Updated US List of Foreign Currency Futures Contracts – Starting Point for Section 1256

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Payment Systems in Mauritius

THE PAYMENT SYSTEM IN MAURITIUS Table of Contents OVERVIEW OF THE NATIONAL PAYMENT SYSTEM IN MAURITIUS .......................... 79 1. INSTITUTIONAL ASPECTS .............................................................................................. 80 1.1 General legal aspects ................................................................................................... 80 1.2 Role of financial intermediaries that provide payment services ............................ 80 1.2.1 Domestic banks ................................................................................................ 81 1.2.2 Offshore banks ................................................................................................. 81 1.2.3 Non-bank financial institutions authorised to transact deposit-taking business .................................................................................... 81 1.2.4 Savings banks ................................................................................................... 82 1.2.5 Housing corporation ........................................................................................ 82 1.2.6 Development bank............................................................................................. 82 1.2.7 Foreign exchange dealers ................................................................................ 82 1.2.8 Other financial institutions ............................................................................... 83 1.3 Role of the central bank ............................................................................................ -

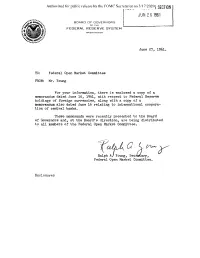

Rec'd Records Section Jun 28 1961

Authorized for public release by the FOMC Secretariat on 3/17/2020 REC'D RECORDS SECTION JUN 28 1961 BOARD OF GOVERNORS OF THE FEDERAL RESERVE SYSTEM WASHINGTON June 27, 1961. TO: Federal Open Market Committee FROM: Mr. Young For your information, there is enclosed a copy of a memorandum dated June 16, 1961, with respect to Federal Reserve holdings of foreign currencies, along with a copy of a memorandum also dated June 16 relating to international coopera- tion of central banks. These memoranda were recently presented to the Board of Governors and, at the Board's direction, are being distributed to all members of the Federal Open Market Committee. Ralph A. Young, Secretary, Federal Open Market Committee. Enclosures Authorized for public release by the FOMC Secretariat on 3/17/2020 REC'D IN RECORDS SECTION JUN 28 1961 June 16, 1961 (Corrected 6/26/61 To: Board of Governors Subject: Federal Reserve holdings of From: Ralph A. Young foreign currencies CONFIDENTIAL (FR) International cooperation between central banks to deal with destabilizing international flows of funds has become not only a subject of active discussion in recent months but also a reality. In March 1961, a number of continental European central banks gave large-scale assistance to the Bank of England to withstand the outflow of funds from the United Kingdom following the German and Netherlands revaluations. The Stabilization Fund of the U. S. Treasury acquired German marks, British pounds, and also Swiss francs in March, April and May 1961, in an effort to help counteract undesirable effects of fund flows resulting from these revaluations. -

Common Core - Core Entities and Services User Guide Oracle Banking Payments Release 14.5.0.0.0

Common Core - Core Entities and Services User Guide Oracle Banking Payments Release 14.5.0.0.0 Part No. F42401-01 May 2021 Common Core - Core Entities and Services User Guide Oracle Financial Services Software Limited Oracle Park Off Western Express Highway Goregaon (East) Mumbai, Maharashtra 400 063 India Worldwide Inquiries: Phone: +91 22 6718 3000 Fax: +91 22 6718 3001 https://www.oracle.com/industries/financial-services/index.html Copyright © 2007, 2021, Oracle and/or its affiliates. All rights reserved. Oracle and Java are registered trademarks of Oracle and/or its affiliates. Other names may be trademarks of their respective owners. U.S. GOVERNMENT END USERS: Oracle programs, including any operating system, integrated software, any programs installed on the hardware, and/or documentation, delivered to U.S. Government end users are “commercial computer software” pursuant to the applicable Federal Acquisition Regulation and agency-specific supplemental regulations. As such, use, duplication, disclosure, modification, and adaptation of the programs, including any operating system, integrated software, any programs installed on the hardware, and/or documentation, shall be subject to license terms and license restrictions applicable to the programs. No other rights are granted to the U.S. Government. This software or hardware is developed for general use in a variety of information management applications. It is not developed or intended for use in any inherently dangerous applications, including applications that may create a risk of personal injury. If you use this software or hardware in dangerous applications, then you shall be responsible to take all appropriate failsafe, backup, redundancy, and other measures to ensure its safe use. -

