Appropriation Accounts 2016-17

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Thiruvallur District

DISTRICT DISASTER MANAGEMENT PLAN FOR 2017 TIRUVALLUR DISTRICT tmt.E.sundaravalli, I.A.S., DISTRICT COLLECTOR TIRUVALLUR DISTRICT TAMIL NADU 2 COLLECTORATE, TIRUVALLUR 3 tiruvallur district 4 DISTRICT DISASTER MANAGEMENT PLAN TIRUVALLUR DISTRICT - 2017 INDEX Sl. DETAILS No PAGE NO. 1 List of abbreviations present in the plan 5-6 2 Introduction 7-13 3 District Profile 14-21 4 Disaster Management Goals (2017-2030) 22-28 Hazard, Risk and Vulnerability analysis with sample maps & link to 5 29-68 all vulnerable maps 6 Institutional Machanism 69-74 7 Preparedness 75-78 Prevention & Mitigation Plan (2015-2030) 8 (What Major & Minor Disaster will be addressed through mitigation 79-108 measures) Response Plan - Including Incident Response System (Covering 9 109-112 Rescue, Evacuation and Relief) 10 Recovery and Reconstruction Plan 113-124 11 Mainstreaming of Disaster Management in Developmental Plans 125-147 12 Community & other Stakeholder participation 148-156 Linkages / Co-oridnation with other agencies for Disaster 13 157-165 Management 14 Budget and Other Financial allocation - Outlays of major schemes 166-169 15 Monitoring and Evaluation 170-198 Risk Communications Strategies (Telecommunication /VHF/ Media 16 199 / CDRRP etc.,) Important contact Numbers and provision for link to detailed 17 200-267 information 18 Dos and Don’ts during all possible Hazards including Heat Wave 268-278 19 Important G.Os 279-320 20 Linkages with IDRN 321 21 Specific issues on various Vulnerable Groups have been addressed 322-324 22 Mock Drill Schedules 325-336 -

Shankar Ias Academy Test 18 - Geography - Full Test - Answer Key

SHANKAR IAS ACADEMY TEST 18 - GEOGRAPHY - FULL TEST - ANSWER KEY 1. Ans (a) Explanation: Soil found in Tropical deciduous forest rich in nutrients. 2. Ans (b) Explanation: Sea breeze is caused due to the heating of land and it occurs in the day time 3. Ans (c) Explanation: • Days are hot, and during the hot season, noon temperatures of over 100°F. are quite frequent. When night falls the clear sky which promotes intense heating during the day also causes rapid radiation in the night. Temperatures drop to well below 50°F. and night frosts are not uncommon at this time of the year. This extreme diurnal range of temperature is another characteristic feature of the Sudan type of climate. • The savanna, particularly in Africa, is the home of wild animals. It is known as the ‘big game country. • The leaf and grass-eating animals include the zebra, antelope, giraffe, deer, gazelle, elephant and okapi. • Many are well camouflaged species and their presence amongst the tall greenish-brown grass cannot be easily detected. The giraffe with such a long neck can locate its enemies a great distance away, while the elephant is so huge and strong that few animals will venture to come near it. It is well equipped will tusks and trunk for defence. • The carnivorous animals like the lion, tiger, leopard, hyaena, panther, jaguar, jackal, lynx and puma have powerful jaws and teeth for attacking other animals. 4. Ans (b) Explanation: Rivers of Tamilnadu • The Thamirabarani River (Porunai) is a perennial river that originates from the famous Agastyarkoodam peak of Pothigai hills of the Western Ghats, above Papanasam in the Ambasamudram taluk. -

