Capabilities for Mass Market Innovations in Emerging Economies

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ford: the Evolution of Automobiles, Components, and Design

Ford: The Evolution of Automobiles, Components, and Design Honors Project In fulfillment of the Requirements for The Esther G. Maynor Honors College University of North Carolina at Pembroke By Janelle Horton Department of Mathematics and Computer Science 04/26/2016 -/ (_,•('"•*"•"-* y^y '.'riJ*'-'-f "^ xf^nelle Horton// Date //-•'Honors Cc Charles Lillie, Ph.D. Date Faculty Mentor Teagan Decker, Ph.D. Date Senior Project Coordinator Acknowledgments I would like to show my greatest appreciation to the assistant professor of the Department of Mathematics and Computer Science, Professor Charles Lillie. Not only for agreeing to be my mentor throughout my honors senior project, but for also suggesting valid points to make within my essay and final PowerPoint presentation that would better my research. I appreciate Professor Lillie for taking the time out of his schedule to meet with me during his office hours to discuss ideas and interesting facts that would be essential to crafting my essay. I would also like to recognize my cousin Neleze Meadows for helping me in narrowing down my broad topic to solely focusing on the evolution of Ford auto-motives. My cousin helped me chose an automobile company that has had the biggest transformation from beginning to end, and is continuously still growing in the 21st century. With the help of both my mentor Professor Lillie and my cousin Neleze Meadows, once again thank you for your input towards devising my Honors Mayor College senior project. ii TABLE OF CONTENTS Abstract.......................................................................................................................................... -

Nine Things I Learned from Alan Mulally Bryce G

Nine Things I Learned from Alan Mulally Bryce G. Hoffman ChangeThis | 93.01 In the summer of 2010, I decided to take a year off from my job as a journalist with The Detroit News to write a book about one of the most amazing comebacks in business history: the turnaround of Ford Motor Company. As the Ford beat reporter for the News, I had covered every twist and turn of that epic drama. I knew that this story was about much more than saving a car company. It was a roadmap for changing cultures. When Alan Mulally arrived in Dearborn in September 2006, he knew little about the automobile industry. However, he had already figured out how to take a dysfunctional organization that was being ripped apart by managerial infighting and turn it into a model of collaboration and effi- ciency. Mulally had proven that at the Boeing Company, where he was credited with saving the commercial aircraft division from a series of catastrophes ranging from the Asian financial crisis of the late 1990s to the terrorist attacks of September 11, 2001, that had cost Boeing most of its business. But Mulally’s biggest accomplishment in Seattle was saving Boeing from itself. Now Bill Ford Jr. was asking him to do the same thing with Ford. It was a daunting task. Ford—the company that put the world on wheels—was on the verge of bankruptcy. For decades, it had been fighting a losing battle against foreign automakers that not only made better cars, but also did so more efficiently and at substantially lower cost. -

