Entertaining Australia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Full Year Statutory Accounts

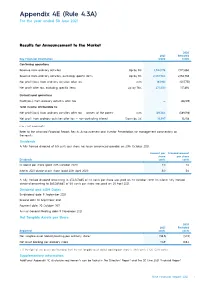

Appendix 4E (Rule 4.3A) For the year ended 30 June 2021 Results for Announcement to the Market 2020 2021 Restated Key Financial Information $’000 $’000 Continuing operations Revenue from ordinary activities Up by 8% 2,342,178 2,172,060 Revenue from ordinary activities, excluding specific items Up by 8% 2,332,984 2,156,785 Net profit/(loss) from ordinary activities after tax n/m 183,961 (507,751) Net profit after tax, excluding specific items Up by 76% 277,530 157,694 Discontinued operations Profit/(loss) from ordinary activities after tax — (66,189) Total income attributable to: Net profit/(loss) from ordinary activities after tax — owners of the parent n/m 169,364 (589,198) Net profit from ordinary activities after tax — non-controlling interest Down by 4% 14,597 15,258 n/m = not meaningful Refer to the attached Financial Report, Results Announcement and Investor Presentation for management commentary on the results. Dividends A fully franked dividend of 5.5 cents per share has been announced payable on 20th October 2021. Amount per Franked amount share per share Dividends cents cents Dividend per share (paid 20th October 2020) 2.0 2.0 Interim 2021 dividend per share (paid 20th April 2021) 5.0 5.0 A fully franked dividend amounting to $34,107,865 of 2.0 cents per share was paid on 20 October 2020. An interim fully franked dividend amounting to $85,269,663 of 5.0 cents per share was paid on 20 April 2021. Dividend and AGM Dates Ex-dividend date: 9 September 2021 Record date: 10 September 2021 Payment date: 20 October 2021 Annual General Meeting date: 11 November 2021 Net Tangible Assets per Share 2020 2021 Restated Reported cents cents Net tangible asset (deficit)/backing per ordinary share 1 (38.3) (40.9) Net asset backing per ordinary share 114.9 108.4 1. -

1997 SMA Conference and Swimming Course 1997-1998 Has Been a Successful and Productive Year for SDA

TABLE OF CONTENTS PRESIDENT’S REPORT - HELEN O’CONNOR .................................................................................... 1 TREASURER/SECRETARY’S REPORT - LIZ BROAD ........................................................................ 3 SPONSORSHIP AND PUBLIC RELATIONS REPORT - KAREN INGE ............................................ 4 MEMBERSHIP SERVICES - LORNA GARDEN ..................................................................................... 5 STRATEGIC PLANNING REPORT - DEBORAH KERR ...................................................................... 6 RESOURCES AND EDUCATION REPORT: - LOUISE BURKE ......................................................... 7 NEWSLETTER COORDINATOR’S REPORT: - GLENN CARDWELL.............................................. 9 STATE DIRECTORS LIAISON OFFICER - HOLLY FRAIL................................................................ 9 STATE REPORTS ...................................................................................................................................... 10 New South Wales – Fiona Pelly .......................................................................................................... 10 Queensland - Ben Desbrow ............................................................................................................... 10 South Australia – Nick Wray .............................................................................................................. 11 Tasmania – Fiona Rowell .................................................................................................................. -

Week9 E-Record .Indd

E-Footy RECORD 31st May 2008 Issue 9 Editorial with Marty King AFL AND AFLPA SET TO MOVE ON NEW ALCOHOL POLICY It’s terrifi c to see the AFL and the AFL Players Association working collaboratively to formulate a new policy on responsible alcohol consumption in the football environment. They are seeking feedback from each of the 16 AFL clubs, together with key national drug and alcohol experts, before framing a policy with guidelines that all AFL clubs and associated bod- ies like AFL Queensland can use to develop their own. This comes after a lot of background work was done over almost two years and the AFL Com- mission received a full briefi ng. The AFL, the Players’ Association and the AFL clubs understand that quite clearly that they have a responsibility to promote responsible drinking within the AFL and among the 16 clubs, the players and staff. But it’s not just about the elite level. The same will apply at the grassroots level and we at AFLQ will look to partner with the League on this important initiative. The guidelines within the AFL Framing Policy will provide a framework for AFL clubs and asso- ciated bodies to assist them in developing their own individual club responsible alcohol policies. The AFL Framing Policy lists a set of objectives for players and club staff, including the devel- opment of approaches for responsible consumption, effective pathways for treatment of alco- hol-related problems, creating responsible drinking cultures and using player welfare oriented and education-based approaches to promote responsible alcohol consumption. -