03/2020N , District : PS: FIR No.: Date: C Orruption Y Ear» 2020

FIRST INFORMATION REPORT TAMIL NADU POLICE (ipga) ajasojo) ^pjliena INTEGRATED INVESTIGATION FORM-1 (Under Section 154 Cr.P.C.) 8064809 (g.jS.ail.Q^ir.Jliflci) 154 ££) Tirunelveli Vigilance and Anti c l o 03/2020n , District : PS: FIR No.: Date: C orruption Y ear» 2020 ............ 31.07.2020 LMQJL.L.LD airojffljflflicoiuii) (jp-£.<3l- CTorr jsuar (i) Act ffLLli): IRC Sections iJliflajstfr: 120 (B), 34, 167, 109 (ii) Act ffLLli): Prevention of Corruption Act 1988 Sections iJliflfi{&err: 13 (2) r/w 7,13(1) (d) (i) (ii) (iii) (iii) Act Sections Jliflojacri: (iv) Other Acts & Sections Jk) ffULisiffi^m, iM o ja 0 ii) (a) Occurrence of Offence Day : Date from : Date to : @{b<D njlatpoj pjtrar p m (tp^cb 21.08.201,^ oiotj 06.10.2017 Time Period : Time from : Time to : GrBCr cSjaraj Cjjijid (jp^ra Srjurio 010)7 (b) Information Received at PS. Date : 3 1.07.2020 Tjme . 14.00 hrs airaia) nflsncoujsssflji)® ^aojsi) sfl6mi_£(5 jpor G^ijii) (c) General Diary Reference : Entry No(s) Time Quirgi j5irL@pJ1uLflo) uafloj aflaiijii ctm Gjbijlo Type of Information : Written/ O ral: ^aaiafleir aicns : er(Lg£§| (jptoiA / euiruj Qiflrryf)iuir«» W ritten Place of Occurrence (a) Direction and Distance from PS: @j)jD nflatpafLir) (*§|) «ir«ia)^1a)touj^aJl®i5g| erojaiaraj g|irij(y>ii), sr£«[knjujii) Tirunelveli District Milk Producers Beat Number: (b) Address : Co-Op Union, (Aavin) Tirunelveli. (tpempja airairi) erm 5 Km South (c) In case outside limit of this Police Station, then the Name of P.S : District: ^aanoicb njlencouj srcbaitoaauuiTa) jBUBgj @0 «@iDniiJldt, ^piflantuiiJlfl) sip jb air.np.Quiuir miraiilLib Complainant /Informant (a) Name : (b) Father's/ Husband's Name gppOprapiiilLffarit/^aoiai ^jB^oiit Gluiufr ^ M C C L A R IN E E S K H C fl® 01^ 1 Sfl,T®1'r Tr.THOMAS ELLIOT (c) Date / Year of Birlh : (d) Nationality : (e) Passport No. -

Chapter 4.1.9 Ground Water Resources Dindugal District

CHAPTER 4.1.9 GROUND WATER RESOURCES DINDUGAL DISTRICT 1 INDEX CHAPTER PAGE NO. INTRODUCTION 3 DINDUGAL DISTRICT – ADMINISTRATIVE SETUP 3 1. HYDROGEOLOGY 3-7 2. GROUND WATER REGIME MONITORING 8-15 3. DYNAMIC GROUND WATER RESOURCES 15-24 4. GROUND WATER QUALITY ISSUES 24-25 5. GROUND WATER ISSUES AND CHALLENGES 25-26 6. GROUND WATER MANAGEMENT AND REGULATION 26-32 7. TOOLS AND METHODS 32-33 8. PERFORMANCE INDICATORS 33-36 9. REFORMS UNDERTAKEN/ BEING UNDERTAKEN / PROPOSED IF ANY 10. ROAD MAPS OF ACTIVITIES/TASKS PROPOSED FOR BETTER GOVERNANCE WITH TIMELINES AND AGENCIES RESPONSIBLE FOR EACH ACTIVITY 2 GROUND WATER REPORT OF DINDUGAL DISTRICT INRODUCTION : In Tamil Nadu, the surface water resources are fully utilized by various stake holders. The demand of water is increasing day by day. So, groundwater resources play a vital role for additional demand by farmers and Industries and domestic usage leads to rapid development of groundwater. About 63% of available groundwater resources are now being used. However, the development is not uniform all over the State, and in certain districts of Tamil Nadu, intensive groundwater development had led to declining water levels, increasing trend of Over Exploited and Critical Firkas, saline water intrusion, etc. ADMINISTRATIVE SET UP The total geographical area of the Dindigul distict is6, 26,664 hectares, which is about 4.82 percent of the total geographical area of Tamil Nadu state.Thedistrict, is well connected by roads and railway lines with other towns within and outside Tamil Nadu.This district comprising 359 villages has been divided into 7 Taluks, 14 Blocks and 40 Firkas. -

