31 March 2010 ARA Asset Management

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Prospectus E.Pdf

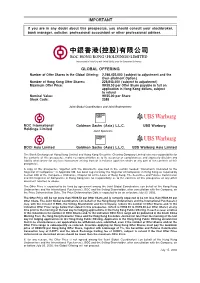

IMPORTANT If you are in any doubt about this prospectus, you should consult your stockbroker, bank manager, solicitor, professional accountant or other professional adviser. (Incorporated in Hong Kong with limited liability under the Companies Ordinance) GLOBAL OFFERING Number of Offer Shares in the Global Offering: 2,298,435,000 (subject to adjustment and the Over-allotment Option) Number of Hong Kong OÅer Shares: 229,843,500 (subject to adjustment) Maximum OÅer Price: HK$9.50 per OÅer Share payable in full on application in Hong Kong dollars, subject to refund Nominal Value: HK$5.00 per Share Stock Code: 2388 Joint Global Coordinators and Joint Bookrunners BOC International Goldman Sachs (Asia) L.L.C. UBS Warburg Holdings Limited Joint Sponsors BOCI Asia Limited Goldman Sachs (Asia) L.L.C. UBS Warburg Asia Limited The Stock Exchange of Hong Kong Limited and Hong Kong Securities Clearing Company Limited take no responsibility for the contents of this prospectus, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this prospectus. A copy of this prospectus, together with the documents speciÑed in the section headed ""Documents Delivered to the Registrar of Companies'' in Appendix VIII, has been registered by the Registrar of Companies in Hong Kong as required by Section 38D of the Companies Ordinance, Chapter 32 of the Laws of Hong Kong. The Securities and Futures Commission and the Registrar of Companies in Hong Kong take no responsibility as to the contents of this prospectus or any other document referred to above. -

Chiyu Banking Corporation Limited Or 2

DIRECT DEBIT AUTHORISATION 直接付款授權書 Application method: 申請方法: 1. Return this form to any branch of Chiyu Banking Corporation Limited or 2. Mail this form to “3/F, Bank of China Centre, 1. 將此表格交回任何一間集友銀行有限公司的分行 或 2. 郵寄表格至“西九龍海輝道 11 號奧海城 Olympian City, 11 Hoi Fai Road, West Kowloon, Hong Kong Attn: Autopay Section” or 3. Via Personal Internet Banking 中銀 中心 3 樓, 送:自動轉賬組”或 3.經個人網上銀行透過「雙重認証」辦理(毋需填寫此表格) with the use of two factor authentication (No need to fill in this form) Please write in BLOCK letters. 請以英文正楷填寫 Customer Information 客戶資料 My/Our Bank Name and Branch 本人/吾等之銀行及分行之名稱 Bank No.銀行編號 Branch No.分行編號 My/Our Account No.本人/吾等之賬戶號碼 Chiyu Banking Corporation Ltd My/Our Name(s) as recorded on Statement/Passbook 本人/吾等在結單/存摺上所紀錄之名稱 貨幣 Currency: Contact Tel No.聯絡電話號碼 HKD Please set up the following Direct Debit Authorisation Records marked with “” for me/us.請為本人(吾等)設立下列已選取 “” 號之直接付款授權紀錄。 Name of Party to be Credited (The Beneficiary) Account no. to be credited †Debtor’s Reference (Compulsory Field) †Limit for Each Payment †Expiry Date 到期日 收款方 (受益人) 收款賬戶號碼 債務人參考 (必須填寫) 每次付款之限額 (DD/MM/YY) (日/月/年) 港幣 HK$: HR21 Limited 012-737-10230564 1. I/We hereby authorise my/our above named Bank to effect transfers from my/our account to the above account in accordance with such instructions as my/our Bank may receive from the beneficiary and/or its banker and/or its banker’s correspondent from time to time provided always that the amount of any one such transfer shall not exceed the limit indicated above. -

