Annual Report 2019/2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Horana Plantations Plc Horan a Plant a Tions P L

HORANA PLANTATIONS PLC ANNUAL REPORT 2017/18 HORANA PLANTATIONS P PLANTATIONS HORANA Think L C | New www.horanaplantations.com ANNU A L REPO R T 2017/18 Contents Corporate Information COMPANY NAME REGISTERED OFFICE ADDRESS LEGAL ADVISORS Horana Plantations PLC No.400 Deans Road, Nithi Murugesu & Associates About Horana Plantations 2 Colombo 10. Attorneys-at-Law & Notaries Public Non-Financial Highlights 3 DOMICILE AND LEGAL FORM Telephone : 011 2627000 No.28 (Level 2) W.A.D.Ramanayake Financial Highlights 4 Horana Plantations PLC is a Quoted 011 2627301-7322 Mawatha, Chairman’s Message 6 Public Company with limited liability, Facsimile: 011 2627323 Colombo 2. Managing Director’s Review of Operations 10 Incorporated and domiciled in Sri Lanka, E Mail: [email protected] Board of Directors 16 under the Companies Act No.17 of [email protected] TAX ADVISORS Management Team 18 1982 in terms of the provisions of the Web: www.horanaplantations.com Nanayakkara & Company Sustainability Report 20 Conversion of Public Corporations Chartered Accountants Statement of Corporate Governance 29 of Government Owned Business PARENT COMPANY 3rd Floor, Yathama Building Risk Management 34 Undertakings into Public Companies Act Vallibel Plantation Management Ltd No.142 Galle Road, Annual Report of the Board of Directors No.23 of 1987 and re-registered under No.400 Deans Road, Colombo 3. on the Affairs of the Company 35 the Companies Act No.7 of 2007 Colombo 10. Statement of Directors’ Responsibilities 39 BANKERS Report of the Remuneration Committee 40 DATE OF INCORPORATION ULTIMATE PARENT COMPANY OF THE Commercial Bank of Ceylon PLC Related Party Transactions Review 22nd June 1992 GROUP Hatton National Bank PLC Committee Report 41 Vallibel One PLC People’s Bank Audit Committee Report 43 REGISTRATION NUMBER Level 29, West Tower, Seylan Bank PLC PQ 126 World Trade Centre, Echelon Square, Financial Reports Colombo 1. -

Annual Report 2017

ANNUAL REPORT 2016/17 KELANI VALLEY PLANTATIONS PLC PLANTATIONS VALLEY KELANI | ANNUAL REPORT 2016/17 REPORT ANNUAL | KVPL’S 25 YEARS OF EXCELLENCE | | KVPL’S 25 YEARS OF EXCELLENCE | | KVPL’S 25 YEARS OF EXCELLENCE | | KVPL’S 25 YEARS OF EXCELLENCE | | KVPL’S 25 YEARS OF EXCELLENCE | KELANI VALLEY PLANTATIONS HAS ALWAYS BEEN INTRICATELY CONNECTED TO THE ROOTS AND NATURE THAT MAKES OUR BUSINESS GROW AND FLOURISH. WITH FORTITUDE, COMMITMENT AND TEAMWORK WE PERSEVERED AND WAS ABLE TO LOOK AT WHAT MAKES US WHO WE ARE. LAUDED AND RECOGNISED IN THE YEAR UNDER REVIEW, OUR TEAM RALLIED TOGETHER AND REMAINED STRONG AS WE WORKED TOGETHER TO LAY THE FOUNDATION THAT WOULD SPRINGBOARD US TO BIGGER AND BETTER THINGS IN THE FUTURE. WE JOURNEYED ON, RELENTLESS, AND WITH A PRESTIGIOUS 25 YEARS IN OUR STEAD, WE WILL CONTINUE TO WORK UNCEASINGLY IN BECOMING THE BEST IN THE INDUSTRY. ANNUAL REPORT 2016/17 | KVPL’S 25 YEARS OF EXCELLENCE | 6 Kelani Valley Plantations PLC Annual Report 2016/17 CONTENTS CORPORATE OVERVIEW GOVERNANCE AND RISK Report Profile 7 GRI Content Index 97 Revenue Distribution Local & Global 8 Corporate Governance 101 Our Land 10 Risk Management 122 Our Spread 11 Annual Report of the Board of Directors Corporate Profile 12 on the Affairs of the Company 135 Milestones 14 Board Of Directors 16 FINANCIAL REPORTS Corporate Management Profiles 18 Financial Calender 139 Statement of Directors’ Responsibilities 140 HIGHLIGHTS FOR 2016/17 Audit Committee Report 141 Highlights 20 Related Party Transactions Review Awards & Accolades 22 Committee -

