What Became of Borders? Some Evolutionary Economic History Of

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Timeline 1994 July Company Incorporated 1995 July Amazon

Timeline 1994 July Company Incorporated 1995 July Amazon.com Sells First Book, “Fluid Concepts & Creative Analogies: Computer Models of the Fundamental Mechanisms of Thought” 1996 July Launches Amazon.com Associates Program 1997 May Announces IPO, Begins Trading on NASDAQ Under “AMZN” September Introduces 1-ClickTM Shopping November Opens Fulfillment Center in New Castle, Delaware 1998 February Launches Amazon.com Advantage Program April Acquires Internet Movie Database June Opens Music Store October Launches First International Sites, Amazon.co.uk (UK) and Amazon.de (Germany) November Opens DVD/Video Store 1999 January Opens Fulfillment Center in Fernley, Nevada March Launches Amazon.com Auctions April Opens Fulfillment Center in Coffeyville, Kansas May Opens Fulfillment Centers in Campbellsville and Lexington, Kentucky June Acquires Alexa Internet July Opens Consumer Electronics, and Toys & Games Stores September Launches zShops October Opens Customer Service Center in Tacoma, Washington Acquires Tool Crib of the North’s Online and Catalog Sales Division November Opens Home Improvement, Software, Video Games and Gift Ideas Stores December Jeff Bezos Named TIME Magazine “Person Of The Year” 2000 January Opens Customer Service Center in Huntington, West Virginia May Opens Kitchen Store August Announces Toys “R” Us Alliance Launches Amazon.fr (France) October Opens Camera & Photo Store November Launches Amazon.co.jp (Japan) Launches Marketplace Introduces First Free Super Saver Shipping Offer (Orders Over $100) 2001 April Announces Borders Group Alliance August Introduces In-Store Pick Up September Announces Target Stores Alliance October Introduces Look Inside The BookTM 2002 June Launches Amazon.ca (Canada) July Launches Amazon Web Services August Lowers Free Super Saver Shipping Threshold to $25 September Opens Office Products Store November Opens Apparel & Accessories Store 2003 April Announces National Basketball Association Alliance June Launches Amazon Services, Inc. -

What Went Wrong with Kmart?

What Went Wrong With Kmart? An Honors Thesis (HONRS 499) by Jacqueline Matyk Thesis Advisor Dr. Mark Myring Ball State University Muncie, Indiana December 2003 Graduation: December 21, 2003 Table of Contents Abstract. ........... ..................................................... 3 Introduction ................................................................................ 4 History ofKnlart .......................................................................... 4 Overview ofKnlart ................................... .................................. 6 Kmart's Problems That Led to Bankruptcy ....... ............... 6 Major Troubles in 2001 .................................................................. 7 2002 and Bankruptcy ..................................................................... 9 Anonymous Letters Lead to Stewardship Review .................................... 9 Emergence from Bankruptcy........................................................... 12 Charles Conaway's Role ................................................................ 14 The Case Against Enio Montini and Joseph Hofmeister ........................... 17 Conclusion.. ............................................................................. 19 Works Cited ............................................................................. 20 2 Abstract This paper provides an in depth look at Krnart Corporation. I will discuss how the company began its operations as a small five and dime store in Michigan and grew into one of the nation's largest retailers. -

