Partnership with Tencent on Payments Has Limited Earnings Impact

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

FIDELITY SALEM STREET TRUST Form NPORT-P Filed 2021-03-17

SECURITIES AND EXCHANGE COMMISSION FORM NPORT-P Filing Date: 2021-03-17 | Period of Report: 2021-01-31 SEC Accession No. 0001752724-21-055741 (HTML Version on secdatabase.com) FILER FIDELITY SALEM STREET TRUST Mailing Address Business Address 245 SUMMER STREET 245 SUMMER STREET CIK:35315| IRS No.: 000000000 | State of Incorp.:MA | Fiscal Year End: 0430 BOSTON MA 02210 BOSTON MA 02210 Type: NPORT-P | Act: 40 | File No.: 811-02105 | Film No.: 21749300 617-563-7000 Copyright © 2021 www.secdatabase.com. All Rights Reserved. Please Consider the Environment Before Printing This Document Quarterly Holdings Report for Fidelity® SAI Emerging Markets Low Volatility Index Fund January 31, 2021 Offered exclusively to certain clients of the Adviser or its affiliates - not available for sale to the general public. Fidelity SAI is a product name of Fidelity® funds dedicated to certain programs affiliated with Strategic Advisers LLC. MLV-QTLY-0321 1.9892172.102 Schedule of Investments January 31, 2021 (Unaudited) Showing Percentage of Net Assets Common Stocks - 99.3% Shares Value Bailiwick of Jersey - 0.6% WNS Holdings Ltd. sponsored ADR (a) 133,901 $8,995,469 Bermuda - 1.3% China Resource Gas Group Ltd. 2,526,000 12,640,996 Shenzhen International Holdings Ltd. 3,307,714 5,452,241 TOTAL BERMUDA 18,093,237 Brazil - 0.2% Atacadao SA 902,600 3,140,970 Cayman Islands - 17.1% Anta Sports Products Ltd. 1,584,000 26,211,872 Bosideng International Holdings Ltd. 9,214,000 4,088,113 China Biologic Products Holdings, Inc. (a) 33,383 3,934,187 Hansoh Pharmaceutical Group Co. -

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016

STOXX Hong Kong All Shares 50 Last Updated: 01.12.2016 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 128.4 1 1 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 69.3 2 2 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 60.3 3 4 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 57.5 4 3 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 37.7 5 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 32.6 6 7 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 32.0 7 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 28.5 8 8 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 26.5 9 9 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 20.4 10 15 HK0016000132 6859927 0016.HK 685992 Sun Hung Kai Properties Ltd. HK HKD Y 19.4 11 10 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 18.9 12 12 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 18.3 13 13 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 17.9 14 11 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 16.8 15 14 HK0688002218 6192150 0688.HK 619215 China Overseas Land & Investme CN HKD Y 14.8 16 16 HK0823032773 B0PB4M7 0823.HK B0PB4M Link Real Estate Investment Tr HK HKD Y 14.6 17 17 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 13.5 18 19 HK0003000038 6436557 0003.HK 643655 Hong Kong & China Gas Co. -

Morgan Stanley's Top-Performing Fund Buys Undervalued Stocks

January 19, 2020 | bloomberg.com Photographer: Michael Nagle/Bloomberg Markets Morgan Stanley’s Top-Performing Fund Buys Undervalued Stocks by Ishika Mookerjee January 19, 2020 ▶ Consumer stocks are a focus; more than half of assets in China ▶ Meituan, Moutai among drivers of fund’s 44% gain in past year A top-performing Morgan Stanley fund remain a key focus this year despite its invested capital and 15% revenue growth is betting on cash-rich consumption- slower growth in 2019. over the past three years, he added. The focused stocks in Asia, especially China, to Asian consumer stocks provide “high MSCI Asia ex Japan Index has gained 3.4% manage risks in market cycles this year. returns on capital, low leverage and so far this year. The Wall Street firm’s Asia Opportunity quality growth prospects,” Hong Kong- With more than 800 million people Portfolio, which focuses on equities in based Heugh said. The region offers “the emerging from poverty since market the region excluding Japan, returned 44% highest ratio” of high-quality companies reforms began in 1978, China is an in the past year, beating 99% of its peers, that have generated both 15% return on especially attractive hunting ground for according to data compiled by Bloomberg. The portfolio focuses on undervalued companies with low debt or net cash on their balance sheets, many of which are found in consumer sectors, said Kristian Heugh, who has been co-managing the fund since its inception in 2016. “We seek to protect investors’ capital by focusing on high quality companies with sustainable competitive advantages and purchasing them at a discount to our estimate of intrinsic value,” Heugh said. -