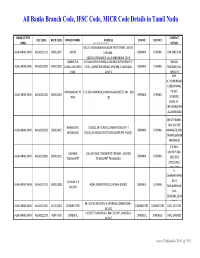

Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu

All Banks Branch Code, IFSC Code, MICR Code Details in Tamil Nadu NAME OF THE CONTACT IFSC CODE MICR CODE BRANCH NAME ADDRESS CENTRE DISTRICT BANK www.Padasalai.Net DETAILS NO.19, PADMANABHA NAGAR FIRST STREET, ADYAR, ALLAHABAD BANK ALLA0211103 600010007 ADYAR CHENNAI - CHENNAI CHENNAI 044 24917036 600020,[email protected] AMBATTUR VIJAYALAKSHMIPURAM, 4A MURUGAPPA READY ST. BALRAJ, ALLAHABAD BANK ALLA0211909 600010012 VIJAYALAKSHMIPU EXTN., AMBATTUR VENKATAPURAM, TAMILNADU CHENNAI CHENNAI SHANKAR,044- RAM 600053 28546272 SHRI. N.CHANDRAMO ULEESWARAN, ANNANAGAR,CHE E-4, 3RD MAIN ROAD,ANNANAGAR (WEST),PIN - 600 PH NO : ALLAHABAD BANK ALLA0211042 600010004 CHENNAI CHENNAI NNAI 102 26263882, EMAIL ID : CHEANNA@CHE .ALLAHABADBA NK.CO.IN MR.ATHIRAMIL AKU K (CHIEF BANGALORE 1540/22,39 E-CROSS,22 MAIN ROAD,4TH T ALLAHABAD BANK ALLA0211819 560010005 CHENNAI CHENNAI MANAGER), MR. JAYANAGAR BLOCK,JAYANAGAR DIST-BANGLAORE,PIN- 560041 SWAINE(SENIOR MANAGER) C N RAVI, CHENNAI 144 GA ROAD,TONDIARPET CHENNAI - 600 081 MURTHY,044- ALLAHABAD BANK ALLA0211881 600010011 CHENNAI CHENNAI TONDIARPET TONDIARPET TAMILNADU 28522093 /28513081 / 28411083 S. SWAMINATHAN CHENNAI V P ,DR. K. ALLAHABAD BANK ALLA0211291 600010008 40/41,MOUNT ROAD,CHENNAI-600002 CHENNAI CHENNAI COLONY TAMINARASAN, 044- 28585641,2854 9262 98, MECRICAR ROAD, R.S.PURAM, COIMBATORE - ALLAHABAD BANK ALLA0210384 641010002 COIIMBATORE COIMBATORE COIMBOTORE 0422 2472333 641002 H1/H2 57 MAIN ROAD, RM COLONY , DINDIGUL- ALLAHABAD BANK ALLA0212319 NON MICR DINDIGUL DINDIGUL DINDIGUL -

Minutes of 162 Meeting of Expert Appraisal Committee for Projects Related to Infrastructure Development, Coastal Regulation Zone

Minutes of 162nd meeting of Expert Appraisal Committee for projects related to Infrastructure Development, Coastal Regulation Zone, Building/Construction, Industrial Estate and Miscellaneous projects held on 29 - 30 August, 2016 Day 1: Monday, 29th August, 2016 1. Opening remarks of the Chairman. 2. Confirmation of the minutes of the 161st Meeting of the EAC held on 28 – 29 July, 2016 at New Delhi. The EAC, having taken note that no comments were offered on the minutes of its 160th meeting held on 28th – 29th June, 2016 at New Delhi, confirmed the same. 3. Consideration of Proposals 3.1 Construction of 2-lane Bridge over Middle Strait Creek (at km 107) of NH-223 connecting South Andaman Island & Baratang Island by Andaman Public Work Department – Further consideration for CRZ Clearance – [F. No. 10- 38/2015- IA.III] 3.1.1 The project was earlier considered by the EAC in its 156th meeting held on 28-29 January, 2016 wherein the EAC noted that no CRZ map was submitted by the project proponent, which was the basic requirement to arrive at the HTL/LTL vis-à- vis the project site, for considering the proposal under the Island Protection Zone Notification, 2011. That time, the proposal was deferred. 3.1.2 During the present meeting, the project proponent made a presentation and provided the following information to the Committee:- (i) The project involves construction of 2-lane Bridge over Middle Strait Creek (at km 107) of NH-223 connecting South Andaman Island & Baratang Island in the Andaman & Nicobar Islands. (ii) Total length of the project is 1963 m out of which 960 m is bridge length & 1003 m (580 m + 423 m) is the approach road on both sides. -

