December 2018 Quarter 43

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

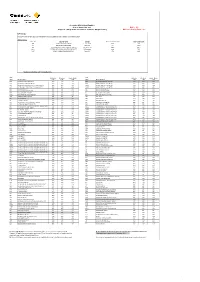

Socially Conscious Australian Equity Holdings

Socially Conscious Australian Equity Holdings As at 30 June 2021 Country of Company domicile Weight COMMONWEALTH BANK OF AUSTRALIA AUSTRALIA 10.56% CSL LTD AUSTRALIA 8.46% AUST AND NZ BANKING GROUP AUSTRALIA 5.68% NATIONAL AUSTRALIA BANK LTD AUSTRALIA 5.32% WESTPAC BANKING CORP AUSTRALIA 5.08% TELSTRA CORP LTD AUSTRALIA 3.31% WOOLWORTHS GROUP LTD AUSTRALIA 2.93% FORTESCUE METALS GROUP LTD AUSTRALIA 2.80% TRANSURBAN GROUP AUSTRALIA 2.55% GOODMAN GROUP AUSTRALIA 2.34% WESFARMERS LTD AUSTRALIA 2.29% BRAMBLES LTD AUSTRALIA 1.85% COLES GROUP LTD AUSTRALIA 1.80% SUNCORP GROUP LTD AUSTRALIA 1.62% MACQUARIE GROUP LTD AUSTRALIA 1.54% JAMES HARDIE INDUSTRIES IRELAND 1.51% NEWCREST MINING LTD AUSTRALIA 1.45% SONIC HEALTHCARE LTD AUSTRALIA 1.44% MIRVAC GROUP AUSTRALIA 1.43% MAGELLAN FINANCIAL GROUP LTD AUSTRALIA 1.13% STOCKLAND AUSTRALIA 1.11% DEXUS AUSTRALIA 1.11% COMPUTERSHARE LTD AUSTRALIA 1.09% AMCOR PLC AUSTRALIA 1.02% ILUKA RESOURCES LTD AUSTRALIA 1.01% XERO LTD NEW ZEALAND 0.97% WISETECH GLOBAL LTD AUSTRALIA 0.92% SEEK LTD AUSTRALIA 0.88% SYDNEY AIRPORT AUSTRALIA 0.83% NINE ENTERTAINMENT CO HOLDINGS LIMITED AUSTRALIA 0.82% EAGERS AUTOMOTIVE LTD AUSTRALIA 0.82% RELIANCE WORLDWIDE CORP LTD UNITED STATES 0.80% SANDFIRE RESOURCES LTD AUSTRALIA 0.79% AFTERPAY LTD AUSTRALIA 0.79% CHARTER HALL GROUP AUSTRALIA 0.79% SCENTRE GROUP AUSTRALIA 0.79% ORORA LTD AUSTRALIA 0.75% ANSELL LTD AUSTRALIA 0.75% OZ MINERALS LTD AUSTRALIA 0.74% IGO LTD AUSTRALIA 0.71% GPT GROUP AUSTRALIA 0.69% Issued by Aware Super Pty Ltd (ABN 11 118 202 672, AFSL 293340) the trustee of Aware Super (ABN 53 226 460 365). -

Stoxx® Pacific Total Market Index

STOXX® PACIFIC TOTAL MARKET INDEX Components1 Company Supersector Country Weight (%) CSL Ltd. Health Care AU 7.79 Commonwealth Bank of Australia Banks AU 7.24 BHP GROUP LTD. Basic Resources AU 6.14 Westpac Banking Corp. Banks AU 3.91 National Australia Bank Ltd. Banks AU 3.28 Australia & New Zealand Bankin Banks AU 3.17 Wesfarmers Ltd. Retail AU 2.91 WOOLWORTHS GROUP Retail AU 2.75 Macquarie Group Ltd. Financial Services AU 2.57 Transurban Group Industrial Goods & Services AU 2.47 Telstra Corp. Ltd. Telecommunications AU 2.26 Rio Tinto Ltd. Basic Resources AU 2.13 Goodman Group Real Estate AU 1.51 Fortescue Metals Group Ltd. Basic Resources AU 1.39 Newcrest Mining Ltd. Basic Resources AU 1.37 Woodside Petroleum Ltd. Oil & Gas AU 1.23 Coles Group Retail AU 1.19 Aristocrat Leisure Ltd. Travel & Leisure AU 1.02 Brambles Ltd. Industrial Goods & Services AU 1.01 ASX Ltd. Financial Services AU 0.99 FISHER & PAYKEL HLTHCR. Health Care NZ 0.92 AMCOR Industrial Goods & Services AU 0.91 A2 MILK Food & Beverage NZ 0.84 Insurance Australia Group Ltd. Insurance AU 0.82 Sonic Healthcare Ltd. Health Care AU 0.82 SYDNEY AIRPORT Industrial Goods & Services AU 0.81 AFTERPAY Financial Services AU 0.78 SUNCORP GROUP LTD. Insurance AU 0.71 QBE Insurance Group Ltd. Insurance AU 0.70 SCENTRE GROUP Real Estate AU 0.69 AUSTRALIAN PIPELINE Oil & Gas AU 0.68 Cochlear Ltd. Health Care AU 0.67 AGL Energy Ltd. Utilities AU 0.66 DEXUS Real Estate AU 0.66 Origin Energy Ltd. -