Update UNHCR/CDR Background Paper on Sri Lanka

NATIONS UNIES UNITED NATIONS HAUT COMMISSARIAT HIGH COMMISSIONER POUR LES REFUGIES FOR REFUGEES BACKGROUND PAPER ON REFUGEES AND ASYLUM SEEKERS FROM Sri Lanka UNHCR CENTRE FOR DOCUMENTATION AND RESEARCH GENEVA, JUNE 2001 THIS INFORMATION PAPER WAS PREPARED IN THE COUNTRY RESEARCH AND ANALYSIS UNIT OF UNHCR’S CENTRE FOR DOCUMENTATION AND RESEARCH ON THE BASIS OF PUBLICLY AVAILABLE INFORMATION, ANALYSIS AND COMMENT, IN COLLABORATION WITH THE UNHCR STATISTICAL UNIT. ALL SOURCES ARE CITED. THIS PAPER IS NOT, AND DOES NOT, PURPORT TO BE, FULLY EXHAUSTIVE WITH REGARD TO CONDITIONS IN THE COUNTRY SURVEYED, OR CONCLUSIVE AS TO THE MERITS OF ANY PARTICULAR CLAIM TO REFUGEE STATUS OR ASYLUM. ISSN 1020-8410 Table of Contents LIST OF ACRONYMS.............................................................................................................................. 3 1 INTRODUCTION........................................................................................................................... 4 2 MAJOR POLITICAL DEVELOPMENTS IN SRI LANKA SINCE MARCH 1999................ 7 3 LEGAL CONTEXT...................................................................................................................... 17 3.1 International Legal Context ................................................................................................. 17 3.2 National Legal Context........................................................................................................ 19 4 REVIEW OF THE HUMAN RIGHTS SITUATION............................................................... -

Census Codes of Administrative Units Western Province Sri Lanka

Census Codes of Administrative Units Western Province Sri Lanka Province District DS Division GN Division Name Code Name Code Name Code Name No. Code Western 1 Colombo 1 Colombo 03 Sammanthranapura 005 Western 1 Colombo 1 Colombo 03 Mattakkuliya 010 Western 1 Colombo 1 Colombo 03 Modara 015 Western 1 Colombo 1 Colombo 03 Madampitiya 020 Western 1 Colombo 1 Colombo 03 Mahawatta 025 Western 1 Colombo 1 Colombo 03 Aluthmawatha 030 Western 1 Colombo 1 Colombo 03 Lunupokuna 035 Western 1 Colombo 1 Colombo 03 Bloemendhal 040 Western 1 Colombo 1 Colombo 03 Kotahena East 045 Western 1 Colombo 1 Colombo 03 Kotahena West 050 Western 1 Colombo 1 Colombo 03 Kochchikade North 055 Western 1 Colombo 1 Colombo 03 Jinthupitiya 060 Western 1 Colombo 1 Colombo 03 Masangasweediya 065 Western 1 Colombo 1 Colombo 03 New Bazaar 070 Western 1 Colombo 1 Colombo 03 Grandpass South 075 Western 1 Colombo 1 Colombo 03 Grandpass North 080 Western 1 Colombo 1 Colombo 03 Nawagampura 085 Western 1 Colombo 1 Colombo 03 Maligawatta East 090 Western 1 Colombo 1 Colombo 03 Khettarama 095 Western 1 Colombo 1 Colombo 03 Aluthkade East 100 Western 1 Colombo 1 Colombo 03 Aluthkade West 105 Western 1 Colombo 1 Colombo 03 Kochchikade South 110 Western 1 Colombo 1 Colombo 03 Pettah 115 Western 1 Colombo 1 Colombo 03 Fort 120 Western 1 Colombo 1 Colombo 03 Galle Face 125 Western 1 Colombo 1 Colombo 03 Slave Island 130 Western 1 Colombo 1 Colombo 03 Hunupitiya 135 Western 1 Colombo 1 Colombo 03 Suduwella 140 Western 1 Colombo 1 Colombo 03 Keselwatta 145 Western 1 Colombo 1 Colombo -

