Scale Economies and Capacity Utilization in U

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Urban Concentration: the Role of Increasing Returns and Transport Costs

i'445o Urban Concentration: The Role of Increasing Retums and Transport Costs Public Disclosure Authorized Paul Krugman Very largeurban centersare a conspicuousfeature of many developingeconomies, yet the subject of the size distribution of cities (as opposed to such issuesas rural-urban migration) has been neglected by development economists. This article argues that some important insights into urban concentration, especially the tendency of some developing countris to have very large primate cdties, can be derived from recent approachesto economic geography.Three approachesare comparedrthe well-estab- Public Disclosure Authorized lished neoclassica urban systems theory, which emphasizes the tradeoff between agglomerationeconomies and diseconomies of city size; the new economic geogra- phy, which attempts to derive agglomeration effects from the interactions among market size, transportation costs, and increasingreturns at the firm level; and a nihilistic view that cities emerge owt of a randon processin which there are roughly constant returns to city size. The arttcle suggeststhat Washingtonconsensus policies of reducedgovernment intervention and trade opening may tend to reducethe size of primate cties or at least slow their relativegrowth. Over the past severalyears there has been a broad revivalof interestin issues Public Disclosure Authorized of regional and urban development. This revivalhas taken two main direc- dions. T'he first has focused on theoretical models of urbanization and uneven regional growth, many of them grounded in the approaches to imperfect competition and increasing returns originally developed in the "new trade" and anew growth" theories. The second, a new wave of empirical work, explores urban and regional growth patterns for clues to the nature of external economies, macro- economic adjustment, and other aspects of the aggregate economy. -

Capacity Utilization, Inflation and Monetary Policy

Capacity Utilization, Inflation and Monetary Policy: Classicals, post-Keynesians and the New Keynesian Consensus Peter Kriesler and Marc Lavoie1 Abstract The paper looks at the adjustment process towards long run equilibrium within Marxian models, defined in terms of normal rates of capacity utilization. The model is reduced to three essential equations: an IS equation, a Phillips curve equation and an central bank reaction function. It is shown that long run convergence depends on the specific inflation (Phillips curve) equation, and on the central bank setting a zero inflationary target. When these conditions are relaxed, the results are shown to accord more closely with post-Keynesian results. The Marxian model is then contrasted with New Consensus models, which only varies in its inflation/Phillips curve equation. Post-Keynesian criticisms of both the IS and the Phillips curve equation are considered, and suggestions for a post-Keynesian alternative are made. Keywords: monetary policy, central bank, inflation, capacity utilization, post-Keynesian, New- Keynesian JEL classification: E12, E40, E52, E58 In an extremely interesting paper, Duménil and Lévy (Duménil and Lévy 1999) explore the adjustment mechanism of an economy towards a long run equilibrium with capacity utilization at normal levels − a fully adjusted position as the Sraffians would call it, or a classical long-term equilibrium as Duménil and Lévy have it. Short run equilibrium within their model is of the Keynes/Kalecki type, with variability in levels of capacity utilization. One distinctive feature of their model is that it is not the forces of competition which push the economy to a fully adjusted position, but rather aspects of the macro economy coupled with the behaviour of the central bank. -

