國立交通大學 管理科學研究所 碩士論文 Operating Strategy Groups In

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

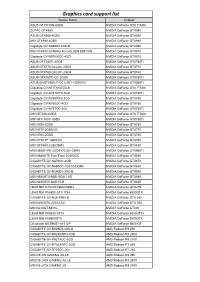

Graphics Card Support List

Graphics card support list Device Name Chipset ASUS GTXTITAN-6GD5 NVIDIA GeForce GTX TITAN ZOTAC GTX980 NVIDIA GeForce GTX980 ASUS GTX980-4GD5 NVIDIA GeForce GTX980 MSI GTX980-4GD5 NVIDIA GeForce GTX980 Gigabyte GV-N980D5-4GD-B NVIDIA GeForce GTX980 MSI GTX970 GAMING 4G GOLDEN EDITION NVIDIA GeForce GTX970 Gigabyte GV-N970IXOC-4GD NVIDIA GeForce GTX970 ASUS GTX780TI-3GD5 NVIDIA GeForce GTX780Ti ASUS GTX770-DC2OC-2GD5 NVIDIA GeForce GTX770 ASUS GTX760-DC2OC-2GD5 NVIDIA GeForce GTX760 ASUS GTX750TI-OC-2GD5 NVIDIA GeForce GTX750Ti ASUS ENGTX560-Ti-DCII/2D1-1GD5/1G NVIDIA GeForce GTX560Ti Gigabyte GV-NTITAN-6GD-B NVIDIA GeForce GTX TITAN Gigabyte GV-N78TWF3-3GD NVIDIA GeForce GTX780Ti Gigabyte GV-N780WF3-3GD NVIDIA GeForce GTX780 Gigabyte GV-N760OC-4GD NVIDIA GeForce GTX760 Gigabyte GV-N75TOC-2GI NVIDIA GeForce GTX750Ti MSI NTITAN-6GD5 NVIDIA GeForce GTX TITAN MSI GTX 780Ti 3GD5 NVIDIA GeForce GTX780Ti MSI N780-3GD5 NVIDIA GeForce GTX780 MSI N770-2GD5/OC NVIDIA GeForce GTX770 MSI N760-2GD5 NVIDIA GeForce GTX760 MSI N750 TF 1GD5/OC NVIDIA GeForce GTX750 MSI GTX680-2GB/DDR5 NVIDIA GeForce GTX680 MSI N660Ti-PE-2GD5-OC/2G-DDR5 NVIDIA GeForce GTX660Ti MSI N680GTX Twin Frozr 2GD5/OC NVIDIA GeForce GTX680 GIGABYTE GV-N670OC-2GD NVIDIA GeForce GTX670 GIGABYTE GV-N650OC-1GI/1G-DDR5 NVIDIA GeForce GTX650 GIGABYTE GV-N590D5-3GD-B NVIDIA GeForce GTX590 MSI N580GTX-M2D15D5/1.5G NVIDIA GeForce GTX580 MSI N465GTX-M2D1G-B NVIDIA GeForce GTX465 LEADTEK GTX275/896M-DDR3 NVIDIA GeForce GTX275 LEADTEK PX8800 GTX TDH NVIDIA GeForce 8800GTX GIGABYTE GV-N26-896H-B -

K8N Neo3 Series MS-7135 (V1.X) ATX Mainboard

K8N Neo3 Series MS-7135 (v1.X) ATX Mainboard English Version G52-M7135X4 i 7135v1.2-Preface.P65 1 2005/2/4, 上午 11:37 Manual Rev: 1.2 Release Date: Feb. 2005 FCC-B Radio Frequency Interference Statement This equipment has been tested and found to comply with the limits for a class B digital device, pursuant to part 15 of the FCC rules. These limits are designed to provide reasonable protection against harmful interference when the equipment is operated in a commercial environment. This equipment generates, uses and can radiate radio frequency energy and, if not installed and used in accordance with the instruction manual, may cause harmful interference to radio communications. Opera- tion of this equipment in a residential area is likely to cause harmful interference, in which case the user will be required to correct the interference at his own expense. Notice 1 The changes or modifications not expressly approved by the party responsible for compliance could void the user’s authority to operate the equipment. Notice 2 Shielded interface cables and A.C. power cord, if any, must be used in order to comply with the emission limits. VOIR LA NOTICE D’INSTALLATION AVANT DE RACCORDER AU RESEAU. Micro-Star International MS-7135 This device complies with Part 15 of the FCC Rules. Operation is subject to the following two conditions: (1) this device may not cause harmful interference, and (2) this device must accept any interference received, including interference that may cause undesired operation. ii 7135v1.2-Preface.P65 2 2005/2/4, 上午 11:37 Copyright Notice The material in this document is the intellectual property of MICRO-STAR INTERNATIONAL. -