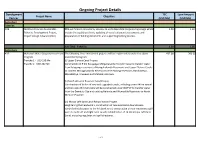

Ongoing Project Details

Ongoing Project Details Development TEC Loan Amount Project Name Objective Partner (USD Mn) (USD Mn) Agriculture Fisheries ADB Northern Province Sustainable PDA will finance consultancy services to undertake detail engineering design which 1.59 1.30 Fisheries Development Project, include the updating of cost, updating of social safeguard assessments and Project Design Advance (PDA) preparation of bidding documents and supporting bidding process. Sub Total - Fisheries 1.59 1.30 Agriculture ADB Mahaweli Water Security Investment The following three investment projects will be implemented under the above 432.00 360.00 Program investment program. Tranche 1 - USD 190 Mn (i) Upper Elahera Canal Project Tranche 2- USD 242 Mn Construction of 9 km Kaluganga-Morgahakanda Transfer Canal to transfer water from Kaluganga reservoir to Moragahakanda Reservoirs and Upper Elehera Canals to connect Moragahakanda Reservoir to the existing reservoirs; Huruluwewa, Manakattiya, Eruwewa and Mahakanadarawa. (ii) North Western Province Canal Project Construction of 96 km of new and upgraded canals, including a new 940 m tunnel and two new 25 m tall dams will be constructed under NWPCP to transfer water from the Dambulu Oya and existing Nalanda and Wemedilla Reservoirs to North Western Province. (iii) Minipe Left Bank Canal Rehabilitation Project Heightening the headwork’s, construction of new automatic downstream- controlled intake gates to the left bank canal; construction of new emergency spill weirs to both left and right bank canals; rehabilitation of 74 km Minipe Left Bank Canal, including regulator and spill structures. 1 of 24 Ongoing Project Details Development TEC Loan Amount Project Name Objective Partner (USD Mn) (USD Mn) IDA Agriculture Sector Modernization Objective is to support increasing Agricultural productivity, improving market 125.00 125.00 Project access and enhancing value addition of small holder farmers and agribusinesses in the project areas. -

Press Release: TEAM up India Ensuring a Sustainable Future for the Indian Tea Industry on 9Th April, the Indian Tea Association

Press Release: TEAM UP India Ensuring a Sustainable Future for the Indian Tea Industry On 9th April, the Indian Tea Association (ITA), the Tea Research Association (TRA), the Ethical Tea Partnership (ETP), and the Sustainable Trade Initiative (IDH) hosted the largest gathering of organisations interested in the future of the Indian tea sector. Indian tea producers and packers, international tea packing companies, and a number of development organisations were present to discuss the critical issues facing the Indian tea sector and ways to address them in order to create a thriving and sustainable tea industry. The Indian tea sector is large, second only to China and over 80% of tea produced is for the local Indian market. Like many places around the world where tea is grown, India faces challenges of prices not keeping pace with increases in costs. There are long standing problems that require a huge amount of change. These problems are exacerbated by the fact that India’s tea industry was largely established over one hundred years ago, leaving it with a set of circumstances and structures which are hard to adapt to twenty-first century requirements. These include changing labour patterns and the need to provide services such as housing and sanitation for continually increasing estate communities. The industry also faces new challenges, particularly relating to climate change. At the meeting, TRA and ETP unveiled the results of climate change impact modelling for Assam which predicted that, over the next 50 years, many areas of current production will become to become less suitable for tea due to changes in temperature and precipitation patterns including increased rainfall during the monsoonal period, reduced rainfall early in the season and increasing temperatures. -

Unilever Sustainable Tea Part II: Reaching out to Smallholders in Kenya and Argentina

Case study Unilever sustainable tea Part II: Reaching out to smallholders in Kenya and Argentina By Dr Tania Moreira Braga, Dr Aileen Ionescu-Somers and Professor Ralf W. Seifert, IMD International Foreword Contents A tipping point happens when a critical mass One of the arenas that is rapidly moving 1.0 Executive summary 4 of people begin to shift their perception of toward a sustainability tipping point and which an issue and take action in a new direction. o ers exemplars of creative partnerships is 2.0 Introduction 8 that of commodity market transformation. As I look across the global landscape, I feel This is the collective e ort by businesses, 3.0 Combining E orts in Kenya 12 that we are approaching a tipping point NGOs, labour unions, and governments to 3.1 Laying the Groundwork with the Farmer Field Schools 13 concerning global sustainability. It is catalyzed restructure the production and distribution 3.2 Combining the Farmer Field Schools with Capacity Building by at least three important realizations by systems of commodities to be more for Certifi cation 15 business, government, and civil society: sustainable, while building broad market 3.3 Certifying Kenyan Smallholders 17 The fi r s t is a realization that the world is demand for sustainable products. If done 3.4 Roll-out Challenges 17 fi nite and that a growing population with well, these improved markets will deliver 3.5 Potential for Replication 18 a higher ambition for living standards will large-scale social and environmental outcomes inevitably lead to a world which will be that advance the millennium development 4.0 Building from Scratch in Argentina 20 resource and carbon constrained. -

