³ a Study on Market Potential of Hp Computer: with Reference To

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Uila Supported Apps

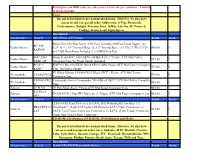

Uila Supported Applications and Protocols updated Oct 2020 Application/Protocol Name Full Description 01net.com 01net website, a French high-tech news site. 050 plus is a Japanese embedded smartphone application dedicated to 050 plus audio-conferencing. 0zz0.com 0zz0 is an online solution to store, send and share files 10050.net China Railcom group web portal. This protocol plug-in classifies the http traffic to the host 10086.cn. It also 10086.cn classifies the ssl traffic to the Common Name 10086.cn. 104.com Web site dedicated to job research. 1111.com.tw Website dedicated to job research in Taiwan. 114la.com Chinese web portal operated by YLMF Computer Technology Co. Chinese cloud storing system of the 115 website. It is operated by YLMF 115.com Computer Technology Co. 118114.cn Chinese booking and reservation portal. 11st.co.kr Korean shopping website 11st. It is operated by SK Planet Co. 1337x.org Bittorrent tracker search engine 139mail 139mail is a chinese webmail powered by China Mobile. 15min.lt Lithuanian news portal Chinese web portal 163. It is operated by NetEase, a company which 163.com pioneered the development of Internet in China. 17173.com Website distributing Chinese games. 17u.com Chinese online travel booking website. 20 minutes is a free, daily newspaper available in France, Spain and 20minutes Switzerland. This plugin classifies websites. 24h.com.vn Vietnamese news portal 24ora.com Aruban news portal 24sata.hr Croatian news portal 24SevenOffice 24SevenOffice is a web-based Enterprise resource planning (ERP) systems. 24ur.com Slovenian news portal 2ch.net Japanese adult videos web site 2Shared 2shared is an online space for sharing and storage. -

Inside HP Labs... O Dolores Hall Fashions an Array of Light Emitting-Diodes at the HPA Division in Palo Alto

Who let the cat out of the bag? Overall, our size, complexity and success tors have been given extra time to rethink make our activities increasingly news and execute their strategy. Your field sales worthy-whether we want that or not. people quickly sense the situation and be To see how it works, put yourself in gm to concentrate on other products. And the place of a division marketing manager: you may even have legal problems. All in Through a combination of marketing all it's going to cost a bundle-in loss of tactics, including news releases, press con sales, of company reputation and of sense ferences, industry showings and advertis of achievement. "Loose as a goose!" ing programs, plus product availability Such potential consequences are by and sales force briefiings, you have plotted no means limited to product introductions. "Leaky as a sieH~" a strategy that you expect will enable your The subject may concern new orders, dol at secrets? Arc there an}' left product to hit the market with maximum lar volume of sales, negotiations of various nd here?" impact. Your goal is to have the world of kinds, price changes, expansion plans, im customers aU of a sudden buzzing with portant contracts, and technical develop the news, clamoring to see and buy-and ments. Leaks of this kind of information getting a big jump on the competition. can be of great interest to the press-and Those comments may sound flippant, Instead, a number of weeks prior to very beneficial and instructive to com but actually they represent serious ap the grand unveiling, Corporate Public petitors. -

GAMING Laptops Why Buy a Desk Hog When Many Portables Pack the Same Horsepower? These Models Do Games, Movies, and More