List of Cosmetics Manufacturers Sl

List of Cosmetics Manufacturers Sl. No Name and Address Lic No Date Validity 1 TSR & Co Madras, No. 102, Mount C14 21.03.2007 20.03.2022 Poonamalle High Road, Ramapuram, Chennai-89. 2 Aravind Laboratories, No. 3/17, Valluvar C23 14.03.2008 13.03.2023 Salai, Ramapuram, Chennai-89 3 Kesavardhini products, Plot No. 1 to 4, C39 02.01.1987 31.12.2022 Chowdry Nagar, 16, Arcot road, Chennai- 87. 4 Veto company, 20/23, Erukkancherry High C72 01.04.2008 31.03.2018 Road, Vyarsarpadi, Chennai-39. 5 Vijaya Chemical and Toilet Works (circar), C162 15.11.1982 31.12.2016 No. 11/New No. 97/3, South phase, Industrial Estate, Ambattur, Chennai-58. 6 Vijaya Chemicals and Toilet Works C163 01.04.2006 31.03.2026 (Telungana), 7/4, 7/7, Panchali Amman Koil Street, Arumbakkam, Chennai-600106. 7 Vijaya Chemicals and ToiletWork (AP) C164 07.07.1999 31.12.2022 Arumbakkam, Chennai-106. 8 Aravind Cottage Industry, 126/3, Chairman C175 10.07.1985 31.12.2021 Meyyappa Chettiar Road, Karaikudi-630001 9 Ahamed company, No. 7A, Umar Pulavar C185 23.05.1997 31.12.2022 Street, Melapalayam, Thirunelveli dt. 10 VA Samy Chemicals Works, New No 156, C222 01.06.1998 31.12.2016 Old No 67, New Market East Street, Karaikudi, Sivaganga Dt 11 Standard Pencils Pvt. Ltd, Super A6, C399 09.03.1984 31.12.2021 Industrial Estate, Guindy, Chennai-32. 12 Pethanna perfumers 101, Thulasiram C456 08.01.2003 07.01.2023 Street, Meenakshi Nagar, Villapuram, Madurai - 625012 13 Springton pharma, Ramasamiapuram, C489 01.01.1990 31.12.2021 Sankarankoil 14 Indian dental works, No. -

Public Works Department Irrigation

PUBLIC WORKS DEPARTMENT IRRIGATION Demand No - 40 N.T.P. SUPPLIED BY THE DEPARTMENT PRINTED AT GOVERNMENT CENTRAL PRESS, CHENNAI - 600 079. POLICY NOTE 2015 - 2016 O. PANNEERSELVAM MINISTER FOR FINANCE AND PUBLIC WORKS © Government of Tamil Nadu 2015 INDEX Sl. No. Subject Page 3.4. Dam Rehabilitation and 41 Sl. No. Subject Page Improvement Project 1.0. 1 (DRIP) 1.1.Introduction 1 4.0. Achievements on 45 Irrigation Infrastructure 1.2. 2 During Last Four Years 1.3. Surface Water Potential 4 4.1. Inter-Linking of Rivers in 54 1.4. Ground Water Potential 5 the State 1.5. Organisation 5 4.2. Artificial Recharge 63 Arrangement Structures 2.0. Historic Achievements 24 4.3. New Anicuts and 72 3.0. Memorable 27 Regulators Achievements 4.4. Formation of New Tanks 74 3.1. Schemes inaugurated by 27 / Ponds the Hon’ble Chief 4.5. Formation of New 76 Minister through video Canals / Supply conferencing on Channels 08.06.2015 4.6. Formation of New Check 81 3.2. Tamil Nadu Water 31 dams / Bed dams / Resources Consolidation Grade walls Project (TNWRCP) 4.7. Rehabilitation of Anicuts 104 3.3. Irrigated Agriculture 40 4.8. Rehabilitation of 113 Modernisation and Regulators Water-bodies Restoration and 4.9. Rehabilitation of canals 119 Management and supply channels (IAMWARM) Project Sl. No. Subject Page Sl. No. Subject Page 4.10. Renovation of Tanks 131 5.0. Road Map for Vision 200 4.11. Flood Protection Works 144 2023 4.12. Coastal Protection 153 5.1. Vision Document for 201 Works Tamil Nadu 2023 4.13. -