Investment Menu 9 August 2021

Investment Menu 9 August 2021 This Investment Menu provides you with up-to-date listing of the Investment Options available through Australian Practical Investor Service. You should read the relevant disclosure documentation or seek appropriate professional advice before making an investment decision. The information in this Investment Menu refers to the Australian Practical Investor Service Guide dated 15 June 2020. Part 1: Core Menu Managed Funds Term Deposits NAME CODE NAME TYPE AMP BANK Janus Henderson Tactical Income IOF0145AU ANZ BANK Mercer Diversified Alternatives MIN0026AU BANK OF QUEENSLAND BANK Mercer Income Plus MIN0027AU GOLDFIELDS MONEY BANK State Street Australian Cash Trust SST0003AU MEMBERS EQUITY BANK BANK State Street Global Equity SST0050AU NAB BANK State Street Multi-Asset Builder SST0052AU Page 1 of 16 Part 2: Full Menu NAME CODE Cromwell Phoenix Property Securities CRM0008AU Managed Funds Cromwell Direct Property CRM0018AU NAME CODE Aberdeen Standard Australian Fixed Income CRS0004AU AAP0001AU Candriam Sustainable Global Equity Bentham Global Income CSA0038AU Ausbil Australian Geared Equity AAP0002AU Bentham Syndicated Loan CSA0046AU Ausbil MicroCap AAP0007AU Eley Griffiths Small Companies EGG0001AU Ausbil Australian Active Equity AAP0103AU Aberdeen Standard Asian Opportunities EQI0028AU Ausbil Australian Emerging Leaders AAP0104AU PIMCO Australian Bond Wholesale ETL0015AU Ausbil Active Dividend Income Wholesale AAP3656AU PIMCO Diversified Fixed Interest Wholesale ETL0016AU AllianceBernstein Managed Volatility Equities ACM0006AU PIMCO Global Bond Wholesale ETL0018AU Advance Balanced Multi Blend Wholesale ADV0050AU Aberdeen Standard Emerging Opportunities ETL0032AU Advance Growth Multi Blend Wholesale ADV0085AU MFS Fully Hedged Global Equity Trust ETL0041AU Advance High Growth Multi Blend Wholesale ADV0087AU SGH 20 ETL0042AU Advance Moderate Multi Blend Wholesale ADV0091AU SGH ICE ETL0062AU Fairview Equity Partners Emerging Companies ANT0002AU T. -

