Pakistan Banking Perspective 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Habib Metropolitan Bank Limited 2

The Pakistan Credit Rating Agency Limited Rating Report Report Contents 1. Rating Analysis Habib Metropolitan Bank Limited 2. Financial Information 3. Rating Scale 4. Regulatory and Supplementary Disclosure Rating History Dissemination Date Long Term Rating Short Term Rating Outlook Action Rating Watch 25-Jun-2021 AA+ A1+ Stable Maintain - 26-Jun-2020 AA+ A1+ Stable Maintain - 27-Dec-2019 AA+ A1+ Stable Maintain - 27-Jun-2019 AA+ A1+ Stable Maintain - 27-Dec-2018 AA+ A1+ Stable Maintain - 28-Jun-2018 AA+ A1+ Stable Maintain - 30-Dec-2017 AA+ A1+ Stable Maintain - 23-Jun-2017 AA+ A1+ Stable Maintain - 23-Jun-2016 AA+ A1+ Stable Maintain - Rating Rationale and Key Rating Drivers The ratings of Habib Metropolitan Bank (HabibMetro) is vested in the brand strength of the Bank, flanked by a family of astute bankers. The Bank is also associated with a diversified and financially strong international bank - Habib Bank AG Zurich (HBZ). This association helps in assimilating the parent's best practices into HabibMetro, while fostering control environment with enhanced level of oversight. The Bank has a formidable presence in the trade business of Pakistan. The benefits continue to accrue in terms of non-markup income. The Bank has a strong forte in the business hub of Pakistan in terms of its presence and contribution of deposits and advances. The Bank grew its customers deposit base by 19.5%, wherein it enhanced its current account deposits by 25.7%, higher than the sector's growth. The Bank continues to remain focused on improving its deposit mix. The Bank’s emphasis in terms of its loan portfolio is evident by the growth of 18.6% in net advances, led by its presence in textile and commodity finance segments. -

The F Ederalisation of Cooperative Banking in Pakistan and Rural Cooperatives in Punjab Province

Institute of Social Studies The F ederalisation of Cooperative Banking in Pakistan and Rural Cooperatives in Punjab Province Farooq Haroon Occasional Paper No. 103 The F ederalisation of Cooperative Banking in Pakistan and Rural Cooperatives in Punjab Province Farooq Haroon January 1986 Institute of Social Studies The views expressed in this publication are those of the author and not necessarily those of the Institute of Social Studies. © Institute of Social Studies The Hague, 1986 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior permis sion of the copyright owner. ISBN 90-6490-020-5 . Printed in The Netherlands 1. INTRODUCTION Pakistan The creation of Pakistan on 14 August 1947 was the result of the irresistible and massive pressure of Muslim nationalism. The British colonial govern ment, despite its initial reservations on the practicability and soundness of the demand, came around to the viewpoint of the Muslims and agreed to partition India. The Pakistan that came into being had two geographical units separated by 1,600 miles ofIndian territory. The Eastern Wing became the independent Republic of Bangladesh at the end of 1971. Pakistan now comprises the West Wing of the Pakistan created in 1947. The territory of Pakistan now covers 796,095 square kilometres. It borders on Iran to the southwest, Afghanistan to the northwest and India to the east. The southern border is the coast of the Arabian Sea. In 19~1, the estimated population was 83.78 million. -

Pakistan's Islamic Banking Sector Review

Pakistan’s Islamic Banking Sector Review 2003 to 2007 ISLAMIC BANKING DEPARTMENT STATE BANK OF PAKISTAN Table of Contents 1. Vision & Mission Statements of State Bank of Pakistan (SBP) ................................................ III 2. Vision & Mission Statements of Islamic Banking Department of SBP.................................... III 3. Governor’s Message ...................................................................................................................... IV 4. Foreword ........................................................................................................................................ VI 5. Executive Summary .................................................................................................................... VII 6. Future Outlook .............................................................................................................................. IX 7. Brief Historical Perspective on Islamic Banking Initiatives in Pakistan ................................... 1 7.1 Steps for Islamization of Banking and Financial System in 1980s ............................................ 1 7.2 Brief Evaluation .......................................................................................................................... 2 7.3 Post Judgment Measures ............................................................................................................. 3 7.4 Policy Decision .......................................................................................................................... -