Management Profiles ဳଉᄙᓯʍ

team ྆අ Management profiles ဳଉᄙᓯʍ Executive Director ਨϷ໎ԑ ȹȾȾȹαכᐢസeᖓͱ́ܧMr. LAW Ka Sing, aged 55, is the Chairman and Chief Executive Offi cer of the Group. Mr. Law joined the ᖓࡼັͱ́cଊα55ัcݯ̯එ྆ɾ˚࠹Ϸ ιϸႇdཌྷਕʥғೕพ৻ʿࠍɰዶୃ༩ɀɊʒαeכGroup in 1991 and has over 26 years’ experience in garment manufacturing, retailing and wholesale business. ˱̯එ྆c He is responsible for the overall management and strategic planning of the Group. ֤߲ஐ̯එ྆ɾኬဳଉʥ೪ஃིɮАe ࠗಋଉɮɣነכMs. CHAN So Kuen, aged 46, is the Director of Finance of the Group. Ms. Chan graduated from The Hong Kong ஹॖɤɡcଊα46ัcݯ̯එ྆ɾল৻໎ԑeஹɤɡଓพ τɮਆဳଉဨɡჀe֤͛ݯߜਝऋஈʔႏผ߮ܛɣነcےPolytechnic University and Oklahoma City University, the United States of America, with a Master’s Degree in ʥਝෙКּ୩ ɀཌྷཌྷɍαɄ˂˱̯එ྆cכBusiness Administration. She is also a fellow member of the Association of Chartered Certifi ed Accountants ʔผʥࠗಋผ߮ʔผɾ༅૯ผࡗeஹɤɡ ᄗ߮ᅢdࣁ༝พdࡼཋพd˸ኒʥཌྷਕϷพ೩ɾᄗ߮dল৻ဳଉʥכ and the Hong Kong Institute of Certifi ed Public Accountants. Ms. Chan joined the Group in August 2003. She has more than 23 years’ experience in auditing, fi nancial management and corporate fi nance in audit fi rm, travel, ဳଉᄙᓯʍ cஹɤɡ߲ஐ̯එ྆ɾኬکพল৻ʿࠍcɰዶୃ༩ɀɊɍαe͌ͬ household appliances, semiconductor and retail industries. Ms. Chan is responsible for the overall fi nancial ɮАe֤͛ݯ̯එ྆ɾڝdʑᄗ߮ʥҙ༅ّᗐ܁ল৻ဳଉdͬพল৻dؒ management, corporate fi nance, legal, internal audit and investor relation functions of the Group. She is also ʔ̇ो࣊ʥ༅ࣟผ߮e the Company Secretary and the Qualifi ed Accountant of the Group. ਨϷ໎ԑڈIndependent Non-executive Director ዟ͓ Management profiles ɀཌྷཌྷ̒αȾ˂Ᏽկͨc͛ݯ̯ʔ̇ᄗ࣏կࡗผכMs. LEUNG Mei Han, aged 47, was appointed in September 2004, is also the Chairman of the Audit Committee ષᄐɤɡcଊα47ัc ɡᙬɣነਆޫነɡነϽcݯዌݘנτዌݘܛand the Remuneration Committee of the Company. -

Route 22M Bus-Bus Interchange Scheme

Route 22M Bus-Bus Interchange Scheme This BBI Scheme is jointly provided by NWFB and Citybus, including Route 20, 22M, 608, 796C, 796E, 796X, A22, A23, E22S, E23 and E23A. It is designed for passengers traveling between Kowloon, Tseung Kwan O, Clear Water Bay, Hong Kong or Airport. Passengers should use the same Octopus card to make interchange within prescribed time limit at the following bus stop to enjoy the fare discount. From Kowloon to Kowloon / Tseung Kwan O / Clear Water Bay / Hong Kong / Airport First Journey on Alighting Point / Interchange Point Second Journey on Discount Fare Time Limited (Direction) (Direction) 22M from Kai Tak Kai Tak (Kai Ching) A23 to Airport First Journey 60 minutes (Cruise Terminal) Free 22M from Kai Tak Muk Hung Street, A23 toTsz Wan Shan First Journey 60 minutes (Cruise Terminal) Shing Kai Road (North) Free 22M from Kai Tak Regal Oriental Hotel, A22 to Airport / Lam Tin First Journey 60 minutes (Cruise Terminal) Prince Edward Road East Station Free E23/ A to Airport / Tsz Wan Shan (South) 796C toOscar By The Sea 796X to Tseung Kwan O Station 22M from Kai Tak Muk Hung Street, 20 to Tai Kok Tsui Free 60 minutes (Cruise Terminal) Shing Kai Road (Island Harbour View) 22M from Kai Tak Regal Oriental Hotel, 796C to So Uk Free 60 minutes (Cruise Terminal) Prince Edward Road East 796E to So Uk 22M from Kai Tak The Latitude, 796X to Tsim Sha Tsui Free 60 minutes (Cruise Terminal) Prince Edward Road East (East) 22M from Kowloon City Kai Tak (Kai Ching) 20 to Kai Tak Free 120 minutes (Muk On Street) 22M from -