W I R E D + 250 PRODUCTS TESTED AND RATED FIND THE RIGHT: Digital Cameras Laptops Phonecams Plasma TVs From the Editors of Video Cameras WIRED Wireless Keyboards America’s Premier Photo Printers Tech Magazine MP3 Players Surround Sound Systems Movies-On-Demand W Tablet PCs W Online Music Services W. Media Streamers THE ULTIMATE W Coffeemakers BUYER’S GUIDE I Gaming Accessories TO THE BEST R PLUS: Home theater gear you can afford PRODUCTS E D. D. CAN C O $5.95 | $6.95 M DISPLAY UNTIL FEBRUARY 9, 2005 TESTTHE ULTIMATE BUYER’S GUIDE TO THE BEST PRODUCTS CONTENTS 14 Surviving the Gizmo Explosion Relax: We tested hundreds of products so you don’t have to. by Chris Anderson PLUS: A sneak preview of 7 cool technologies of tomorrow. PLUS: The top 10 reviews from Wired’s Gadget Lab newsletter. 23 Mobile Phones Multifunction phones, megapixel phonecams, and phone-PDA hybrids 32 Scorecard COMMUNICATION PLUS: Internet phone services 35 Digital Cameras 47 Digital Video Cameras Pocket-sized, full-featured compact, MiniDV and tapeless video cameras and digital SLR cameras 43 Scorecard 52 Scorecard CAMERAS PLUS: Photo printers 55 High-Definition TVs 69 Digital Video Recorders Plasma, LCD, and rear-projection TVs, High-definition, standard-definition, and high-end projectors and DVD-burning DVRs 63 Scorecard 75 Scorecard VIDEO PLUS: Budget projectors & PLUS: DVD rental by mail & widescreen PC monitors movies-on-demand RED COVER: Sanyo XactiVPC-C1 pocket camcorder, © PSC/T3 Magazine. Find the US version, Sanyo Fisher FVD-C1, on page 52. BLUE COVER: Panasonic D-Snap SV-AV50A tapeless camcorder, Craig Maxwell. -

Hewlett-Packard Company ("HP") 3000 Hanover Street Palo Alto, California 94304

The NASDAQ Stock Market LLC Form 1 - Exhibit C, Tab 29 Name and Address: Hewlett-Packard Company ("HP") 3000 Hanover Street Palo Alto, California 94304 Details of organization: Stock corporation organized under in its current form under the General Corporation law of the State of Delaware on February 11, 1998. Contractual relationship: The Nasdaq Stock Market, Inc. and HP are parties to Master Lease and Financing Agreements dated October 26,2004 and October 27,2004 and an Enterprise Site License Agreement dated November 15,2004, and 11/15/04. Business or functions: Hewlett-Packard provides the servers and operating systems software for the systems that comprise the Nasdaq Market Center and securities information processor. Certificate of Incorporation: Attached as Exhibit A. By-Laws: Attached as Exhibit B. Officers, Governors, and Standing Committee Members Attached as Exhibit C. I, HARRIET SMITH WINDSOR, SECRETARY OF STATE OF THE STATE OF DELAWARE, DO HEREBY CER!CIPY THE ATTACHED IS A TRUE AND CORRECT COPY OF THE CERTIFICATE OF INCORPORATION OF "HBWLETT-PACRARD COMPANY", FILED IN THIS OFFICE ON THE ELEVENTH DAY OF FEBRUARY, A.D. 1998, AT 5 O'CLOCK P.M. 5d-%b Huric Smith Windsor. kr~yof State 2858384 8100 AUTBEWTICATION: 1665671 020170126 * DATE: 03-14-02 - STATE OF DWiAMARE SZCRETARP OF STAR DXVfSICHI OF CORRaRPTIWS FZW 05: 00 FW 02/11/2998 981055490 - 2858384 CERTIFICATE OF INCORPORATION HEWLET'#'-PACKARD COMPANY ARTICLE I The name of this corporation is Hewlett-Packard Company (the "Corporationn). The addresa of the Corporation's registered office in the State of Ddawan is 1209 Orange Strat, Wilmington, Delaware 19801, County ofNew Castle. -

HP Pavilion Tx2500 Entertainment PC Maintenance and Service Guide © Copyright 2008 Hewlett-Packard Development Company, L.P

HP Pavilion tx2500 Entertainment PC Maintenance and Service Guide © Copyright 2008 Hewlett-Packard Development Company, L.P. AMD, Athlon, Turion, and combinations thereof, are trademarks of Advanced Micro Devices, Inc. Bluetooth is a trademark owned by its proprietor and used by Hewlett- Packard Company under license. Microsoft, Windows, and Windows Vista are either trademarks or registered trademarks of Microsoft Corporation in the United States and/or other countries. SD Logo is a trademark of its proprietor. The information contained herein is subject to change without notice. The only warranties for HP products and services are set forth in the express warranty statements accompanying such products and services. Nothing herein should be construed as constituting an additional warranty. HP shall not be liable for technical or editorial errors or omissions contained herein. This guide is a troubleshooting reference used for maintaining and servicing the computer. It provides comprehensive information on identifying computer features, components, and spare parts; on troubleshooting computer problems; and on performing computer disassembly procedures. First Edition: May 2008 Document Part Number: 488788-001 Safety warning notice WARNING! To reduce the possibility of heat-related injuries or of overheating the computer, do not place the computer directly on your lap or obstruct the computer air vents. Use the computer only on a hard, flat surface. Do not allow another hard surface, such as an adjoining optional printer, or a soft surface, such as pillows or rugs or clothing, to block airflow. Also, do not allow the AC adapter to contact the skin or a soft surface, such as pillows or rugs or clothing, during operation. -