IBFT- Account Number Formats

IBFT- Account Number Formats Allied Bank Please enter Allied Bank Account Number by following the layout below: Total Digits of Account Number: 13 or 20 Digits Format Example: BBBBAAAAAAAAA or BBBBAAAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 9 Digit Account Number, AAAAAAAAAAAAAAAA = 16 Digit Account Number Apna Microfinance Bank Please enter Apna Microfinance Bank Account Number by following the layout below: Total Digits of Account Number: 16 Digits Format Example: BBBBAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAA = 12 Digits Askari Bank Please enter Askari Bank Account Number by following the layout below: Total Digits of Bank Account Number: 14 Digits Format Example: BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Branchless Banking Account # Always consist of 11 digits Mobile Number. Al-Baraka Please enter Bank Al-Baraka total digits of account Number: Total Digits of Account Number: 13 Digits Bank Alfalah Please enter Bank Alfalah Account Number by following the layout below: Conventional A/C#: Total Digits of Account Number: 14 Format Example: BBBBAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAA = 10 Digit Account Number Islamic A/C#: Total Digits of Account Number: 18 Digit Format Example: BBBBAAAAAAAAAAAAAA BBBB = 4 Digit Branch Code, AAAAAAAAAAAAAA = 14 Digit Account Number Branchless Banking Account # : Always consist of 11 digits Mobile Number. Bank Al-Habib Please enter Bank Al-Habib Account Number by following the layout below: Total Digits of Account Number: 17 Digit Format -

State Bank of Pakistan I.I. Chundrigarh Road Karachi KHI001 United Bank Ltd

State Bank of Pakistan I.I. Chundrigarh Road Karachi KHI001 United Bank Ltd. NEAR BALOCH COLONY BUS STOP Karachi KHI003 United Bank Ltd. RAFIH E AAM SOCIETY Karachi KHI004 BankIslami Ltd. DHA PHASE-2 Karachi KHI005 Allied Bank Ltd. SCHEME-36,GULISTAN-E-JOHAR, UNI ROAD Karachi KHI006 United Bank Ltd. STOCK EXCHANGE BLDG.I.I.CHUNDRIGAR Karachi KHI007 Allied Bank Ltd. SADDAR BAZAR QUARTER, ZAIB UN NISA St Karachi KHI008 Allied Bank Ltd. WEST WHARF DOCKYARD ROAD, Karachi KHI009 Askari Bank Ltd. ASKARI BANK LTD., MALIR CANTT BRANCH Karachi KHI010 Faysal Bank Ltd. Q-14, Sector 33-A, Korangi # 2 (209) Karachi KHI011 HBL LASBELA Karachi KHI012 HBL SHIREEN JINNAH Karachi KHI013 Habib Metropolitan North Western Zone Prt Qasim Karachi KHI014 Bank Ltd. Askari Bank Ltd. Guslah-e-Iqbal Branch Karachi KHI015 Meezan Bank Ltd. Opp Jungle Shah College, Kemari Town Karachi KHI016 Bank Al Habib Ltd. Malir Halt Railway Stn,Shahrah Faisal Karachi KHI017 Bank Al Habib Ltd. Near Siemens Chowrangi, S.I.T.E Karachi KHI018 Silk Bank Ltd. KCHS bahadurabad karachi Karachi KHI019 Bank Al Habib Ltd. Rashid Minhas,Block B Gulshan-e-Jamal Karachi KHI020 Bank Al Habib Ltd. Speedy Towers, Phase-I, DHA Karachi KHI021 Bank Al Habib Ltd. Block 17 KDA36,Shalimar Center,Jauhar Karachi KHI022 BankIslami Ltd. 13-C, GULSHAN E IQBAL UNIVERSIITY ROAD Karachi KHI023 BankIslami Ltd. I I CHUNDRIGAR ROAD, Karachi KHI024 Bank Al Habib Ltd. Block 13A, Uni Road Gulshan Iqbal Karachi KHI025 BankIslami Ltd. BLOCK-15 KDA SCHEME 36,GULISTAN-E-JOHER Karachi KHI026 Faysal Bank Ltd. ST - 02, Main Shahrah-e-Faisal (110) Karachi KHI027 MCB Bank Ltd MCB Shah Faisal Colony Branch No. -