FRONT WHEEL BEARINGS W.E.F:-01/02/2016 Sr No Kingtec No

ANAND BEARING CORPORATION 381/B,VITHAL NIWAS,V.P.ROAD MUMBAI-4, INDIA TEL:- 00-91-22-23883045,65914227 MOB:- 9820414446/9820085500 EMAIL:- [email protected] website:- www.mnrgoldbearings.com FRONT WHEEL BEARINGS W.E.F:-01/02/2016 Sr No Kingtec No. Vehicle Application Price (Rs.) Maruti 1000, Esteem, Zen (N/M)& Maruti Car 1 DAC 3668 AWCS36 2RS (Koyo, FAG Type) Type II/ Van type 2/3 370.00 2 DAC 3562AWCS5 Suzuki Wagon R & Alto/Estilo/A-Star 450.00 3 DAC35680037 Uno Diesel,Tata Indica,Siena & Palio 385.00 Hyundai Accent & Santro N/M, Getz, i10, i20, 4 DAC3870 (38 x 70 x 37) Verna 450.00 4A 51720-3870 HYUNDAI I20 ELITE (2014 ONWARDS) POR Ford Ikon, Fiesta, Fusion, Figo, Escort, Opel N/M, 5 DAC39720037 Indigo & Marina 450.00 5A DAC 39720037 ABS Fiesta, Fusion,Figo,Indigo,Marina ABS 625.00 6 BAHB 633313CA Uno Petrol, Mahindra Gio Fw and Rw 400.00 7 DAC 3872W-10CS42 Honda City - Type 1-2 515.00 8 DAC 3873040 Honda City - Type 3-4, CRV RR Wheel 560.00 8C DAC 3873040 ABS Honda City - Type 3-4, CRV RR Wheel 900.00 8A DAC 387440 ABS Honda City - Type 5/Jazz 750.00 8B DAC 437844 ABS Honda Civic 850.00 Mitsibushi Lancer Petrol & Diesel New Model 9 40x74x36 ZZ CLOSED DESIGN Closed Design 570.00 10 40X74X36/34 OPEN DESIGN Mitsibushi Lancer O/M (without Seal) 530.00 10A 40X80 Lancer Cedia 11 34BWD04 - 6437 Chevrolet Aveo, Cielo, U-VA,Chevy Beat 400.00 12 805800 Maruti Suzuki Swift , Ritz 560.00 12A DAC 3666 Hyundai Eon 575.00 12B 805800 ABS Maruti Suzuki Swift , Ritz 750.00 13 BAHB 636149CC N/ ABS Suzuki SX4 & Tata Winger/ERTIGA 780.00 14 BAHB 636149CC -

International Bulletin October 2012

www.smmt.co.uk/international International Bulletin October 2012 Key Contents Editorial SMMT dates Book now! UK events Trade events around the world Industry support initiatives International market snapshots International business opportunities JCC customs information papers SMMT, the 'S' symbol and the ‘Driving the motor industry’ brandline are trademarks of SMMT Ltd 2 Attending international trade shows A dozen ways to ensure your investment doesn’t fail. Attending trade shows is a big investment in time and money but works on a number of levels and it can be an extremely cost-effective way to develop leads and make sales if properly planned. Sustainable success is only likely to develop with regular year-on-year attendance at the same shows demonstrating your credibility, stability and long-term intention in the market. It may take several years of attendance at the same show before potential customers start to develop stronger interest in your company. Taking part in overseas shows and exhibitions is a considerable cost- although the SMMT UK Group Pavilion format and UKTI Tradeshow Access Grant scheme support can substantially reduce costs compared to “going it alone”. Skilful planning and execution, before, during and after the trade show, is essential to get results and the following checklist of 12 points might help you get the most from future events: 1. Set objectives – Understand what you want to achieve and who on the stand is tasked to do what each day. You may want to increase market share, introduce new products or services, check out competitors, meet and socialise with existing clients, meet / train agents or distributors, etc. -

3Aces Enterprises

+91-8048372769 3aces Enterprises https://www.indiamart.com/3acesenterprises/ We are leading wholesale trader and manufacturer of Car Seat Cover, Car Neck Pillow, PVC Leather Fabric, Waterproof Car Body Cover, Leather Steering Wheel Cover and many more. About Us A premier name of this domain, “3 Aces Enterprises” is engrossed in this occupation of manufacturing and wholesale trading since 2009. Formed at Madhurawada, Visakhapatnam, Andhra Pradesh by a squad of experts with vast experience and sound knowledge of this field. The spectrum of products we ship to our clients includes Car Seat Cover,Car Neck Pillow and Leather Steering Wheel Cover. Every order that we undertake is developed on the principles of innovation, learning and immense knowledge that we garner from each of our every assignment is utilize for better benefits. For more information, please visit https://www.indiamart.com/3acesenterprises/aboutus.html CAR SEAT COVER O u r P r o d u c t R a n g e Swift Car Seat Cover PVC Leather Car Seat Cover Designer Car Seat Covers Synthetic Leather Car Seat Cover SEAT COVER O u r P r o d u c t R a n g e Mahindra Bolero polo leather Mahindra Xylo Car Seat Cover seat covers BLR Polo Leather VSP Maruthi Suzuki Alto Car Seat Alto LXI Car Seat Cover Polo Cover Polo Leather VSP Leather VSP LEATHER CAR SEAT COVERS O u r P r o d u c t R a n g e Mahindra Scorpio Seat Covers Mahindra XUV 300 Car Seat Polo Leather HYD Covers Polo Leather VSP Mahindra TUV 300 Car Seat Swift Nappa Leather Car Seat Cover Polo Leather VSP Cover CAR NECK PILLOW O u r -

