Chapter 3. the VA Loan and Guaranty Overview

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

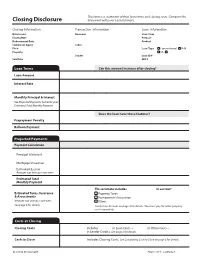

Closing Disclosure Document with Your Loan Estimate

This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term Closing Date Purpose Disbursement Date Product Settlement Agent Seller File # Loan Type Conventional FHA Property VA _____________ Lender Loan ID # Sale Price MIC # Loan Terms Can this amount increase after closing? Loan Amount Interest Rate Monthly Principal & Interest See Projected Payments below for your Estimated Total Monthly Payment Does the loan have these features? Prepayment Penalty Balloon Payment Projected Payments Payment Calculation Principal & Interest Mortgage Insurance Estimated Escrow Amount can increase over time Estimated Total Monthly Payment This estimate includes In escrow? Estimated Taxes, Insurance Property Taxes & Assessments Homeowner’s Insurance Amount can increase over time Other: See page 4 for details See Escrow Account on page 4 for details. You must pay for other property costs separately. Costs at Closing Closing Costs Includes $5,877.00 in Loan Costs + $7,642.43 in Other Costs – $0 in Lender Credits. See page 2 for details. Cash to Close Includes Closing Costs. See Calculating Cash to Close on page 3 for details. CLOSING DISCLOSURE PAGE 1 OF 5 • LOAN ID # 0000000000 This form is a statement of final loan terms and closing costs. Compare this Closing Disclosure document with your Loan Estimate. Closing Information Transaction Information Loan Information Date Issued Borrower Loan Term -

5/1 MOP Loan Program

GENERAL GUIDELINES 5/1 Maximum Loan-to-Value Ratio: Same as Standard MOP LTV Thresholds Fixed Rate Period: 5 Years ORTGAGE M Maximum Loan Term: 30 Years RIGINATION Qualifying Interest Rate: Initial 5/1 MOP Interest Rate O Minimum Interest Rate: 3.25% ROGRAM P Maximum Payment-to-Income Ratio: 40% Maximum Overall Debt-to-Income Ratio: 48% PROGRAM OVERVIEW 5/1 MOP Initial Interest Rate The 5/1 Mortgage Origination Program (5/1 MOP) loan is a fully-amortizing mortgage loan The initial fixed interest rate* in effect during the Fixed Rate that offers an initial fixed interest rate and payment for the first 5 years of the loan, after which Period of the loan is comprised of the following three (3) the loan converts to a 1-year adjustable rate mortgage (“Standard MOP”) for the remaining components: loan term. The maximum overall loan term is 30 years. All or any portion of the principal Index: 5-year Treasury Bond Yield balance may be prepaid without penalty at any time and there is no negative amortization associated with 5/1 MOP loans. For eligibility requirements, refer to the MOP Brochure. Spread: J.P. Morgan U.S. Liquid Index (JULI) Index Service Fee: .25% IMPORTANT CONSIDERATIONS: *The minimum 5/1 MOP Initial Interest Rate is 3.25% • The 5/1 MOP Initial Interest Rate may be higher or lower than the current Standard Rate offered for a Standard MOP loan. The current interest rate for each of these loan products is available at www.ucop.edu/loan-programs. QUESTIONS? • Fixed rate payments during the first 5 years of the loan provide a stable monthly payment Contact the local Campus Housing Programs to borrowers; however, there is potential for increased monthly payments when the Fixed Representative or the University of California Home Loan Rate Period ends. -

CITY of BREMERTON, WASHINGTON PLANNING COMMISSION AGENDA ITEM AGENDA TITLE: Workshop to Discuss Nonconformities and Substitute Senate Bill 5451

Commission Meeting Date: March 20, 2012 Agenda Item: V.B.1 CITY OF BREMERTON, WASHINGTON PLANNING COMMISSION AGENDA ITEM AGENDA TITLE: Workshop to discuss Nonconformities and Substitute Senate Bill 5451. DEPARTMENT: Community Development PRESENTED BY: Nicole Floyd, City Planner SUMMARY: This workshop is part of a series of workshops to discuss the Draft Shoreline Master Program (SMP) update. Each workshop focuses on a different set of topics and or sections of the code. The Planning Commission has held two previous workshops focusing on general nonconformities and how they are applicable to the Shoreline Master Program. This workshop will focus on the potential impacts of utilizing the allowed language from Substitute Senate Bill (SSB) 5451in relationship to the nonconforming provisions of the Shoreline Master Program Update. In summary, the Bill was drafted to clarify The Department of Ecology’s review authority over the Statewide SMP update process. Specifically, it is not Ecology’s responsibility to determine what terms are used when referring to existing residential structures. Statewide, this means that there will continue to be substantial variation as to how local jurisdictions address nonconformities within the Shoreline. For Bremerton, it provides the opportunity to change how nonconformities are classified and how they are regulated. This report aims to help provide a better understanding of the underlying issues surrounding the optional language changes to the nonconforming code section. Staff is asking the Planning Commission to provide direction by answering the following questions: 1. Should the City create an alternate name for legal nonconforming residential structures on the shoreline; and 2. Should the City allow for the full replacement of such residential structures an unlimited number of times? Please keep these questions in mind when reading the report and reviewing the attachments, as the report is intended to help provide a wide range of data surrounding these two questions. -

