Date 21 Oct 2016 Version 0.6 Approved By

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Country Iioijs1 of Greater Mancheste

COUNTRY IIOIJS1 OF GREATER MANCHESTE * P .•» I COUNTRY HOUSES OF GREATER MANCHESTER EDITORS :J.S.F. WALKER & A.S.TINDALL (;itiL\n<it MANCHESTER ARCHAEOLOGICAL UNIT 1985 osi CHAIRMAN'S STATEMENT The country house is part of the diverse and rich heritage of Greater Manchester. This volume follows the development of the country house from the Middle Ages to the present day, using a combination of .archaeological excavation, documentary research and survey to present a coherent study of a building type which reflects the social and economic development of the community in a singularly direct way. By their survival they .demonstrate the entrepreneurial skills of the owner and the abilities of those artisans who built and maintained them. The form and function of the country house change over the centuries, and the fabric of individual buildings mirrors these changes and encapsulates much of the history of the time. Many of our country houses are in good hands, well maintained and with a secure future. Many others described in this volume are already lost, and even the land upon which they stood has been so disturbed as to allow no further site investigation. Their loss, in many cases, was inevitable but I hope that this publication will create an awareness that others, too valuable to be allowed to disappear, are at risk. The protection and refurbishment of old buildings is costly, but I am confident that present conservation policies, allied with improving public and private attitudes towards preservation, have created a strong body of opinion in favour of the constructive re-use of the best of those which survive. -

AUGUST 2020 Stay Safe

AUGUST 2020 St Mary's Church is the oldest parish church in Stockport. It stands in Churchgate overlooking the market place. The church is recorded in the National Heritage List for England as a designated Grade I listed building. Cover photo courtesy of David Pechey Stay Safe - Stay in Touch Photo-montage courtesy of Bramhall U3A Photography Group August was named in honour of the Roman Emperor, Caesar Augustus (27BC to AD14). After Julius Caesar’s grandnephew Augustus defeated Marc Antony and Cleopatra, and became emperor of Rome, the Roman Senate decided that he too should have a month named after him. The month Sextillus (sex = six) was chosen. Not only did the Senate name a month after Augustus, but it decided that since Julius Caesar’s month, July, had 31 days, Augustus's month should equal it, as under the Roman, or Julian calendar, the months alternated evenly between 30 and 31 days (with the exception of February), which made August 30 days long. So, instead of August having a mere 30 days, it was lengthened to 31, preventing anyone from claiming that Emperor Augustus was saddled with an inferior month. Jackie Harmer Eileen Elliott Ann Green Photo Measuring Lockdown Nature carries on. Flowers bloom, grass grows, and the Photo courtesy of Hubert Worrell. slugs and bugs always survive. We've seen and heard more birds this year, everywhere has been so quiet. I have always grown vegetables. Every year is different, our Spring weather is never the same, but it's the busiest time. The greenhouse is now a forest of tomato and pepper plants. -

Bramhall & District Books and Maps, a Short Guide

Bramhall & District Books and Maps, a short guide The following is a selection of books, booklets and maps about Bramhall, Woodford, Hazel Grove & Poynton. (For many years until the local government reorganisation of 1974 Bramhall & Hazel Grove were part of the same Urban District Council.) If you know of others, please send us details. Regrettably, apart from the admirable Alan Godfrey maps, most of them are out of print, but second-hand copies of some can readily be found on websites such as eBay, AbeBooks and Amazon. Books Bramall Hall, by E. Barbara Dean pub. Stockport MBC & the Friends of Bramall Hall, 1999. Bramall Hall, a room-by-room guide to the Hall i) booklet pub. Hazel Grove & Bramhall Urban District Council, undated ii) booklet pub. Stockport MBC, 1981 Bygone Bramhall, by E. Barbara Dean Three editions, 1980, 1990 & 2002, the last published by Stockport MBC 40 page A4 booklet, well worth obtaining. The Diary of Peter Pownall, a Bramhall Farmer, 1765-1858: an Introduction to Local History, by Peter Pownall, edited by Heather Coutie pub. Old Vicarage Publications, 1989 Hazel Grove & Bramhall, compiled by Heather Coutie pub. Chalford 1997, one of the publisher’s Archive Photographs Series The History of Hazel Grove, by D.H. Trowsdale pub. D.H. Trowsdale, 1976 This 100 page A4 booklet seems to have been home-printed and bound. It identified itself as vol.1 of a history of Hazel Grove & Bramhall, so, if vol.2 was ever published, it presumably covered Bramhall. Memories of Bramhall, ed. Mrs. G. Wilsdon A project undertaken by 4th year pupils (Year 6) at Pownall Green Junior School, 1981, and printed for the benefit of them and their parents – reference copies in Bramhall Library, Stockport Local History Library and our own library for members of the Group. -