The Edge, Spring 2003

Eastern Michigan University DigitalCommons@EMU Alumni News University Archives 2003 The dE ge, Spring 2003 Eastern Michigan University Follow this and additional works at: http://commons.emich.edu/alumni_news Recommended Citation Eastern Michigan University, "The dE ge, Spring 2003" (2003). Alumni News. 200. http://commons.emich.edu/alumni_news/200 This Article is brought to you for free and open access by the University Archives at DigitalCommons@EMU. It has been accepted for inclusion in Alumni News by an authorized administrator of DigitalCommons@EMU. For more information, please contact [email protected]. SPRING2003 A publicatio1 lor alumni and lri1nds ol lastentMichigan Universilv Gettin downt bu sine Talking strateuv11f AdvancementVP Stu INSIDE: • EMU homecomin1upllate • campus dilital maleovers- • New Sludentunion ll'Oiect l:------------------�--=���S_PR_I_G__N 20_ 0 ___3 �------------�--------- I I I I Ci!iMU.MiMay 19 - Faculty Seminar Se- CB·folnt%Mli ries at EMU - Monroe, 1555 S. l:.ve1ygeneration of EMU Raisinville Rd., Monroe, students and alumni has · challenges to deal with. Il ow Mic· h ., 6 :30 - 8 p.m. "N egouat- we handle those challenges ing Win-Win Relationships in l • adi·ngOff helps define us. the Workplace" presented by e With the University now Dr. Sally McCracken. Cost: About our new look facing financial challenges $15. R.S.V.P. to 734.487.0250 due to the state's decision to May 29 - Grand Rapids, Mich., cul several million dollars alumni reception, 6-8 p.m., an d OU r new ffllSSIOD. from its appropriation, it's up Amway Grand Plaza. Cost: • • to us to respond to the needs $10. -

Borders Release

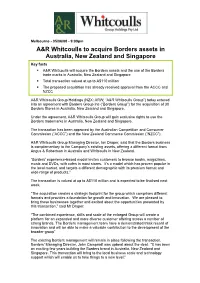

Melbourne - 05/06/08 - 9:00pm A&R Whitcoulls to acquire Borders assets in Australia, New Zealand and Singapore Key facts A&R Whitcoulls will acquire the Borders assets and the use of the Borders trade marks in Australia, New Zealand and Singapore Total transaction valued at up to A$110 million The proposed acquisition has already received approval from the ACCC and NZCC A&R Whitcoulls Group Holdings (NZX: ARW; “A&R Whitcoulls Group”) today entered into an agreement with Borders Group Inc (“Borders Group”) for the acquisition of 30 Borders Stores in Australia, New Zealand and Singapore. Under the agreement, A&R Whitcoulls Group will gain exclusive rights to use the Borders trademarks in Australia, New Zealand and Singapore. The transaction has been approved by the Australian Competition and Consumer Commission (“ACCC”) and the New Zealand Commerce Commission (“NZCC”). A&R Whitcoulls Group Managing Director, Ian Draper, said that the Borders business is complementary to the Company’s existing assets, offering a different format from Angus & Robertson in Australia and Whitcoulls in New Zealand. “Borders’ experience-based model invites customers to browse books, magazines, music and DVDs, with cafes in most stores. It’s a model which has proven popular in the local market, and targets a different demographic with its premium format and wide range of products.” The transaction is valued at up to A$110 million and is expected to be finalised next week. “The acquisition creates a strategic footprint for the group which comprises different formats and provides a foundation for growth and innovation. We are pleased to bring these businesses together and excited about the opportunities presented by this transaction,” said Mr Draper. -

2008 Newsmakers of the Year

20080105-NEWS--0001-NAT-CCI-CD_-- 12/31/2008 5:24 PM Page 1 ® www.crainsdetroit.com Vol. 25, No. 1 JANUARY 5 – 11, 2009 $2 a copy; $59 a year ©Entire contents copyright 2009 by Crain Communications Inc. All rights reserved Inside Michigan banks get Detroit Lions redo business playbook The 2010 Buick LaCrosse sedan is short end of TARP one of three new production vehicles Page 3 GM is expected to unveil at the auto show. Treasury avoiding state, some bankers say Inland Pipe acquires a national presence BY TOM HENDERSON lar Inc. bank got $935 million. (It was announced on NAIAS CRAIN’S DETROIT BUSINESS Dec. 29 that Detroit-based GMAC Financial Services Page 3 L.L.C. would receive $5 billion but that money is not With the deadline for federal approval fast ap- included for this story because GMAC is not a tradi- proaching, a summary of Michi- tional bank.) gan-based banks that have received One other state bank was ap- Local companies scope out greener, funding from the U.S. Treasury as proved for funding but declined $3B defense contract part of the Troubled Asset Relief the offer of $84 million — Mid- Program is short and, from the per- $172 billion land-based Chemical Financial Page 17 spective of local bankers, not so Of TARP funds distributed to Corp. leaner sweet. 208 banks nationwide in the Many national and large re- The Treasury has set a deadline first round gional banks that have branches of Jan. 15 for approving applica- in Michigan have been approved This Just In tions still pending. -