Submission to the Inquiry Into Broadcasting, Online Content and Live Production to Rural and Regional Australia

SUBMISSION TO THE INQUIRY INTO BROADCASTING, ONLINE CONTENT AND LIVE PRODUCTION TO RURAL AND REGIONAL AUSTRALIA The Hon Bronwyn Bishop MP Chair Standing Committee on Communications and the Arts PO Box 6021 Parliament House CANBERRA ACT 2600 By email: [email protected] Introduction Thank you for the opportunity to make a submission to the House of Representatives Standing Committee on Communications and the Arts inquiry into broadcasting, online content and live production to rural and regional Australia. This letter is on behalf of the three major regional television providers, Prime Media Group (Prime Media), the WIN Network (WIN) and Southern Cross Austereo (SCA). Prime Media and SCA are members of Free TV Australia, the television peak body which has also made a submission to this inquiry on behalf of the industry. Prime Media broadcasts in northern New South Wales, southern New South Wales, the Australian Capital Territory, regional Victoria, Mildura, the Gold Coast area of south eastern Queensland and all of regional Western Australia. WIN broadcasts in southern New South Wales, the Australian Capital Territory, regional Queensland, regional Victoria, Tasmania, Griffith, regional WA, Mildura, Riverland and Mt Gambier in South Australia. SCA broadcasts in northern New South Wales, southern New South Wales, Queensland, the Australian Capital Territory, Griffith, regional Victoria, Tasmania, the Northern Territory and the Spencer Gulf region of South Australia. Through affiliation agreements, Prime Media, WIN and SCA purchase almost all of their programming from metropolitan networks1 and using more than 500 transmission towers located across the country, retransmit that programming into regional television licence areas. -

1 Transcript of 2019 Nine Entertainment AGM Sydney

1 Transcript of 2019 Nine Entertainment AGM Sydney, November 12, 2019 Chairman Peter Costello Good morning ladies and gentleman. As your Chairman, it's my pleasure to welcome you to the 2019 AGM of Nine Entertainment Company. My name is Peter Costello. Before opening the meeting, I refer you to the disclaimer here on the screen behind me and available through our ASX lodgement. It is now shortly after 10am and I am advised that this is a properly constituted meeting. There's a quorum of at least two shareholders present so I declare the 2019 Annual General Meeting open. Unless there are any objections, I propose to take the Notice of Meeting as read. Copies of the Notice of Meeting are available from the registration desk outside should you require them. Let me now introduce the people who are with us this morning. To my immediate left is Rachel Launders, our General Counsel and Company Secretary. Then Hugh Marks, our Chief Executive Officer, who will address the meeting a little later. Next to Hugh is Nick Falloon, the Independent, Non-Executive Director and Deputy Chair and Member of the People and Remuneration Committee. Then we have Patrick Alloway, Independent, Non-Executive Director and a member of the Audit and Risk Management Committee. Next to Patrick is Sam Lewis, Independent, Non-Executive Director, Chair of the Audit and Risk Committee and a Member of the People and Remuneration Committee. Then we have Mickie Rosen, Independent, Non-Executive Director. At the far end, we have Catherine West, Independent, Non-Executive Director, the Chair of the People and Remuneration Committee and a member of the Audit and Risk Committee. -

