An Investment Analysis Case Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

EDITED TRANSCRIPT Eros STX Global Corporation – Business Update Call

NOVEMBER 04, 2020 / 9:30PM GMT, Eros STX Global Corporation – Business Update Call REFINITIV STREETEVENTS EDITED TRANSCRIPT Eros STX Global Corporation – Business Update Call EVENT DATE/TIME: NOVEMBER 04, 2020 / 9:30PM GMT REFINITIV STREETEVENTS | www.refinitiv.com | Contact Us ©2020 Refinitiv. All rights reserved. Republication or redistribution of Refinitiv content, including by framing or similar means, is prohibited without the prior written consent of Refinitiv. 'Refinitiv' and the Refinitiv logo are registered trademarks of Refinitiv and its affiliated companies. 1 NOVEMBER 04, 2020 / 9:30PM GMT, Eros STX Global Corporation – Business Update Call CORPORATE PARTICIPANTS Adam Fogelson: STX Films - Chairman Andy Warren: Eros STX Global Corporation - CFO Bob Simonds: Eros STX Global Corporation - Co-Chairman & CEO Drew Borst: Eros STX Global Corporation - EVP Investor Relations & Business Development Noah Fogelson: Eros STX Global Corporation - Co-President Rishika Lulla Singh: Eros STX Global Corporation - Co-President & Director CONFERENCE CALL PARTICIPANTS Eric Katz, Wolfe Research, LLC - Research Analyst Robert Routh, FBN Securities, Inc., Research Division - Research Analyst Robert Fishman, MoffettNathanson LLC - Analyst Ted Cronin, Citigroup Inc., Research Division - Research Analyst Tim Nollen, Macquarie Research - Senior Media Analyst PRESENTATION Operator Good afternoon, ladies and gentlemen, and welcome to Eros STX Global Corporation Business Update Call. This call is being broadcast live on the Internet, and a replay of the call will be available on the company's website. The company published earlier certain financial information, including a 20-F transition report and 6-K filing which are available on the company's website. The company would like to remind everyone listening that during this call, it will be making forward- looking statements under the safe harbor provisions of the federal securities laws. -

Annual Report and Financial Statements

Annual Report and Financial Statements for the year ended 31 December 2018 Dimensional Funds ICVC Authorised by the Financial Conduct Authority No marketing notification has been submitted in Germany for the following Funds of Dimensional Funds ICVC: Global Short-Dated Bond Fund International Core Equity Fund International Value Fund United Kingdom Core Equity Fund United Kingdom Small Companies Fund United Kingdom Value Fund Accordingly, these Funds must not be publicly marketed in Germany. Table of Contents Dimensional Funds ICVC General Information* 2 Investment Objectives and Policies* 3 Authorised Corporate Directors’ Investment Report* 6 Incorporation and Share Capital* 10 The Funds 10 Fund Cross-Holdings 10 Authorised Status* 10 Regulatory Disclosure* 10 Potential Implications of Brexit* 10 Responsibilities of the Authorised Corporate Director 11 Responsibilities of the Depositary 11 Report of the Depositary to the Shareholders 11 Directors' Statement 11 Independent Auditors’ Report to the Shareholders of Dimensional Funds ICVC 12 The Annual Report and Financial Statements for each of the below sub-funds (the “Funds”); Emerging Markets Core Equity Fund Global Short-Dated Bond Fund International Core Equity Fund International Value Fund United Kingdom Core Equity Fund United Kingdom Small Companies Fund United Kingdom Value Fund are set out in the following order: Fund Information 14 Portfolio Statement* 31 Statement of Total Return 149 Statement of Change in Net Assets Attributable to Shareholders 149 Balance Sheet 150 Notes to the Financial Statements 151 Distribution Tables 168 Remuneration Disclosures (unaudited)* 177 Supplemental Information (unaudited) 178 * These collectively comprise the Authorised Corporate Directors’ (“ACD”) Report. Dimensional Fund Advisors Ltd. Annual Report and Financial Statements, 31 December 2018 1 Dimensional Funds ICVC General Information Authorised Corporate Director (the “ACD”): Dimensional Fund Advisors Ltd. -