Commsec Margin Lending Approved Securities List

Accepted ASX Listed Equities as at 21 September 2021 Buffer - 5% Subject to change at the discretion of CommSec Margin Lending Maximum Gearing Ratio - 90% LVR Changes Changes since the last Approved Securities List was published are outlined in the below table: ASX Securities ASX Code Security Name Change Previous Portfolio LVR New Portfolio LVR AST AUSNET SERVICES LIMITED Capped LVR 75% 75% BGL BELLEVUE GOLD LIMITED New LVR 0% 40%* SXL SOUTHERN CROSS MEDIA GROUP LIMITED Uncapped LVR 40%* 40%* QLTY BETASHARES GLOBAL QUALITY LEADERS ETF LVR Increase 65% 70% CLNE VANECK GLOBAL CLEAN ENERGY ETF New LVR 0% 65% *Available via facilities with PLVR enabled only ASX Portfolio Standard Single Stock ASX Portfolio Standard Single Stock Code Security Name LVR LVR LVR Code Security Name LVR LVR LVR A200 BETASHARES AUSTRALIA 200 ETF 80% 75% 70% BNKS BETASHARES GLOBAL BANKS ETF 70% 65% 60% A2M THE A2 MILK COMPANY LIMITED 55% 50% 45% BOQ BANK OF QUEENSLAND LIMITED 70% 65% 60% AAA BETASHARES AUSTRALIAN HIGH INTEREST CASH ETF 90% 85% 80% BOQPE BANK OF QUEENSLAND LIMITED 70% 65% 60% AAC AUSTRALIAN AGRICULTURAL COMPANY LIMITED 50% 45% 40% BOQPF BANK OF QUEENSLAND LIMITED 70% 65% 60% ABA AUSWIDE BANK LTD 50% 45% 40% BPT BEACH ENERGY LIMITED 50% 45% 40% ABC ADELAIDE BRIGHTON LIMITED 60% 55% 50% BRG BREVILLE GROUP LIMITED 65% 60% 55% ABP ABACUS PROPERTY GROUP 65% 60% 55% BSL BLUESCOPE STEEL LIMITED 70% 65% 60% ACDC ETFS BATTERY TECH & LITHIUM ETF 60% 55% 50% BVS BRAVURA SOLUTIONS LIMITED 45% 40% 35% AD8 AUDINATE GROUP LIMITED 40% 0% 0% BWP BWP TRUST 70% 65% 60% ADH ADAIRS LIMITED 45% 40% 35% BWX BWX LIMITED 45% 40% 35% ADI APN INDUSTRIA REIT 60% 55% 50% BXB BRAMBLES LIMITED 80% 75% 70% AEF AUSTRALIAN ETHICAL INVESTMENT LIMITED 40% 35% 30% CAJ CAPITOL HEALTH LIMITED 40% 0% 0% AFG AUSTRALIAN FINANCE GROUP LTD 40% 35% 30% CAR CARSALES.COM LIMITED. -

September 2018 Selector High Conviction Equity Fund Quarterly Newsletter #61

1 6 8 No. 201 Quarterly Newsletter FML September S In this quarterly edition, we review performance and attribution for the quarter. We visit John Guest in London and trek to Alaska. We try to understand the human genome and we call for a more balanced media. Photo. We seek humble management, Peter Botten Oil Search CEO, opening the door to Alaska. Selector Funds Management Limited ACN 102756347 AFSL 225316 Level 8, 10 Bridge Street Sydney NSW 2000 Australia Tel 612 8090 3612 www.selectorfund.com.au September 2018 Selector High Conviction Equity Fund Quarterly Newsletter #61 About Selector We are a boutique fund manager with a combined experience of over 150 years. We believe in long-term wealth creation and building lasting relationships with our investors. Our focus is stock selection. Our funds are high conviction, concentrated and index unaware. As a result, we have low turnover and produce tax effective returns. We seek businesses with leadership qualities, run by competent management teams, underpinned by strong balance sheets and with a focus on capital management. 1 September 2018 Selector High Conviction Equity Fund Quarterly Newsletter #61 Dear Investor, The September quarter proved more eventful than the benign market moves would suggest. Company reporting season brought the usual variety of outcomes, however, it was the external regulatory and political shocks that stole the show. The swearing in of Scott Morrison as our newest Prime Minister was an event all too familiar for Australians, following the loss of party room support for the outgoing PM Malcolm Turnbull. This, at a time of strong economic results is a blight on those elected to lead. -