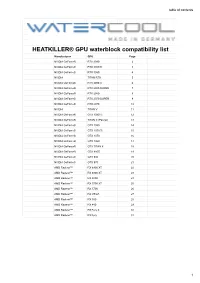

HEATKILLER® GPU Waterblock Compatibility List

table of contents HEATKILLER® GPU waterblock compatibility list Manufacturer GPU Page NVIDIA GeForce® RTX 3090 2 NVIDIA GeForce® RTX 3080 Ti 3 NVIDIA GeForce® RTX 3080 4 NVIDIA TITAN RTX 5 NVIDIA GeForce® RTX 2080Ti 6 NVIDIA GeForce® RTX 2080 SUPER 7 NVIDIA GeForce® RTX 2080 8 NVIDIA GeForce® RTX 2070 SUPER 9 NVIDIA GeForce® RTX 2070 10 NVIDIA TITAN V 11 NVIDIA GeForce® GTX 1080 Ti 12 NVIDIA GeForce® TITAN X (Pascal) 13 NVIDIA GeForce® GTX 1080 14 NVIDIA GeForce® GTX 1070 Ti 15 NVIDIA GeForce® GTX 1070 16 NVIDIA GeForce® GTX 1060 17 NVIDIA GeForce® GTX TITAN X 18 NVIDIA GeForce® GTX 980Ti 19 NVIDIA GeForce® GTX 980 20 NVIDIA GeForce® GTX 970 21 AMD Radeon™ RX 6900 XT 22 AMD Radeon™ RX 6800 XT 23 AMD Radeon™ RX 6800 24 AMD Radeon™ RX 5700 XT 25 AMD Radeon™ RX 5700 26 AMD Radeon™ RX VEGA 27 AMD Radeon™ RX 580 28 AMD Radeon™ RX 480 29 AMD Radeon™ R9 Fury X 30 AMD Radeon™ R9 Fury 31 1 RTX 3090 NVIDIA RTX 3090 Compatibility List - Last Update: 30.11.2020 The information given here is for reference only and is provided “as is” without any warranties. Despite thorough checking, some entries might be false, especially as graphic card manufacturers occasionally change PCB-layouts without notice. If you notice an error or if you are missing a specific card, please help us to improve the list and send an e-mail to [email protected]. Manufacturer Product Product Code PCB Layout Compatible Waterblocks Backplates Comments ALIENWARE Alienware RTX 3090 RTX 30 Partner Reference 15640, 15641, 15642, 15643, 15644, 15645 16072, 16073 ASUS GeForce® RTX -

20060801-Parts

MSY Technology Prices List – The Name You Can Trust - more than 10 years in computer industry WEB SITE: www.msy.com.au Best Quality + Best Services + Best Prices + Best Performance Costs you No more –Genuine Best “Hot” Prices Offer Everyday Policy Prices change & availability without any further notices. E&OE. Condition: All Parts-1 year return to manufacturer warranty (From Date of invoice).Replace/Upgrade/Refund (15%re-stocking fee apply & Credit Card Surcharge non-Refundable) within 7 Days from Date of Invoice VIC. Malvern Branch (Melway Ref. 68 G1) 121 Waverley Road, East Malvern VIC 3145 TEL:(03) 9572 4411, (03) 9572 5186 Fax:(03) 95724022 Email [email protected] M-F 10:30AM-7:30PM Sat. 10:30AM-2:00PM VIC. Pascoe Vale Branch (Melway Ref. 16 K9) 439 Gaffney Street, Pascoe Vale VIC 3044 TEL:(03) 9379 4677, (03) 9379 4678 Fax:(03) 93794622 Email [email protected] M-F 10:30AM-6:30PM Sat. 10:30AM-2:00PM VIC. Clayton Branch (VIC) (Mel Ref. 70 K12) 9, 214-224 Wellington Road Clayton VIC 3168 TEL:(03) 9560 2288, (03) 9560 2388 Fax:(03) 95602588 Email [email protected] M-F 10:30AM-6:30PM Sat. 10:30AM-2:00PM VIC. Box Hill Branch (VIC) (Mel Ref. 47 D10) Suit 1, 2A Cambridge St., Box Hill VIC 3128 TEL:(03) 9897 4833, (03) 9897 4233 Fax:(03) 98974433 Email [email protected] M-F 10:30AM-6:30PM Sat. 10:30AM-2:00PM QLD. Morningside (Gregory’s & UBD Ref. 160 R7) 188 Thynne Road Morningside QLD 4170 TEL:(07) 3217 9070, (07) 3217 9080 fax:(07) 32179686 or [email protected] M-F 10:30AM-6:30PM Sat. -