Agency Guideline Revisions Note: Suntrust Mortgage Specific Overlays Are Underlined

Agency Guideline Revisions Note: SunTrust Mortgage specific overlays are underlined. Impacted Revised Guidelines Topic Impacted Products Current Guidelines Document Effective Immediately for NEW AND EXISTING Loan Applications ON OR After May 26, 2017 Appraisal Correspondent HomeReady® Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Appraisal Analysis: Agency Loan Programs / Improvements Section of the Appraisal Report Requirements Section 1.07 Mortgage / Accessory Appraisal- (non-AUS & Non-AUS Non-AUS Units Guideline DU) Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Note: Below is an EXCERPT only of the guidance from the above referenced section. All other currently published Home guidelines from this section remain the same. guidelines from this section remain the same. Possible® Accessory Units Accessory Units Mortgage Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an Fannie Mae will purchase a one-unit property with an accessory unit. An accessory unit is typically an (LPA) additional living area independent of the primary dwelling unit, and includes a fully functioning additional living area independent of the primary dwelling unit, and includes a fully functioning kitchen and bathroom. Some examples may include a living area over a garage and basement units. kitchen and bathroom. Some examples may include a living area over a garage and basement units. Whether a property is defined as a one-unit property with an accessory unit or a two-unit property Whether a property is defined as a one-unit property with an accessory unit or a two-unit property will be based on the characteristics of the property, which may include, but are not limited to, the will be based on the characteristics of the property, which may include, but are not limited to, the existence of separate utilities, a unique postal address, and whether the unit is rented. -

Housing and the Financial Crisis

This PDF is a selection from a published volume from the National Bureau of Economic Research Volume Title: Housing and the Financial Crisis Volume Author/Editor: Edward L. Glaeser and Todd Sinai, editors Volume Publisher: University of Chicago Press Volume ISBN: 978-0-226-03058-6 Volume URL: http://www.nber.org/books/glae11-1 Conference Date: November 17-18, 2011 Publication Date: August 2013 Chapter Title: The Future of the Government-Sponsored Enterprises: The Role for Government in the U.S. Mortgage Market Chapter Author(s): Dwight Jaffee, John M. Quigley Chapter URL: http://www.nber.org/chapters/c12625 Chapter pages in book: (p. 361 - 417) 8 The Future of the Government- Sponsored Enterprises The Role for Government in the US Mortgage Market Dwight Jaffee and John M. Quigley 8.1 Introduction The two large government- sponsored housing enterprises (GSEs),1 the Federal National Mortgage Association (“Fannie Mae”) and the Federal Home Loan Mortgage Corporation (“Freddie Mac”), evolved over three- quarters of a century from a single small government agency, to a large and powerful duopoly, and ultimately to insolvent institutions protected from bankruptcy only by the full faith and credit of the US government. From the beginning of 2008 to the end of 2011, the two GSEs lost capital of $266 billion, requiring draws of $188 billion under the Treasured Preferred Stock Purchase Agreements to remain in operation; see Federal Housing Finance Agency (2011). This downfall of the two GSEs was primarily a question of “when,” not “if,” given that their structure as a public/private Dwight Jaffee is the Willis Booth Professor of Banking, Finance, and Real Estate at the University of California, Berkeley. -