Billy Brownless

BILLY BROWNLESS Talent Profile © TLA Worldwide 2020 TLAWorldwide.com A loveable character on and off air, Billy Brownless has enjoyed a 25-year connection to footy fans through the media since hanging up the boots. NATIONALITY CAPABILITIES Australian Guest Panellist Ambassador DATE OF BIRTH Social Media 1/28/67 PR Campaign Appearances TEAMS INTERESTS Geelong Football Club Triple M Lifestyle Nine Network Wellbeing Leadership Family Business © TLA Worldwide 2020 TLAWorldwide.com BIO Brownless first came to prominence as a high-flying forward for Geelong. Growing up in Jerilderie in southern NSW, Brownless was a schoolboy star with Assumption College before making his debut with Cats in 1986. The proud father of four has son Oscar following in his footsteps, with the young midfielder in to his second year on the Cats’ AFL list. Brownless made his senior VFL debut in Round 1, 1986 and quickly made a name for himself as a strong full-forward, winning the Cats’ best first year player award that year. Twice he led Geelong’s goalkicking, was All-Australian in 1991 and had a thirst for the big occasion. Nine goals in the 1992 Qualifying Final, eight in the classic 1991 Elimination Final win over St Kilda and an average of three goals per game across the four Grand Finals he played in stamped his qualities. Today, he sits fifth with 441 goals on Geelong all-time list, alongside iconic names Gary Ablett Snr, Doug Wade, Tom Hawkins and Steve Johnson. © TLA Worldwide 2020 TLAWorldwide.com For the past decade, Billy and good friend James Brayshaw have been part of Melbourne’s drive home as hosts of ‘The Rush Hour’ on Triple M. -

Premier's Diary - 1 March 2015 to 27 July 2015

Right to Information - Premier's Diary - 1 March 2015 to 27 July 2015 DATE SUBJECT 4/03/2015 Australian Wooden Boat Festival 5/03/2015 UTas ICC Cricket World Cup 2015, Government House Reception & Irish Team Celebration 6/03/2015 West Winds Community Centre 25th Anniversary Ambassador of Zimbabwe 7/03/2015 Opening of the 16th National Welsh Corgi Specialty Show 2015 Cripps Tasmanian Age Swimming Championships Morning Heat Session World Cup - Zimbabwe v Ireland 10/03/2015 Regional Cabinet Meeting with Meander Valley Councillors, General Manager, Guy Barnett and Mark Shelton Regional Cabinet Morning Tea 11/03/2015 World Cup - Sri Lanka v Scotland 12/03/2015 Tasmanian Aboriginal Centre Tas Irrigation Welcome event for Cricket Scotland 13/03/2015 Dale Elphinstone & Minister Gutwein - Pre-JCTEC Vodafone Hobart Customer Care Centre JCTEC Meeting 14/03/2015 ICC Cricket world Cup 2015 Media Breakfast World Cup - Australia v Scotland James Sutherland - Cricket Australia 15/03/2015 C3 Convention Centre 20th Year Celebration BUPA Kidfit Triathlon Race Start ICC Cricket World Cup 2015 Volunteer Thank You 17/03/2015 Ambassador of Finland 19/03/2015 State Government Celebration of Harmony Day TasCOSS Infrastructure Australia Board Dinner 20/03/2015 TCCI Export Growth China Launch Tasmanian Hospitality Association 21/03/2015 Seafood Seduction Tour 23/03/2015 Oakdale Industries with Governor-General, Sir Peter Cosgrove & Lady Cosgrove 24/03/2015 Richard Flanagan Official Reception Oak Tasmania Constituent 25/03/2015 Mark Ryan Gordon Fyfe - Be Well 4 Work -