View Annual Report

2007 ANNUAL REPORT TSE:2303 NYSE:UMC Corporate Information Spokesperson Fab 8C ADR Depositary and Registrar Chitung Liu No.6 Li-Hsin 3rd Rd., Hsinchu Science Citibank, N.A. Chief Financial Officer Park, Hsinchu, Taiwan 30078, R.O.C. Depositary Receipt Services 886 (2) 2700 6999 886 (3) 578 2258 14F, 388 Greenwich Street, [email protected] New York, NY 10013, U.S.A. Fab 8D 1 (877) 248 4237 (Toll-free) Deputy Spokesperson(s) No.8 Li-Hsin 3rd Rd., Hsinchu Science Stockholder Service Representatives are Sandy Yen Park, Hsinchu, Taiwan 30078, R.O.C. available Monday through Friday, The Chairman and CEO Office 886 (3) 578 2258 8:30a.m. to 6:00p.m., Eastern Time. Senior Manager http://wwss.citissb.com/adr/www/ 886 (2) 2700 6999 Fab 8E [email protected] [email protected] No.17 Li-Hsin Rd., Hsinchu Science Park, Hsinchu, Taiwan 30078, R.O.C. ADR Exchange Marketplace Bowen Huang 886 (3) 578 2258 New York Stock Exchange, Inc. Finance Division 11 Wall Street Senior Manager Fab 8F New York, NY 10005, U.S.A. 886 (2) 2700 6999 No.3 Li-Hsin 6th Rd., Hsinchu Science 1 (212) 656 3000 [email protected] Park, Hsinchu, Taiwan 30078, R.O.C. www.nyse.com 886 (3) 578 2258 Ticker/Search Code: UMC Headquarters No.3 Li-Hsin 2nd Rd., Hsinchu Science Fab 8S Exchangeable Bond Exchange Park, Hsinchu, Taiwan 30078, R.O.C. No.16 Creation 1st Rd., Hsinchu Science Marketplace 886 (3) 578 2258 Park, Hsinchu, Taiwan 30077, R.O.C. -

John Hancock Emerging Markets Fund

John Hancock Emerging Markets Fund Quarterly portfolio holdings 5/31/2021 Fund’s investments As of 5-31-21 (unaudited) Shares Value Common stocks 98.2% $200,999,813 (Cost $136,665,998) Australia 0.0% 68,087 MMG, Ltd. (A) 112,000 68,087 Belgium 0.0% 39,744 Titan Cement International SA (A) 1,861 39,744 Brazil 4.2% 8,517,702 AES Brasil Energia SA 14,898 40,592 Aliansce Sonae Shopping Centers SA 3,800 21,896 Alliar Medicos A Frente SA (A) 3,900 8,553 Alupar Investimento SA 7,050 36,713 Ambev SA, ADR 62,009 214,551 Arezzo Industria e Comercio SA 1,094 18,688 Atacadao SA 7,500 31,530 B2W Cia Digital (A) 1,700 19,535 B3 SA - Brasil Bolsa Balcao 90,234 302,644 Banco Bradesco SA 18,310 80,311 Banco BTG Pactual SA 3,588 84,638 Banco do Brasil SA 15,837 101,919 Banco Inter SA 3,300 14,088 Banco Santander Brasil SA 3,800 29,748 BB Seguridade Participacoes SA 8,229 36,932 BR Malls Participacoes SA (A) 28,804 62,453 BR Properties SA 8,524 15,489 BrasilAgro - Company Brasileira de Propriedades Agricolas 2,247 13,581 Braskem SA, ADR (A) 4,563 90,667 BRF SA (A) 18,790 92,838 Camil Alimentos SA 11,340 21,541 CCR SA 34,669 92,199 Centrais Eletricas Brasileiras SA 5,600 46,343 Cia Brasileira de Distribuicao 8,517 63,718 Cia de Locacao das Americas 18,348 93,294 Cia de Saneamento Basico do Estado de Sao Paulo 8,299 63,631 Cia de Saneamento de Minas Gerais-COPASA 4,505 14,816 Cia de Saneamento do Parana 3,000 2,337 Cia de Saneamento do Parana, Unit 8,545 33,283 Cia Energetica de Minas Gerais 8,594 27,209 Cia Hering 4,235 27,141 Cia Paranaense de Energia 3,200 -