A Unique Office Space for South Manchester 2 3

1 A UNIQUE OFFICE SPACE FOR SOUTH MANCHESTER 2 3 WELCOME TO EDEN POINT. HIGH QUALITY, CONTEMPORARY OFFICE SPACE TO HELP YOUR BUSINESS THRIVE. 4 5 AN INTRODUCTION TO EDEN POINT Eden Point is a unique office space for South Manchester. The building has undergone a comprehensive refurbishment / remodelling to create contemporary workspaces with personality to meet the needs of the modern business. Every detail has been thought through to create an environment where professional, creative and start-up businesses can thrive. The new spaces are designed to offer opportunities for interactions with informal seating areas, landscaped outdoor spaces and Eat@Eden, our fantastic on site café. 6 7 CONTEMPORARY MEETS INDUSTRIAL. Eden Point has benefited from an extensive refurbishment, from the impressive entrance to all the interior spaces. The workspaces have been stripped back and exposed to give a bright, modern feel. Steel framed glass doors and contemporary high end light fittings have been used throughout. UP TO TO UP 14,000 SQ AVAILABLE FT 8 9 OUTSTANDING FACILITIES Eden Point boasts a wealth of facilities. Our café Eat@Eden has an extensive menu offering fresh food, snacks and drinks, and is a perfect venue for breakfast and lunch. The café booths provide display screens with multiple connections, perfect for informal meetings and presentations. We have also created lounge areas and privacy rooms throughout the building, including our dramatic reception area. To complement our enviable transport links, we have facilities for cyclists with a bike store and showers. We also have extensive parking spaces available for drivers. We know that 9-5 working hours are a thing of the past, and therefore offer secure, 24 hour access to our occupiers. -

CHESHIRE This Table Includes Buildings That Are Now in Greater Manchester

Tree rings dated buildings © VAG 2021 INDEX OF TREE-RING DATED BUILDINGS IN ENGLAND COUNTY LIST approximately in chronological order, revised to VA51 (2020). © Vernacular Architecture Group 2021 These files may be copied for personal use, but should not be published or further distributed without written permission from the Vernacular Architecture Group. Always access these tables via the VAG website. Unauthorised copies released without prior consent on search engines may be out of date and unreliable. Since 2016 a very small number of construction date ranges from historical sources have been added. These entries are entirely in italics. Before using the index you are recommended to read or print the introduction and guidance, which includes a key to the abbreviations used on the tables CHESHIRE This table includes buildings that are now in Greater Manchester. County – Felling date Placename Address VA ref HE ref Description / keywords NGR Historic range Other refs and later Ches 1220 + Chester 73 Watergate 31.114 UoW Re-used beam over cellar. SJ 403662 Street Ches 1263 + Stockport 30a and 31 Market 30.119 Sh Rafters re-used in dormer window. Also see 1553 /4 SJ 897906 Place Ches 1268 + Risley Old Abbey 30.115 Sh (1) Aisled hall, based on excavated evidence and several re-used timbers. Moated. SJ 662935 Farmhouse Demolished. Coupled rafters and collar. Also see 1534-1572. Ches 1308 -33 Stockport Church of St Mary - Most of church 19thC but chancel roof has 23 arch-braced coupled rafter frames with SJ 898905 (GrMan) RDR 24-2011 spandrel struts and scissor-bracing. Ches 1327 + Chester 36 Bridge Street 23.44 Sh Undercroft ceiling SJ 405662 Ches 1351 -76 Knutsford Tabley Old Hall, 51.123 Notm Mainly ex-situ timbers. -

Comedy Club (FP-Feb).Qxp Layout 1 26/01/2015 17:16 Page 1 Contents Feb Region 2.Qxp Layout 1 26/01/2015 18:11 Page 1