Sustainable Investing Bulletin 30 June 2020

Sustainable Year ended Investing Bulletin 30 June 2020 from TelstraSuper This Bulletin summarises our sustainable Incorporating ESG Issues into Investment investing activities for the year ended Analysis and Decision-Making 30 June 2020. External Manager Selection and Monitoring Our approach to Sustainable Investment follows · Eighteen managers were reviewed during the financial the guidelines of the UN Principles for Responsible year for new or follow-on investment. Thirteen of these Investing (PRI), which are: managers were subsequently appointed or recommended. Incorporating Environmental, Social and · Five new managers were approved in Australian Equities, two in International Equities, four in Alternatives 1 Governance (ESG) issues into investment analysis and decision-making and two in Property. Our assessment confirmed the approved managers integrate ESG analysis in their investment processes. 2 Active ownership · A comprehensive review was also undertaken on two incumbent Australian equities managers and one International manager. All three managers were assessed as having strong ESG capabilities. ESG disclosure 3 by investee companies · These reviews involve validating the manager’s integration of ESG activities into its investment process and discussing key portfolio holdings. Advocacy and Collaboration · ESG issues covered with incumbent managers were 4 corporate governance, voting activity, climate change, worker’s rights and modern slavery. Internal Investment Management Reporting on our activities 5 Australian Equities · The Australian Equities and Sustainable Investing Team developed an ESG assessment tool for Australian TelstraSuper’s Sustainable Investment companies and commenced rating the top 200 listed Policy can be accessed here. companies on the ASX. TelstraSuper Sustainable Investing Bulletin Year ended 30 June 2020 1 Fixed Income Strategy/ · Met with several sustainable finance ESG Operating Company Matters Update and green bond issuers. -

Aussie Equities 2021 Feb End.Xlsx

Security Name Market Value BHP GROUP $180,008,291.34 AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED $107,263,999.63 NATIONAL AUSTRALIA BANK $100,116,632.00 WESTPAC BANKING CORPORATIONORD F/PD SHARES $80,685,914.76 CSL LIMITED $75,662,945.19 MACQUARIE GROUP LTD $72,477,296.32 COMMONWEALTH BANK OF AUSTRALIA $71,881,437.92 TELSTRA CORPORATION LTD $67,183,032.84 WOOLWORTHS GROUP LIMITED $47,628,808.20 RIO TINTO LTD $47,221,068.16 WOODSIDE PETROLEUM LIMITED $43,518,359.43 JAMES HARDIE INDUSTRIES PLC CDI $37,144,105.68 WESFARMERS LIMITED ORD FULLY PAID SHARES $37,136,069.40 LENDLEASE GROUP $35,794,263.40 ARISTOCRAT LEISURE LTD $33,565,985.64 QBE INSURANCE GROUP LIMITED $32,171,864.56 SOUTH32 LIMITED ORDINARY FULLYPAID $30,752,265.77 COMPUTERSHARE LIMITED $30,129,389.03 COLES GROUP LTD $27,637,767.15 AMCOR LIMITED CDI $26,561,345.12 TABCORP HOLDINGS $25,919,874.95 QUBE HOLDINGS LTD $25,666,575.36 SANTOS LIMITED $25,031,127.60 HARVEY NORMAN HOLDINGS LIMITED $21,484,681.20 VIRGIN MONEY UK PLC - CDI $20,078,022.25 FORTESCUE METALS GROUP LIMITEDORDINARY FULLY APID SHARES $20,060,797.83 ALS LIMITED $19,710,175.16 REA GROUP LTD ORD F/PD $18,907,264.80 AUD RECEIVABLE $18,594,893.91 SUNCORP GROUP LIMITED $18,429,356.40 SEEK LIMITED $18,215,928.70 MINERAL RESOURCES LIMITED $18,198,718.08 SEVEN GROUP HOLDINGS LTD $17,153,297.91 FLETCHER BUILDING LIMITED $16,555,029.96 MEDIBANK PRIVATE LTD $16,134,244.49 IRESS LTD $15,953,463.21 NINE ENTERTAINMENT CO HOLDINGS $15,925,251.16 SCENTRE GROUP $14,896,500.48 WORLEY LTD $14,363,655.30 DOMINOS PIZZA ENTERPRISES -

Annual Report 2020

BREVILLE GROUP LIMITED Annual Report 2020 For personal use only Breville Group Limited Annual report 2020 Contents: Chairman’s review 1 CEO’s review 3 Strategy and brands 5 Financial report 13 Shareholder information 114 Company information 116 Annual general meeting: Thursday 12 November 2020 at 10am Virtual AGM. For personal use only (this page and outside covers) the 3X Bluicer™ Pro Chairman’s review “The Group successfully navigated an unprecedented FY20 and has come out even stronger” In the 2020 Financial year the Group continued up The Board increased the full year dividend for the curve of our acceleration program with double- the year by 10.8% to 41.0 cents from 37.0 cents in digit sales and EBIT growth, on a normalised1 the prior year, with a fully underwritten Dividend basis, in the face of a series of challenging events Reinvestment Plan (DRP) activated to preserve including the global pandemic. cash and to allow future flexibility. The Group delivered total sales revenue of $952.2m, On behalf of the Board, I would like to take this a 25.3% growth on prior year with the core Global opportunity to express our gratitude to Jim Clayton Product segment growing by 24.9%, or 20.1% and to his talented, motivated and passionate team on a constant currency basis, to $764.4m. The members who have shown exceptional nimbleness, Distribution segment revenue for the year also grew and resilience, in these unprecedented times. We 26.9% to $187.8m. are privileged to have such an exceptional group on the Breville team. -