Hang Seng Indexes Announces Index Review Results

14 August 2020 Hang Seng Indexes Announces Index Review Results Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 30 June 2020. All changes will take effect on 7 September 2020 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents remains unchanged at 50. Inclusion: Code Company 1810 Xiaomi Corporation - W 2269 WuXi Biologics (Cayman) Inc. 9988 Alibaba Group Holding Ltd. - SW Removal: Code Company 83 Sino Land Co. Ltd. 151 Want Want China Holdings Ltd. 1088 China Shenhua Energy Co. Ltd. - H Shares The list of constituents is provided in Appendix 1. The Hang Seng Index Advisory Committee today reviewed the fast expanding innovation and new economy sectors in the Hong Kong capital market and agreed with the proposal from Hang Seng Indexes to conduct a comprehensive study on the composition of the Hang Seng Index. This holistic review will encompass various aspects including, but not limited to, composition and selection of constituents, number of constituents, weightings, and industry and geographical representation, etc. The underlying aim of the study is to ensure the Hang Seng Index continues to serve as the most representative and important benchmark of the Hong Kong stock market. Hang Seng Indexes will report its findings and propose recommendations to the Advisory Committee within six months. The number of constituents of the Hang Seng Index may increase during this period. Hang Seng Indexes Announces Index Review Results /2 2. -

Schedule of Investments (Unaudited) Ishares MSCI Total International Index Fund (Percentages Shown Are Based on Net Assets) September 30, 2020

Schedule of Investments (unaudited) iShares MSCI Total International Index Fund (Percentages shown are based on Net Assets) September 30, 2020 Mutual Fund Value Total International ex U.S. Index Master Portfolio of Master Investment Portfolio $ 1,034,086,323 Total Investments — 100.4% (Cost: $929,170,670) 1,034,086,323 Liabilities in Excess of Other Assets — (0.4)% (3,643,126) Net Assets — 100.0% $ 1,030,443,197 iShares MSCI Total International Index Fund (the “Fund”) seeks to achieve its investment objective by investing all of its assets in International Tilts Master Portfolio (the “Master Portfolio”), which has the same investment objective and strategies as the Fund. As of September 30, 2020, the value of the investment and the percentage owned by the Fund of the Master Portfolio was $1,034,086,323 and 99.9%, respectively. The Fund records its investment in the Master Portfolio at fair value. The Fund’s investment in the Master Portfolio is valued pursuant to the pricing policies approved by the Board of Directors of the Master Portfolio. Fair Value Hierarchy as of Period End Various inputs are used in determining the fair value of financial instruments. These inputs to valuation techniques are categorized into a fair value hierarchy consisting of three broad levels for financial reporting purposes as follows: • Level 1 – Unadjusted price quotations in active markets/exchanges for identical assets or liabilities that the Fund has the ability to access • Level 2 – Other observable inputs (including, but not limited to, quoted prices -

Hang Seng Indexes Announces Index Review Results

25 February 2016 HANG SENG INDEXES ANNOUNCES INDEX REVIEW RESULTS Hang Seng Indexes Company Limited (“Hang Seng Indexes”) today announced the results of its review of the Hang Seng Family of Indexes for the quarter ended 31 December 2015. All changes will be effective on 14 March 2016 (Monday). 1. Hang Seng Index The following constituent changes will be made to the Hang Seng Index. The total number of constituents is fixed at 50. Inclusion: Code Company FAF (%) Sub-Index Cheung Kong Infrastructure 1038 25 Utilities Holdings Ltd. Removal: Code Company FAF (%) Sub-Index China Resources Beer 291 50 Commerce & Industry (Holdings) Co. Ltd. The list of constituents is provided in Appendix 1. 2. Hang Seng China Enterprises Index There is no change to the constituents of the Hang Seng China Enterprises Index. The total number of constituents is fixed at 40. The list of constituents is provided in Appendix 2. 3. Hang Seng Composite LargeCap & MidCap Index The following constituent changes will be made to the Hang Seng Composite LargeCap & MidCap Index. The total number of constituents will increase from 280 to 299. more… HANG SENG INDEXES ANNOUNCES INDEX REVIEW RESULTS/ 2 Inclusion: Code Company 10 Hang Lung Group Ltd. 109 Good Resources Holdings Ltd. 136 HengTen Networks Group Ltd. 400 Cogobuy Group 405 Yuexiu Real Estate Investment Trust 607 Fullshare Holdings Ltd. 715 China Oceanwide Holdings Ltd. 911 Hang Fat Ginseng Holdings Co. Ltd. 958 Huaneng Renewables Corporation Ltd. - H Shares 1071 Huadian Power International Corporation Ltd. - H Shares 1282 China Goldjoy Group Ltd. 1308 SITC International Holdings Co. -