Bossini International Holdings Ltd. Fundamental Company Report

+44 20 8123 2220 [email protected] Bossini International Holdings Ltd. Fundamental Company Report Including Financial, SWOT, Competitors and Industry Analysis https://marketpublishers.com/r/B74D30F6452BEN.html Date: September 2021 Pages: 50 Price: US$ 499.00 (Single User License) ID: B74D30F6452BEN Abstracts Bossini International Holdings Ltd. Fundamental Company Report provides a complete overview of the company’s affairs. All available data is presented in a comprehensive and easily accessed format. The report includes financial and SWOT information, industry analysis, opinions, estimates, plus annual and quarterly forecasts made by stock market experts. The report also enables direct comparison to be made between Bossini International Holdings Ltd. and its competitors. This provides our Clients with a clear understanding of Bossini International Holdings Ltd. position in the Retail Industry. The report contains detailed information about Bossini International Holdings Ltd. that gives an unrivalled in-depth knowledge about internal business- environment of the company: data about the owners, senior executives, locations, subsidiaries, markets, products, and company history. Another part of the report is a SWOT-analysis carried out for Bossini International Holdings Ltd.. It involves specifying the objective of the company's business and identifies the different factors that are favorable and unfavorable to achieving that objective. SWOT-analysis helps to understand company’s strengths, weaknesses, opportunities, and possible threats against it. The Bossini International Holdings Ltd. financial analysis covers the income statement and ratio trend-charts with balance sheets and cash flows presented on an annual and quarterly basis. The report outlines the main financial ratios pertaining to profitability, margin analysis, asset turnover, credit ratios, and Bossini International Holdings Ltd. -

2015-16 Outlook for the Retail and Consumer Products Sector in Asia

www.pwc.com 2015-16 Outlook for the Retail and Consumer Products Sector in Asia Foreword One doesn’t have to live in Shanghai or particularly active users of mobile products. Not a bad place to start for Mumbai to understand that the most technology and social media, and the global retailers looking for new paths dynamic markets – and many of today’s use of these technologies for to growth. most creative retailers – reside in Asia. purchasing, while still nascent, is Just this past November the Western bound to increase as screen size and I invite you to read this report to learn press was filled with stories touting security issues are resolved. In fact, more about the retail opportunities in China’s 2014 Singles Day sales of China will soon overtake the US as the Asia. Finally, I would like to express my US$9.3 billion, which beat out the world’s biggest retail market, and most great appreciation to Mr Chitranjan Dar combined US’s Black Friday and Cyber of the rest of the region will see retail of ITC Limited, Ms Lixia Tan of Haier, Mr Monday shopping days by more than spending growth far in excess of the Masaaki Kanai of Ryohin Keikaku, and two times. global average over the next five Mr Weiming Cao of Hermès, for their years.3 time and sharing their business insights The genius of Singles Day is that it’s the and visions. I am sure you will enjoy perfect microcosm for the scope and Then there is the urbanisation factor. -