Brave New World

The Booksellers Association of the United Kingdom & Ireland Brave New World Digitisation of Content: the opportunities for booksellers and The Booksellers Association Report to the BA Council from the DOC Working Group Martyn Daniels Member of the BA's Working Group November 2006 1 The Booksellers Association of the United Kingdom & Ireland Limited 272 Vauxhall Bridge Road, London SW1V 1BA United Kingdom Tel: 0044 (0)207 802 0802 e-mail: [email protected] website: http://www.booksellers.org.uk © The Booksellers Association of the United Kingdom & Ireland Limited, 2006 First edition November 2006 All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, without the prior permission of The Booksellers Association. British Library Cataloguing in Publication Data Brave New World Digitisation of Content: the opportunities for booksellers and The Booksellers Association ISBN 978-0-9552233-3-4 This publication was digitally printed by Lightning Source and is available on demand through booksellers. This publication is also digitally available for download to be read by DX Reader, MS Reader, Mobipocket & Adobe eBook reader from www.booksellers.org.uk This digitisation plus the digitisation for Lightning Source has been performed by Value Chain International www.value-chain.biz 2 Members of the DOC Working Group Members of the working group are as follows: Joanne Willetts Entertainment UK (Chairman) -

A Postmortem for Sears - Transcript

A Postmortem for Sears - Transcript Tom Mullooly: In episode 123, we're going to do a postmortem on Sears Roebuck. Stick around. Welcome to the Mullooly Asset show. I'm your host, Tom Mullooly, and this is episode number 123. One, two, three red light. So today, the day that we're recording this, it looks like Sears Roebuck is going to ask the bankruptcy court to enter liquidation, and that's the end of Sears as we know it. So I thought it would be a good time to just kind of take a walk down memory lane. There's a lot of people in the media today who are comparing Amazon to Sears saying, "Hey, Sears was the Amazon of its day." And I just want to share a couple of things that I've learned over the years about Sears. It was started in 1886 as a mail order company. Richard Sears actually sold watches through a catalog that he put together. A year later, in 1887, he hires a guy named Alvah Roebuck to repair watches. So I guess they had problems with some of the watches that they were selling through their catalog. They then added jewelry, and the mail order business really took off. What helped them, a little bit of history for you, is that in the late 1880s, the US government started a program called rural free delivery, or RFD. Some of you are around my age may remember a TV show after Andy Griffith left. It was called Mayberry RFD, and everybody always wanted to know what RFD stood for. -

THE CHAIN of DESTRUCTION F Rom Canada's Ancient Rainfore S T S To

THE CHAIN OF DESTRUCTION Fr om Canada’s Ancient Rainfores t s to the United States Market 1 9 9 9 1436 U Street, NW Washington, DC 20009 © Greenpeace 1999 TABLE OF CONTENTS I. Executive Summary 1 II. State of the World’s Ancient Forests 4 III. The Great Bear Rainforest 7 IV. The Canadian Logging Company 10 V. The U.S. Connection to Canada’s Rainforests 14 1. The Lumber Wholesaler 16 2. The Lumber Processor 18 3. The Builder 19 4. The “Do It Yourself” (DIY) Store 20 5. The Publisher/Printer 22 6. The Paper Products Manufacturer 24 7. The Dissolving Pulp Processor 25 8. The Retailer 26 VI. The Greenpeace Ancient Forests Campaign 27 VII. Alternatives to Ancient Forest Wood 28 VIII. Moving Forward 32 I. EXECUTIVE S U M M A R Y The world’s ancient forests provide us with clean air and water, and places to hike, camp, fish and swim. They are home to the majority of the Earth’s terrestrial species of plants, insects, birds and animals. They regulate weather patterns and help stabilize the Earth’s cli- mate. By storing carbon, ancient forests play a critical role in reducing global warming. Approximately 433 billion tons of carbon — more carbon than will be released from the burning of fossil fuels over the next 69 years — are stored in ancient forests. Ancient forests are home to as many as 200 million indigenous and tribal people worldwide. Protection of the world’s remaining ancient forests requires an immediate end to destructive activities. First and foremost, "Any fool can destroy trees. -