Birth and Evolution of Korean Reality Show Formats

Georgia State University ScholarWorks @ Georgia State University Film, Media & Theatre Dissertations School of Film, Media & Theatre Spring 5-6-2019 Dynamics of a Periphery TV Industry: Birth and Evolution of Korean Reality Show Formats Soo keung Jung [email protected] Follow this and additional works at: https://scholarworks.gsu.edu/fmt_dissertations Recommended Citation Jung, Soo keung, "Dynamics of a Periphery TV Industry: Birth and Evolution of Korean Reality Show Formats." Dissertation, Georgia State University, 2019. https://scholarworks.gsu.edu/fmt_dissertations/7 This Dissertation is brought to you for free and open access by the School of Film, Media & Theatre at ScholarWorks @ Georgia State University. It has been accepted for inclusion in Film, Media & Theatre Dissertations by an authorized administrator of ScholarWorks @ Georgia State University. For more information, please contact [email protected]. DYNAMICS OF A PERIPHERY TV INDUSTRY: BIRTH AND EVOLUTION OF KOREAN REALITY SHOW FORMATS by SOOKEUNG JUNG Under the Direction of Ethan Tussey and Sharon Shahaf, PhD ABSTRACT Television format, a tradable program package, has allowed Korean television the new opportunity to be recognized globally. The booming transnational production of Korean reality formats have transformed the production culture, aesthetics and structure of the local television. This study, using a historical and practical approach to the evolution of the Korean reality formats, examines the dynamic relations between producer, industry and text in the -

Pan Entertainment (068050 KQ) Poised to Benefit from China’S Growing Content Demand

Pan Entertainment (068050 KQ) Poised to benefit from China’s growing content demand Snapshot: Producer of Winter Sonata, the origin of the Korean Wave Founded in 1998, Pan Entertainment was mainly engaged in the business of managing Company Report recording artists and making soundtracks before producing its first drama series “Winter December 5, 2014 Sonata” in 2002. The drama became a huge hit in Japan, setting in motion the “Korean Wave” across the country. Since then, the company has established itself as a drama producer, but has struggled to maintain stable profits due to the small size and buyer- Not Rated driven culture of the domestic market. Catalyst: China’s video content demand is surging, but options are limited Target Price (12M, W) - In China, there are over 4,000 television channels, all of which rely on advertising as their Share Price (12/03/14, W) 6,380 biggest source of income. Because advertising revenue is largely determined by primetime ratings, many broadcasters crave killer content, most preferably in the form Expected Return - of dramas and entertainment shows. But, while China’s video content demand has been rapidly increasing in terms of both quantity and quality, the country’s production capabilities have lagged far behind. Demand has been growing not only among major OP (14F, Wbn) 1 broadcasters and studios, but also among internet portals like Alibaba, and online video Consensus OP (14F, Wbn) 0 streaming sites such as Youku Tudou and Sohu. To make up for the lack of content, EPS Growth (14F, %) - Chinese companies are increasingly turning to Korean pr oducers, as Korean content is 1) Market EPS Growth (14F, %) 1.1 hugely popular in China, 2) of higher quality, and 3) cheaper to produce. -

Clare M. Wilkinson-Weber

Clare M. Wilkinson-Weber TAILORING EXPECTATIONS How film costumes become the audience’s clothes ‘Bollywood’ film costume has inspired clothing trends for many years. Female consumers have managed their relation to film costume through negotiations with their tailor as to how film outfits can be modified. These efforts have coincided with, and reinforced, a semiotic of female film costume where eroticized Indian clothing, and most forms of western clothing set the vamp apart from the heroine. Since the late 1980s, consumer capitalism in India has flourished, as have films that combine the display of material excess with conservative moral values. New film costume designers, well connected to the fashion industry, dress heroines in lavish Indian outfits and western clothes; what had previously symbolized the excessive and immoral expression of modernity has become an acceptable marker of global cosmopolitanism. Material scarcity made earlier excessive costume display difficult to achieve. The altered meaning of women’s costume in film corresponds with the availability of ready-to-wear clothing, and the desire and ability of costume designers to intervene in fashion retailing. Most recently, as the volume and diversity of commoditised clothing increases, designers find that sartorial choices ‘‘on the street’’ can inspire them, as they in turn continue to shape consumer choice. Introduction Film’s ability to stimulate consumption (responding to, and further stimulating certain kinds of commodity production) has been amply explored in the case of Hollywood (Eckert, 1990; Stacey, 1994). That the pleasures associated with film going have influenced consumption in India is also true; the impact of film on various fashion trends is recognized by scholars (Dwyer and Patel, 2002, pp. -