BOC HKGCC VISA Card Application Form

BOC HKGCC VISA Card Perpetual Annual Fee Waiver Hong Kong Residential Country Area OTHER INSTRUCTIONS Application Form Tel. No. Code Code Signature of Main Card applicant (Please do not alter) Date Mobile Phone/ Country Area Please send statement to : Residential Address Company Address Pager No. Code Code ATM Screen Language : Chinese 1 English 2 Accommodation Private Property (Mortgaged) 2 Home Ownership Scheme Housing (Mortgaged) 3 Rented 6 The address selected above will be used as your correspondence address in the event your application Please submit the completed application form with the supporting documents to BOC Credit Card (Int’l) Ltd., 3/F, Bank of China Centre, Olympian City, 11 Hoi Fai Road, West Kowloon. Monthly Installment / Rental: Singly Jointly HKD is approved. Referral Branch / Dept. No. 012 Self-owned (Not Mortgaged) 1 Public Housing / Tenants Purchase Scheme 5 Relatives 4 Quarters / Others 7 Set-up opt-out of “Over-the-limit Facility” function Staff No. 0 0 Education University or above 01 Post Secondary 02 Secondary 03 I request the Company to set up the parameters for my main and additional credit card(s) (if any) SC=390 RoadShow SC approved as a result of this application to decline over-the-limit transaction whenever it occurs so Primary 04 Others 05 CIN record checked: □ No SP / □ Yes with SP, please specify: as to avoid any charge for Overlimit Handling Fee. Please complete in BLOCK Letters and put a “3” in the appropriate box. If you wish to set-up opt-out of Over-the-limit Facility function for other BOC credit card account(s), BOC Credit Card (International) Ltd. -

GEO REPORT No. 282

EXPERT REPORT ON THE GEOLOGY OF THE PROPOSED GEOPARK IN HONG KONG GEO REPORT No. 282 R.J. Sewell & D.L.K. Tang GEOTECHNICAL ENGINEERING OFFICE CIVIL ENGINEERING AND DEVELOPMENT DEPARTMENT THE GOVERNMENT OF THE HONG KONG SPECIAL ADMINISTRATIVE REGION EXPERT REPORT ON THE GEOLOGY OF THE PROPOSED GEOPARK IN HONG KONG GEO REPORT No. 282 R.J. Sewell & D.L.K. Tang This report was originally produced in June 2009 as GEO Geological Report No. GR 2/2009 2 © The Government of the Hong Kong Special Administrative Region First published, July 2013 Prepared by: Geotechnical Engineering Office, Civil Engineering and Development Department, Civil Engineering and Development Building, 101 Princess Margaret Road, Homantin, Kowloon, Hong Kong. - 3 - PREFACE In keeping with our policy of releasing information which may be of general interest to the geotechnical profession and the public, we make available selected internal reports in a series of publications termed the GEO Report series. The GEO Reports can be downloaded from the website of the Civil Engineering and Development Department (http://www.cedd.gov.hk) on the Internet. Printed copies are also available for some GEO Reports. For printed copies, a charge is made to cover the cost of printing. The Geotechnical Engineering Office also produces documents specifically for publication in print. These include guidance documents and results of comprehensive reviews. They can also be downloaded from the above website. The publications and the printed GEO Reports may be obtained from the Government’s Information Services Department. Information on how to purchase these documents is given on the second last page of this report. -

District Profiles 地區概覽

Table 1: Selected Characteristics of District Council Districts, 2016 Highest Second Highest Third Highest Lowest 1. Population Sha Tin District Kwun Tong District Yuen Long District Islands District 659 794 648 541 614 178 156 801 2. Proportion of population of Chinese ethnicity (%) Wong Tai Sin District North District Kwun Tong District Wan Chai District 96.6 96.2 96.1 77.9 3. Proportion of never married population aged 15 and over (%) Central and Western Wan Chai District Wong Tai Sin District North District District 33.7 32.4 32.2 28.1 4. Median age Wan Chai District Wong Tai Sin District Sha Tin District Yuen Long District 44.9 44.6 44.2 42.1 5. Proportion of population aged 15 and over having attained post-secondary Central and Western Wan Chai District Eastern District Kwai Tsing District education (%) District 49.5 49.4 38.4 25.3 6. Proportion of persons attending full-time courses in educational Tuen Mun District Sham Shui Po District Tai Po District Yuen Long District institutions in Hong Kong with place of study in same district of residence 74.5 59.2 58.0 45.3 (1) (%) 7. Labour force participation rate (%) Wan Chai District Central and Western Sai Kung District North District District 67.4 65.5 62.8 58.1 8. Median monthly income from main employment of working population Central and Western Wan Chai District Sai Kung District Kwai Tsing District excluding unpaid family workers and foreign domestic helpers (HK$) District 20,800 20,000 18,000 14,000 9. -