STOXX Hong Kong All Shares 50 Last Updated: 01.10.2015

STOXX Hong Kong All Shares 50 Last Updated: 01.10.2015 Rank Rank (PREVIOUS ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) ) KYG875721634 BMMV2K8 0700.HK B01CT3 Tencent Holdings Ltd. CN HKD Y 79.6 1 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 59.3 2 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 55.8 3 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 49.6 4 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 36.3 5 CNE1000001Z5 B154564 3988.HK CN0032 BANK OF CHINA 'H' CN HKD Y 29.3 6 HK0388045442 6267359 0388.HK 626735 Hong Kong Exchanges & Clearing HK HKD Y 23.2 7 CNE1000002L3 6718976 2628.HK CN0043 China Life Insurance Co 'H' CN HKD Y 23.1 8 CNE1000003X6 B01FLR7 2318.HK CN0076 PING AN INSUR GP CO. OF CN 'H' CN HKD Y 22.6 9 KYG217651051 BW9P816 0001.HK 619027 CK HUTCHISON HOLDINGS HK HKD Y 18.5 10 KYG2103F1019 BWX52N2 1113.HK HK50CI CK Property Holdings HK HKD Y 18.3 11 HK0004000045 6435576 0004.HK 643557 Wharf (Holdings) Ltd. HK HKD Y 15.2 12 HK0883013259 B00G0S5 0883.HK 617994 CNOOC Ltd. CN HKD Y 14.6 13 CNE1000002Q2 6291819 0386.HK CN0098 China Petroleum & Chemical 'H' CN HKD Y 13.9 14 CNE1000003W8 6226576 0857.HK CN0065 PetroChina Co Ltd 'H' CN HKD Y 13.1 15 HK0002007356 6097017 0002.HK 619091 CLP Holdings Ltd. HK HKD Y 11.7 16 HK0011000095 6408374 0011.HK 640837 Hang Seng Bank Ltd. -

Xiaomi Sews up Deals for Smart Homes

16 BUSINESS Thursday, November 29, 2018 CHINA DAILY HONG KONG EDITION Xiaomi sews Shenzhen firms hike investment up deals for in R&D sector By ZHOU MO in Shenzhen, Guangdong smart homes [email protected] 20 percent of Shenzhenregistered list Tech tieups with Ikea, Microsoft and Nearly 20 percent of ed companies devoted more Shenzhenregistered listed than 10 percent of their iKongjian ‘to create better life for people’ companies devoted more operating revenue to R&D than 10 percent of their oper By OUYANG SHIJIA shortly after Ikea, the world’s ating revenue to research ouyangshijia@ largest furniture retailer, said and development last year, a chinadaily.com.cn last week that it would acceler level on par with globally ate its transformation to fully leading hightech enterpris the sector that took the lead. Chinese technology giant embrace new technologies and es like Google and Apple, Of the 10 listed companies Xiaomi Corp announced on offer better user experiences. according to a report. with the biggest R&D invest Wednesday it has teamed up Bjorn Block, business leader In all, 256 companies cov ment, eight were IT compa with Sweden’s furniture titan for Ikea’s Home Smart divi Lei Jun, founder and CEO of Xiaomi Corp, delivers a speech on Wednesday during the MIDC Xiaomi ered in the Shenzhenregis nies. Ikea to offer smart home prod sion, told during the confer AIoT Developer Conference in Beijing. PROVIDED TO CHINA DAILY tered Listed Companies The R&D investment of ucts. ence that the new partnership Development Report dis Tencent Holdings Ltd, the The tieup is part of its larg marked a key step in creating a closed their R&D spending world’s largest game maker er efforts to expand into the seamless experience for cus partnership would benefit home renovation service plat in their 2017 annual reports. -