Wolves & B'Cntry Cover .qxp_Wolves & B/Country 02/02/2015 15:10 Page 1 WOLVERHAMPTON & BLACK WOLVERHAMPTON COUNTRY ON WHAT’S THE MIDLANDS ULTIMATE ENTERTAINMENT GUIDE WOLVERHAMPTON & BLACK COUNTRY ISSUE 350 ’ Whatwww.whatsonlive.co.uk sOnISSUE 350 FEBRUARY 2015 JO CAULFIELD FEBRUARY FEBRUARY 2015 BRINGS HER UNINFORMED OPINIONS TO THE REGION... JODIE PRENGER having a whip-cracking time as Calamity Jane PART OF MIDLANDS WHAT’S ON MAGAZINE GROUP PUBLICATIONS GROUP MAGAZINE ON WHAT’S MIDLANDS OF PART interview inside... EDWARD SCISSORHANDS Matthew Bourne’s revised production arrives in the Midlands @WHATSONWOLVES WWW.WHATSONLIVE.CO.UK @WHATSONWOLVES NEW ART WEST MIDLANDS showcasing the region’s artistic talent... MON 16 - SAT 21 FEBRUARY Box Office 01902 42 92 12 BOOK ONLINE AT grandtheatre.co.uk Manford Comedy Club (FP-Feb).qxp_Layout 1 26/01/2015 17:16 Page 1 Contents Feb Region 2.qxp_Layout 1 26/01/2015 18:11 Page 1 February 2015 Editor: INSIDE: Davina Evans [email protected] 01743 281708 Editorial Assistants: Curious Incident... Brian O’Faolain Simon Stephens talks [email protected] 01743 281701 about his stage adaptation Lauren Foster interview p6 [email protected] 01743 281707 Adrian Parker [email protected] 01743 281714 Sales & Marketing: Lei Woodhouse [email protected] 01743 281703 Chris Horton [email protected] 01743 281704 Subscriptions: Adrian Parker [email protected] 01743 281714 Managing Director: New Art West Midlands Paul Oliver [email protected] showcasing the region’s 01743 281711 artistic talent... p51 Publisher and CEO: Martin Monahan [email protected] 01743 281710 Graphic Designers: Lisa Wassell Chris Atherton Accounts Administrator Jo Caulfield - comedian talks about bringing her Uninformed Opinions to Julia Perry [email protected] the Midlands. -

All Approved Premises

All Approved Premises Local Authority Name District Name and Telephone Number Name Address Telephone BARKING AND DAGENHAM BARKING AND DAGENHAM 0208 227 3666 EASTBURY MANOR HOUSE EASTBURY SQUARE, BARKING, 1G11 9SN 0208 227 3666 THE CITY PAVILION COLLIER ROW ROAD, COLLIER ROW, ROMFORD, RM5 2BH 020 8924 4000 WOODLANDS WOODLAND HOUSE, RAINHAM ROAD NORTH, DAGENHAM 0208 270 4744 ESSEX, RM10 7ER BARNET BARNET 020 8346 7812 AVENUE HOUSE 17 EAST END ROAD, FINCHLEY, N3 3QP 020 8346 7812 CAVENDISH BANQUETING SUITE THE HYDE, EDGWARE ROAD, COLINDALE, NW9 5AE 0208 205 5012 CLAYTON CROWN HOTEL 142-152 CRICKLEWOOD BROADWAY, CRICKLEWOOD 020 8452 4175 LONDON, NW2 3ED FINCHLEY GOLF CLUB NETHER COURT, FRITH LANE, MILL HILL, NW7 1PU 020 8346 5086 HENDON HALL HOTEL ASHLEY LANE, HENDON, NW4 1HF 0208 203 3341 HENDON TOWN HALL THE BURROUGHS, HENDON, NW4 4BG 020 83592000 PALM HOTEL 64-76 HENDON WAY, LONDON, NW2 2NL 020 8455 5220 THE ADAM AND EVE THE RIDGEWAY, MILL HILL, LONDON, NW7 1RL 020 8959 1553 THE HAVEN BISTRO AND BAR 1363 HIGH ROAD, WHETSTONE, N20 9LN 020 8445 7419 THE MILL HILL COUNTRY CLUB BURTONHOLE LANE, NW7 1AS 02085889651 THE QUADRANGLE MIDDLESEX UNIVERSITY, HENDON CAMPUS, HENDON 020 8359 2000 NW4 4BT BARNSLEY BARNSLEY 01226 309955 ARDSLEY HOUSE HOTEL DONCASTER ROAD, ARDSLEY, BARNSLEY, S71 5EH 01226 309955 BARNSLEY FOOTBALL CLUB GROVE STREET, BARNSLEY, S71 1ET 01226 211 555 BOCCELLI`S 81 GRANGE LANE, BARNSLEY, S71 5QF 01226 891297 BURNTWOOD COURT HOTEL COMMON ROAD, BRIERLEY, BARNSLEY, S72 9ET 01226 711123 CANNON HALL MUSEUM BARKHOUSE LANE, CAWTHORNE, -