Branch Network & Corporate

BRANCH NETWORK & CORPORATE BANKING CENTRES Bank of China (Hong Kong) – Branch Network Hong Kong Island Branch Address Telephone Branch Address Telephone Central & Western District Quarry Bay Branch Parkvale, 1060 King’s Road, Quarry Bay, 2564 0333 Bank of China Tower Branch 1 Garden Road, Hong Kong 2826 6888 Hong Kong Sheung Wan Branch 252 Des Voeux Road Central, Hong Kong 2541 1601 Queen’s Road West 2-12 Queen’s Road West, Sheung Wan, 2815 6888 Southern District (Sheung Wan) Branch Hong Kong Tin Wan Branch 2-12 Ka Wo Street, Tin Wan, Hong Kong 2553 0135 Connaught Road Central Branch 13-14 Connaught Road Central, Hong Kong 2841 0410 Stanley Branch Shop 401, Shopping Centre, Stanley Plaza, 2813 2290 Central District Branch 2A Des Voeux Road Central, Hong Kong 2160 8888 Hong Kong Central District 71 Des Voeux Road Central, Hong Kong 2843 6111 Aberdeen Branch 25 Wu Pak Street, Aberdeen, Hong Kong 2553 4165 (Wing On House) Branch South Horizons Branch G38, West Centre Marina Square, 2580 0345 South Horizons, Ap Lei Chau, Hong Kong Shek Tong Tsui Branch 534 Queen’s Road West, Shek Tong Tsui, 2819 7277 Hong Kong South Horizons Branch Safe Box Shop 118, Marina Square East Centre, 2555 7477 Service Centre Ap Lei Chau, Hong Kong Western District Branch 386-388 Des Voeux Road West, Hong Kong 2549 9828 Wah Kwai Estate Branch Shop 17, Shopping Centre, Wah Kwai Estate, 2550 2298 Shun Tak Centre Branch Shop 225, 2/F, Shun Tak Centre, 2291 6081 Hong Kong 200 Connaught Road Central, Hong Kong Chi Fu Landmark Branch Shop 510, Chi Fu Landmark, Pok Fu Lam, -

Participating Buildings in Tsuen Wan District 荃灣區的參與屋苑

Tsuen Wan (荃灣) Estates (屋苑) Estate/Building 屋苑/大廈 Allway Gardens 荃威花園 Anglers' Bay 海雲軒 Bayview Garden 灣景花園 Bellagio 碧堤半島 Belvedere Garden (Phase I) 麗城花園(第一期) Belvedere Garden (Phase II) 麗城花園(第二期) Belvedere Garden (Phase III) 麗城花園(第三期) Bo Shek Mansion 寶石大廈 Chelsea Court 爵悅庭 Cheung Shan Estate 象山邨 City Point 環宇海灣 Clague Garden Estate 祈德尊新邨 Discovery Park 愉景新城 Fou Wah Centre 富華中心 Fuk Loi Estate 福來邨 Golden Villa 金麗苑 Greenview Terrace 翠景臺 H Cube 立坊 Hanley Villa 恆麗園 Harmony Garden Block 2 康睦庭園(第二座) Hong Kong Garden 豪景花園 Indihome 樂悠居 Jade Plaza 翡翠廣場 Kam Fung Garden 錦豐園 Lei Muk Shue (1) Estate 梨木樹(一)邨 Lei Muk Shue (2) Estate 梨木樹(二)邨(松樹樓,竹樹樓,葵樹樓) (Chung Shue, Chuk Shue & Kwai Shue Hse) Estate/Building 屋苑/大廈 Lei Muk Shue Estate 梨木樹邨 Lido Garden 麗都花園 Long Beach Garden 海濤花園 Lotus Villa 芙蓉雅苑 Luk Yeung Sun Chuen 綠楊新邨 Lung Tang Court 龍騰閣 Moon Lok Dai Ha 滿樂大廈 New Haven 名逸居 Ocean Pointe 縉皇居 Ocean Pride 海之戀 Parc City 全·城滙 Park Island 珀麗灣 Primrose Hill 縉庭山 Rhine Garden 海韻花園 Rhine Terrace 海韻臺 Riviera Gardens 海濱花園 Royal Dragon Villa 嘉御龍庭 Royal Sea Crest 帝華軒 Sea Crest Villa Phase 1 浪翠園(第1期) Sea Crest Villa Phase 2 浪翠園(第2期) Sea Crest Villa Phase 3 浪翠園(第3期) Sea Crest Villa Phase 4 浪翠園(第4期) Serenade Cove 韻濤居 Sheeny Terrace 千里台 Shek Wai Kok Estate 石圍角邨 Sheung Chui Court 尚翠苑 Skyline Plaza 灣景廣場 Summit Terrace 翠豐臺 The Blue Yard 海天豪苑 Estate/Building 屋苑/大廈 The Cairnhill 朗逸峯 The Cliveden 寶雲匯 The Dynasty 御凱 The Panorama 蔚景花園 The Pavilia Bay 柏傲灣 The Rise 昇柏山 The Westminster Terrace 皇壁 Tsuen Fung Centre 荃豐中心 Tsuen Kam Centre 荃錦中心(住宅) Tsuen King Garden (II) 荃景花園第二期 Tsuen -