Company Description

Analysis of Strategic Alliance with Ford MINOR PROJECT REPORT ON STRATEGIC ALLIANCES – FORD MOTOR COMPANY BUILT FOR THE ROAD AHEAD. Submitted for fulfillment of the requirement for the award of the degree of Bachelor of Business Administration To Guru Gobind Singh Indraprastha University Under the guidance of: Mrs. Nidhi Prasad Submitted by: Sandeep Singh Sethi 1 SANDEEP SINGH Analysis of Strategic Alliance with Ford Roll No.: 05910601709 ANSAL INSTITUTE OF TECHNOLOGY TO WHOMSOEVER IT MAY CONCERN This is to certify that the minor project report titled STRATEGIC ALLIANCES – FORD MOTOR COMPANY carried out by SANDEEP SINGH has been accomplished under my guidance and supervision as a duly registered BBA student of the ANSAL INSTITUTE OF TECHNOLOGY (G.G.S I.P. University, New Delhi). This project is being submitted by him in the partial fulfillment of the requirements for the award of the Bachelor of Business Administration from I.P. University. His dissertation represents his original work and is worthy of consideration for the award of the degree of Bachelor of Business Administration. ____________________ (Name and Signature of the Internal Faculty Advisor) Title: Date: 2 SANDEEP SINGH Analysis of Strategic Alliance with Ford ACKNOWLEDGEMENT The Project Report is the outcome of many individuals without whom it cannot be molded, so they deserve thanks. I thank my teacher, Mrs. Nidhi Prasad under whose guidance I have been able to successfully complete this project. I thank all of my friends and fellow classmates for their assistance in this project. – Sandeep Singh 3 SANDEEP SINGH Analysis of Strategic Alliance with Ford CONTENTS Page no. -

Fast Forward 2006 Annual Report

Ford Motor Company Ford Motor Company / 2006 Annual Report Fast Forward 2006 www.ford.com Annual Fast Forward Ford Motor Company • One American Road • Dearborn, Michigan 48126 Report cover printer spreads_V2.indd 1 3/14/07 7:41:56 PM About the Company Global Overview* Ford Motor Company is transforming itself to be more globally integrated and customer-driven in the fiercely competitive world market of the 21st century. Our goal is to build more of the products that satisfy the wants and needs of our customers. We are working as a single worldwide team to improve our cost structure, raise our Automotive Core and Affi liate Brands quality and accelerate our product development process to deliver more exciting new vehicles faster. Featured on the front and back cover of this report is one of those vehicles, the 2007 Ford Edge. Ford Motor Company, a global industry leader based in Dearborn, Michigan, manufactures or distributes automobiles in 200 markets across six continents. With more than Dealers 9,480 dealers 1,515 dealers 1,971 dealers 125 dealers 871 dealers 2,352 dealers 1,376 dealers 6,011 dealers and 280,000 employees and more than 100 plants worldwide, the company’s core and affiliated Markets 116 markets 33 markets 25 markets 27 markets 64 markets 102 markets 138 markets 136 markets automotive brands include Ford, Jaguar, Land Rover, Lincoln, Mercury, Volvo, Aston Martin Retail 5,539,455 130,685 188,579 7,000 74,953 428,780 193,640 1,297,966** and Mazda. The company provides financial services through Ford Motor Credit Company. -