Product Line Card

Product Line Card 3Com Corporation ATI Technologies Distribution CCT Technologies 3M Attachmate Corporation Century Software 4What, Inc. Autodesk, Inc. Certance 4XEM Avaya, Inc. Certance LLC Averatec America, Inc. Chanx Absolute Software Avocent Huntsville Corp. Check Point Software ACCPAC International, Inc. Axis Communications, Inc. Cherry Electrical Products Acer America Corporation Chicony Adaptec, Inc. Barracuda Networks Chief Manufacturing ADC Telecommunications Sales Battery Technology, Inc. Chili Systems Addmaster Bay Area Labels Cingular Interactive, L.P. Adesso Bay Press & Packing Cisco Systems, Inc. Adobe Systems, Inc. Belkin Corporation CMS Products, Inc. Adtran Bell & Howell CNET Technology, Inc. Advanced Digital Information BenQ America Corporation Codi Advanced Micro Devices, Inc. Best Case & Accessories Comdial AEB Technologies Best Software SB, Inc. Computer Associates Aegis Micro/Formosa– USA Bionic CCTV ComputerLand AI Coach Bionic Video Comtrol Corporation Alcatel Internetworking, Inc. Black Box Connect Tech All American Semi Block Financial Corel Corporation Allied Telesyn BorderWare Corporate Procurement Altec Lansing Technologies, Inc. Borland Software Corporation Corsair Althon Micro Boundless Technologies, Inc. Corsair Altigen Brady Worldwide Countertrade Products Alvarion, Inc. Brands, Inc. Craden AMCC Sales Corp. Brenthaven Creative Labs, Inc. AMD Bretford Manufacturing, Inc. CRU-Dataport American Portwell Technology Brooktrout Technology, Inc. CryptoCard American Power Conversion Brother International Corporation CTX Anova Microsystems Buffalo Technology/Melco Curtis Young Corporation Antec, Inc. Business Objects Americas AOpen America, Inc. BYTECC Dantz Development Corp. APC Data911 Arco Computer Products, LLC Cables To Go, Inc. Datago Ardence Cables Unlimited Dataram Areca. US Caldera Systems, Inc. Datawatch Corporation Arima Computer Cambridge Soundworks Decision Support Systems Artronix Canon USA Inc. Dedicated Micros Aspen Touch Solutions, Inc. Canton Electronics Corporation Dell Astra Data, Inc. -

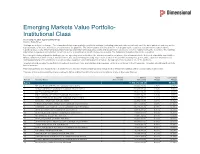

Emerging Markets Value Portfolio- Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings Are Subject to Change

