The Origins of the Market for Corporate Control

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Revisionist History of Regulatory Capture WILLIAM J

This chapter will appear in: Preventing Regulatory Capture: Special Interest . Influence and How to Limit it. Edited by Daniel Carpenter and David Moss. Copyright © 2013 The Tobin Project. Reproduced with the permission of Cambridge University Press. Please note that the final chapter from the Cambridge University Press volume may differ slightly from this text. A Revisionist History of Regulatory Capture WILLIAM J. NOVAK A Revisionist History of Regulatory Capture WILLIAM J. NOVAK PROFESSOR, UNIVERSITY OF MICHIGAN SCHOOL OF LAW The idea of regulatory capture has controlled discussions of economic regulation and regulatory reform for more than two generations. Originating soon after World War II, the so-called “capture thesis” was an early harbinger of the more general critique of the American regulatory state that dominated the closing decades of the 20th century. The political ramifications of that broad critique of government continue to be felt today both in the resilient influence of neoliberal policies like deregulation and privatization as well as in the rise of more virulent and populist forms of anti-statism. Indeed, the capture thesis has so pervaded recent assessments of regulation that it has assumed something of the status of a ground norm – a taken-for-granted term of art and an all-purpose social-scientific explanation – that itself frequently escapes critical scrutiny or serious scholarly interrogation. This essay attempts to challenge this state of affairs by taking a critical look at the emergence of regulatory capture theory from the perspective of history. After introducing a brief account of the diverse intellectual roots of the capture idea, this essay makes three interpretive moves. -

Daniel Drew and the Saratoga & Hudson River

MADE AVAILABLE BY THE GREENE COUNTY HISTORICAL SOCIETY'S VEDDER RESEARCH LIBRARY A PUBLICATION OF THE GREENE COUNTY HISTORICAL SOCIETY, INC. 90 County Route 42 Volume 36 Numbers 1+2 Coxsackie, N. Y. 12051 ISBN 0894-8135 Spring & Summer 2012 UNCLE DANIEL'S WHITE ELEPHANT: DANIEL DREW AND THE SARATOGA & HUDSON RIVER RAILROAD BY DANIEL W. BIGLER Daniel Drew, shown here in an engraving from the Library of Congress, represented the American romantic ideal of the self-made man, rising from humble beginnings to a position of great wealth and power. He worked in a number of fields over the years, ranging from cattle-driving to the stock market to steamboats and railroads. Over the years Drew frequently found himself involved with Cornelius Vanderbilt, and in 1864 a joint railroad venture between them would bring Drew to the town of Athens in Greene County. This venture, officially known as the Saratoga & Hudson River Railroad, would become known colloquially as the "White Elephant Railroad." Drew was a prime example of the larger-than-life Romantic hero (or anti-hero), who would do whatever was necessary to get ahead, while the "White Elephant" represented the grand dreams of one particular community. Its dramatic end served as a fitting symbol of the end of its era. continued on page 02 DOUBLE EDITION: SPRING & SUMMER 2012 TOGETHER! VEDDER RESEARCH LIBRARY 90 COUNTY ROUTE 42, COXSACKIE, NY 12051 MADE AVAILABLE BY THE GREENE COUNTY HISTORICAL SOCIETY'S VEDDER RESEARCH LIBRARY UNCLE DANIEL'S WHITE ELEPHANT ... from page 01 FROM BOY TO MAN the Sixty-First New York State Militia Daniel Drew was born on a farm in Carmel, Regiment. -

Phrenology, Physiognomy, and the Character of Big Business, 1895-1914 Coleman Sherry Undergraduate Senior Thesi

Corporate Heads: Phrenology, Physiognomy, and the Character of Big Business, 1895-1914 Coleman Sherry Undergraduate Senior Thesis Department of History Columbia University 29 March 2021 Seminar Advisor: Professor Samuel Roberts Second Reader: Professor Richard John Abstract In this thesis I argue that practical phrenology—a loose set of practices for reading character in heads, faces, and bodies—played an important and underappreciated role in the popular coverage of the large new corporations that emerged from the “Great Merger Movement” around the turn of the twentieth century. I suggest that the scope and pace of the transition from proprietor to corporate ownership created a crisis of economic representation, defined by a lack of stable, mature conventions for describing and illustrating the actual activities of the new consolidated firms. In this context, journalists and cartoonists borrowed from the wildly-popular practical phrenology and personalized the corporations, describing the firms as if they were the straightforward extensions of famous individual owners. Through a close, comparative reading of biographical profiles published in Fowler and Wells’ Phrenological Journal, McClure’s Magazine, and the muckraking cartoons of Puck, I document the trespass of phrenological methods, language, and assumptions into popular contexts and publications. This phrenological personalization allowed public commentators to publish powerful polemics focused on the character of the new firms, but obscured and distorted their true forms. Table -

