Cash, Cash Conversion Cycle, Inventory and COVID-19

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

“The Relationship Between Cash Conversion Cycle and Financial Characteristics of Industrial Sectors: an Empirical Study”

“The relationship between cash conversion cycle and financial characteristics of industrial sectors: an empirical study” AUTHORS Faris Nasif Al-Shubiri Nassem Mohammad Aburumman Faris Nasif Al-Shubiri and Nassem Mohammad Aburumman (2013). The ARTICLE INFO relationship between cash conversion cycle and financial characteristics of industrial sectors: an empirical study. Investment Management and Financial Innovations, 10(4) RELEASED ON Monday, 09 December 2013 JOURNAL "Investment Management and Financial Innovations" FOUNDER LLC “Consulting Publishing Company “Business Perspectives” NUMBER OF REFERENCES NUMBER OF FIGURES NUMBER OF TABLES 0 0 0 © The author(s) 2021. This publication is an open access article. businessperspectives.org Investment Management and Financial Innovations, Volume 10, Issue 4, 2013 Faris Nasif Al-Shubiri (Jordan), Nassem Mohammad Aburumman (Jordan) The relationship between cash conversion cycle and financial characteristics of industrial sectors: an empirical study Abstract This study aims to investigate the relationship between cash conversion cycle and financial characteristics. A sample of Jordanian different industrial sector of 11 was selected covering the period 2005-2011 listed on the Amman Stock Exchange (ASE). Cash conversion cycle is an important measure for companies in measuring the operating cycle where the work cycle of raw materials for the purposes of manufacturing and production that ends the existence of a good or service offers customers ready. Hence, the flow of financial resources in firms is very important supply chain and presents the center of attention. The results of this study indicate there is statistically significant and positive relationship between cash conversion cycle and independent variables, such as: debt, market, productivity, liquidity and dividends indicator at different significant level 1% and 5%, and the size indicator is weak relationship with significant level at 10% and there is no significant relationship with profitability indicator and cash conversion cycle. -

Cash Conversion Cycle

Session # 205 5/18/17 from 2:00-3:15 Cash Conversion 250 Commercial Street, STE 3012 Manchester, NH 03101 Cycle (603)573‐9206 Breathing Life into a Stale Dying Process Background FASB describes liquidity as reflecting “an asset’s or liability’s nearness to cash” (Statement of Financial Accounting Concepts No. 5, Recognition and Measurement in Financial Statements of Business Enterprises; PP 24, Footnote13). In accounting and auditing textbooks, the current and quick ratios continue to be the focus of liquidity analysis. Noticeably absent from most accounting and auditing textbooks is an approach to liquidity analysis that incorporates the element of time—the cash conversion cycle (CCC), was introduced in 1980 by Verlyn Richards and Eugene Laughlin in their article “A Cash Conversion Cycle Approach to Liquidity Analysis,” Financial Management, Vol. 9, No.1 (Spring 1980). Consideration of the CCC along with the traditional measures of liquidity should lead to a more thorough analysis of a company’s liquidity position. Static measures of liquidity, such as the current ratio, do not account for the amount of time involved in converting current assets to cash or the amount of time involved in paying current liabilities and…can be easily manipulated. Methodology Let’s discuss the elephant in the room… Static Measures of Liquidity An illustration of Static Measures Company A has $1,000,000 in current assets and $750,000 in current liabilities. The current ratio reveals that the Company A can cover its current liabilities with its current assets 1.33 times [$1,000,000 ÷ $750,000]. If Company A wished to maintain a higher current ratio or if a creditor’s loan covenant requires a higher current ratio, Company A could pay $500,000 of its current liabilities. -