List of Currencies of All Countries

The CSS Point List Of Currencies Of All Countries Country Currency ISO-4217 A Afghanistan Afghan afghani AFN Albania Albanian lek ALL Algeria Algerian dinar DZD Andorra European euro EUR Angola Angolan kwanza AOA Anguilla East Caribbean dollar XCD Antigua and Barbuda East Caribbean dollar XCD Argentina Argentine peso ARS Armenia Armenian dram AMD Aruba Aruban florin AWG Australia Australian dollar AUD Austria European euro EUR Azerbaijan Azerbaijani manat AZN B Bahamas Bahamian dollar BSD Bahrain Bahraini dinar BHD Bangladesh Bangladeshi taka BDT Barbados Barbadian dollar BBD Belarus Belarusian ruble BYR Belgium European euro EUR Belize Belize dollar BZD Benin West African CFA franc XOF Bhutan Bhutanese ngultrum BTN Bolivia Bolivian boliviano BOB Bosnia-Herzegovina Bosnia and Herzegovina konvertibilna marka BAM Botswana Botswana pula BWP 1 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Brazil Brazilian real BRL Brunei Brunei dollar BND Bulgaria Bulgarian lev BGN Burkina Faso West African CFA franc XOF Burundi Burundi franc BIF C Cambodia Cambodian riel KHR Cameroon Central African CFA franc XAF Canada Canadian dollar CAD Cape Verde Cape Verdean escudo CVE Cayman Islands Cayman Islands dollar KYD Central African Republic Central African CFA franc XAF Chad Central African CFA franc XAF Chile Chilean peso CLP China Chinese renminbi CNY Colombia Colombian peso COP Comoros Comorian franc KMF Congo Central African CFA franc XAF Congo, Democratic Republic Congolese franc CDF Costa Rica Costa Rican colon CRC Côte d'Ivoire West African CFA franc XOF Croatia Croatian kuna HRK Cuba Cuban peso CUC Cyprus European euro EUR Czech Republic Czech koruna CZK D Denmark Danish krone DKK Djibouti Djiboutian franc DJF Dominica East Caribbean dollar XCD 2 www.thecsspoint.com www.facebook.com/thecsspointOfficial The CSS Point Dominican Republic Dominican peso DOP E East Timor uses the U.S. -

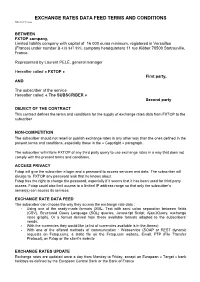

EXCHANGE RATES DATA FEED TERMS and CONDITIONS July 2013 Version

EXCHANGE RATES DATA FEED TERMS AND CONDITIONS July 2013 Version BETWEEN FXTOP company, Limited liability company with capital of 16 000 euros minimum, registered in Versailles (France) under number B 438 847 899, company headquarters 11 rue Kléber 78500 Sartrouville, France. Represented by Laurent PELÉ, general manager Hereafter called « FXTOP » First party, AND The subscriber of the service Hereafter called « The SUBSCRIBER » Second party OBJECT OF THE CONTRACT This contract defines the terms and conditions for the supply of exchange rates data from FXTOP to the subscriber NON-COMPETITION The subscriber should not resell or publish exchange rates in any other way than the ones defined in the present terms and conditions, especially those in the « Copyright » paragraph. The subscriber will inform FXTOP of any third party query to use exchange rates in a way that does not comply with the present terms and conditions. ACCESS PRIVACY Fxtop will give the subscriber a login and a password to access services and data. The subscriber will divulge to FXTOP any password leak that he knows about. Fxtop has the right to change the password, especially if it seems that it has been used for third party access. Fxtop could also limit access to a limited IP address range so that only the subscriber’s server(s) can access its services. EXCHANGE RATE DATA FEED The subscriber can choose the way they access the exchange rate data : - Using one of the ready-made formats (XML, Text with semi colon separation between fields (CSV), Structured Query Language (SQL) queries, Javascript Script, Ajax/JQuery, exchange rates graph). -