French Firms in Macau -.:: GEOCITIES.Ws

TABLE OF CONTENTS LIST OF FIRMS: BREAKDOWN BY SECTORS 3 LIST OF FIRMS BY ALPHABETICAL ORDER 9 LIST OF FIRMS BY PARENT COMPANY 89 LIST OF FIRMS BY PARENT COMPANY 95 French Firms in Hong Kong and Macau - 1999 Edition LIST OF FIRMS: BREAKDOWN BY SECTORS Advertising EURO RSCG PARTNERSHIP Beverages, wines & spirits FIRST VISION LTD. ADET SEWARD FLEXICOM BELCOMBE CO. LTD. FRENCH FASHION LTD CALDBECKS LTD. IMAGE SOLUTIONS CASELLA FAR EAST LIMITED MERCURY PUBLICITY (HK) LTD. CHATEAU DE LA TOUR (ASIA) LTD. SPICY CREATION HK LTD. CHEVAL QUANCARD ASIA LTD CREACTION INTERNATIONAL LTD. CULINA (H.K.) LIMITED Aeronautics DUISDALE LTD. AIRBUS INDUSTRIE-MACAO EURO LUXE (HONG KONG) LTD. DASSAULT FALCON JET CORP FICOFI (INTERNATIONAL) LTD. ELTRA AERONAUTICS FIMOXY CO LTD. METROJET LTD. GRANDS CRUS DE FRANCE LTD. / FRENCH WINE J.L.C. & MOUEIX FAR EAST LTD. JEAN PHILIPPE INTERNATIONAL (HK) LTD Agriculture - Foodstuffs MARTELL FAR EAST TRADING LTD. MEGAREVE AMOY FOOD LTD. MOET HENNESSY ASIA PACIFIC ASIATIQUE EUROPEENNE DE COMMERCE LTD. OLIVIER ASIA LTD. BALA FAR EAST LIMITED OLIVIER HONG KONG LTD. CULINA (H.K.) LIMITEDDELIFRANCE (HK) LTD. PR ASIA DANONE REMY CHINA & HK LTD. EURO LUXE (HONG KONG) LTD. REMY PACIFIQUE LTD. FARGO SERVICES (H.K.) LTD. RICHE MONDE LTD. GRANDS CRUS DE FRANCE LTD. / FRENCH WINE SAVEURS INTERNATIONAL LIMITED INNOLEDGE INTERNATIONAL LTD. SINO-FRENCH RESOURCES LTD. INTERNATIONAL COMMERCIAL AGENCIES SOPEXA LTD. LA ROSE NOIRE TAHLEIA LTD. LESAFFRE (FAR EAST) LTD. LVMH ASIA PACIFIC LTD. OLIVIER ASIA LTD. OLIVIER HONG KONG LTD. Building construction SOPEXA LTD. BACHY SOLETANCHE GROUP TAHLEIA LTD. BOUYGUES DRAGAGES ASIA VALRHONA FAR EAST BYME ENGINEERING (HK) LTD CAMPENON BERNARD SGE DEXTRA PACIFIC LTD.