Freddie Mac Conforming and Super Conforming Fixed Rate

Freddie Mac Conforming and Super Conforming Fixed Rate This matrix is intended as an aid to help determine whether a property/loan qualifies for certain Freddie Mac offered programs. It is not intended as a replacement for Freddie Mac guidelines. Users are expected to know and comply with Freddie Mac’s requirements. NOTE: This matrix includes overlays which may be more restrictive than Freddie Mac’s requirements. Program Qualifications x Eligible loans are conforming and super conforming mortgages (using higher maximum loan limits permitted in designated high cost areas) fixed rate only receiving LP Accept findings Maximum Loan Amount 2017 Conforming Maximum Loan Amounts (available 12/2/16) Units Continental US Alaska & Hawaii 1 $424,100 $636,150 2 $543,000 $814,500 3 $656,350 $984,525 4 $815,650 $1,223,475* 2017 Super Conforming Loan Amounts (available 12/2/16) Continental US Alaska and Hawaii Units Minimum Loan Maximum Loan Minimum Loan Maximum Loan 1 $424,101 $636,150 $636,151 $954,225 2 $543,001 $814,500 $814,501 $1,221,750* 3 $656,351 $984,525 $984,526 $1,476,775* 4 $815,651 $1,223,475* Ineligible Ineligible Permanent High Cost area the maximum potential loan limits for designated high-cost areas. Actual loan limits are established for each county (or equivalent) and the loan limits for specific high-cost areas may be lower. The original balance of a Mortgage must not exceed the maximum loan limit for the specific areas in which the mortgage premises is located. For specific loan limits for each high cost area, as released by the Federal Housing Finance Agency visit http://www.fhfa.gov/DataTools/Downloads/Pages/Conforming-Loan-Limits.aspx *Maximum Loan Amount in all cases may not exceed $1,000,000. -

Mortgage-Backed Securities & Collateralized Mortgage Obligations

Mortgage-backed Securities & Collateralized Mortgage Obligations: Prudent CRA INVESTMENT Opportunities by Andrew Kelman,Director, National Business Development M Securities Sales and Trading Group, Freddie Mac Mortgage-backed securities (MBS) have Here is how MBSs work. Lenders because of their stronger guarantees, become a popular vehicle for finan- originate mortgages and provide better liquidity and more favorable cial institutions looking for investment groups of similar mortgage loans to capital treatment. Accordingly, this opportunities in their communities. organizations like Freddie Mac and article will focus on agency MBSs. CRA officers and bank investment of- Fannie Mae, which then securitize The agency MBS issuer or servicer ficers appreciate the return and safety them. Originators use the cash they collects monthly payments from that MBSs provide and they are widely receive to provide additional mort- homeowners and “passes through” the available compared to other qualified gages in their communities. The re- principal and interest to investors. investments. sulting MBSs carry a guarantee of Thus, these pools are known as mort- Mortgage securities play a crucial timely payment of principal and inter- gage pass-throughs or participation role in housing finance in the U.S., est to the investor and are further certificates (PCs). Most MBSs are making financing available to home backed by the mortgaged properties backed by 30-year fixed-rate mort- buyers at lower costs and ensuring that themselves. Ginnie Mae securities are gages, but they can also be backed by funds are available throughout the backed by the full faith and credit of shorter-term fixed-rate mortgages or country. The MBS market is enormous the U.S. -

Adjustable-Rate Mortgage (ARM) Is a Loan with an Interest Rate That Changes

The Federal Reserve Board Consumer Handbook on Adjustable-Rate Mortgages Board of Governors of the Federal Reserve System www.federalreserve.gov 0412 Consumer Handbook on Adjustable-Rate Mortgages | i Table of contents Mortgage shopping worksheet ...................................................... 2 What is an ARM? .................................................................................... 4 How ARMs work: the basic features .......................................... 6 Initial rate and payment ...................................................................... 6 The adjustment period ........................................................................ 6 The index ............................................................................................... 7 The margin ............................................................................................ 8 Interest-rate caps .................................................................................. 10 Payment caps ........................................................................................ 13 Types of ARMs ........................................................................................ 15 Hybrid ARMs ....................................................................................... 15 Interest-only ARMs .............................................................................. 15 Payment-option ARMs ........................................................................ 16 Consumer cautions ............................................................................. -

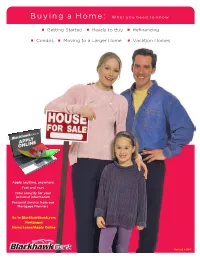

Buying a Home: What You Need to Know

Buying a Home: What you need to know n Getting Started n Ready to Buy n Refinancing n Condos n Moving to a Larger Home n Vacation Homes Apply anytime, anywhere Fast and easy Total security for your personal information Personal Service from our Mortgage Planners Go to Blackhawkbank.com Mortgages Home Loans/Apply Online Revised 4.2018 Owning a home has long been “the American In Wisconsin: WHEDA Fannie Mae Advantage: When you use the WHEDA Fannie Mae Advantage, you need less cash dream.” It’s a long-term commitment, but as your to close your loan and you will have lower monthly house equity increases with time (and payments) your payments than with most mortgages. What’s more, you’ll have peace of mind that your rate will never change with home will be a source of financial stability for you. their fixed rate and term. WHEDA FHA Advantage: With the WHEDA FHA Advantage, Wisconsin residents have the flexibility to leverage down payment assistance and other There are many things to think about whether you’re advantages to buy a home with an affordable mortgage. buying your first home, moving up, refinancing, or considering a vacation property. Let’s get the In Illinois: IHDA works with financial partners across Illinois conversation started! to offer programs that help qualified Illinois first-time homebuyers to receive down payment and closing cost assistance. Buying a home can be both exciting and intimidating, so IHDA strives to make the goal of homeownership as streamlined as possible. Be sure to ask your Blackhawk Mortgage Planner for a current list what IDHA offers. -