List of Currencies Sorted by Iso Currency Code and Country Or Area Name

ANNEX F.II LIST OF CURRENCIES SORTED BY ISO CURRENCY CODE AND COUNTRY OR AREA NAME Currency ISO code Currency name Country name AED UAE Dirham United Arab Emirates AFN Afghani Afghanistan ALL Lek Albania AMD Armeniam Dram Armenia ANG Netherlands Antillian Guilder Curaçao ANG Netherlands Antillian Guilder Sint Maarten AOA Kwanza Angola ARS Argentine Peso Argentina AUD Australian Dollar Australia AUD Australian Dollar Christmas Island AUD Australian Dollar Cocos (Keeling) Islands AUD Australian Dollar Kiribati AUD Australian Dollar Nauru AUD Australian Dollar Tuvalu AWG Aruban Florin Aruba AZN Azerbaijanian Manat Azerbaijan BAM Convertible Mark Bosnia and Herzegovina BBD Barbados Dollar Barbados BDT Taka Bangladesh BGN Bulgarian Lev Bulgaria BHD Bahraini Dinar Bahrain BIF Burundi Franc Burundi BMD Bermudian Dollar Bermuda BND Brunei Dollar Brunei Darussalam BOB Boliviano Bolivia (Plurinat.State) BRL Brazilian Real Brazil BSD Bahamian Dollar Bahamas BTN Ngultrum Bhutan BWP Pula Botswana BYN Belarusian Ruble Belarus BZD Belize Dollar Belize CAD Canadian Dollar Canada CDF Congolese Franc Congo, Dem. Rep. of the CHF Swiss Franc Liechtenstein CHF Swiss Franc Switzerland CLP Chilean Peso Chile CNY Yuan Renminbi China COP Colombian Peso Colombia CRC Costa Rican Colón Costa Rica CUP Cuban Peso Cuba CVE Cabo Verde Escudo Cabo Verde CZK Czech Koruna Czechia DJF Djibouti Franc Djibouti DKK Danish Krone Denmark DKK Danish Krone Faroe Islands DKK Danish Krone Greenland DOP Dominican Peso Dominican Republic DZD Algerian Dinar Algeria EGP Egyptian Pound -

Foreign Currency Exchange Service Instructions and Enrollment Form

Foreign Currency Exchange Service Instructions and Enrollment Form Company Name: Amount Number: Company Number: LT Number: ➊ Payment Instructions Check the box to receive your payment in connection with the transaction associated with the enclosed Letter of Transmittal in a foreign currency (not in U.S. dollars). Note: The Foreign Currency Exchange Service does not apply to any other types of payments (for example, dividends) issued by the above company (the “Company”), any other company, or American Stock Transfer & Trust Company, LLC (“AST”). ➋ Requested Currency for Payment Refer to the Foreign Currency Codes listed on the enclosed “Foreign Currency Exchange Service” section, and enter the three-letter code of your preferred payment. If the currency you selected is not allowed for the country, or if there are any legal restrictions within the country where your bank is located, we will be unable to enroll you for the Foreign Currency Exchange Service. Please contact your local bank with any questions. ➌ Contact Information Clearly print your email address and phone numbers where you can be reached regarding your enrollment. ➍ Indicate if you wish to receive your proceeds in the form of a check (mailed to the address above), or in the form of a wire transfer. ➎ Sign the Authorization and Return this form along with your Letter of Transmittal Print and sign your name exactly as it appears on your account, and exactly as signed on the Letter of Transmittal. If more than one name is listed, all parties must sign. Your signature authorizes the action and agrees to the terms and conditions detailed in the Foreign Currency Exchange Service Agreement Foreign Currency Exchange Service Enrollment Form ➊ Payment Instructions I wish to receive my payment in foreign currency (non-USD). -