Index Rebalance

Index Rebalance Friday 11th June 2021 Reference No: 0004/21 Subject: Index Rebalance The June 2021 quarterly rebalancing results for the CXA 200 Index will be effective at the open on Monday 21st June 2021. The additions and deletions, as well as other changes made to the indices, resulting from the June 2021 quarterly rebalancing are shown below. Inclusions Ticker Name Reason GXY Galaxy Resources Ltd New Entrants with ranking equal or above 180 SLK Sealink Travel Group Ltd New Entrants with ranking equal or above 180 IMU Imugene Ltd New Entrants with ranking equal or above 180 PTM Platinum Asset Management New Entrants with ranking equal or above 180 PDN Paladin Energy Ltd New Entrants with ranking equal or above 180 Exclusions Ticker Name Reason GWA Gwa Group Ltd Failed Eligibility Rank 251 MMS Mcmillan Shakespeare Ltd Failed Eligibility Rank 258 NXL Nuix Ltd Exclusions with ranking equal or below 220 PRN Perenti Global Ltd Exclusions with ranking equal or below 220 VOC Vocus Group Ltd Excluded due to upcoming M&A Please contact [email protected] with any queries. Chi-X Market Operations Phone: +61 2 8078 1701 | Email: [email protected]| Web: chi-x.com.au | Disclaimer Appendix A: Constituent List The index portfolio below is based on data from 1 June 2021. Newly added constituents are in BOLD. Chi-X indices (CXA 200 Index) Ticker Name CBA COMMONWEALTH BANK OF AUSTRALIA BHP BHP GROUP LTD CSL CSL LTD WBC WESTPAC BANKING CORP NAB NATIONAL AUSTRALIA BANK LTD ANZ AUST AND NZ BANKING GROUP WES WESFARMERS LTD WOW WOOLWORTHS GROUP LTD -

Accredited Sponsors at 3 June 2020 and ANZSCO Unit Group 2613 Primary Visa Grants

Document 1 Freedom of Information Request FA 20/06/00144 Accredited Sponsors at: 3 June 2020 Sponsor Name 1300SMILES Ltd 2XU PTY LTD 3D Systems Asia-Pacific Pty Ltd 3M australia 3P Learning Limited 4mation Technologies Pty Ltd A & G ENGINEERING PTY LTD A ABRAHAMS & OTHERS A CROOK & Others A HARTRODT AUSTRALIA PTY LTD A Trahair & Others A.N. COOKE MANUFACTURING COMPANY PROPRIETARY LIMITED A.P. Eagers Limited AAA NEXTT GROUP PTY LTD AAM PTY LTD AAPC LIMITED AAW Global Logistics Pty Ltd ABARIS PRINTING AND PUBLISHING CO PTY LTD ABB Australia Pty Ltd ABB POWER GRIDS AUSTRALIA PTY LIMITED Abbott Australasia PTY LTD Abbott Risk Consulting Ltd Abbvie Pty Ltd ABERDEEN STANDARD INVESTMENTS AUSTRALIA LIMITED ABERGELDIE PERSONNEL PTY LTD ABM Systems Australia Pty Ltd ABN AMRO CLEARING SYDNEY PTY LTD ABT ASSOCIATES PTY LTD Acadian Asset Management (Australia) Ltd ACCENT GROUP LIMITED Accenture Australia Holdings Pty Ltd ACCESS TESTING PTY LTD ACCIDENT & HEALTH INTERNATIONAL UNDERWRITING PTY LTD ACCIONA ENERGY AUSTRALIA GLOBAL PTY LTD ACCIONA INFRASTRUCTURE AUSTRALIA PTY LTD ACCOLADE WINES AUSTRALIA LIMITED Accordant Pty Ltd Achmea Schadeverzekeringen N.V. ACI Operations Pty Ltd ACI WORLDWIDE (PACIFIC) PTY LTD ACN 150 898 605 PTY LTD ACON Health Limited ACT Corrective Services ACT Education and Training Directorate ACT EMERGENCY SERVICES AGENCY ACTIVE CONTRACTING PTY LTD Activision Blizzard Pty Limited Page 1 Document 1 Adapt-A-Lift Group Pty Ltd Adecco Australia Pty Ltd Adelaide Animal Hospitals Pty Ltd Adelaide Community Healthcare Alliance Incorporated Adelaide Festival Centre Trust ADELAIDE UNICARE PTY LTD ADG ENGINEERS (AUST) PTY LTD ADIDAS AUSTRALIA PTY LIMITED ADOBE SYSTEMS PTY LTD Adrenalin Media Pty Ltd Adult Multicultural Education Services Advance Delivery Consulting Pty Ltd ADVANCE VISION TECHNOLOGY (AUST.) PTY. -