The Robber Barons

The robber barons In a classic, The“ Age of Uncertainty”, the author, late economist John Kenneth Galbraith, writes on the robber buyers. “We turn now to how the rich were singled out for their success. It brings us inevitably to the railroads. Nothing in the last century, and nothing so far in this century, so altered the fortunes of so many people so suddenly as the American or Canadian railroad. The contractors who built it, those whose real estate was in its path, those who owned it, those who shipped by it and those who looted it could all get rich, some of them in a week. The only people connected with the railroads who were spared the burdens of wealth were those who laid the rails and ran the trains. Railroading in the last century was not a highly paid occupation, and it was also very dangerous. The casualty rates of those who ran the trains – the incidence of mutilation and death – approached that of a first-class war. The railroads got built. A great many honest men bent their efforts to their construction and operation; this should not be forgotten. But the business also attracted a legion of rascals. The latter were by far the best known, and they may well have been the most successful in enriching themselves. Spencer's natural selection operated excellently on behalf of scoundrels. Sometimes it tested one set against another. A railroad allowed for an interesting choice between two kinds of larceny-robbery of the customers and robbery of the stockholders. The most spectacular struggle occurred in the late eighteen-sixties between rival practitioners of these two basic arts. -

Hudson River Railroad

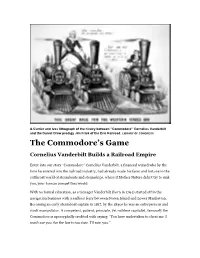

A Currier and Ives lithograph of the rivalry between “Commodore” Cornelius Vanderbilt and the Daniel Drew prodigy Jim Frisk of the Erie Railroad. LIBRARY OF CONGRESS The Commodore’s Game Cornelius Vanderbilt Builds a Railroad Empire Enter into our story “Commodore” Cornelius Vanderbilt, a financial wizard who by the time he entered into the railroad industry, had already made his fame and fortune in the cutthroat world of steamboats and steamships, where if Mother Nature didn’t try to sink you, your human competitors would. With no formal education, as a teenager Vanderbilt (born in 1794) started off in the navigation business with a sailboat ferry between Staten Island and Lower Manhattan. Becoming an early steamboat captain in 1817, by the 1830s he was an entrepreneur and stock manipulator. A competent, patient, principle, yet ruthless capitalist, famously the Commodore is apocryphally credited with saying: “You have undertaken to cheat me. I won't sue you, for the law is too slow. I'll ruin you.” The nickname “Commodore” came from Vanderbilt’s battles with the Hudson River steamboat monopolies, his eventual dominance of steam navigation in the Long Island Sound, ownership of the Staten Island Ferry, transport of California Gold Rush passengers through Central America, and a dalliance with trans-Atlantic steamship service. Once a common nickname for steamboat line owners – the name coming from the US Navy rank for a senior captain commanding a flotilla – the moniker became synonymous with Vanderbilt. During the American Civil War, the steamship tycoon donated his large and fast 331-foot long and 3,360 tons displacement SS Vanderbilt to the Union Navy, becoming the cruiser USS Vanderbilt. -

The Gilded Age 2/13/12 1:18 PM Page Iii

DM - The Gilded Age 2/13/12 1:18 PM Page iii Defining Moments the Gilded Age Diane Telgen 155 W. Congress, Suite 200 Detroit, MI 48226 DM - The Gilded Age 2/13/12 1:18 PM Page v Table of Contents Preface . .ix How to Use This Book . .xiii Research Topics for Defining Moments: The Gilded Age . .xv NARRATIVE OVERVIEW Prologue . 3 Chapter One: America’s Postwar Expansion . 9 Chapter Two: The Rise of the Robber Barons . 23 Chapter Three: Captains of Industry . 39 Chapter Four: Gilded Age Politics, Reformers, and Regulators . 55 Chapter Five: The Rise of Labor . 71 Chapter Six: The 1890s: A Decade of Upheaval . 89 Chapter Seven: Legacy of the Gilded Age . 105 BIOGRAPHIES William Jennings Bryan (1860-1925) . 125 Populist Leader and Three-time Democratic Candidate for President Andrew Carnegie (1835-1919) . 129 Steel Magnate and Philanthropist Grover Cleveland (1837-1908) . 133 Democratic President of the United States v DM - The Gilded Age 2/13/12 1:18 PM Page vi Defining Moments: The Gilded Age Eugene V. Debs (1855-1926) . 137 Founder of the American Railway Union and the Socialist Party of America Samuel Gompers (1850-1924) . 141 Founder and President of the American Federation of Labor Jay Gould (1836-1892) . 144 Gilded Age Financier and Railroad Owner Mary Elizabeth Lease (1853-1933) . 147 Reformist Speaker and Politician J. P. Morgan (1837-1913) . 150 Leading Banker and Financier of the Gilded Age Terence V. Powderly (1849-1924) . 153 Leader of the Knights of Labor John D. Rockefeller (1839-1937) . 156 Founder of the Standard Oil Company PRIMARY SOURCES Mark Twain Describes the Get-Rich-Quick Mining Culture . -