ASSETLINE RESEARCH 1 Beta Values Against ASPI

ASSETLINE RESEARCH 1 Beta Values against ASPI Note: Values are calculated considering the market prices of each share from 01 st July 2009 – 30 th June 2014 Share Code Company Name Beta Bank, Finance & Insurance AAF ASIA ASSET FINANCE PLC 0.890 AAIC ASIAN ALLIANCE INSURANCE PLC 1.011 ABL AMANA BANK LIMITED 4.794 ACAP ASIA CAPITAL PLC 0.583 AFSL ABANS FINANCE PLC 1.666 ALLI ALLIANCE FINANCE COMPANY PLC 0.637 AMF ASSOCIATED MOTOR FINANCE COMPANY PLC 1.410 ARPI ARPICO FINANCE COMPANY PLC 0.846 ATL AMANA TAKAFUL PLC 0.954 BLI BIMPUTH FINANCE PLC 0.767 CALF CAPITAL ALLIANCE FINANCE PLC 1.000 CDB CITIZENS DEVELOPMENT BUSINESS FINANCE PLC 0.837 CDIC N D B CAPITAL HOLDINGS PLC 1.241 CFIN CENTRAL FINANCE COMPANY PLC 0.655 CFL CHILAW FINANCE PLC 1.085 CFVF FIRST CAPITAL HOLDINGS PLC 0.761 CIFL CENTRAL INVESTMENTS & FINANCE PLC 0.560 CINS CEYLINCO INSURANCE PLC 1.515 CLC COMMERCIAL LEASING & FINANCE PLC 0.942 COCR COMMERCIAL CREDIT AND FINANCE PLC 0.307 COMB COMMERCIAL BANK OF CEYLON PLC 1.206 CRL SOFTLOGIC FINANCE PLC 0.820 CSF NATION LANKA FINANCE PLC 0.553 CTCE A I A INSURANCE LANKA PLC 1.569 DFCC DFCC BANK 0.902 ESL ENTRUST SECURITIES PLC 0.642 GSF GEORGE STEUART FINANCE PLC 9.977 HASU HNB ASSURANCE PLC 1.200 HDFC THE HOUSING DEVELOPMENT FINANCE 0.566 HNB HATTON NATIONAL BANK PLC 1.142 Disclaimer: This document is purely based on information obtained from sources considered to be reliable. However, please note that we do not make any representations and warranties as to its accuracy, completeness or correctness. -

Water Balance Variability Across Sri Lanka for Assessing Agricultural and Environmental Water Use W.G.M

Agricultural Water Management 58 (2003) 171±192 Water balance variability across Sri Lanka for assessing agricultural and environmental water use W.G.M. Bastiaanssena,*, L. Chandrapalab aInternational Water Management Institute (IWMI), P.O. Box 2075, Colombo, Sri Lanka bDepartment of Meteorology, 383 Bauddaloka Mawatha, Colombo 7, Sri Lanka Abstract This paper describes a new procedure for hydrological data collection and assessment of agricultural and environmental water use using public domain satellite data. The variability of the annual water balance for Sri Lanka is estimated using observed rainfall and remotely sensed actual evaporation rates at a 1 km grid resolution. The Surface Energy Balance Algorithm for Land (SEBAL) has been used to assess the actual evaporation and storage changes in the root zone on a 10- day basis. The water balance was closed with a runoff component and a remainder term. Evaporation and runoff estimates were veri®ed against ground measurements using scintillometry and gauge readings respectively. The annual water balance for each of the 103 river basins of Sri Lanka is presented. The remainder term appeared to be less than 10% of the rainfall, which implies that the water balance is suf®ciently understood for policy and decision making. Access to water balance data is necessary as input into water accounting procedures, which simply describe the water status in hydrological systems (e.g. nation wide, river basin, irrigation scheme). The results show that the irrigation sector uses not more than 7% of the net water in¯ow. The total agricultural water use and the environmental systems usage is 15 and 51%, respectively of the net water in¯ow. -