Uncovering Cash and Insights from Working Capital

17 Uncovering cash and insights from working capital Improving a company’s management of working capital can generate cash and improve performance far beyond the finance department. Here’s how. Ryan Davies and Managing a company’s working capital1 isn’t the Working capital can amount to as much as several David Merin sexiest task. It’s often painstakingly technical. months’ worth of revenues, which isn’t trivial. It’s hard to know how well a company is doing, even Improving its management can be a quick way to relative to peers; published financial data are too free up cash. We routinely see companies high level for precise benchmarking. And because generate tens or even hundreds of millions of working capital doesn’t appear on the income dollars of cash impact within 60 to 90 days, statement, it doesn’t directly affect earnings or without increasing sales or cutting costs. And the operating profit—the measures that most rewards for persistence and dedication to commonly influence compensation. Although continuous improvement can be lucrative. The working capital management has long been global aluminum company Alcoa made working a business-school staple, our research shows that capital a priority in 2009 in response to the performance is surprisingly variable, even financial crisis and global economic downturn, and among companies in the same industry (exhibit). it recently celebrated its 17th straight quarter of year-on-year reduction in net working capital. That’s quite a missed opportunity—and it has Over that time, the company has reduced its implications beyond the finance department. -

Cash Conversion Cycle: Which One and Does It Matter?

International Journal of Accounting and Financial Reporting ISSN 2162-3082 2019, Vol. 9, No. 4 Cash Conversion Cycle: Which One and Does It Matter? Xin Tan (Corresponding Author) Silberman College of Business, Fairleigh Dickinson University 1000 River Rd, Teaneck, NJ 07666, United States Tel: 201-692-7283 E-mail: [email protected] Sorin A. Tuluca Silberman College of Business, Fairleigh Dickinson University 285 Madison Avenue, Madison, NJ 07940, United States Received: September 28, 2019 Accepted: October 17, 2019 Published: October 24, 2019 doi:10.5296/ijafr.v9i4.15529 URL: https://doi.org/10.5296/ijafr.v9i4.15529 Abstract In the present study, we attempt to investigate the information validity of an important financial metric, the cash conversion cycle (CCC.) A survey of scholarly papers and textbooks reveals that multiple methods to compute the CCC components are employed. Based on a relatively large dataset for six public companies, we explore two of the different methods and their effect on the resulting CCC value. We find that the means of the time series of the two methods over 20 years have only mild statistically significant differences. However, there are important differences in several annual periods for some of the firms analyzed. Since financial managers and financial analysts use the CCC for decision-making, analysis and valuation purposes, the findings of this research represent a warning that the CCC computations might not yield reliable conclusions, as they are dependent on the input used in the calculations. Keywords: Cash conversion cycle, Information validity, Working capital management 1. Introduction Financial statements can help investors, supply chain partners, and other stakeholders of a company analyze its operating performance and financial health. -

Cash Conversion Cycle Strategies to Avoid Business Failure

Walden University ScholarWorks Walden Dissertations and Doctoral Studies Walden Dissertations and Doctoral Studies Collection 2020 Cash Conversion Cycle Strategies to Avoid Business Failure Brian Savino Walden University Follow this and additional works at: https://scholarworks.waldenu.edu/dissertations Part of the Finance and Financial Management Commons This Dissertation is brought to you for free and open access by the Walden Dissertations and Doctoral Studies Collection at ScholarWorks. It has been accepted for inclusion in Walden Dissertations and Doctoral Studies by an authorized administrator of ScholarWorks. For more information, please contact [email protected]. Walden University College of Management and Technology This is to certify that the doctoral study by Brian J. Savino has been found to be complete and satisfactory in all respects, and that any and all revisions required by the review committee have been made. Review Committee Dr. Chad Sines, Committee Chairperson, Doctor of Business Administration Faculty Dr. Craig Martin, Committee Member, Doctor of Business Administration Faculty Dr. Judith Blando, University Reviewer, Doctor of Business Administration Faculty Chief Academic Officer and Provost Sue Subocz, Ph.D. Walden University 2020 Abstract Cash Conversion Cycle Strategies to Avoid Business Failure by Brian J. Savino MBA, Wright State University, 2010 BS, Wright State University, 2006 Doctoral Study Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Business Administration Walden University August 2020 Abstract At the end of 2018, the leading 2,000 U.S. and European companies had more than $2.5 trillion of cash unnecessarily tied up in working capital. The efficient management of working capital will lead to more cash invested in profitable projects leading to long term stability. -