Employment and Capacity Utilization Over the Business Cycle

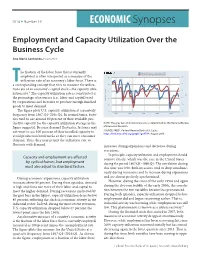

2016 n Number 19 ECONOMIC Synopses Employment and Capacity Utilization Over the Business Cycle Ana Maria Santacreu, Economist he fraction of the labor force that is currently Capacity Utilization: Total Industry (left) 100-Civilian Unemployment Rate (right) 98 employed is often interpreted as a measure of the 90 utilization rate of an economy’s labor force. There is 96 T 85 a corresponding concept that tries to measure the utiliza- tion rate of an economy’s capital stock—the capacity utili- 94 80 zation rate.1 The capacity utilization rate is constructed as 100-% 92 the percentage of resources (i.e., labor and capital) used 75 Percent of Capacity by corporations and factories to produce enough finished 90 goods to meet demand. 70 88 The figure plots U.S. capacity utilization at a quarterly 65 frequency from 1967:Q1–2016:Q1. In normal times, facto- 1970 1980 1990 2000 2010 ries tend to use around 80 percent of their available pro- fred.stlouisfed.org myf.red/g/6ZXZ ductive capacity (as the capacity utilization average in the NOTE: The gray bars indicate recessions as determined by the National Bureau figure suggests). Because demand fluctuates, factories may of Economic Research. SOURCE: FRED®, Federal Reserve Bank of St. Louis; not want to use 100 percent of their installed capacity to https://fred.stlouisfed.org/graph/?g=6TA4; August 2016. avoid production bottlenecks so they can meet consumer demand. Thus, they may permit the utilization rate to fluctuate with demand. increases during expansions and decreases during recessions. In principle, capacity utilization and employment should Capacity and employment are affected comove closely, which was the case in the United States by cyclical factors, but employment during the period 1967:Q1–1990:Q1. -

1 Objective 2 Examples of Cost Functions

BEE1020 { Basic Mathematical Economics Dieter Balkenborg Week 8, Lecture Thursday 28.11.02 Department of Economics Increasing and convex functions University of Exeter 1Objective The ¯rst and the second derivative of a function contain important qualitative information about the graph of a function. The ¯rst derivative of a function measures the steepness of its graph. The second derivative (the derivative of the derivative) measures how \curved" the graph is. We illustrate this and discuss for cost functions what it means in economic terms. 2 Examples of cost functions A function describes how one quantity changes in response to another quantity. An ex- ample is the total cost function of a ¯rm. Consider, for instance, a publisher selling a particular newspaper. His production costs depend on the number of newspapers he prints. This information { together with information on the demand side { will be im- portant if the publisher tries to make a pro¯t out of his business. There are three ways to describe the relation between production costs and the number of newspapers produced: 1. by a table, 2. by a graph, 3. using an algebraic expression to describe the relationship. Here are three examples of types of cost functions frequently used in microeconomics. 2.1 Example 1: Constant marginal costs In tabular form: quantity (in 100.000) 0 1 2 3 4 5 6 7 total costs (in 1000$) 90 110 130 150 170 190 210 230 With the aid of a graph: 220 200 180 160 140 TC120 100 80 60 40 20 0 1234567Q In algebraic form: TC(Q)=90+20Q 2.2 Example 2: Increasing -

TRANSACTION COST LIMITS to ECONOMIES of SCALE Cotton M

DO RATE AND VOLUME MATTER? TRANSACTION COST LIMITS TO ECONOMIES OF SCALE Cotton M. Lindsay & Michael T. Maloney Department of Economics Clemson University In the traditional treatment, economies of scale are attributed to a hodgepodge of sources. A typical list might include Adam Smith's famous "division of labour," economies of large machines, the integration of processes, massed reserves, and standardization. The list can be partly systematized because, when considered in detail, these various economies are themselves the result of various other more basic and occasionally overlapping principles. For example, both economies of massed reserves and economies of standardi- zation are to a certain extent the product of the statistical “law of large numbers.” However, even this analysis fails to strike to the heart of the matter because the technological factors however described that reduce costs with scale do not in themselves imply that large firms can produce at lower cost than small firms. The possible presence of such technological scale economies does not give us adequate knowledge to predict the structure of industry. These forces of nature may combine to make it cheaper to get things done in big chunks. However, this potential will be economically important only in the presence of transactions costs. Firms can specialize their production processes and hire out the jobs that require large scale. Realistically all firms hire out some portion of the production process regard- less of their size. General Motors ships many of its automobiles by rail, but does not own a railroad for this purpose. Anaconda uses a great deal of fuel oil in its production of copper, but it does not own oil wells or refineries. -