Aspirational Movie List

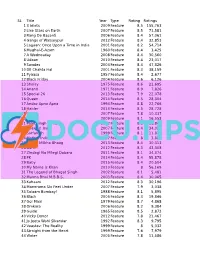

SL Title Year Type Rating Ratings 1 3 Idiots 2009 Feature 8.5 155,763 2 Like Stars on Earth 2007 Feature 8.5 71,581 3 Rang De Basanti 2006 Feature 8.4 57,061 4 Gangs of Wasseypur 2012 Feature 8.4 32,853 5 Lagaan: Once Upon a Time in India 2001 Feature 8.2 54,714 6 Mughal-E-Azam 1960 Feature 8.4 3,425 7 A Wednesday 2008 Feature 8.4 30,560 8 Udaan 2010 Feature 8.4 23,017 9 Swades 2004 Feature 8.4 47,326 10 Dil Chahta Hai 2001 Feature 8.3 38,159 11 Pyaasa 1957 Feature 8.4 2,677 12 Black Friday 2004 Feature 8.6 6,126 13 Sholay 1975 Feature 8.6 21,695 14 Anand 1971 Feature 8.9 7,826 15 Special 26 2013 Feature 7.9 22,078 16 Queen 2014 Feature 8.5 28,304 17 Andaz Apna Apna 1994 Feature 8.8 22,766 18 Haider 2014 Feature 8.5 28,728 19 Guru 2007 Feature 7.8 10,337 20 Dev D 2009 Feature 8.1 16,553 21 Paan Singh Tomar 2012 Feature 8.3 16,849 22 Chakde! India 2007 Feature 8.4 34,024 23 Sarfarosh 1999 Feature 8.1 11,870 24 Mother India 1957 Feature 8 3,882 25 Bhaag Milkha Bhaag 2013 Feature 8.4 30,313 26 Barfi! 2012 Feature 8.3 43,308 27 Zindagi Na Milegi Dobara 2011 Feature 8.1 34,374 28 PK 2014 Feature 8.4 55,878 29 Baby 2015 Feature 8.4 20,504 30 My Name Is Khan 2010 Feature 8 56,169 31 The Legend of Bhagat Singh 2002 Feature 8.1 5,481 32 Munna Bhai M.B.B.S. -

Form 20-F Eros International

SECURITIES AND EXCHANGE COMMISSION WASHINGTON, DC 20549 FORM 20-F ☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ☑ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended March 31, 2019 OR ☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number 001-36176 EROS INTERNATIONAL PLC (Exact name of Registrant as specified in its charter) Not Applicable (Translation of Registrant’s name into English) Isle of Man (Jurisdiction of incorporation or organization) 550 County Avenue Secaucus, New Jersey 07094 Tel: +1(201) 558 9001 (Address of principal executive offices) Oliver Webster IQ EQ (Isle of Man) Limited First Names House Victoria Road Douglas, IM2 4DF Isle of Man Tel: (44) 1624 630 630 Email: [email protected] (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered pursuant to Section 12(b) of the Act. Trading Title of each class Symbol(s) Name of each exchange on which registered A ordinary share, par value GBP 0.30 per share EROS The New York Stock Exchange Securities registered or to be registered pursuant to Section 12(g) of the Act. None (Title of Class) Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act None (Title of Class) Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. -