Analysis of All Payment Types

Optimizing Payments Efficiency, Risk and Incentives May 21, 2018 Agenda • The History – Where Did We Start? • The Future is Now • Why is This Important? • Balancing Your Payment Environment • Payment Types – Pros and Cons • Payment Acceptance Costs • Trends in the Payment Industry • How to Optimize • The Future 2 The Start Spaceship Earth The History – Where Did We Start? The Communication Progression Carving, Painting, Writing Papyrus - Transportable Books – Knowledge Consolidation Immovable Printing Press Cars The Internet Knowledge for the Masses Expanding Reasonable Business 4 Blockchain Technology Information herein is considered proprietary and 5 confidential. The Future Is Now Today’s Technology Focus – Security – Speed – Savings Payment Technology Enhances Profits Abstract or Indirect Profit – Think of opportunity – Improve the customer relationship and experience – Benefit your suppliers business for B2B payments Cost Center vs Opportunity Center 6 Why Is This Important? Your accounts payable environment has transitioned away from ‘how you pay’. Ratios Days Payables = Accounts Payable/COGS x 365 Cash Conversion Cycle = Days Inventory + Days Receivable – Days Payable Thinking Big Picture Cash Turnover = 365/Cash conversion Cycle You are using your working capital more efficiently When? Your suppliers’ terms are no longer your terms, to a certain extent Your payment float is increased Where? Anywhere Virtual Cards Payments via smartphones/tablets Internet Satellites Why? Challenge the status quo Why do you have to pay now? Pay later -

Cash Conversion Cycle (CCC) Compare Across Time Periods And

Dickinson Bransford, CM&AA, Managing Director [email protected]; (415) 294-0002 Cash Conversion Cycle (CCC) = Days Inventory Outstanding (DIO) + Days Sales Outstanding (DSO) – Days Payable Outstanding (DPO) Each component is calculated as both a time period in days and a ratio, expressed as the # of times during the accounting period that a cycle occurs. 365 days is indicated below for a year; substitute as appropriate, e.g. 90 days for a quarter, ensuring that all other figures align with that time period. Inventory Turnover 1. From income statement, find Cost of Goods Sold (COGs) for the total period, e.g. the year or the quarter 2. From balance sheets, calculate the Average Inventory for the period: (Beginning inventory + Ending inventoryi) / 2 3. Inventory Turnover Ratio (ITR) = Total COGS for the period/Average Inventory Days Inventory Outstanding (DIO), also known as Days on Hand = Days in Period, e.g. 365 or 90 / ITR Receivables Turnover 4. From income statement, find total Accounts Receivable, in other words sales made on credit for the period (see footnote) ii 5. From balance sheets, calculate Average Accounts Receivable for period using beginning + ending formula above. 6. Receivables Turnover Ratio (RTR) = Total Accounts Receivable/Average Accounts Receivable Days Sales Outstanding (DSO) = 365 / RTR Payables Turnover 7. “Purchases” is not a typical income statement line item, since it’s reflected in COGs. To derive it, add COGs in step 1. to ending inventory used in step 2., then subtract beginning inventory also used in step 2. 8. From the balance sheets, calculate the Average Accounts Payable for the period as above. -