Corporate Responsibility for Human Rights in Assam Tea Plantations: a Business and Human Rights Approach

sustainability Article Corporate Responsibility for Human Rights in Assam Tea Plantations: A Business and Human Rights Approach Madhura Rao 1 and Nadia Bernaz 2,* 1 Food Claims Centre Venlo, Maastricht University, 5911 BV Venlo, The Netherlands; [email protected] 2 Law Group, Wageningen University, 6708 PB Wageningen, The Netherlands * Correspondence: [email protected] Received: 16 July 2020; Accepted: 7 September 2020; Published: 9 September 2020 Abstract: This paper explores how UK-based companies deal with their responsibility to respect the human rights of Assam (India) tea plantation workers. Through qualitative content analysis of publicly available corporate reports and other documents, it investigates how companies approach and communicate their potential human rights impacts. It highlights the gap between well-documented human rights issues on the ground and corporate reports on these issues. It aims to answer the following research question: in a context where the existence of human rights violations at the end of the supply chain is well-documented, how do companies reconcile their possible connection with those violations and the corporate responsibility to respect human rights under the United Nations Guiding Principles on Business and Human Rights? This paper reveals the weakness of the current corporate social responsibility (CSR) approach from the perspective of rights-holders. It supports a business and human rights approach, one that places the protection of human rights at its core. Keywords: tea plantations; Assam; business and human rights; corporate social responsibility; UN Guiding Principles on Business and Human Rights; UK Modern Slavery Act 1. Introduction This paper explores how UK-based tea companies deal with their responsibility to respect the human rights of Assam tea plantation workers. -

Vallibel Finance PLC | Annual Report 2018/19

STAYING STRONG Vallibel Finance PLC | Annual Report 2018/19 Vision To change the financial landscape of our country; bringing more people in more areas to become stakeholders of a national reawakening. We are driven by relentless passion to seek out people who need help. Mission Our work ethics involve working tirelessly to formulate and offer a financial product spread that understands the pulse of the people. Our search is for excellence in all we do including accountability in financial stewardship and in our responsibility towards customers,stakeholders and our country. Read this report online ^^^]HSSPILSÄUHUJLJVT STAYING STRONG At Vallibel Finance, for over a decade we have delivered excellence through our people and processes to the many stakeholders we serve. And over those years, we have emphasized a spirit of care, innovation, industry expertise and sustainability as key drivers in our story of success. While the year has been a challenging one, we have kept our pace, moving forward against all odds. We are confident in our ability to sustain well into the future – for our strong fundamentals keep us dynamic and vibrant, creating a limitless cycle of value creation that encircles the thousands of lives we impact. Built on a solid foundation and a powerful vision, our promise remains; to stay strong and resilient, as we generate value that’s both equitable and enduring, both now and in the years to come. Vallibel Finance PLC l Annual Report 2018/19 1 STAYING STRONG Incorporated as Rupee Finance in to cater to the diverse needs of the the year 1974, the Company became different members of society across About Vallibel Finance immediately after the Sri Lanka. -

RESETTLEMENT PLAN SRI: Southern Road Connectivity Project

RESETTLEMENT PLAN June 2013 SRI: Southern Road Connectivity Project Kesbewa to Pokunuwita Road (B084) Prepared by Ministry of Public Highways, Government of Sri Lanka for the Asian Development Bank CONTENTS EXECUTIVE SUMMARY ............................................................................................................. i I. PROJECT DESCRIPTION .............................................................................................. 1 II. SCOPE OF LAND ACQUISITION AND RESETTLEMENT ............................................. 5 III. SOCIO ECONOMIC INFORMATION .............................................................................. 9 IV. INFORMATION DISCLOSURE, CONSULTATION AND PARTICIPATION ................... 15 V. GRIEVANCE REDRESS MECHANISMS ...................................................................... 19 VI. LEGAL FRAMEWORK .................................................................................................. 22 VII. ENTITLEMENTS, ASSISTANCE AND BENEFITS ....................................................... 30 VIII. RELOCATION OF HOUSING AND SETTLEMENTS .................................................... 40 IX. INCOME RESTORATION AND REHABILITATION ...................................................... 43 X. RESETTLEMENT BUDGET AND FINANCING PLAN .................................................. 47 XI. INSTITUTIONAL ARRANGEMENTS ............................................................................ 49 XII. IMPLEMENTATION SCHEDULE .................................................................................