This Document Specifies the Dutycalculator Webservice API

This document specifies the DutyCalculator webservice API Version 2.1.4 May 23rd 2013 Follow us on twitter for service updates: @DutyCalculator. Contact us if you have any questions. Base URI The base URI of all resources is http://www.dutycalculator.com/api2.1/{APIkey}/ where {APIkey} is the API key which you can pick up from your account details. For testing purposes, requests can be passed to the sandbox. The base URI of all sandbox requests is http://www.dutycalculator.com/api2.1/sandbox/{APIkey}/. For some requests, the sandbox API functionality is limited. List of supported 'Importing from' and ‘Manufactured in’ countries Returns a list of countries that DutyCalculator accepts as 'importing from' and ‘manufactured in’ parameter. The response includes the country name (in English) and the ISO 31661alpha3 or ISO 31661alpha2 code for the country (http://en.wikipedia.org/wiki/ISO_31661_alpha3 and http://en.wikipedia.org/wiki/ISO_31661_alpha2). Request: GET http://www.dutycalculator.com/api2.1/{APIkey}/supportedcountries/from?display_alpha2_code={0 or 1} Response example: <?xml version="1.0" encoding="UTF8"?> <countries> <country code="AFG">Afghanistan</country> <country code="ALB">Albania</country> <country code="DZA">Algeria</country> <! Repeat for all supported countries > <country code="ZWE">Zimbabwe</country> </countries> Parameter display_alpha2_code is optional, if left out the value of 0 is assumed and ISO 31661alpha3 code is returned in the response. In case value of 1 is passed with the request the code returned is ISO 31661alpha2. -

List of Currencies

List of currencies Incoming Payments Outgoing Payments GBP UK Global (Faster Pay, BACS, UK Banks Only, Real-time CHAPS, SWIFT) on Faster Pay EUR Euro Global (SEPA/SWIFT) Global (SEPA/SWIFT) USD USA Global (SWIFT) Global (SWIFT) CNY China Global (SWIFT) Global (SWIFT) RUB Russia Global (SWIFT), Local Banks Local Banks SGD Singapore Global (SWIFT) Global (SWIFT), Real-time to Local Banks HKD Hong Kong Global (SWIFT) Global (SWIFT) AUD Australia Global (SWIFT) Global (SWIFT) PLN Poland Global (SWIFT) Global (SWIFT) CHF Switzerland Global (SWIFT) Global (SWIFT) AED UAE Global (SWIFT) Global (SWIFT) CAD Canada Global (SWIFT) Global (SWIFT) CZK Czech Republic Global (SWIFT) Global (SWIFT) DKK Denmark Global (SWIFT) Global (SWIFT) HRK Croatia Global (SWIFT) Global (SWIFT) HUF Hungary Global (SWIFT) Global (SWIFT) JPY Japan Global (SWIFT) Global (SWIFT) MXN Mexico Global (SWIFT) Global (SWIFT) NOK Norway Global (SWIFT) Global (SWIFT) NZD New Zealand Global (SWIFT) Global (SWIFT) SAR Saudi Arabia Global (SWIFT) Global (SWIFT) SEK Sweden Global (SWIFT) Global (SWIFT) ZAR South Africa Global (SWIFT) Global (SWIFT) KZT Kazakhstan Global (SWIFT) Global (SWIFT) INR India — Real-time and Local Banks IDR Indonesia — Real-time and Local Banks MYR Malaysia — Local Banks PHP Philippines — Real-time and Local Banks LKR Sri Lanka — Local Banks TRY Turkey — Real-time and Local Banks THB Thailand — Local Banks KRW South Korea — Local Banks 41 Luke Street, London EC2A 4DP +44 2038 079645, [email protected] www.3s.money. -