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming

Nine Network Australia Selects Intelsat to Distribute Domestic Television Programming October 24, 2016 Intelsat will provide satellite connectivity and global fiber services via the IntelsatOne network to bring news content from around the world to Australia LUXEMBOURG--(BUSINESS WIRE)--Oct. 24, 2016-- Intelsat (NYSE: I), operator of the world’s first Globalized Network, powered by its leading satellite backbone, today announced a contract with Nine Network Australia to distribute programming to the company’s six domestic television stations as well as provide global satellite and fiber connectivity using the IntelsatOne terrestrial network to bring news content and special events from around the world to Australia for its network affiliates. Nine Network Australia (NNA) is one of the country’s top-rated commercial television networks, with local stations in Sydney, Melbourne, Brisbane, Adelaide, Perth and Darwin, along with a regional broadcaster, NBN. The network also has news bureaus in Canberra, London and Los Angeles. NNA is a subsidiary of Nine Entertainment Co., one of Australia’s leading media companies. Intelsat initially is providing services via the Australia/New Zealand Ku-Band beam on Intelsat 19 for the network’s broadcasting requirement. Under the agreement, Intelsat’s network support will extend well into the next decade. “Our Globalized Network allows us to meet NNA’s needs today and to increase our level of support if the network expands over time to meet the demands of multi-platform coverage,” said Terry Bleakley, Regional Vice President, Asia Pacific Sales, Intelsat. “NNA will also benefit from Intelsat’s global coverage for international contribution and distribution requirements.” NNA previously used Intelsat for its domestic and international occasional use requirements. -

Corporate Results Monitor

Corporate Results Monitor FNArena's All-Year Round Australian Corporate Results Monitor. Currently monitoring August 2019. TOTAL STOCKS: 272 Total Rating Upgrades: 61 Beats In Line Misses Total Rating Downgrades: 66 61 140 71 Simple average net target price change: 2.40% 22.4% 51.5% 26.1% Beat/Miss Ratio: 0.86 Latest Prev New Company Result Upgrades Downgrades Buy/Hold/Sell Brokers Target Target ABC - ADELAIDE BRIGHTON IN LINE 0 0 0/2/4 3.28 3.13 6 While Adelaide Brighton's result matched fresh guidance provided following a profit warning in July, it did still exceed most broker forecasts. FY20 guidance is bleak, given the housing construction downturn has as yet no end in sight and increased infrastructure construction is not sufficient to offset. The suspension of the dividend also came as no shock, but an intent to acquire and build out an integrated, infrastructure-oriented business model carries risk and reduces dividend prospects near-term. APT - AFTERPAY TOUCH BEAT 0 0 2/0/0 30.43 33.43 2 Afterpay Touch's FY19 net loss was slightly less than Morgans expected. The results suggest continuing strong sales momentum and stable margins across the business. Morgans downgrades FY20-21 earnings estimates, factoring in higher investment expenditure associated with offshore expansion. Traction in the US is strong but the key for Ord Minnett in the FY19 result were the initial customer acquisitions in the UK, which were well above expectations. Average merchant fees were slightly ahead of expectations, particularly in the US. AOG - AVEO IN LINE 0 1 0/2/0 2.15 2.15 2 Aveo Group's FY19 net profit was in line with recently downgraded guidance. -

2015 SWM Annual Report

ABN 91 053 480 845 Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Seven West Media cares about the environment. By printing 2000 copies of this Annual Report on ecoStar Silk and ecoStar Offset the environmental impact was reduced by*: 1,185kg 171kg 1,707km of landfill of CO2 and travel in the average greenhouse gases European car 26,982 2,486kWh 1,926kg litres of water of energy of wood Source: European BREF data (virgin fibre paper). Carbon footprint data evaluated by Labelia Conseil in accordance with the Bilan Carbone® methodology. Results are obtained according to technical information and are subject to modification. *compared to a non-recycled paper. Delivering the future of content. Anywhere. Any screen. Anytime. Annual Report 2015 Contents What We Do 4 The Future of Us 44 Our Brands 6 Board of Directors 46 Our Strategy 8 Corporate Governance Statement 49 Our Strategic Framework 10 Directors’ Report 60 Letter from the Chairman 12 Remuneration Report 64 Letter from the Managing Director & CEO 14 Auditor’s Independence Declaration 83 Performance Dashboard 16 Financial Statements 84 Performance of the Business 18 Directors’ Declaration 134 Group Performance 20 Independent Auditor’s Report 135 Television 26 Company Information 137 Newspapers 32 Investor Information 138 Magazines 36 Shareholder Information 139 Other Business and New Ventures 40 Risk, Environment and Social Responsibility 42 2 Seven West Media Annual Report 2015 ABN 91 053 480 845 Contents The right people creating great content across television, digital, mobile and newspaper and magazine publishing. Delivering the future of content 3 What We Do We are achieving growth in the delivery of our content across our portfolio of integrated media platforms. -