Hp-3000/4000

HP-3000/4000 Terminal User’s Guide This equipment has been tested and found to comply with the limits for a Class B digital device, pursuant to part 15 of the FCC Rules. These limits are designed to provide reasonable protection against harmful interference when the equipment is operated in a commercial environment. This equipment generates, uses, and can radiate radio frequency energy, and, if not installed and used in accordance with the Installation Manual, may cause harmful interference to radio communications. Operation of this equipment in a residential area is likely to cause harmful interference, in which case the user will be required to correct the interference at the user’s own expense. This Class A digital apparatus meets all requirements of the Canadian Interference-Causing Equipment Regulations. Cet appareil numerique de la classe A respecte toutes les exigences du Reglemente sure le materiel brouilleur du Canada. © 2014 Allegion Document Part Number: 70100-6003 – Rev. 3.3 – 07/15/14 HandPunch is a trademark of Schlage Biometrics, Inc. The trademarks used in this Manual are the property of the trademark holders. The use of these trademarks in this Manual should not be regarded as infringing upon or affecting the validity of any of these trademarks. Schlage Biometrics, Inc. reserves the right to change, without notice, product offerings or specifications. No part of this publication may be reproduced in any form without the express written permission from Schlage Biometrics, Inc. Table of Contents Introduction 3 Biometrics -

Retail Prices in RED Color Are Sale Prices. Limit One Per Customer

Retail prices in RED color are sale prices. Limit one per customer. Limited to stock on hand. Cases The parts listed below are normal stock items. However, we also have access to and can special order Addtronics, A-Top, Boomrack, Coolermaster, Enlight, Foxconn, Intel, InWin, Lite-On, PC Power & Cooling, Startech and SuperMicro. Description Manufacturer Model# Mid-Tower ATX Cases Retail Stock Black Elite 350 Mid-Tower ATX Case, Includes 500Watt Power Supply, (4) RC-350- Cooler Master 5.25" & (1) 3.5" External Bays, (6) 3.5" Internal Bays, 16.1"Hx7.1"Wx17.9"D, $95.00 3 KKR500 w/2-USB Front Ports, Includes (1) 120MM Rear Fan SGC-2000- Storm Scout SGC-2000-KKN1-GP Black Steel / Plastic ATX Mid Tower Cooler Master $95.00 1 KKN1-GP Computer Case No Power Supply Included RC-912- HAF 912 RC-912-KKN1 Black SECC/ ABS Plastic ATX Mid Tower Computer Cooler Master $75.00 0 KKN1 Case, No Power Supply V3 Black Edition VL80001W2Z Black SECC / Plastic ATX Mid Tower Thermaltake VL80001W2Z $70.00 4 Computer Case VN900A1W2 Commander Series Commander MS-II Black SECC ATX Mid Tower Computer Thermaltake $80.00 1 N Case Zalman Z9 PLUS Z9 Plus Black Steel / Plastic ATX Mid Tower Computer Case $80.00 1 Z11 PLUS Zalman ZALMAN Z11 Plus HF1 Black Steel / Plastic ATX Mid Tower Computer Case $95.00 1 HF1 Manufacturer Model# Retail Stock 2.5in SATA Hard Drive to 3.5in Drive Bay Mounting Kit (Includes 1 x BRACKET25 Combined 7+15 pin SATA plus LP4 Power to SATA Cable Connectors 1x Startech $15.00 7 SAT SATA 7 pin Female Connector Connectors 1x SATA 15 pin Female Connector Connectors 1x LP4 Male Connector) CD-ROM, CD-Burners, DVD-ROM, DVD-Burners and Media The parts listed below are normal stock items. -