The Determinants of Attitudes Towards Strategic Default on Mortgages∗

June 2011 The Determinants of Attitudes towards Strategic Default on Mortgages∗ Luigi Guiso European University Institute, EIEF, & CEPR Paola Sapienza Northwestern University, NBER, & CEPR Luigi Zingales University of Chicago, NBER, & CEPR Abstract We use survey data to measure households’ propensity to default on mortgages even if they can afford to pay them (strategic default) when the value of the mortgage exceeds the value of the house. The willingness to default increases both in the absolute and in the relative size of the home- equity shortfall. Our evidence suggests that this willingness is affected both by pecuniary and non- pecuniary factors, such as views about fairness and morality. We also find that exposure to other people who strategically defaulted increases the propensity to default strategically because it conveys information about the probability of being sued. ∗ An earlier version of this paper circulated with the title “Moral and Social Constraints to Strategic Default on Mortgages.” We would like to thank the University of Chicago Booth School of Business and Kellogg School of Management for financial support in establishing and maintaining the Chicago Booth Kellogg School Financial Trust Index. Luigi Guiso is grateful to PEGGED for financial support. We thank Campbell Harvey (editor), Amir Sufi, two anonymous referee and seminar participants at the University of Chicago and New York University for very useful suggestions, Gabriella Santangelo and Filippo Mezzanotti for excellent research assistantship, and Peggy Eppink for editorial help. We also thank Amit Seru for providing us with a time series of actual strategic default within his sample. 1 In 2009, for the first time since the Great Depression, millions of American households found themselves with a mortgage that exceeded the value of their home. -

An Overview of the Housing Finance System in the United States

An Overview of the Housing Finance System in the United States Updated January 18, 2017 Congressional Research Service https://crsreports.congress.gov R42995 An Overview of the Housing Finance System in the United States Summary When making a decision about housing, a household must choose between renting and owning. Multiple factors, such as a household’s financial status and expectations about the future, influence the decision. Few people who decide to purchase a home have the necessary savings or available financial resources to make the purchase on their own. Most need to take out a loan. A loan that uses real estate as collateral is typically referred to as a mortgage. A potential borrower applies for a loan from a lender in what is called the primary market. The lender underwrites, or evaluates, the borrower and decides whether and under what terms to extend a loan. Different types of lenders, including banks, credit unions, and finance companies (institutions that lend money but do not accept deposits), make home loans. The lender requires some additional assurance that, in the event that the borrower does not repay the mortgage as promised, it will be able to sell the home for enough to recoup the amount it is owed. Typically, lenders receive such assurance through a down payment, mortgage insurance, or a combination of the two. Mortgage insurance can be provided privately or through a government guarantee. After a mortgage is made, the borrower sends the required payments to an entity known as a mortgage servicer, which then remits the payments to the mortgage holder (the mortgage holder can be the original lender or, if the mortgage is sold, an investor). -

Predatory Mortgage Loans

CONSUMER Information for Advocates Representing Older Adults CONCERNS National Consumer Law Center® Helping Elderly Homeowners Victimized by Predatory Mortgage Loans Equity-rich, cash poor, elderly homeowners are an attractive target for unscrupulous mortgage lenders. Many elderly homeowners are on fixed or limited incomes, yet need access to credit to pay for home repairs, medical care, property or municipal taxes, and other expenses. The equity they have amassed in their home may be their primary or only financial asset. Predatory lenders seek to capitalize on elders’ need for cash by offer- ing “easy” credit and loans packed with high interest rates, excessive fees and costs, credit insurance, balloon payments and other outrageous terms. Deceptive lending practices, including those attributable to home improvement scams, are among the most frequent problems experienced by financially distressed elderly Americans seeking legal assistance. This is particularly true of minority homeowners who lack access to traditional banking services and rely disproportionately on finance compa- nies and other less regulated lenders. But there are steps advocates can take to assist vic- tims of predatory mortgage loans. • A Few Examples One 70 year old woman obtained a 15-year mortgage in the amount of $54,000 at a rate of 12.85%. Paying $596 a month, she will still be left with a final balloon payment of nearly $48,000 in 2011, when she will be 83 years old. Another 68 year old woman took out a mortgage on her home in the amount of $20,334 in the early 1990s. Her loan was refinanced six times in as many years, bringing the final loan amount to nearly $55,000.