Technology and Telecommunications Industry Profile

Technology and Telecommunications Industry Profile Overview Technology and Telecommunications ASX offers companies a globally recognised listing and Indices v S&P/ASX 200 capital raising venue, attracting both Australian and international investors. 175 Listing on ASX provides companies with: 150 • Access to capital • Liquidity 125 • Visibility ebased) 100 (r Australia has the 6th largest pool of investment assets 75 in the world and the largest in Asia*. With around 2,100 value listed companies, spread across all sectors and a range 50 of geographical regions, ASX is the world’s 9th largest Index equity market by free-float market capitalisation, 25 and is consistently ranked in the world’s top equity markets for equity capital raising. 0 * Source: Austrade; Investment Company Institute, Jul17 Jul 11 Jul 13 Jul 15 Jul 12 Jul 16 Jul 14 Jul 10 Jan 11 Jul 07 Jul 09 Jan 17 Jan 13 Jan 15 Jul 08 Jan 12 Jan 16 Jan 14 Jan 10 Jan 07 Jan 09 Worldwide Mutual Fund Market Data, Q1 2017. Jan 08 S&P/ASX 200 S&P/ASX 200 Info Tech S&P/ASX 200 Telecommunications Source: Bloomberg, August 2017 Recent IPOs ASX COMPANY SECTOR LISTING CAPITAL MARKET LEAD MANAGER CODE NAME DATE RAISED CAPITALISATION (A$ M) ON LISTING (A$ M) APT Afterpay Touch Group Ltd Software & Services Jun-17 - 404.4 n/a ELO Elmo Software Ltd Software & Services Jun-17 25.0 108.3 Wilsons Corporate Finance Canaccord Genuity DN8 Dreamscape Networks Ltd Software & Services Dec-16 25.0 86.0 (Australia) Technology Hardware & AD8 Audinate Group Ltd Jun-17 21.0 72.6 Shaw and Partners Equipment -

Asx200 Senior Executive Census 2019 Foreword

Chief Executive Women Women leaders enabling women leaders ASX200 SENIOR EXECUTIVE CENSUS 2019 FOREWORD Chief Executive Women (CEW) presents the results of our third ASX200 Senior Executive Census (the Census). The Census measures annual progress of ASX200 companies in improving the representation of women in their executive leadership teams. Alongside the aggregate measurements of the ASX200 leadership teams, the Census focuses on the representation of women in ‘line’ and ‘function’ roles within executive leadership teams. Line roles are those that directly drive key commercial outcomes of a company and generally include accountability for profit and loss. Line roles are predominately a pathway to CEO. Approximately 90% of CEO appointments this year were from line roles. In contrast, functional roles govern specific operations of an organisation such as finance, legal, compliance, marketing or human resources. Of these, the role of CFO, frequently one of the most senior and influential roles in the executive leadership team, can directly progress to a CEO role. In 2019, the overall number of women occupying CFO roles is 16%, up from 12% in 2018 and 9% in 2017. CEW recognises other improvements in 2019. The number of companies with no women in their executive leadership team has fallen from 23 to 17, and the number of companies with one or more women in their executive leadership team has increased from 89% to 92%. Women represent 25% of total executive leadership positions, an increase from 23% in 2018. However, 75% of these roles are functional roles, and women remain underrepresented in line roles, at a mere 13%.