The Role of Industrial and Post-Industrial Cities in Economic Development

Joint Center for Housing Studies Harvard University The Role of Industrial and Post-Industrial Cities in Economic Development John R. Meyer W00-1 April 2000 John R. Meyer is James W. Harpel Professor of Capital Formation and Economic Growth, Emeritus and chairman of the faculty committee of the Joint Center for Housing Studies. by John R. Meyer. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including notice, is given to the source. Draft paper prepared for the World Bank Urban Development Division's research project entitled "Revisiting Development - Urban Perspectives." Any opinions expressed are those of the author and not those of the Joint Center for Housing Studies of Harvard University or of any of the persons or organizations providing support to the Joint Center for Housing Studies, nor of the World Bank Urban Development Division. The Role of Industrial and Post-Industrial Cities in Economic Development by John R. Meyer Once upon a time the location of towns and cities, at least superficially, seemed to be largely determined by the preferences of kings, princes, bishops, generals and other political and military leaders of society. A site’s defensibility or its capabilities for imposing military or administrative control over surrounding countryside were often of paramount importance. As one historian summed up the conventional wisdom: “Cities...were to be found...wherever agriculture produced sufficient surplus to sustain a population of rulers, soldiers, craftsmen and other nonfood producers.”1 The key to successful urbanization, in short, wasn’t so much what the city could do for the countryside as what the countryside could do for the city.2 This traditional view of early cities, while perhaps correct in its essentials, is also almost surely too limited.3 Cities were never just parasitic; most have always added at least some economic value. -

Cost Concepts the Cost Function

(Largely) Review: Cost concepts The Cost Function • Cost function C(q): minimum cost of producing a given quantity q • C(q) = F + V C(q), where { Fixed costs F : cost incurred regardless of output amount. Avoidable vs. sunk: crucial for determining shut-down decisions for the firm. { Variable costs V C(q); vary with the amount produced. C(q) { Average cost AC(q) = q @C(q) { Marginal cost MC(q) = @q V C(q) F { AV C(q) = q ; AF C(q) = q ; AC(q) = AV C(q) + AF C(q). Example • C(q) = 125 + 5q + 5q2 • AC(q) = • MC(q) = • AF C(q) = 125=q • AV C(q) = 5 + 5q q AC(q) MC(q) 1 135 15 • 3 61.67 35 5 55 55 7 57.86 75 9 63.89 95 • AC rises if MC exceeds it, and falls if MC is below it. Implies that MC intersects AC at the minimum of AC. Short-run vs. long-run costs: • Short run: production technology given • Long run: can adapt production technology to market conditions • Long-run AC curve cannot exceed short-run AC curve: its the lower envelope Example: \The division of labor is limited by the extent of the market" (Adam Smith) • Division of labor requires high fixed costs (for example, assembly line requires high setup costs). • Firm adopts division of labor only when scale of production (market demand) is high enough. • Graph: Price-taking firm has \choice" between two production technologies. Opportunity cost The opportunity cost of a product is the value of the best forgone alternative use of the resources employed in making it. -