Banking Survey 2016

kpmg KPMG Taseer Hadi & Co. Chartered Accountants Banking Survey 2016 Commercial Banks Operating in Pakistan © 2017 KPMG Taseer Hadi & Co., a Partnership firm registered in Pakistan and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. p Banking Survey 2016 © 2017 KPMG Taseer Hadi & Co., a Partnership firm registered in Pakistan and a member firm of the KPMG network of independent ii member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Banking Survey 2016 This survey has been prepared by KPMG Taseer Hadi & Co. and summarizes the performance of selected commercial banks in Pakistan for the year ended 31 December 2016. Banking sector in Pakistan has been divided in four categories for the purpose of this survey to facilitate comparison of peer groups: I. Large Banks: Total assets in excess of Rs. 900 billion. II. Medium size Banks: Total assets in excess of Rs. 150 billion but less than Rs. 900 billion. III. Small Banks: Total assets less than Rs. 150 billion. IV. Islamic Banks: All banks carrying out Islamic banking activities only. “Islamic Banks” have been presented as a separate category and included in their respective category of Medium and Small Banks based on total assets threshold. Further, summarized financial information of “Islamic Banking Branches of Conventional Banks” has also been presented to have an idea about size of Islamic Banking in Pakistan. Reference should be made to the published financial statements of the banks and definitions included in this survey to enhance the understanding of ratios and analysis of performance of a particular bank. -

Wide Screen Template

KPMG Taseer Hadi & Co. Chartered Accountants Snapshot of results ofBanks inPakistan Snapshot of results of banks in Pakistanfor the six months period ended 30 June2019 This snapshot has been prepared by KPMG Taseer Hadi & Co. and summarizes the performance of selected commercial banks in Pakistan for the six months period ended 30 June 2019. The information contained in this snapshot has been obtained from the published interim consolidated financial statements of the banks. Reference should be made to the published interim financial statements of the banks to enhance the understanding of ratios and analysis of performance of a particular bank. The interim financial statements of Summit Bank and First Woman Bank Limited were not published till the date of our publication, and accordingly their results are not included in this snapshot. We have tried to provide relevant financial analysis of the banks which we thought would be useful for benchmarking and comparison. However, we welcome any comments, which would facilitate in improving the contents of this document. The comments may be sent at [email protected] Dated: 25 September 2019 Karachi © 2019 KPMG Taseer Hadi & Co., a Partnership firm registered in Pakistan and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rightsreserved. 2 HBL NBP UBL MCB ABL BAH Meezan 2019 2018 2019 2018 2019 2018 2019 2018 2019 2018 2019 2018 2019 2018 Ranking By total assets 1 1 2 2 3 3 4 4 5 5 6 6 7 -