Decision Digest Template

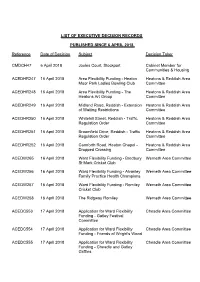

LIST OF EXECUTIVE DECISION RECORDS PUBLISHED SINCE 6 APRIL 2018 Reference Date of Decision Subject Decision Taker CMDCH47 6 April 2018 Joules Court, Stockport Cabinet Member for Communities & Housing ACEDHR247 16 April 2018 Area Flexibility Funding - Heaton Heatons & Reddish Area Moor Park Ladies Bowling Club Committee ACEDHR248 16 April 2018 Area Flexibility Funding - The Heatons & Reddish Area Heatons Art Group Committee ACEDHR249 16 April 2018 Midland Road, Reddish - Extension Heatons & Reddish Area of Waiting Restrictions Committee ACEDHR250 16 April 2018 Whitehill Street, Reddish - Traffic Heatons & Reddish Area Regulation Order Committee ACEDHR251 16 April 2018 Broomfield Drive, Reddish - Traffic Heatons & Reddish Area Regulation Order Committee ACEDHR252 16 April 2018 Carnforth Road, Heaton Chapel - Heatons & Reddish Area Dropped Crossing Committee ACEDW265 16 April 2018 Ward Flexibility Funding - Bredbury Werneth Area Committee St Mark Cricket Club ACEDW256 16 April 2018 Ward Flexibility Funding - Alvanley Werneth Area Committee Family Practice Health Champions ACEDW257 16 April 2018 Ward Flexibility Funding - Romiley Werneth Area Committee Cricket Club ACEDW258 16 April 2018 The Ridgway Romiley Werneth Area Committee ACEDC553 17 April 2018 Application for Ward Flexibility Cheadle Area Committee Funding - Gatley Festival Committee ACEDC554 17 April 2018 Application for Ward Flexibility Cheadle Area Committee Funding - Friends of Wright's Wood ACEDC555 17 April 2018 Application for Ward Flexibility Cheadle Area Committee Funding -

Adult Social Care Portfolio

Date: July 2018 Version 1.0 Approved by KB 1 ECONOMY AND REGENERATION PORTFOLIO OVERVIEW Portfolio Summary It is not long since the Portfolio Agreement was signed off and the extent to which the performance of the Portfolio reflects the plans and targets set out on the Agreement will be clearer in the Autumn. There is still significant progress to report this quarter however. The Get Digital Faster Superfast Broadband programme deployment completed at the end of May 2018. Take-up of service is currently 38.5% in Stockport and will continue to grow. GMCA has accessed £23.9m from the Local Full Fibre Challenge Fund and feasibility work took place this quarter - Stockport has 123 public premises in scope for full fibre. Work arising from the Stockport Work & Skills Commission has included development of the report and Action Plan. This includes proposals for focused support for young people, in particular to improve work placements and information, advice and guidance for young people. A Partnership Board is being set to drive this work. GM Working Well programme progressed well during the quarter with local services being integrated with the programme. A Local Integration Plan and Board has been set up to ensure that the programme matches local need as closely as possible. It has now achieved its first job outcomes in Stockport and referral numbers are increasing each month. Visitor numbers to our Museums and other cultural attractions remain healthy. During the quarter, the Arts Council England granted full museum accreditation status to the Hat Works, Bramall Hall, Air Raid Shelters, Chadkirk Chapel, Staircase House and Stockport Museum. -