KPMG FICCI 2013, 2014 and 2015 – TV 16

#shootingforthestars FICCI-KPMG Indian Media and Entertainment Industry Report 2015 kpmg.com/in ficci-frames.com We would like to thank all those who have contributed and shared their valuable domain insights in helping us put this report together. Images Courtesy: 9X Media Pvt.Ltd. Phoebus Media Accel Animation Studios Prime Focus Ltd. Adlabs Imagica Redchillies VFX Anibrain Reliance Mediaworks Ltd. Baweja Movies Shemaroo Bhasinsoft Shobiz Experential Communications Pvt.Ltd. Disney India Showcraft Productions DQ Limited Star India Pvt. Ltd. Eros International Plc. Teamwork-Arts Fox Star Studios Technicolour India Graphiti Multimedia Pvt.Ltd. Turner International India Ltd. Greengold Animation Pvt.Ltd UTV Motion Pictures KidZania Viacom 18 Media Pvt.Ltd. Madmax Wonderla Holidays Maya Digital Studios Yash Raj Films Multiscreen Media Pvt.Ltd. Zee Entertainmnet Enterprises Ltd. National Film Development Corporation of India with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. entity. (“KPMG International”), a Swiss with KPMG International Cooperative © 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated and a member firm of the KPMG network of independent member firms Partnership KPMG, an Indian Registered © 2015 #shootingforthestars FICCI-KPMG Indian Media and Entertainment Industry Report 2015 with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. entity. (“KPMG International”), a Swiss with KPMG International Cooperative © 2015 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated and a member firm of the KPMG network of independent member firms Partnership KPMG, an Indian Registered © 2015 #shootingforthestars: FICCI-KPMG Indian Media and Entertainment Industry Report 2015 Foreword Making India the global entertainment superpower 2014 has been a turning point for the media and entertainment industry in India in many ways. -

Media Content the Next Players of China’S Growth

Media Content The next players of China’s growth A look into the growth pattern of China’s culture industry Overweight (Maintain) China has become a central player in almost every industry across the world. The media content industry is no exception. In our recent overseas marketing trip, we met many Industry Report foreign investors asking about Korean content stocks, and were left with the impression March 23, 2016 that investors were looking for the next players to benefit from China’s growth. In 2015, the tertiary industry contributed to more than half of China’s GDP for the first Daewoo Securities CCCo.,Co., Ltd. time ever, signaling a change in global stock leadership. China’s box-office market has been growing at an astonishing rate, outpacing forecasters’ predictions. Historically, US [Telecom Service / Media] cultural spending increased significantly when the country’s GDP per capita rose from Jee-hyun Moon US$4,000 to US$20,000. At present, China’s GDP per capita is just US$8,000. +822-768-3615 Furthermore, the Chinese government has pledged to develop the culture industry into [email protected] one of the backbones of its economy. Nu-ri Ha With infrastructure nearly complete, next big investment will be in content +822-768-4130 [email protected] China’s culture industry now has most of the necessary infrastructure in place. The boom in multiplex theater co nstruction has led to a considerable rise in the number of Hong-mei Cui screens, and box-office revenue is surging in third- and fourth-tier cities. -

Presentation Title

April 17, 2020 Creating a Global Entertainment Content, Digital Media & OTT Powerhouse Disclaimer This communication contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Exchange Act, and such statements are subject to the safe harbors created thereby. Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “approximately,” “anticipate,” “believe,” “estimate,” “continue,” “could,” “expect,” “future,” “intend,” “may,” “plan,” “potential,” “predict,” “project,” “seek,” “should,” “will” and similar expressions. Those statements include, among other things, the discussions of Eros International’s business strategy and expectations concerning its and the combined company’s market position, future operations, margins, profitability, liquidity and capital resources, tax assessment orders and future capital expenditures. All such forward- looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that Eros International is expecting, including, without limitation: Eros International’s and the combined company’s ability to successfully and cost-effectively source film content; Eros International’s and the combined company’s ability to achieve the desired growth rate of Eros Now, its digital over-the-top (“OTT”) entertainment service; Eros International’s and the combined company’s ability to maintain or raise sufficient capital; -