IBFT Guideline

MCB Bank Limited IBFT- Guidelines 1. Al Baraka Bank (Pakistan) Limited Please enter Bank Al-Baraka total digits of account Number: Total Digits of Account Number: 13 Digits Format Example: AAAAAAAAAAAAA Note: A = Account Number 2. Allied Bank Limited Please enter Allied Bank Account Number by following the layout below: Total Digits of Account Number: 13 or 20 Digits Format Example: BBBBAAAAAAAAA or BBBBAAAAAAAAAAAAAAAA Note: B = Branch Code, A = Account Number 3. APNA Microfinance Bank Please enter APNA Microfinance Bank Account Number by following the layout below: Total Digits of Account Number: 16 Digits Format Example: BBBBAAAAAAAAAAAA Note: B = Branch Code, A = Account Number 4. Askari Bank Limited Please enter Askari Bank Account Number by following the layout below: For Branch Banking: Total Digits of Bank Account Number: 14 Digits Format Example: BBBBAAAAAAAAAA Note: B = Branch Code, A = Account Number For Branchless Banking: Total Digits of Bank Account Number: 11 Digits Format Example: 03XXXXXXXXX 5. Bank Al-Habib Limited Please enter Bank Al-Habib Account Number by following the layout below: Total Digits of Account Number: 17 Digits Format Example: BBBBTTTTBBBBBBRRC Note: B = Branch Code, A = Account Number, T = Account Type, BBBB= Base Number, RR = Digit Running Number, C = Check Digit 111 000 622 mcb.com.pk /MCBBankPk Over 1350 Branches & ATMs 6. Bank Al-Falah Limited Please enter Bank Al-Falah Account Number by following the layout below: For Conventional Banking: Total Digits of Account Number: 14 Digits Format Example: BBBBAAAAAAAAAA Note: B = Branch Code, A = Account Number For Islamic Banking: Total Digits of Account Number: 18 Digits Format Example: BBBBAAAAAAAAAAAAAA Note: B = Branch Code, A = Account Number For Branchless Banking: Total Digits of Account Number: 11 Digits Format Example: 03XXXXXXXXX 7. -

The Importance of Islamic Finance for Pakistan and the Challenges Ahead

Governor : Mr. Tariq Bajwa Title : Governor SBP’s Address to the Launching Ceremony of AAOIFI Shariah Standards – Urdu Version Date : December 12, 2018 Event : Launching Ceremony of AAOIFI Shariah Standards – Urdu Version Venue : Marriott Hotel Karachi. - Shaikh Ebrahim Bin Khalifa Al Khalifa, Chairman, Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI) - Mufti Taqi Usmani, Chairman Shariah Board, AAOIFI - Distinguished speakers, ladies and gentlemen Assalam-o-Alaikum and Good Morning! I feel honored to be here on this important occasion of launch of Urdu version of AAOIFI’s Shariah Standards. We are all aware that national language is an important ingredient of any culture and most effective mode of communication in a country. With this in perspective, translation of global standards into our national language is an important milestone, as it would remove language barriers to understand Shariah Standards. I believe this Urdu version of the Shariah Standards will be instrumental in improving awareness about Islamic finance especially amongst the Shariah scholars, academia and practitioners of Islamic finance. The scholars and all other experts involved in this project deserve great appreciation for their commendable role. As we are all aware, Islamic Finance Industry is relatively new to the Global Financial Landscape. Events like these are important not only for dissemination and awareness but also reinforce the emerging significance of fast growing Islamic Finance. Page 1 of 6 Ladies & Gentlemen! Islamic banking started initially as a niche market for the faith sensitive clientele and is now increasingly becoming an integral component of global financial system. Islamic finance industry has grown at a fast pace. -