Self-Insured Employer Certificate of Authority Numbers

Self-Insured Employer Certificate of Authority Numbers NV Certificate of Certificate Authority Self-Insured Employer Name Status Number 261 ACCUSTAFF INCORPORATED Inactive 26 AETNA LIFE & CASUALTY Inactive 397 AFFINITY GAMING Active 360 ALADDIN GAMING HOLDINGS LLC Inactive 145 ALLIANCE GAMING CORPORATION Inactive 276 ALUSUISSE-LONZA AMERICA INC Inactive 277 AMERICA WEST HOLDINGS CORPORATION Inactive 146 AMERICAN ASPHALT & GRADING COMPANY Inactive 337 AMERICAN BUILDINGS COMPANY Inactive 279 AMERICAN CASINO & ENTERTAINMENT PROPERTIES LLC Inactive 125420 AMERICAN CASINO AND ENTERTAINMENT PROPERTIES, LLC Active 54 AMERICAN STORES COMPANY Inactive 106 AMERISTAR CASINOS, INC. Inactive 50 AMOCO MINERALS COMPANY Inactive 269 ANDERSON DAIRY INC Inactive 151 ANGLOGOLD USA INC Inactive 231 APL HEALTHCARE GROUP INC Inactive 225 AQUATIC CO. Inactive 31 ARC AMERICA CORPORATION Inactive 102 ARC MATERIALS CORPORATION Inactive 55 ARCHON CORPORATION Inactive 367 ARIZONA CHARLIE'S INC Inactive 45 ARKANSAS BEST CORPORATION Active 297 ARMSTRONG BROS HOLDING CO Inactive 329 ASPLUNDH TREE EXPERT CO Inactive 71 AT & T CORPORATION Inactive 61 ATLANTIC RICHFIELD COMPANY Inactive 353 AUTONATION INC Inactive 32 B F GOODRICH COMPANY THE Inactive 66 BABY GRAND CORPORATION Inactive 100 BAKER HUGHES INCORPORATED Inactive 14 BALLY'S GRAND INC Inactive 234 BANK OF AMERICA CORPORATION Inactive 156 BARBARY COAST HOTEL & CASINO Inactive 149 BARRICK GOLD CORPORATION Inactive 175 BARRICK GOLDSTRIKE MINES INC Inactive 21 BATTLE MOUNTAIN GOLD COMPANY Inactive 20 BBB OPERATING -

Top 10 3PL Excellence Awards 126 3Pls Put on the White Gloves

2018 88 Market Research: 3PL Perspectives 97 Top 100 3PL Providers 115 Readers’ Choice: Top 10 3PL Excellence Awards 126 3PLs Put on the White Gloves July 2018 • Inbound Logistics 87 Inbound Logistics’ 13th annual 3PL market research report examines challenges, trends, and future expectations that are driving shippers and logistics providers to reinvent the way they manage logistics and supply chain operations. By Jason McDowell he current supply chain Shippers are better off investing environment is tumultuous FIGURE 1: How many 3PLs do resources in logistics partnerships. T at best, both domestically and shippers use? Supply chain disruptions may stem globally. Logistics and supply chain Just one 12% from skilled labor shortages, tight professionals may be facing more 60= capacity, fluctuating international trade compounded difficulties in 2018 than More than one 100= 20% relationships, outdated technology, or they’ve ever faced before. Fortunately, It depends 340= 68% some combination of one or more of however, third-party logistics (3PL) these issues. However, it’s when the sup- providers have stepped up to combat ply chain gets turned on its head that these challenges and help shippers to remember that economic booms like logistics providers shine. mitigate the increased risks plaguing the one we’re experiencing now are At times like these, shippers must the supply chain. cyclical. When economic growth even- let their 3PLs do what they do best— On the up side, the U.S. economy tually slows, and capacity opens up leverage relationships and experience is on firm footing and showing signs of again, shippers that make reactionary to address any number of supply chain continuing expansion. -