DFA INVESTMENT DIMENSIONS GROUP INC Form NPORT-EX Filed

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-EX Filing Date: 2019-09-30 | Period of Report: 2019-07-31 SEC Accession No. 0001752724-19-129438 (HTML Version on secdatabase.com) FILER DFA INVESTMENT DIMENSIONS GROUP INC Mailing Address Business Address 6300 BEE CAVE ROAD 6300 BEE CAVE ROAD CIK:355437| IRS No.: 363129984 | State of Incorp.:MD | Fiscal Year End: 1031 BUILDING ONE BUILDING ONE Type: NPORT-EX | Act: 40 | File No.: 811-03258 | Film No.: 191125054 AUSTIN TX 78746 AUSTIN TX 78746 (512) 306-7400 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document SELECTIVELY HEDGED GLOBAL EQUITY PORTFOLIO SCHEDULE OF INVESTMENTS July 31, 2019 (Unaudited) Shares Value† AFFILIATED INVESTMENT COMPANIES — (100.0%) Investment in U.S. Core Equity 2 Portfolio of DFA Investment Dimensions Group Inc. 9,403,760 $211,302,493 Investment in International Core Equity Portfolio of DFA Investment Dimensions Group Inc. 10,310,486 130,840,067 Investment in Emerging Markets Core Equity Portfolio of DFA Investment Dimensions Group Inc. 3,534,273 72,028,480 TOTAL INVESTMENTS IN AFFILIATED INVESTMENT COMPANIES (Cost $342,503,851)^^ $414,171,040 As of July 31, 2019, Selectively Hedged Global Equity Portfolio had entered into the following forward currency contracts and the net unrealized forward currency gain (loss) is reflected in the accompanying financial statements: Unrealized Foreign Exchange Settlement Appreciation Currency Purchased Currency Sold Counterparty Date (Depreciation) USD 18,823,847 GBP 14,866,173 Citibank, N.A. 08/01/19 $ 745,099 USD 3,344,317 SEK 31,085,997 Bank of America Corp. -

![YG Entertainment (122870 KQ) [Summary] Korea’S 2019 Media/Entertainment Competitiveness](https://docslib.b-cdn.net/cover/7182/yg-entertainment-122870-kq-summary-korea-s-2019-media-entertainment-competitiveness-1707182.webp)

YG Entertainment (122870 KQ) [Summary] Korea’S 2019 Media/Entertainment Competitiveness

2019 Outlook Media platform/Content Most favorable environment in history; focus on PR.I.C.E Analyst Jay Park +822-3774-1652 [email protected] Contents [Summary] 3 I. Outlook by segment 4 II. Medium-/long-term outlook 10 III. Key points to watch 12 IV. Global peer group (valuation) , Investment strategy 21 V. Top Picks 23 Studio Dragon (253450 KQ) YG Entertainment (122870 KQ) [Summary] Korea’s 2019 media/entertainment competitiveness Shares to be driven by content sales (p, US$m) (%) Media/content business model focused on direct sales 500 40 FTSE KOREA MEDIA indx (L) Key words: Global platforms, geopolitics, licensing fees, Domestic ad market growth (R, YoY) blockbusters, investments, leverage Broadcast content export growth (R, YoY) 400 30 Media/content business model focused on ads Key words: Domestic market, ad trends, seasonality, politics/sports 300 20 200 10 100 0 OTT export expansion in 2016-18 Chinese market lull 0 OTT export expansion in 2019F + Chinese market recovery -10 04 05 06 07 08 09 10 11 12 13 14 15 16 17 18 19 20 Note: 2017 exports are based on KOCCA’s estimates; 2018 exports based on our estimates Source: Thomson Reuters, KOCCA, Cheil Worldwide, Mirae Asset Daewoo Research 3| 2019 Outlook [Media platform/Content] Mirae Asset Daewoo Research I. Outlook by segment: Media ads Ad market: Mobile and • We expect the domestic ad market to grow 3% YoY (similar to GDP growth) to W11.3tr, amid the absence of large- generalist/cable TV scale sporting events. • We forecast positive growth across all segments (except print ads), with mobile, generalist channels and cable TV channel ads are growing channels likely to drive growth.