Imbalance Game 2.0: a Tale of Two Productivities

NEW THINKING Imbalance Game 2.0: A Tale of Two Productivities Michael Craig, CFA Vice President & Director Haining Zha, CFA Vice President September 2017 Almost nine years after the financial crisis, the global economy remains mired in low growth. Low productivity growth is certainly a key contributing factor, but our research shows that current productivity measures don’t tell the whole story. In this article, we propose a fundamental change to how people should examine productivity: we believe the supply and demand sides should be viewed separately to obtain more robust insights. Taking this approach allows us to differentiate supply-side progress from demand-side malaise and shows that the economy may be more promising than commonly thought. In addition, it highlights large supply-side divergences within and across different sectors of the economy, which are not reflected in the aggregate productivity measure – potentially leading to a distorted economic picture. Viewing productivity through this new lens, we believe that: • Nominal economic growth will remain low • Inflation will remain subdued • Interest rates will stay lower for longer • Technology-driven progress and persistent supply-side divergence will create investment risks and opportunities in equity markets In the investment world, economic growth is a big deal. We believe investment returns across asset classes can ultimately be traced back to one source: economic growth. Occasionally, asset prices can deviate from fundamentals, but over the long term, the relationship between returns and growth is very strong. That’s why it is critical to have a better understanding of the low growth phenomenon and key contributing factors, such as productivity. -

A Primer on Profit Maximization

Central Washington University ScholarWorks@CWU All Faculty Scholarship for the College of Business College of Business Fall 2011 A Primer on Profit aM ximization Robert Carbaugh Central Washington University, [email protected] Tyler Prante Los Angeles Valley College Follow this and additional works at: http://digitalcommons.cwu.edu/cobfac Part of the Economic Theory Commons, and the Higher Education Commons Recommended Citation Carbaugh, Robert and Tyler Prante. (2011). A primer on profit am ximization. Journal for Economic Educators, 11(2), 34-45. This Article is brought to you for free and open access by the College of Business at ScholarWorks@CWU. It has been accepted for inclusion in All Faculty Scholarship for the College of Business by an authorized administrator of ScholarWorks@CWU. 34 JOURNAL FOR ECONOMIC EDUCATORS, 11(2), FALL 2011 A PRIMER ON PROFIT MAXIMIZATION Robert Carbaugh1 and Tyler Prante2 Abstract Although textbooks in intermediate microeconomics and managerial economics discuss the first- order condition for profit maximization (marginal revenue equals marginal cost) for pure competition and monopoly, they tend to ignore the second-order condition (marginal cost cuts marginal revenue from below). Mathematical economics textbooks also tend to provide only tangential treatment of the necessary and sufficient conditions for profit maximization. This paper fills the void in the textbook literature by combining mathematical and graphical analysis to more fully explain the profit maximizing hypothesis under a variety of market structures and cost conditions. It is intended to be a useful primer for all students taking intermediate level courses in microeconomics, managerial economics, and mathematical economics. It also will be helpful for students in Master’s and Ph.D. -

Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets

Managerial Economics & Business Strategy Chapter 8 Managing in Competitive, Monopolistic, and Monopolistically Competitive Markets McGraw-Hill/Irwin Copyright © 2010 by the McGraw-Hill Companies, Inc. All rights reserved. Overview I. Perfect Competition – Characteristics and profit outlook. – Effect of new entrants. II. Monopolies – Sources of monopoly power. – Maximizing monopoly profits. – Pros and cons. III. Monopolistic Competition – Profit maximization. – Long run equilibrium. 8-2 Perfect Competition Environment Many buyers and sellers. Homogeneous (identical) product. Perfect information on both sides of market. No transaction costs. Free entry and exit. 8-3 Key Implications Firms are “price takers” (P = MR). In the short-run, firms may earn profits or losses. Entry and exit forces long-run profits to zero. 8-4 Unrealistic? Why Learn? Many small businesses are “price-takers,” and decision rules for such firms are similar to those of perfectly competitive firms. It is a useful benchmark. Explains why governments oppose monopolies. Illuminates the “danger” to managers of competitive environments. – Importance of product differentiation. – Sustainable advantage. 8-5 Managing a Perfectly Competitive Firm (or Price-Taking Business) 8-6 Setting Price $ $ S Pe Df D QM Qf Market Firm 8-7 Profit-Maximizing Output Decision MR = MC. Since, MR = P, Set P = MC to maximize profits. 8-8 Graphically: Representative Firm’s Output Decision Profit = ( Pe - ATC ) × Qf* MC $ ATC AVC Pe Pe = Df = MR ATC Qf* Qf 8-9 A Numerical Example Given – P=$10 – C(Q) = 5 + Q 2 Optimal Price? – P=$10 Optimal Output? – MR = P = $10 and MC = 2Q – 10 = 2Q – Q = 5 units Maximum Profits? – PQ - C(Q) = (10)(5) - (5 + 25) = $20 8-10 Should this Firm Sustain Short Run Losses or Shut Down? Profit = ( Pe - ATC ) × Qf* < 0 MC ATC $ AVC ATC Loss Pe Pe = Df = MR f Qf* Q 8-11 Shutdown Decision Rule A profit-maximizing firm should continue to operate (sustain short-run losses) if its operating loss is less than its fixed costs . -