HP Integrity Nonstop Operations Guide for H-Series and J-Series Rvus

HP Integrity NonStop Operations Guide for H-Series and J-Series RVUs HP Part Number: 529869-023 Published: February 2014 Edition: J06.03 and subsequent J-series RVUs and H06.13 and subsequent H-series RVUs © Copyright 2014 Hewlett-Packard Development Company, L.P. Legal Notice Confidential computer software. Valid license from HP required for possession, use or copying. Consistent with FAR 12.211 and 12.212, Commercial Computer Software, Computer Software Documentation, and Technical Data for Commercial Items are licensed to the U.S. Government under vendor’s standard commercial license. The information contained herein is subject to change without notice. The only warranties for HP products and services are set forth in the express warranty statements accompanying such products and services. Nothing herein should be construed as constituting an additional warranty. HP shall not be liable for technical or editorial errors or omissions contained herein. Export of the information contained in this publication may require authorization from the U.S. Department of Commerce. Microsoft, Windows, and Windows NT are U.S. registered trademarks of Microsoft Corporation. Intel, Pentium, and Celeron are trademarks or registered trademarks of Intel Corporation or its subsidiaries in the United States and other countries. Java® is a registered trademark of Oracle and/or its affiliates. Motif, OSF/1, Motif, OSF/1, UNIX, X/Open, and the "X" device are registered trademarks, and IT DialTone and The Open Group are trademarks of The Open Group in the U.S. and other countries. Open Software Foundation, OSF, the OSF logo, OSF/1, OSF/Motif, and Motif are trademarks of the Open Software Foundation, Inc. -

January-February 1991

HP Labs: singular! 3 For 2:) y<'ars, HP Lahoratories ha.... (pd HP's long-rangt' rest'arch. page 10 Driving up quality at Ford 10 Ford amI liP team to develop an ele<.'troni<- toolhox for automohiles. Your turn 14 History in a box 15 HP's profl'ssional ar('hives is a trt'aSUfC'-trov(' of information. Open for business: Silicon Valley's new garage 19 A million people a year art' expected to visit a new high-tl'eh {·xhihil. People 22 ,Jim Hanl('Y's inten'sts range from high tN'h to primitiw art. No room for dinosaurs 25 1900 was a da....sie exampll' ofttw constant Ill'ell to adapt to change. Letter from John Young 27 John ('xplains hew,; HP's new organizational structure is taking shape. ExtraMeasure 29 MEASURE Editor AssocIate edrtor Aft D,rector GraphiC des,gner Crrculat.on JoyCoIemon Belly Gerard Annerte Yc10VllZ Thomas J Brown Kathleen Miller Measure IS published SI' t'mes a year lor emplayees ana assoclctes 01 HewleN·Packard Compo<1y Produced by Corporate PublIC RelaIJon\ Employee CommunlcaIJon\ Department Brad Whll'worttl manager Addless correspondence 10 Measure....ew'e"·Pac~ard Companv. WBR PO Box 10301 Palo Alto. Calitornla 9<1303-0890 UY>. (.l15) 857-4146 Report changes ol address 10 yOU' local perSOnnel deportment c Copynghl 1991 by HewlelT Pac~ard Company MoIenal may be reprinted wllh permiSSIon Member. Inlerna1ranal Association of BUSiness Communicators Hewlert·Packard Company IS an International monufacturer 01 measurement ana computaTion products and sy.;lems recognized lOt excellence In quality and support The compony's products and services ore used ,n Industry. -

HP G60-120US Notebook PC Datasheet

HP G60-120US Notebook PC Datasheet The HP Difference* • Enjoy full-screen HDTV content playback with the 16:9 15.6" diagonal widescreen display. • Make an impact with an exceptionally clean mobile design and seperate numeric keypad. • Enjoy the extra durability of HP Imprint finish in highly-polished black and silver. • Get online quickly with integrated high-speed wireless LAN to stay in touch.(10b) • Create personalized, silkscreen-quality DVD and CD labels with LightScribe.(16a) • Chat face-to-face or capture video clips using the HP Webcam(15) and integrated microphone. • Relax with virus protection right out of the box. HP recommends Windows Vista® Home Premium. Key Specifications • AMD Turion™ X2 RM-70 Dual-Core Mobile Processor (3a)(4b) Designed for everyone • Genuine Windows Vista® Home Premium with Service For those who want technology to connect and manage Pack 1 (1)(20a) everyday computing tasks in a stunning design that balances • 15.6" Diagonal High Definition (8) HP Brightview Display performance and mobility, the HP G60 series Notebook PC (1366x768) delivers! Its elegant piano black and silver Imprint finish helps • NVIDIA GeForce 8200M with up to 1407MB Total Available protect your system. Graphics Memory (6) • 3072MB DDR2 System Memory (2 Dimm) HP Pavilion notebook PCs help you work faster, connect in new • 250GB (5400RPM) Hard Drive (SATA) (7) ways and play more. • LightScribe SuperMulti 8X DVD±R/RW with Double Layer Support (6d) (16a) (16d) • Wireless LAN 802.11a/b/g/n WLAN (10a) • Connect with the HP Webcam. Turn your next instant message into a live video chat with the integrated webcam, omni directional microphone and an IM solution. -