Historical Dictionary of the Gilded Age

HISTORICAL DICTIONARIES OF U.S. HISTORICAL ERAS Jon Woronoff, Series Editor 1. From the Great War to the Great Depression, by Neil A. Wynn, 2003. 2. Civil War and Reconstruction, by William L. Richter, 2004. 3. Revolutionary America, by Terry M. Mays, 2005. 4. Old South, by William L. Richter, 2006. 5. Early American Republic, by Richard Buel Jr., 2006. 6. Jacksonian Era and Manifest Destiny, by Terry Corps, 2006. 7. Reagan–Bush Era, by Richard S. Conley, 2007. 8. Kennedy–Johnson Era, by Richard Dean Burns and Joseph M. Siracusa, 2008. 9. Nixon–Ford Era, by Mitchell K. Hall, 2008. 10. Roosevelt–Truman Era, by Neil A. Wynn, 2008. 11. Eisenhower Era, by Burton I. Kaufman and Diane Kaufman, 2009. 12. Progressive Era, by Catherine Cocks, Peter Holloran, and Alan Lessoff, 2009. 13. Gilded Age, by T. Adams Upchurch, 2009. Historical Dictionary of the Gilded Age T. Adams Upchurch Historical Dictionaries of U.S. Historical Eras, No. 13 The Scarecrow Press, Inc. Lanham, Maryland • Toronto • Plymouth, UK 2009 SCARECROW PRESS, INC. Published in the United States of America by Scarecrow Press, Inc. A wholly owned subsidiary of The Rowman & Littlefi eld Publishing Group, Inc. 4501 Forbes Boulevard, Suite 200, Lanham, Maryland 20706 www.scarecrowpress.com Estover Road Plymouth PL6 7PY United Kingdom Copyright © 2009 by T. Adams Upchurch All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior permission of the publisher. British Library Cataloguing in Publication Information Available Library of Congress Cataloging-in-Publication Data Upchurch, Thomas Adams. -

Legal Phenomenon1 Claire A

Mergers and acquisitions: a cyclical and legal phenomenon 1. Mergers and acquisitions: a cyclical and legal phenomenon1 Claire A. Hill, Brian J.M. Quinn and Steven Davidoff Solomon Mergers and acquisitions (M&A) have a rich history in the American economy. Over the course of the past century and a half, merger activity has proceeded in waves, each wave inevitably followed by a regulatory and legal response. Merger activity emerged during the late nineteenth century. The succeeding trust era, characterized by monopolies and fre- netic acquisition activity, resulted in new regulations in the 1890s and early nineteenth century. Merger activity created vast conglomerates during the 1960s. During the 1970s and 1980s, the leveraged buyout boom led to the development of modern M&A legal doctrine. The late 1980s and 1990s saw the embracing of new participants such as private equity firms. Today, the Internet Age and globalization have led to the current M&A market, char- acterized by transactions that are global, very large (multi-billion dollar), and sometimes both. 1. AN EARLY EXAMPLE OF U.S. MERGER ACTIVITY: THE ERIE WAR Following the Civil War and lasting through the Panic of 1873, the rail- road industry underwent a period of growth as federal money flowed into the South to rebuild railroad stock. Estimates put the number of railroad organizations at the time in the thousands. Simultaneously and in part to meet the needs of these new organizations, a national capital market, cen- tered around the New York Stock Exchange, began to develop. It was at this point that the U.S. -

Jay Gould. the Union Pacific and Value Creation

24 FINANCIAL HISTORY | Fall 2016 | www.MoAF.org Jay Gould, the Union Pacific Railroad and Value Creation By Maury Klein and Joseph Calandro, Jr. Third, Gould was uncommonly suc- left home to work for a surveyor. Already cessful in investment, speculation/trading he had learned to push his stamina to the During a recent financial history pre- and business due to a variety of strategic limit and to master any skill that came sentation, the name Jay Gould was men- moves frequently so audacious and com- his way. He taught himself surveying, tioned. It was immediately followed by a plex that few, if any, of his contemporaries wrote an impressive history of Delaware discernable “gasp” from the audience. This understood what he was doing, or why. County and learned how to cultivate the apparently was the reaction the presenter Moreover, Gould did not socialize with confidence of those older than himself. He was looking for as he proceeded to deride the elite of his day, preferring instead to won the trust of a prominent tanner and Gould’s memory (Gould passed away in spend his non-working hours with his at age 20 was sent into the woods of Penn- 1892). This presenter’s criticisms were very family and his books. Over time, factors sylvania to build and run a tannery from broad and culminated with a reference such as these resulted in an information scratch. Despite his youth, older workers to Gould as an “infamous speculator.” vacuum. As the press, like nature, abhors a respected him well enough that the settle- The criticisms and comments were gener- vacuum, information was generated to fill ment was named Gouldsboro. -