Report No. 2020-06 Economies of Scale in Community Banks

Federal Deposit Insurance Corporation Staff Studies Report No. 2020-06 Economies of Scale in Community Banks December 2020 Staff Studies Staff www.fdic.gov/cfr • @FDICgov • #FDICCFR • #FDICResearch Economies of Scale in Community Banks Stefan Jacewitz, Troy Kravitz, and George Shoukry December 2020 Abstract: Using financial and supervisory data from the past 20 years, we show that scale economies in community banks with less than $10 billion in assets emerged during the run-up to the 2008 financial crisis due to declines in interest expenses and provisions for losses on loans and leases at larger banks. The financial crisis temporarily interrupted this trend and costs increased industry-wide, but a generally more cost-efficient industry re-emerged, returning in recent years to pre-crisis trends. We estimate that from 2000 to 2019, the cost-minimizing size of a bank’s loan portfolio rose from approximately $350 million to $3.3 billion. Though descriptive, our results suggest efficiency gains accrue early as a bank grows from $10 million in loans to $3.3 billion, with 90 percent of the potential efficiency gains occurring by $300 million. JEL classification: G21, G28, L00. The views expressed are those of the authors and do not necessarily reflect the official positions of the Federal Deposit Insurance Corporation or the United States. FDIC Staff Studies can be cited without additional permission. The authors wish to thank Noam Weintraub for research assistance and seminar participants for helpful comments. Federal Deposit Insurance Corporation, [email protected], 550 17th St. NW, Washington, DC 20429 Federal Deposit Insurance Corporation, [email protected], 550 17th St. -

Working Paper No

Department of Economics Natural or Unnatural Monopolies in UK Telecommunications? Lisa Correa Working Paper No. 501 September 2003 ISSN 1473-0278 Natural or Unnatural Monopolies In UK ∗ Telecommunications? ≅ Lisa Correa September 2003 ABSTRACT This paper analyses whether scale economies exists in the UK telecommunications industry. The approach employed differs from other UK studies in that panel data for a range of companies is used. This increases the number of observations and thus allows potentially for more robust tests for global subadditivity of the cost function. The main findings from the study reveal that although the results need to be treated with some caution allowing/encouraging infrastructure competition in the local loop may result in substantial cost savings. JEL Classification Numbers: D42, L11, L12, L51, L96, Keywords: Telecommunications, Regulation, Monopoly, Cost Functions, Scale Economies, Subadditivity ∗ The author is indebted to Richard Allard and Paul Belleflamme for their encouragement and advice. She would however also like to thank Richard Green and Leonard Waverman for their insightful comments and recommendations on an earlier version of this paper. All views expressed in the paper and any remaining errors are solely the responsibility of the author. ≅ Department of Economics, Queen Mary, University of London (UK). Preferred e- mail address for comments is [email protected] 1 Natural or Unnatural Monopolies in U.K. Telecommunications? 1. Introduction The UK has historically pursued a policy of infrastructure or local loop competition in the telecommunications market with the aim of delivering dynamic competition, the key focus of which is innovation. Recently, however, Directives from Europe have been issued which could be argued discourages competition in the local loop.