Ford India Pvt. Ltd

FORD INDIA PVT. LTD. Background new products in various segments as well as variants Routine calls are also made to Ford dealerships Ford Motor Company (FMC) is the world’s second for existing products. to check the quality of cars delivered to them. largest automotive company after General Motors. • Ford India sells Ikon in five variants viz. Ford Ikon, Constant monitoring of its supplier base Ford had revenues worth US$ 164.5 billion in 2003 Ford Ikon NXT, Ford Ikon 1.3 CLXi NXT, Ford Ford uses a monitoring system to ensure that and is spread across 200 countries with over 327,000 Ikon Sxi, Ford Ikon Flair employees. suppliers adhere to high quality standards and deliver • Ford launched ‘Flair’, at a price aimed at attracting shipments on time. This gives it an assurance of the Ford sells vehicles under various brand names such as the B Plus segment of car customers Aston Martin, Ford, Jaguar, Land Rover, Lincoln, inventory management. • Ford Mondeo comes in two different variants: Mercury and Volvo. Ford India follows its US parent Ford Motor Ford Mondeo, Ford Mondeo Ghia In 1995, FMC established a joint venture company Company’s policy of sourcing components from Q1 with Mahindra & Mahindra (M&M) to assemble and • Ford launched Endeavour to cater to the Sports certified vendors. Achieving the Q1 certification is a distribute the Ford Escort, the company’s first model Utility Vehicle (SUV) market collaborative effort of Ford and its vendors. to be showcased in India. The company was re- Ford India’s purchasing policy requires that all primary christened Ford India in 1999, following a change in High degree of localisation suppliers achieve TPM, TQM, ISO 9000, ISO 14000, equity holding, with Ford buying out a majority stake. -

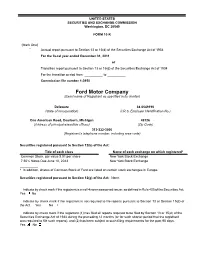

Ford Motor Company (Exact Name of Registrant As Specified in Its Charter)

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, DC 20549 FORM 10-K (Mark One) Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the fiscal year ended December 31, 2011 or Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 For the transition period from __________ to __________ Commission file number 1-3950 Ford Motor Company (Exact name of Registrant as specified in its charter) Delaware 38-0549190 (State of incorporation) (I.R.S. Employer Identification No.) One American Road, Dearborn, Michigan 48126 (Address of principal executive offices) (Zip Code) 313-322-3000 (Registrant’s telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered* Common Stock, par value $.01 per share New York Stock Exchange 7.50% Notes Due June 10, 2043 New York Stock Exchange __________ * In addition, shares of Common Stock of Ford are listed on certain stock exchanges in Europe. Securities registered pursuant to Section 12(g) of the Act: None. Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No Indicate by check mark if the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

AN AUTONEWS 05-26-08 a 54 AUTONEWS.Qxd

AN AUTONEWS 05-26-08 A 54 AUTONEWS 5/23/2008 4:05 PM Page 1 54 • MAY 26, 2008 Top North America-based automotive CEOs, ranked by 2007 total compensation Captains of industry Retirement pay Blue = supplier; Green = automaker; Red = dealership group 2007 2007 2007 2007 2007 deferred Name (age) 2007 2006 2007 bonus & incentive stock option stock award 2007 accumulated compensation Rank title Company total compensation total compensation base salary plan compensation gains gains other pension benefits balance 1 Alexander Cutler (56) Eaton $24,545,516 $14,303,055 $1,069,305 $9,520,197 $11,910,433 $1,820,803 $224,778 $12,842,426 $60,074,535 chairman, president & CEO 2 John Plant (54) TRW Automotive 22,670,224 12,954,324 1,594,167 3,904,000 14,329,500 2,459,110 383,447 39,256,900 614,163 president & CEO 3 Robert Keegan (60) Goodyear Tire & Rubber 18,763,103 11,470,710 1,176,667 12,300,000 5,204,113 0 82,323 11,509,825 642,761 chairman, president & CEO 4 Christopher Kearney (53) SPX 14,936,872 6,119,213 1,000,000 2,500,000 6,023,174 4,842,804 570,894 7,698,910 3,373,713 chairman, president & CEO 5 Theodore Solso (61) Cummins 13,223,409 12,238,722 1,110,000 6,274,000 0 5,691,000 148,409 17,635,689 5,493,879 president & CEO 6 Siegfried Wolf (49) Magna International* 12,686,685 4,422,180 100,000 9,467,000 2,897,880 N.A. -