Emerging Markets Value Portfolio- Institutional Class As of July 31, 2021 (Updated Monthly) Source: State Street Holdings are subject to change. The information below represents the portfolio's holdings (excluding cash and cash equivalents) as of the date indicated, and may not be representative of the current or future investments of the portfolio. The information below should not be relied upon by the reader as research or investment advice regarding any security. This listing of portfolio holdings is for informational purposes only and should not be deemed a recommendation to buy the securities. The holdings information below does not constitute an offer to sell or a solicitation of an offer to buy any security. The holdings information has not been audited. By viewing this listing of portfolio holdings, you are agreeing to not redistribute the information and to not misuse this information to the detriment of portfolio shareholders. Misuse of this information includes, but is not limited to, (i) purchasing or selling any securities listed in the portfolio holdings solely in reliance upon this information; (ii) trading against any of the portfolios or (iii) knowingly engaging in any trading practices that are damaging to Dimensional or one of the portfolios. Investors should consider the portfolio's investment objectives, risks, and charges and expenses, which are contained in the Prospectus. Investors should read it carefully before investing. This fund operates as a feeder fund in a master-feeder structure and the holdings listed below are the investment holdings of the corresponding master fund. Your use of this website signifies that you agree to follow and be bound by the terms and conditions of use in the Legal Notices. -

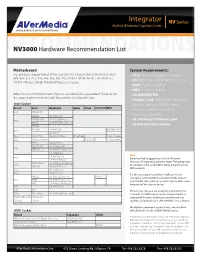

Integrator ® NV Series Hybrid Windows Capture Cards

Integrator ® NV Series www.avermedia-usa.com/surveillance Hybrid Windows Capture Cards www.averusa.com/surveillance RNV3000ECOMMENDATIONS Hardware Recommendation List Motherboard System Requirements: Our products support most of the current Intel chipsets for motherboards. Intel • CPU: Pentium 4 3.0 GHz or higher 848, 865, 875, 915, 925, 945, 955, 965, P35, NVIDIA nFORCE4 SLI - Intel Edition, • OS: Windows 7/XP/Vista/2000 - 32 bit NVIDIA nForce3 250Gb Platform Processor chipsets • RAM: 512MB or higher • HDD: 120GB or higher Below is a list of Motherboards that our validation labs have tested; however we • CD-RM/DVD-RM do support other motherboards beyond the ones listed below • Graphic Card: 32-bit high color SVGA Intel Socket graphics card with 128MB video Brand Asus Gigabyte Epox Intel FOXCONN MSI memory and DirectDraw/YUV 848 P4P800 SE Rendering Capability P4P800 GA-8IPE1000 P4P800-VM GA-8IG1000Pro-G • 10/100 Base-T Ethernet card 865 P4P8X GA-8IPE1000-G (Rev 3.1) • Sound card and speaker P5P800 P4C800 GA-8IK1100 875P Neo FISR 875 GA-8I875 915 P5GD1 Pro GA-8I915G-Duo EP-5EPA+ 915G Combo 925 P5AD2 Premium D925XCV 915G Combo P5LD2 GA-8I945P-G P5LD2-VM GA-8I 945G -MF 945 P5PL2-E GA-945PL-S3 (Rev 2.0) GA-8I945PL-G GA-8I955X Pro Note: 955 GA-8I955X Royal Based on Intel’s suggestion, for all of Microsoft P5B Deluxe/ GA-965P-DS3P (Rev 3.3) Windows XP Operating Systems, Hyper-Threading must 965 WiFi-AP GA-965P-DS3 2.0 be disabled in the system BIOS Setup program for our 975 GA-G1975X-C DVR products. -

DFA INVESTMENT DIMENSIONS GROUP INC Form NPORT-P Filed

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2020-09-29 | Period of Report: 2020-07-31 SEC Accession No. 0001752724-20-200730 (HTML Version on secdatabase.com) FILER DFA INVESTMENT DIMENSIONS GROUP INC Mailing Address Business Address 6300 BEE CAVE ROAD 6300 BEE CAVE ROAD CIK:355437| IRS No.: 363129984 | State of Incorp.:MD | Fiscal Year End: 1031 BUILDING ONE BUILDING ONE Type: NPORT-P | Act: 40 | File No.: 811-03258 | Film No.: 201208198 AUSTIN TX 78746 AUSTIN TX 78746 (512) 306-7400 Copyright © 2020 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document DFA INVESTMENT DIMENSIONS GROUP INC. FORM N-Q REPORT July 31, 2020 (UNAUDITED) Table of Contents DEFINITIONS OF ABBREVIATIONS AND FOOTNOTES Emerging Markets Portfolio Emerging Markets Small Cap Portfolio Emerging Markets Value Portfolio Emerging Markets Core Equity Portfolio U.S. Large Cap Equity Portfolio DFA Commodity Strategy Portfolio DFA One-Year Fixed Income Portfolio DFA Two-Year Global Fixed Income Portfolio DFA Selectively Hedged Global Fixed Income Portfolio DFA Short-Term Government Portfolio DFA Five-Year Global Fixed Income Portfolio DFA World ex U.S. Government Fixed Income Portfolio DFA Intermediate Government Fixed Income Portfolio DFA Short-Term Extended Quality Portfolio DFA Intermediate-Term Extended Quality Portfolio DFA Targeted Credit Portfolio DFA Investment Grade Portfolio DFA Inflation-Protected Securities Portfolio DFA Short-Term Municipal Bond Portfolio DFA Intermediate-Term Municipal Bond Portfolio -