The 100 Most Significant Events in American Business : an Encyclopedia / Quentin R

THE 100 MOST SIGNIFICANT EVENTS IN AMERICAN BUSINESS An Encyclopedia Quentin R. Skrabec, Jr. (c) 2012 ABC-Clio. All Rights Reserved. The 100 Most Significant Events in American Business (c) 2012 ABC-Clio. All Rights Reserved. THE 100 MOST SIGNIFICANT EVENTS IN AMERICAN BUSINESS An Encyclopedia Quentin R. Skrabec, Jr. (c) 2012 ABC-Clio. All Rights Reserved. Copyright 2012 by ABC-CLIO, LLC All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording, or otherwise, except for the inclusion of brief quotations in a review, without prior permission in writing from the publisher. Library of Congress Cataloging-in-Publication Data Skrabec, Quentin R. The 100 most significant events in American business : an encyclopedia / Quentin R. Skrabec, Jr. p. cm. Includes bibliographical references and index. ISBN 978-0-313-39862-9 (hbk. : alk. paper) — ISBN 978-0-313-39863-6 (ebook) 1. United States—Commerce—History—Encyclopedias. 2. Industries— United States—History—Encyclopedias. 3. Business—History—Encyclopedias. I. Title. II. Title: One hundred most significant events in American business. HF3021.S57 2012 338.097303—dc23 2011050442 ISBN: 978-0-313-39862-9 EISBN: 978-0-313-39863-6 16 15 14 13 12 1 2 3 4 5 This book is also available on the World Wide Web as an eBook. Visit www.abc-clio.com for details. Greenwood An Imprint of ABC-CLIO, LLC ABC-CLIO, LLC 130 Cremona Drive, P.O. Box 1911 Santa Barbara, California 93116-1911 This book is printed on acid-free paper Manufactured in the United States of America (c) 2012 ABC-Clio. -

“Browsing Madness” and Global Sponsors of Literacy: the Politics and Discourse of Deterritorialized Reading Practices and Space in Singapore

. Volume 8, Issue 2 November 2011 “Browsing Madness” and Global Sponsors of Literacy: The Politics and Discourse of Deterritorialized Reading Practices and Space in Singapore Kim Trager Bohley Indiana University-Purdue University, USA Abstract Drawing on empirical data collected from interviews, focus groups, surveys, and participant observation, this article explores the intersections between cultural globalization, transnational booksellers and print cultures in Singapore, placing the changing nature of textual practices and reading audiences within the “micropolitics of local/global interactions.” In doing this, the article considers how and why various sponsors of literacy in Singapore (local, global, corporate, and individual) attempted to propagate their ideologies of reading through affirmation and censure. More specifically, it is a case study of the well- known browsing controversy at Borders Bookstore Singapore, which was debated in The Straits Times, online, and elsewhere for almost a decade. In these forums, Borders employees, newspaper editors and “good patrons” censured “rough book browsers” for dog-earring magazines, clogging book aisles and failing to return magazines where they belong. In this way, practices and discourses surrounding the browsing debacle at Borders became "boundary drawing" activities that divided "good patrons"/"civilized behavior," and "a cosmopolitan mindset" from "bad patrons"/"uncivilized behavior" and "a provincial mindset." By engaging in this "discourse of difference," these social actors began to construct a cosmopolitan identity through negation that positioned them as sponsors of literacy. As with other cultural conflicts, the Borders browsing controversy became a site for the reworking of class and ethnic stereotypes, revealing how everyday media practices such as book browsing are tied to larger socio-economic structures and meta-narratives (e.g., survival = globalization).