Irrigation Projects of Tamil Nadu from 2001-2021

IRRIGATION PROJECTS OF TAMIL NADU FROM 2001-2021 NAME – VRINDA GUPTA INSTITUTION – K.R. MANGALAM UNIVERSITY 1 ABSTRACT From the ancient times water is always most important for agriculture purpose for growing crops. Since thousand years, humans have relied on agriculture to feed their communities and they have needed irrigation to water their crops. Irrigation includes artificially applying water to the land to enhance the growing of crops. Over the years, irrigation has come in many different forms in countries all over the world. Irrigation projects involves hydraulic structures which collect, convey and deliver water to those areas on which crops are grown. Irrigation projects unit may starts from a small farm unit to those serving extensive areas of millions of hectares. Irrigation projects consist of two types first a small irrigation project and second a large irrigation project. Small irrigation project includes a low diversion or an inexpensive pumping plant along with small channels and some minor control structures. Large irrigation project includes a huge dam, a large storage reservoir, hundreds kilometers of canals, branches and distributaries, control structures and other works. In this paper we discussing about irrigation plan of Tamil Nadu from 2001-2021. INTRODUCTION Water is the important or elixir of life, a precious gift of nature to humans and millions of other species living on the earth. It is hard to find in most part of the world. 4% of India’s land area in Tamil Nadu and inhabited by 6% of India’s population but water resources in India is only 2.5%. In Tamil Nadu, water is a serious limiting factor for agriculture growth which leads to irrigation reduces risk in farming, increases crop productivity, provides higher employment opportunities to the rural areas and increases farmer income. -

Groundwater Quality Assessment in Dindigul District, Tamil Nadu Using GIS

Nature Environment and Pollution Technology ISSN: 0972-6268 Vol. 13 No. 1 pp. 49-56 2014 An International Quarterly Scientific Journal Original Research Paper Groundwater Quality Assessment in Dindigul District, Tamil Nadu Using GIS J. Colins Johnny and M. C. Sashikkumar* Department of Civil Engineering, Anna University, Tirunelveli Region, Tirunelveli, T.N., India *Department of Civil Engineering, University VOC College of Engineering, Anna University, Thoothukudi Campus, Tuticorin, T. N., India ABSTRACT Nat. Env. & Poll. Tech. Website: www.neptjournal.com Groundwater is a significant source of water in many parts of India, especially in semiarid and arid regions. Received: 10-6-2013 About 50% of the total irrigated area is dependent on groundwater. Groundwater is the major source of Accepted: 13-8-2013 drinking water in both urban and rural areas. Also, it is an important source of water for the agricultural and the industrial sectors. Groundwater quality is as important as the quantity. Poor quality of water adversely Key Words: affects the plant growth and human health. Hence, the demarcation of groundwater quality is of vital importance Groundwater to augment groundwater resources. The present study attempts to prepare the spatial variation map of the Spatial variation various groundwater quality parameters for Dindigul district, Tamil Nadu using Geographical Information Water quality System (GIS). GIS has been applied to visualize the spatial distribution of groundwater quality in the study Geographical information area. The major water quality parameters such as pH, total dissolved solids, total hardness, calcium, system (GIS) magnesium, fluoride, chloride and sulphates etc. were analysed. The final integrated map shows three Dindigul district priority classes such as high, moderate and poor groundwater quality zones of the study area and provides a guideline for the suitability of groundwater for drinking purposes. -