A Comparison of the Current Ratio and the Cash Conversion Cycle in Evaluating

A Comparison of the Current Ratio and the Cash Conversion Cycle in Evaluating Working Capital Cash Flows By Costa John A Dissertation Submitted in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy in Business Administration California Coast University 2001 1 The Dissertation of Costa John is approved: ________________________________ ________________________________ ________________________________ Committee Chairperson California Coast University 2001 2 Abstract of the Dissertation A Comparison of the Current Ratio and the Cash Conversion Cycle in Evaluating Working Capital Cash Flows By Costa John Doctor of Philosophy in Business Administration California Coast University 2001 The purpose of this study was to compare the effectiveness of the current ratio and the cash conversion cycle in evaluating working capital cash flows from a diagnostic and a predictive aspect. The author analyzed two case studies. Each company was reviewed over a five-year period. For each company the writer calculated the annual current ratio and the cash conversion cycle and examined the trends over the five-year periods under review. Results of these analyses indicated that the cash conversion cycle was more effective than the current ratio in diagnosing the health of each company’s working capital cash flows. The cash conversion cycle also signaled a change in liquidity earlier than the current ratio, suggesting that the former had more effective predictive capabilities than the latter. 3 The central implication of these findings is that the cash conversion cycle might be a more useful diagnostic and predictive tool than the current ratio in liquidity analysis. The research findings were also consistent with improvement or deterioration in each company’s underlying strategic performance as measured by critical changes in its competitive position at the same point in time as the cash conversion cycle trend shifted. -

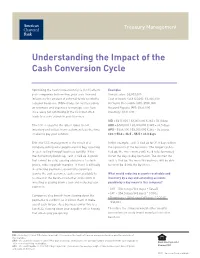

Understanding the Impact of the Cash Conversion Cycle

Treasury Management Understanding the Impact of the Cash Conversion Cycle Optimizing the Cash Conversion Cycle (CCC) affects Example: your companies bottom-line, your cash flow and Annual sales: $5,000,000 influences the amount of external funds needed to Cost of Goods Sold (COGS): $3,000,000 run your business. While many concentrate solely Accounts Receivable (AR): $500,000 on revenues and expenses to manage cash flow, Account Payable (AP): $456,000 it’s usually not optimizing of the CCC that often Inventory: $411,000 leads to a cash crunch in your business. IOD = $411,000 / $3,000,000 X 365 = 50.0 days The CCC is equal to the time it takes to sell ARO = $500,000 / $5,000,000 X 365 = 36.5 days inventory and collect from customers less the time APO = $456,000 / $3,000,000 X 365 = 55.5 days it takes to pay your vendors. CCC = 50.0 + 36.5 – 55.5 = 31.0 days Effective CCC management is the result of a In this example, cash is tied up for 31.0 days within company selling what people want to buy, resulting the operation of the business. The longer cash is in cash cycling through business quickly. If too tied up, the more money will need to be borrowed much inventory builds up, cash is tied up in goods to run the day-to-day operation. The shorter the that cannot be sold, causing a business to slash cash is tied up, the more the business will be able prices, reducing profit margins. -

A Return to the Cash Conversion Cycle and Corporate Returns

Utah State University DigitalCommons@USU All Graduate Plan B and other Reports Graduate Studies 8-2018 A Return to the Cash Conversion Cycle and Corporate Returns Madyson McPherson Utah State University Follow this and additional works at: https://digitalcommons.usu.edu/gradreports Part of the Corporate Finance Commons Recommended Citation McPherson, Madyson, "A Return to the Cash Conversion Cycle and Corporate Returns" (2018). All Graduate Plan B and other Reports. 1266. https://digitalcommons.usu.edu/gradreports/1266 This Report is brought to you for free and open access by the Graduate Studies at DigitalCommons@USU. It has been accepted for inclusion in All Graduate Plan B and other Reports by an authorized administrator of DigitalCommons@USU. For more information, please contact [email protected]. A RETURN TO THE CASH CONVERSION CYCLE AND CORPORATE RETURNS by Madyson McPherson A plan B paper submitted in partial fulfillment of the requirements for the degree of MASTERS OF SCIENCE in Financial Economics Approved: ___________________________ _____________________________ Tyler Brough, PhD Jared DeLisle, PhD Major Professor Committee Member ____________________________ ______________________________ Jason Smith, PhD Mark McLellan, PhD Committee Member Vice President for Research and Dean of the School of Graduate Studies UTAH STATE UNIVERSITY Logan, Utah 2018 ii Copyright © Madyson McPherson 2018 All Rights Reserved iii ABSTRACT A Return to the Cash Conversion Cycle and Corporate Returns By Madyson McPherson, Masters of Science Utah State University 2018 Major Professor: Dr. Tyler Brough Department: Economics and Finance A little over twenty years ago, Jose, Lancaster, and Stevens (1996) wrote a paper examining the relationship between profitability and ongoing liquidity management for firms over a twenty- year period, from 1974 to 1993. -