Bill Krause | Zero to a Million Ethernet Ports + the Epiphany

Bill Krause | Zero to a Million Ethernet Ports + The Epiphany Derick: So Brandon, I think you'll agree with me that there aren't many people like Bill Krause who can coherently, but also in an entertaining way, tell their biography, right, totally off the cuff. Brandon: Yeah, I totally agree, and it's always awesome to hear unique stories from back in the day. We got to sit down with Bill to talk about his experiences as someone who was really there on the ground floor, bringing whole new categories of technology to market, n this case, first with personal computing, and then with networking. So Bill was there when a computer was a thing that a company had, or maybe a company department head, and Bill helped make it a thing a person has as the first computer salesperson at HP. Look for all I know when I ate lunch at HP in Palo Alto, as an intern in 2008, four decades earlier, Bill was eating at that same picnic table with Bill Hewlett. Derick: "The first person to sell" in, in this category, personal computing. That is, that is kind of crazy to think about, like - how many billions of dollars is that category now. Brandon: Uh, well searching Google here... it looks like the first search hit. It says $688 billion. And it's growing. Derick: So, so just a little bit of money. Brandon: LIttle bit of money. Yeah. And then to be the CEO of a company that led Ethernet from approximately zero to the first million ports in under a decade, two years before their goal.. -

Zerohack Zer0pwn Youranonnews Yevgeniy Anikin Yes Men

Zerohack Zer0Pwn YourAnonNews Yevgeniy Anikin Yes Men YamaTough Xtreme x-Leader xenu xen0nymous www.oem.com.mx www.nytimes.com/pages/world/asia/index.html www.informador.com.mx www.futuregov.asia www.cronica.com.mx www.asiapacificsecuritymagazine.com Worm Wolfy Withdrawal* WillyFoReal Wikileaks IRC 88.80.16.13/9999 IRC Channel WikiLeaks WiiSpellWhy whitekidney Wells Fargo weed WallRoad w0rmware Vulnerability Vladislav Khorokhorin Visa Inc. Virus Virgin Islands "Viewpointe Archive Services, LLC" Versability Verizon Venezuela Vegas Vatican City USB US Trust US Bankcorp Uruguay Uran0n unusedcrayon United Kingdom UnicormCr3w unfittoprint unelected.org UndisclosedAnon Ukraine UGNazi ua_musti_1905 U.S. Bankcorp TYLER Turkey trosec113 Trojan Horse Trojan Trivette TriCk Tribalzer0 Transnistria transaction Traitor traffic court Tradecraft Trade Secrets "Total System Services, Inc." Topiary Top Secret Tom Stracener TibitXimer Thumb Drive Thomson Reuters TheWikiBoat thepeoplescause the_infecti0n The Unknowns The UnderTaker The Syrian electronic army The Jokerhack Thailand ThaCosmo th3j35t3r testeux1 TEST Telecomix TehWongZ Teddy Bigglesworth TeaMp0isoN TeamHav0k Team Ghost Shell Team Digi7al tdl4 taxes TARP tango down Tampa Tammy Shapiro Taiwan Tabu T0x1c t0wN T.A.R.P. Syrian Electronic Army syndiv Symantec Corporation Switzerland Swingers Club SWIFT Sweden Swan SwaggSec Swagg Security "SunGard Data Systems, Inc." Stuxnet Stringer Streamroller Stole* Sterlok SteelAnne st0rm SQLi Spyware Spying Spydevilz Spy Camera Sposed Spook Spoofing Splendide