Mahindra-Integrated-Report-FY17.Pdf

MAHINDRA & MAHINDRA LTD. INTEGRATED REPORT FY 2016-17 MANUFACTURED NATURAL CAPITAL CAPITAL HUMAN CAPITAL FINANCIAL CAPITAL INTELLECTUAL SOCIAL AND CAPITAL RELATIONSHIP CAPITAL EXECUTIVE MESSAGES Message from the Chairman Emeritus 01 Message from the Chairman 02 Message from the Managing Director 03 Message from the Chairman, Group Sustainability Council 05 Message from the Group CFO 07 HOW TO READ OUR REPORT Scope of the Report 08 Report Scope Limitaons 08 Contact Informaon 08 Independent Assurance Statement 09 HOW WE CREATE VALUE Mahindra Group 11 M&M Limited 11 Business Model & Vision 12 Highlights 15 Automove Division 17 Farm Division 19 Awards 20 HOW WE SUSTAIN VALUE Corporate Governance 21 Sustainability & Us 22 Materiality 23 Sustainability Roadmaps 2019 26 Risk Management 31 HOW WE DELIVERED VALUE Financial Capital 33 Manufactured Capital 39 Intellectual Capital 49 Human Capital 51 Natural Capital 60 Social & Relaonship Capital 72 HOW WE PLAN TO ENHANCE VALUE Strategy & Resource Allocaon 88 Opportunies & Outlook 90 ANNEXURES How We Contribute To The SDGs 91 Performance Tables (Natural and Human Capital) 92 GRI G4 Content Index 98 Acronyms 101 Glossary 105 Forward Looking Statements: In this Integrated Report, we have disclosed forward looking informaon to enable stakeholders to comprehend our prospects. This report and other statements - wrien and oral-that we periodically make, contain forward looking statements that set out ancipated results based on the management’s plans and assumpons. We have tried wherever possible to idenfy such statements by using words such as, ‘ancipate’, ‘esmate’, ‘expects’, ‘projects’, ‘intends’, ‘plans’, ‘believes’, and words of similar substance in connecon with any discussion of future performance. -

Iccrbrief Vol. 18 No.6, 1989

ICCRBrief Vol. 18 No.6, 1989 White Wheels of Fortune: Ford and GM in South Africa After decades at the top of the South reevaluated their involvement in South the largest union, the non-racial Na African motor industry, both Ford and Africa. When rumors surfaced that Ford tional Automobile and Allied Workers General Motors moved during might be pulling out, analysts sensed an Union (NAA WU). 1987 -1988 to end all direct investment in important turning point in the history of the country. But neither withdrawal was the industry. Companies like Alfa GENERAL MOTORS: "Braaivleis, what it appeared to be. Both companies Romeo, Peugeot, Renault and Leyland, Rugby, Sunny Skies and Chevrolet" continue to play important behind-the though neither large nor influential in The Ford-Amcar merger left scenes roles in South Africa. They re South Africa, abandoned commercial General Motors as the only wholly- own main a prominent focus for the antiapar manufacturing there. ed American motor vehicle manufac theid movement because of their contin turer in South Africa. GM had followed uing ties to their former South African The Ford-Amcar Merger of 1985 Ford to South Africa in 1926, and like subsidiaries, because of the controversial Ford, chose to build its assembly plant in way in which they sold their South In mid-1984 Ford .secretly began Port Elizabeth. Over the years GM and African assets and because their suc negotiating with Anglo-American's car Ford shared top billing as the leading cessors have resumed vehicle sales to the making company, Amcar, over a possi manufacturers.