IPA User Guide for EPIM Workstation

IPA User Guide for EPIM Workstation Mandatory/ Field Description Example Format Length IPA Action Optional Alphanumeric field Dealer’s participant account number 8 digits (triple zero The dealer is required to Dealer Account combined with the designated 00011111EBA + account number) complete this field before Mandatory 11 Number location 00022222CBL followed by the 3 submitting to the IPA. No letters representing action from the IPA. the ICSD location The IPA account numbers are hard-coded and available Alphanumeric field. from a drop-down list. The IPA’s account number combined 8 digits (triple zero Dealer is required to IPA Account 00033333EBA with the designated location Mandatory + account number) 11 complete this field before Number 00044444CBL followed by the 3 submitting the request. IPA letters location can check and change the account number from a drop down list, if required. Select YES if a Common Alphabetic field Code is required or NO if a Common Code Common code request indicator Mandatory with 2 options: N.A. common code is not required. Indicator “Yes” or “No” To create new ISIN requests, keep this field at “Yes” Leave this field blank when Common code assigned to the creating a new ISIN request. Common Code 123456789 Optional Numeric field 9 issue For Update requests, this field is optional. Free format. As the IPA Reference dealer wishes IPA internal reference to be IPA’s reference number Optional 16 Number (Alphanumeric manually filled in field) Numeric field. Issuer’s programme New Programme 0000012345 Normally the IPA to check and correct if identifier/number assigned by IPA Mandatory 5 ID Programme ID has necessary. -

Dividend Currency Election Form NYSE Registered

+ Computershare Trust Company, N.A. PO Box 43078 Providence, RI 02940-3078 www.computershare.com Name Address Holder Account Number __ __ __ __ __ __ __ __ __ __ __ Company Name __________________________________ International Currency and Wire Payment Registration Form To receive payments for this account in a currency other than U.S. Dollars (USD), or to receive a USD wire to a bank outside the U.S. (if allowed by the recipient bank), follow the below steps. For assistance in completing the form correctly, review the Glossary of Terms, Instructions, and Frequently Asked Questions. You may set up payment instructions immediately for your account at the web address appearing above. Step 1: Your Instructions: I wish to set up or change my international currency payment instructions for dividends. All future dividends will be paid in accordance with the payment method and currency choice selected below and a USD processing fee of $ for a check, or $ for an electronic funds transfer, will be deducted from the dividend payment. The payment instructions you provide will remain on file on your account. If your dividend payment is less than the processing fee, your payment will instead be made by check in USD. I wish to set up or change my payment instructions for future sales. I understand at the time of sale I may choose a USD payment. A USD processing fee of $ for an international currency check or $ for an electronic funds transfer (regardless of currency) will be deducted from the sales payment (in addition to any sales fees). Future sales requests made in writing must specify to use these existing instructions or proceeds will be sent by check in USD. -

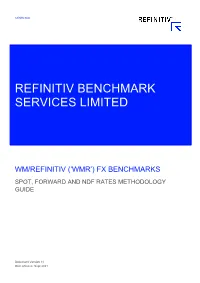

Wm/Refinitiv ('Wmr') Fx Benchmarks

refinitiv.com REFINITIV BENCHMARK SERVICES LIMITED WM/REFINITIV (‘WMR’) FX BENCHMARKS SPOT, FORWARD AND NDF RATES METHODOLOGY GUIDE Document Version 14 Date of issue: Sept 2021 Contents About this document .....................................................................................................................................................4 Benchmark Description .................................................................................................................................................4 Chapter 1 INTRODUCTION .........................................................................................................................................5 1.1 History...........................................................................................................................................................5 1.2 Use of the Rates ...........................................................................................................................................5 1.3 Key Points ....................................................................................................................................................5 Benchmark Administration ........................................................................................................................................5 Expert Judgement .....................................................................................................................................................6 Active Market ............................................................................................................................................................6