Annual Report 2020 Contents

Annual Report 2020 Contents Business Performance Overview 2 Chairman’s Report 4 CEO’s Report 6 Corporate Social Responsibility 10 Directors' Report 19 Remuneration Report 26 Corporate Governance Statement 45 Management Discussion and Analysis Report 59 Auditor’s Independence Declaration 62 2020 Financial Report 63 Shareholder Information 117 Corporate Directory 120 Inspiring confidence for all of life’s property decisions We are a leading property technology and services business that is home to one of the largest portfolios of property brands in Australia. Domain helps agents and consumers at every step in the property lifecycle – renting, buying, selling, investing, financing, insurance and utilities. The Domain Group is home to Domain, Allhomes, Commercial Real Estate, and CommercialView. Our portfolio also includes agent products Homepass, Pricefinder and Real Time Agent. Our consumer solutions products include Domain Loan Finder and Domain Insure. As a customer-centric property marketplace, we are committed to making the property journey easier, more enjoyable and connected at every stage. Annual Report 2020 1 Business Performance Overview Core Digital Residential by COVID-19’s impact on key advertising Residential generates revenue through categories in H2. The Developer market listings of ‘for sale’ and rental properties was impacted by the deferral of high rise across its desktop, mobile and social apartment projects resulting from lower platforms. Premium (depth) listing investor demand and COVID-19 impacts products account for the largest on immigration. Activity in smaller, proportion of revenue, with monthly boutique projects was stronger, however these require lower levels of marketing * subscriptions contributing the balance. $227.0m support. Commercial Real Estate (CRE) FY20 Revenue Residential revenue reduced 7%, a delivered solid revenue growth for the solid performance in an environment year. -

Premium Home Loan

THE BYRON SHIRE Volume 25 #41 Tuesday, March 22, 2011 Mullumbimby 02 6684 1777 Byron Bay 02 6685 5222 Fax 02 6684 1719 [email protected] BONUS SUPPLEMENT [email protected] Your Sustainable Community 2011 www.echo.net.au inserted in this week’s Echo 23,000 copies every week ARGUE OR CUDDLE WITH ME – IT’S YOUR CHOICE www.yoursustainablecommunity.net Harmony celebrated Empty mansions are ‘on-shore tax havens’ Echo Forum hears need for tax reform and local action on aff ordable housing Ray Moynihan to fi nd an aff ordable property close to Lismore. Australia’s leading advocate for aff ord- ‘I didn’t want my child growing up able housing, Professor Julian Disney, in a garage,’ she told Th e Echo. called for major changes to the way Chair of the National Housing houses are taxed at a forum in Byron Affordability Summit, Professor last week attended by over 200 people. Disney urged local councils to cre- Professor Disney told the forum, ate not-for-profi t companies to work ‘excessively generous’ tax concessions with developers to build genuinely meant houses were increasingly seen aff ordable housing, which could of- as speculative investments rather fer people the security of long-term than places to live, with very expen- rental leases, virtually unheard of in sive mansions becoming ‘on-shore tax Australia, though extremely common havens’ which sucked resources away in Europe. from more productive investments. Also at the forum Byron Commu- He called for changes to the nega- nity Centre general manager Paul tive gearing concessions for invest- Spooner launched a new campaign ment properties, reform to land or called ‘One Year, One House’ which capital gains taxes for very high-cost aims to garner community support to houses, and a reduction in stamp build at least one aff ordable house in Isabelle and Fleur from Mullumbimby St John’s primary school get along nicely, unlike some politicians (see below).