Blancco Erasure Sw 4.10 Hardware Support

BLANCCO ERASURE SW 4.10 HARDWARE SUPPORT Blancco Ltd Länsikatu 15 FIN-80110 JOENSUU, FINLAND [email protected] Tel. +358-207-433-850 [email protected] Tel. +358-207-433-860 Fax +358-207-433-859 PAGE 1/74 Blancco Erasure SW v4.10 hardware support 30/06/2009 TABLE OF CONTENTS Mass storage controllers ....................................................................................................10 SCSI ......................................................................................................................................10 Adaptec .......................................................................................................................... 10 Advanced Micro Devices [AMD] ..................................................................................... 12 Advanced System Products, Inc..................................................................................... 12 Areca Technology Corp. .................................................................................................12 Artop Electronic Corp......................................................................................................12 BusLogic......................................................................................................................... 12 DTC Technology Corp. ...................................................................................................12 Digital Equipment Corporation ........................................................................................ 12 Future Domain Corp. -

Bluepoint Price List

file:///D|/eshot/2009/week 07/friday/faxshot/faxhtml/faxshot.html bluepoint price list Valid to Friday 27/03/09 Sales: 0870 121 8001 [email protected] Acer Extensa 5230-571G16Mn 15.4" Wide Celeron £ 272.50 Netgear 54G VPN/Fwall ADSL Modem/Router £ 41.50 Mustek PowerMust 424 400VA Line Interactive UPS £ 33.50 USB Brother DCP-350C Multifunction Colour Inkjet £ 36.25 Printer 2" A4 Storage Products CPUs Cases Crucial Gizmo 1GB USB 2.0 Flash Drive 3.75 Akasa AK-675 Intel 478-pin P4 3.4GHz Pre 3.90 Akasa 50x10mm 12V 3 Pin, 1Ball 1 Sleeve 3.19 Kingston Data Traveler USB flash drive 2.95 Akasa Socket 604 CPU Cooler 14.85 Akasa Copper RAM Sink with ShinEtsu for 5.00 Transcend 2GB JetFlash V30 with neckstra 4.15 Akasa AK-875 AMD Cooler Fan for Skt AM2 15.10 Midi Tower Computer Case without PSU 6.55 Kingston 2GB DataTraveler 100 USB2.0 Fla 4.17 AMD Sempron 3000+ 1.8 GHz Processor 17.50 Akasa PAX.mate Noise reduction matting 5.75 Kingston 2GB USB flash drive 4.95 Intel Celeron 420 1.6GHz Processor Socke 20.35 C200 Micro ATX Case USB 2.0 Audio+MIC Po 8.95 2.0GB USB 2.0 Flash Drive 4.81 AMD Sempron LE-1250 2.20GHz 512KB L2 800 23.25 FSC-303 Midi ATX Tower Case 8.45 Kingston 4 GB Data Traveler USB Flash 6.95 Intel Celeron D 2.8GHz 533FSB LGA775 Rtl 22.75 400w LK Mini Tower Black/Silver Snd/USB 13.35 Transcend 4GB JetFlash V30 USB 2.0 6.45 Intel Celeron D 352 3.2 GHz CPU - LGA775 26.35 Trust LE-MD 350W Black Midi Tower Case 14.95 Transcend StoreJet 2.5" ID Hard Disk Enc 6.95 Intel Celeron 430 1.8GHz Processor Socke 26.50 Q-Tec L-MD 350W MIDI Tower