District Census Handbook

Census of India 2011 TAMIL NADU PART XII-B SERIES-34 DISTRICT CENSUS HANDBOOK SIVAGANGA VILLAGE AND TOWN WISE PRIMARY CENSUS ABSTRACT (PCA) DIRECTORATE OF CENSUS OPERATIONS TAMIL NADU CENSUS OF INDIA 2011 TAMIL NADU SERIES-34 PART XII - B DISTRICT CENSUS HANDBOOK SIVAGANGA VILLAGE AND TOWN WISE PRIMARY CENSUS ABSTRACT (PCA) Directorate of Census Operations TAMIL NADU MOTIF SIVAGANGA PALACE Sivaganga palace in Sivaganga Town was built near the Teppakulam has its historical importance. It is a beautiful palace, once the residence of the Zamindar of Sivaganga. The palace was occupied by the ex-rulers, one of the biggest and oldest, wherein Chinna Marudhu Pandiyar gave asylum to Veerapandiya Katta Bomman of Panchalankurichi when the British was trying to hang him as he was fighting against the colonial rule. There i s a temple for Sri Raja Rajeswari, inside the palace. CONTENTS Pages 1 Foreword 1 2 Preface 3 3 Acknowledgement 5 4 History and Scope of the District Census Handbook 7 5 Brief History of the District 9 6 Administrative Setup 10 7 District Highlights - 2011 Census 11 8 Important Statistics 12 9 Section - I Primary Census Abstract (PCA) (i) Brief note on Primary Census Abstract 16 (ii) District Primary Census Abstract 21 Appendix to District Primary Census Abstract Total, Scheduled Castes and (iii) 35 Scheduled Tribes Population - Urban Block wise (iv) Primary Census Abstract for Scheduled Castes (SC) 55 (v) Primary Census Abstract for Scheduled Tribes (ST) 63 (vi) Rural PCA-C.D. blocks wise Village Primary Census Abstract 71 (vii) Urban PCA-Town wise Primary Census Abstract 163 Tables based on Households Amenities and Assets (Rural 10 Section –II /Urban) at District and Sub-District level. -

A Local Response to Water Scarcity Dug Well Recharging in Saurashtra, Gujarat

RETHINKING THE MOSAIC RETHINKINGRETHINKING THETHE MOSAICMOSAIC Investigations into Local Water Management Themes from Collaborative Research n Institute of Development Studies, Jaipur n Institute for Social and Environmental Transition, Boulder n Madras Institute of Development Studies, Chennai n Nepal Water Conservation Foundation, Kathmandu n Vikram Sarabhai Centre for Development Interaction, Ahmedabad Edited by Marcus Moench, Elisabeth Caspari and Ajaya Dixit Contributing Authors Paul Appasamy, Sashikant Chopde, Ajaya Dixit, Dipak Gyawali, S. Janakarajan, M. Dinesh Kumar, R. M. Mathur, Marcus Moench, Anjal Prakash, M. S. Rathore, Velayutham Saravanan and Srinivas Mudrakartha RETHINKING THE MOSAIC Investigations into Local Water Management Themes from Collaborative Research n Institute of Development Studies, Jaipur n Institute for Social and Environmental Transition, Boulder n Madras Institute of Development Studies, Chennai n Nepal Water Conservation Foundation, Kathmandu n Vikram Sarabhai Centre for Development Interaction, Ahmedabad Edited by Marcus Moench, Elisabeth Caspari and Ajaya Dixit 1999 1 © Copyright, 1999 Institute of Development Studies (IDS) Institute for Social and Environmental Transition (ISET) Madras Institute of Development Studies (MIDS) Nepal Water Conservation Foundation (NWCF) Vikram Sarabhai Centre for Development Interaction (VIKSAT) No part of this publication may be reproduced nor copied in any form without written permission. Supported by International Development Research Centre (IDRC) Ottawa, Canada and The Ford Foundation, New Delhi, India First Edition: 1000 December, 1999. Price Nepal and India Rs 1000 Foreign US$ 30 Other SAARC countries US$ 25. (Postage charges additional) Published by: Nepal Water Conservation Foundation, Kathmandu, and the Institute for Social and Environmental Transition, Boulder, Colorado, U.S.A. DESIGN AND TYPESETTING GraphicFORMAT, PO Box 38, Naxal, Nepal.