Stockport Landscape Character Assessment 2018

Stockport Landscape Character Assessment and Landscape Sensitivity Study Produced for Stockport Metropolitan Borough Council Final Report Prepared by LUC August 2018 Front cover photograph: The edge of Ludworth Moor, looking back towards Greater Manchester Project Title: Stockport Landscape Character Assessment and Landscape Sensitivity Study Client: Stockport Metropolitan Borough Council Version Date Version Details Prepared by Checked by Approved by 1.0 29.3.18 Draft report Sally Marshall Sally Marshall Nick James Maria Grant Chris Cox Jacqueline Whitworth-Allan 2.0 31.5.18 Final report Sally Marshall Sally Marshall Nick James Maria Grant 3.0 14.8.18 Final report Maria Grant Nick James Nick James following Nick James comments Stockport Landscape Character Assessment and Landscape Sensitivity Study Produced for Stockport Metropolitan Borough Council Final Report Prepared by LUC August 2018 Planning & EIA LUC BRISTOL Offices also in: Land Use Consultants Ltd Design 12th Floor Colston Tower Edinburgh Registered in England Registered number: 2549296 Landscape Planning Colston Street Bristol Glasgow Registered Office: Landscape Management BS1 4XE Lancaster 43 Chalton Street Ecology T +44 (0)117 929 1997 London London NW1 1JD GIS & Visualisation [email protected] Manchester FS 566056 EMS 566057 LUC uses 100% recycled paper Contents 1 Executive Summary 1 Background 1 Purpose of the Stockport Landscape Character Assessment 1 How was the Landscape Character Assessment prepared? 1 How is this report structured? 2 2 Introduction and background -

Bramall Hall & Park Conservation Management Plan

DONALD INSALL ASSOCIATES Chartered Architects, Historic Building & Planning Consultants BRAMALL HALL, STOCKPORT Conservation Management Plan September 2010 BRAMALL HALL Conservation Management Plan This page has been left blank intentionally Donald Insall Associates Ltd STBH.03 c.002 Final Version – September 2010 BRAMALL HALL Conservation Management Plan BRAMALL HALL CONSERVATION MANAGEMENT PLAN for STOCKPORT METROPOLITAN BOROUGH COUNCIL Prepared by Donald Insall Associates Ltd. Bridgegate House 5 Bridge Place Chester CH1 1SA Tel. 01244 350063 Fax. 01244 350064 www.insall-architects.co.uk SEPTEMBER 2010 Donald Insall Associates Ltd i STBH.03 c.002 Final Version – September 2010 BRAMALL HALL Conservation Management Plan This page has been left blank intentionally Donald Insall Associates Ltd STBH.03 c.002 Final Version –September 2010 BRAMALL HALL Conservation Management Plan BRAMALL HALL CONSERVATION MANAGEMENT PLAN CONTENTS EXECUTIVE SUMMARY ACKNOWLEDGEMENTS 1.0 INTRODUCTION.....................................................................................................1 1.1 Background to the Plan ...............................................................................................1 1.2 Production of the Plan and Copyright .........................................................................1 1.3 The Site Location, its Setting and Notes on Orientation .............................................2 1.4 General Purpose and Scope of the Plan.......................................................................2 1.5 Structure -

Minutes Template

BRAMHALL & CHEADLE HULME SOUTH AREA COMMITTEE Meeting: 19 April 2018 At: 6.30 pm PRESENT Councillor Lisa Walker (Chair) in the chair; Councillor Mike Hurleston (Vice-Chair); Councillors Brian Bagnall, Stuart Bodsworth, Mark Hunter, John McGahan, Alanna Vine and Suzanne Wyatt. 1. MINUTES The Minutes (copies of which had been circulated) of the meeting held on 8 March 2018 were approved as a correct record and signed by the Chair. 2. DECLARATIONS OF INTEREST Councillors and officers were invited to declare any interest which they had in any of the items on the agenda for the meeting. The following interests were declared:- Personal and Prejudicial Interests Councillor Interest Mark Hunter and Agenda Item 4(vii) – ‘Ward Flexibility Funding – Friends of Bramall Alanna Vine Hall and Park’ as members of the applicant organisation. Councillors Hunter and Vine left the meeting during the consideration of this item and took no part in the discussion or vote. 3. URGENT DECISIONS No urgent decisions were reported. 4. COMMUNITY ENGAGEMENT (i) Chair's Announcements The Chair reported that this would be the last meeting of the Area Committee to be attended by Councillor Stuart Bodsworth who would be retiring from the Council in May 2018 after 15 years of service. The Chair paid tribute to the contribution that Councillor Bodsworth had made to the work of the Area Committee and the wider Borough during his term of office, and wished him well in his future endeavours. Bramhall & Cheadle Hulme South Area Committee - 19 April 2018 (ii) Neighbourhood Policing The Chair reported that representatives of Greater Manchester Police had been unable to attend the meeting on this occasion.