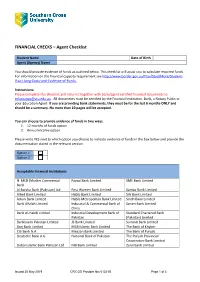

FINANCIAL CHECKS – Agent Checklist

FINANCIAL CHECKS – Agent Checklist Student Name Date of Birth Agent (Agency) Name You should provide evidence of funds as outlined below. This checklist will assist you to calculate required funds. For information on the financial capacity requirement see http://www.border.gov.au/Trav/Stud/More/Student- Visa-Living-Costs-and-Evidence-of-Funds. Instructions: Please complete this checklist and return it together with bank/agent certified financial documents to [email protected] . All documents must be certified by the Financial Institution, Bank, a Notary Public or your Education Agent. If you are providing bank statements, they must be for the last 6 months ONLY and should be a summary. No more than 10 pages will be accepted. You can choose to provide evidence of funds in two ways. 1. 12 months of funds option 2. Annual income option Please write YES next to which option you choose to indicate evidence of funds in the box below and provide the documentation stated in the relevant section. Option 1 Option 2 Acceptable Financial Institutions N MCB (Muslim Commercial Faysal Bank Limited SME Bank Limited Bank Al Baraka Bank (Pakistan) Ltd First Women Bank Limited Samba Bank Limited Allied Bank Limited Habib Bank Limited Silk Bank Limited Askari Bank Limited Habib Metropolitan Bank Limited Sindh Bank Limited Bank Alfalah Limited Industrial & Commercial Bank of Soneri Bank Limited China Bank Al-Habib Limited Industrial Development Bank of Standard Chartered Bank Pakistan (Pakistan) Limited BankIslami Pakistan Limited JS Bank Limited Summit -

Islamization of Financial System in Pakistan

10 Islamization of Financial System in Pakistan Islamic banking has been defined as banking in consonance with the ethos and value system of Islam and governed by the principles and rules laid down by Islamic Shariah. Interest free banking is a narrow concept denoting a number of banking instruments or operations, which avoid interest. Islamic banking, the more general term is expected not only to avoid interest-based transactions, prohibited in the Islamic Shariah, but also to participate actively in achieving the goals and objectives of an Islamic economy. Establishment of a small saving bank in a rural area of Egypt in 1963 was the first formal attempt for putting the principles of Islamic finance into practice. Islamic banking and finance is now an established sector and an important segment of the international financial market arena (see Box 10.1). Steps for Islamization of banking and financial system of Pakistan were started in 1977-78. Pakistan was among the three countries in the world that had been trying to implement interest free banking at comprehensive/national level. But as it was a mammoth task, the switchover plan was implemented in phases.1 An Ordinance was promulgated to allow the establishment of Mudaraba companies and floatation of Mudaraba certificates for raising risk capital. Amendments were also made in the Banking Companies Ordinance (BCO), 1962 to include provision of bank finance through PLS, mark- up in prices, leasing and hire purchase. Separate Interest-free counters started operating in all the nationalized commercial banks, and one foreign bank (Bank of Oman) on January 1, 1981 to mobilize deposits on profit and loss sharing basis. -

Assessing the Financial Performance of Investment Banks in Pakistan During the Current Financial Crisis

The Lahore Journal of Business 2 : 2 (Spring 2014): pp. 67–88 Assessing the Financial Performance of Investment Banks in Pakistan During the Current Financial Crisis Mirza Asjad Baig,* Muhammad Ali Usman,** Mirza Owais Baig*** Abstract Investment banks play a vital role in the economic development of a country through their impact on capital and money markets. In developing countries, they promote and support business investors in bringing about economic stability. The investment banking industry faced significant challenges as a result of the financial crisis in 2008. This study presents a detailed financial analysis of the recent performance of seven investment banks in Pakistan for the period 2007–11 with the help of financial ratios. The banks were assessed across several perspectives: profitability, efficiency, liquidity, leverage, and other financial measures such as institution size. Our findings show that all banks faced a significant squeeze on profitability, although the smaller banks performed better overall. This implies that successful performance does not necessarily depend on economies of scale. Keywords: Investment banks, financial ratios, financial crisis, economic instability. JEL classification: G32, G01, O16, G24. 1. Introduction The banking sector plays a vital role in the development and welfare of a society, and are especially important for a healthy economy among developed countries. During the 18th century, industries expanded their business and trading activities with the beginning of large-scale production. The banking industry became important in promoting business operations as an essential facility. In today’s global market, it is necessary for the banking sector to provide quality products/services and focus on customer satisfaction to augment its performance.