When Cornelius Vanderbilt Died in 1877, He Left an Estate

Cornelius Vanderbilt Born May 27, 1794 (Port Richmond, New York) Died January 4, 1877 (New York, New York) Shipping executive Railroad executive Financier ‘‘I for one will never go to a hen Cornelius Vanderbilt died in 1877, he left an estate court of law when I have W valued at $100 million. Vanderbilt’s astonishing fortune the power in my own ranked him as the richest American in his lifetime, and his wealth had seemed to grow right along with the rapidly expanding new hands to see myself right.’’ nation. Known as the ‘‘Commodore,’’ he made his first fortune in shippingandwentontoownalargesectionoftherailroadtracks that connected the East Coast to Chicago, Illinois. Vanderbilt had a skill for recognizing coming changes and trends, and his talent for investment opportunities made him one of the American Industrial Revolution’s leading figures. His estate also created one of the country’s great family fortunes. An early start in the shipping business Born in May 1794 on Staten Island, New York, Vanderbilt came from a Dutch farming family who lived in Port Richmond, on the north shore of the island. His great-great-great-grand- father, Jan Aertson, came to New York in 1650 as an indentured servant, a common form of contract labor in the era and a way for poor men and women to try their luck in the New World. In exchange for promising their labor for a number of years, the 234 Cornelius Vanderbilt. (ª Bettmann/Corbis.) indentured servant was provided with transportation to North America and food and shelter during his work years. -

J. Pierpont Morgan

J. PIERPONT MORGAN (1837-1913). Financier. Probably the most prolific and powerful banker in American Financial history, J. Pierpont Morgan epitomized the financial genius, courage and flair that made possible many of the most important financings of the late 1800s and early 1900s. His career in banking spanned the period from Abraham Lincoln’s administration to Theodore Roosevelt’s. Throughout his career he displayed a financial skill and daring matched by few in the entire history of Wall Street. Following the financial panic of 1893, Morgan helped reorganize nu- merous railroads including giants such as The Northern Pacific, The Erie, The Southern and The Philadelphia and Reading. His formation of The United States Steel Corpo- ration in 1901 created the largest corporation in the world at that time. During the panic of 1907, it was Mor- gan who averted a nationwide catastrophe by lending money to banks to keep them from closing. “A sociable, convivial man who thoroughly enjoyed life and entertained what would now be known as ‘beautiful people’ on his famous steam yacht, the Cor- sair, he nevertheless frightened people by his overwhelming personality and his pierc- ing eye, which was compared to the headlight of an oncoming locomotive. Seldom has a man of such complexity and power crossed the world’s stage.” (The Incredible Pierpont Morgan by Cass Canfield). DUNCAN, SHERMAN & CO. DABNEY, MORGAN & CO. GEORGE PEABODY & CO. J. P. MORGAN & COMPANY DREXEL, MORGAN & CO. DREXEL AND COMPANY DREXEL, HARJES & CO. 1 IMPORTANT POINTS IN J. PIERPONT MORGAN’S BUSINESS CAREER 1837 Born in Hartford, Connecticut 1856 Begins work at Duncan, Sherman & Co., the American representatives of George Peabody & Co. -

BACKGROUND INFORMATION President William Mckinley William

BACKGROUND INFORMATION President William McKinley William McKinley served in the U.S. Congress and as governor of Ohio before running for the presidency in 1896. As a longtime champion of protective tariffs, the Republican McKinley ran on a platform of promoting American prosperity and won a landslide victory over William Jennings Bryan to become the 25th president of the United States. Soon after taking office, McKinley called a special session of Congress in order to raise customs duties, an effort he believed would reduce other taxes and encourage the growth of domestic industry and employment for American workers. The result was the Dingley Tariff Act, the highest protective tariff in American history. McKinley's support for the Dingley Tariff strengthened his position with organized labor, while his generally business-friendly administration allowed industrial combinations or "trusts" to develop at an unprecedented rate. In 1898, McKinley led the nation into war with Spain over the issue of Cuban independence. The Treaty of Paris, signed in December 1898 and narrowly ratified by Congress in February, officially ended the Spanish-American War. Spain ceded Puerto Rico, Guam and the Philippines to the United States and Cuba gained its independence. McKinley's administration also pursued an influential "Open Door" policy aimed as supporting American commercial interests in China and ensuring a strong U.S. position in world markets. In general, McKinley's bold foreign policy opened the doors for the United States to play an increasingly active role in world affairs. Reelected in 1900, McKinley was assassinated by a deranged anarchist in Buffalo, New York, in September 1901.