73 [email protected] (512) 463-0325 César Blanco (D) 76 [email protected] (512) 463-0622 Dwayne Bohac (R) 138 [email protected] (512) 463-0727 Dennis H. Bonnen (R) 25 [email protected] (512) 463-0564 Greg Bonnen (R) 24 [email protected] (512) 463-0729 Cindy Burkett (R) 113 [email protected] (512) 463-0464 DeWayne Burns (R) 58 [email protected] (512) 463-0538 Dustin Burrows (R) 83 [email protected] (512) 463-0542 Angie Chen Button (R) 112 [email protected] (512) 463-0486 Briscoe Cain (R) 128 [email protected] (512) 463-0733 Terry Canales (D) 40 [email protected] (512) 463-0426 Giovanni Capriglione (R) 98 [email protected] (512) 463-0690 Travis Clardy (R) 11 [email protected] (512) 463-0592 Garnet Coleman (D) 147 [email protected] (512) 463-0524 Nicole Collier (D) 95 [email protected] (512) 463-0716 Byron C. -

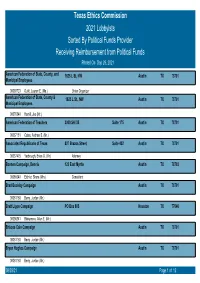

Texas Ethics Commission 2021 Lobbyists Receiving

Texas Ethics Commission 2021 Lobbyists Sorted By Political Funds Provider Receiving Reimbursement from Political Funds Printed On Sep 29, 2021 American Federation of State, County, and 1625 L St, NW Austin TX 78701 Municipal Employees 00085723 Guild, Lauren E. (Ms.) Union Organizer American Federation of State, County & 1625 L St., NW Austin TX 78701 Municipal Employees 00070846 Hamill, Joe (Mr.) American Federation of Teachers 3000 SH I35 Suite 175 Austin TX 78701 00067181 Cates, Andrew S. (Mr.) Associated Republicans of Texas 807 Brazos Street Suite 402 Austin TX 78701 00037475 Yarbrough, Brian G. (Mr.) Attorney Bonnen Campaign, Dennis 122 East Myrtle Austin TX 78703 00085040 Eichler, Shera (Mrs.) Consultant Brad Buckley Campaign Austin TX 78701 00061160 Berry, Jordan (Mr.) Brett Ligon Campaign PO Box 805 Houston TX 77046 00056241 Blakemore, Allen E. (Mr.) Briscoe Cain Campaign Austin TX 78701 00061160 Berry, Jordan (Mr.) Bryan Hughes Campaign Austin TX 78701 00061160 Berry, Jordan (Mr.) 09/29/21 Page 1 of 12 Buckingham Campaign, Dawn P.O. Box 342524 Austin TX 78701 00055627 Blocker, Trey J. (Mr.) Attorney Burrows Campaign, Dustin P.O. Box 2569 Austin TX 78703 00085040 Eichler, Shera (Mrs.) Consultant Capriglione, Giovanni (Rep.) 1352 Ten Bar Trail AUSTIN TX 78767 00068846 Lawson, Drew (Mr.) Lobby Charles "Doc" Anderson Campaign P.O. Box 7752 Austin TX 78747 00053964 Smith, Todd M. (Mr.) Impact Texas Communicaions, LLP Charles Perry Campaign Austin TX 78701 00061160 Berry, Jordan (Mr.) Claudia Ordaz Perez for Texas PO Box 71738 El Paso TX 79943 00053635 Smith, Mark A. (Mr.) Lobbyist Cody Vasut Campaign Austin TX 78701 00061160 Berry, Jordan (Mr.) Cole Hefner Campaign Austin TX 78701 00061160 Berry, Jordan (Mr.) Contaldi, Mario (Dr.) 7728 Mid Cities Blvd Austin TX 78705 00012897 Avery, Bj (Ms.) Texas Optometric Asso.