Cash and Cash Conversion Cycle”, Chapter 17 from the Book Finance for Managers (Index.Html) (V

This is “Cash and Cash Conversion Cycle”, chapter 17 from the book Finance for Managers (index.html) (v. 0.1). This book is licensed under a Creative Commons by-nc-sa 3.0 (http://creativecommons.org/licenses/by-nc-sa/ 3.0/) license. See the license for more details, but that basically means you can share this book as long as you credit the author (but see below), don't make money from it, and do make it available to everyone else under the same terms. This content was accessible as of December 29, 2012, and it was downloaded then by Andy Schmitz (http://lardbucket.org) in an effort to preserve the availability of this book. Normally, the author and publisher would be credited here. However, the publisher has asked for the customary Creative Commons attribution to the original publisher, authors, title, and book URI to be removed. Additionally, per the publisher's request, their name has been removed in some passages. More information is available on this project's attribution page (http://2012books.lardbucket.org/attribution.html?utm_source=header). For more information on the source of this book, or why it is available for free, please see the project's home page (http://2012books.lardbucket.org/). You can browse or download additional books there. i Chapter 17 Cash and Cash Conversion Cycle Cash is King PLEASE NOTE: This book is currently in draft form; material is not final. During the financial crisis of 2008 many of the very wealthy were doing the unthinkable: they were flying commercial! Instead of taking the private jet to Aspen or Monaco, the wealthy were arriving two hours early for flights and going through security (just like us commonfolk). -

Relationship Between Cash Conversion Cycle (CCC) with Firm Size and Profitability

International Journal of Academic Research in Accounting, Finance and Management Sciences Vol. 7, No. 4, October 2017, pp. 296–304 E-ISSN: 2225-8329, P-ISSN: 2308-0337 © 2017 HRMARS www.hrmars.com Relationship between Cash Conversion Cycle (CCC) with Firm Size and Profitability Hassan Subhi AL-ABASS Dean at Hadbaa UnIversity College, E-mail: [email protected] Abstract There are two main areas in which this article focus (1) checking the length of cash conversion cycle with respect to the size of the firms. (2) Examining the length of CCC with respect to the profitability of the firm. For the purpose of research the data is collected from the listed companies of Karachi Stock Exchange (KSE) over the period of 2012-2016. Descriptive statistics of the study shows that all firms of the sample have favorable Cash conversion cycle but Tobacco sector is at number one with the lowest value of Cash conversion cycle. The Pearson correlation and regression analysis is conducted for the empirically testing of the results. The results of the study show that the relationship of Cash conversion cycle with profitability and size is insignificant. It means that the favorable answers of the Cash conversion cycle is not due to the firm size and favorable answer does not has a positive impact on the profitability of the firms. Key words Cash Conversion Cycle (CCC), firm size and profitability http://dx.doi.org/10.6007/IJARAFMS/v7-i4/3692 (DOI: 10.6007/IJARAFMS/v7-i4/3692) 1. Introduction Cash conversion cycle (CCC) is a powerful tool for accessing how well a company managing its working capital.