Greater China 2019

IR Magazine Awards – Greater China 2019 Winners and nominees AWARDS BY RESEARCH Best overall investor relations (large cap) ANTA Sports Products China Resources Beer WINNER China Telecom China Unicom Shenzhou International Group Holdings Best overall investor relations (small to mid-cap) Alibaba Pictures Group Far East Consortium International WINNER Health and Happiness H&H International Holdings Li-Ning NetDragon Websoft Holdings Best investor relations officer (large cap) ANTA Sports Products Suki Wong Cathay Financial Holdings Yajou Chang & Sophia Cheng China Resources Beer Vincent Tse WINNER China Telecom Lisa Lai China Unicom Jacky Yung Best investor relations officer (small to mid-cap) Agile Group Holdings Samson Chan BizLink Holding Tom Huang Far East Consortium International Venus Zhao WINNER Li-Ning Rebecca Zhang Yue Yuen Industrial (Holdings) Olivia Wang Best IR by a senior management team Maggie Wu, CFO & Daniel Zhang, Alibaba Group CEO Tomakin Lai Po-sing, CFO & China Resources Beer Xiaohai Hou, CEO Xiaochu Wang, CEO & Zhu WINNER China Unicom Kebing, CFO Wai Hung Boswell Cheung, CFO & Far East Consortium International David Chiu, Chairman & CEO Ma Jianrong, CEO & Cun Bo Wang, Shenzhou International Group Holdings CFO AWARDS BY REGION Best in region: China Alibaba Pictures Group ANTA Sports Products China Resources Beer WINNER China Telecom China Unicom Shenzhou International Group Holdings Best in region: Hong Kong AIA Group Far East Consortium International WINNER Health and Happiness H&H International Holdings Yue Yuen -

2016 Annual Report (PDF)

Table of Contents 2 Corporate Information 3 CEO’s Statement 6 Management Discussion and Analysis 23 Biographies of Directors and Senior Management 27 Corporate Governance Report 39 Report of the Directors 59 Independent Auditor’s Report 64 Consolidated Statement of Profit or Loss and Other Comprehensive Income 65 Consolidated Statement of Financial Position 67 Consolidated Statement of Changes in Equity 68 Consolidated Statement of Cash Flows 70 Notes to the Consolidated Financial Statements 166 Five-year Financial Summary Corporate Information BOARD OF DIRECTORS REGISTERED OFFICE Executive Directors Maples Corporate Services Limited PO Box 309 Ms. GAO Lina (Deputy Chairman and Chief Executive Officer) Ugland House Mr. HAN Chunlin (Chief Operation Officer) Grand Cayman, KY1-1104, Cayman Islands Non-Executive Directors HONG KONG OFFICE Mr. YU Xubo (Chairman) Unit 2402, 24/F, Mr. WOLHARDT Julian Juul Alliance Building 130-136 Mr. HUI Chi Kin, Max Connaught Road Central Sheung Wan Mr. ZHANG Ping Hong Kong Mr. SUN Yugang PRINCIPAL SHARE REGISTRAR AND Independent Non-Executive Directors TRANSFER OFFICE Mr. LI Shengli Maples Finance Limited Mr. LEE Kong Wai, Conway PO Box 1093, Mr. KANG Yan Queensgate House Mr. ZOU Fei Grand Cayman, KY1-1102 Cayman Islands AUDIT COMMITTEE HONG KONG BRANCH SHARE REGISTRAR Mr. LEE Kong Wai, Conway (Chairman) AND TRANSFER OFFICE Mr. HUI Chi Kin, Max Mr. ZOU Fei Computershare Hong Kong Investor Services Limited Rooms 1712-1716, 17/F, Hopewell Centre REMUNERATION COMMITTEE 183 Queen’s Road East Wanchai Hong Kong Mr. LI Shengli (Chairman) Mr. WOLHARDT Julian Juul LEGAL ADVISORS Mr. ZOU Fei NOMINATION COMMITTEE As to Hong Kong Law Mr. -

Schedule of Investments (Unaudited) Blackrock Advantage Emerging Markets Fund January 31, 2021 (Percentages Shown Are Based on Net Assets)

Schedule of Investments (unaudited) BlackRock Advantage Emerging Markets Fund January 31, 2021 (Percentages shown are based on Net Assets) Security Shares Value Security Shares Value Common Stocks China (continued) China Life Insurance Co. Ltd., Class H .................. 221,000 $ 469,352 Argentina — 0.0% China Longyuan Power Group Corp. Ltd., Class H ....... 52,000 76,119 (a) 313 $ 60,096 Globant SA .......................................... China Mengniu Dairy Co. Ltd.(a) ......................... 15,000 89,204 Brazil — 4.9% China Merchants Bank Co. Ltd., Class H ................ 36,000 275,683 Ambev SA ............................................. 236,473 653,052 China Overseas Land & Investment Ltd.................. 66,500 151,059 Ambev SA, ADR ....................................... 94,305 263,111 China Pacific Insurance Group Co. Ltd., Class H......... 22,000 90,613 B2W Cia Digital(a) ...................................... 20,949 315,188 China Railway Group Ltd., Class A ...................... 168,800 138,225 B3 SA - Brasil Bolsa Balcao............................. 33,643 367,703 China Resources Gas Group Ltd. ....................... 30,000 149,433 Banco do Brasil SA..................................... 15,200 94,066 China Resources Land Ltd. ............................. 34,000 134,543 BRF SA(a).............................................. 22,103 85,723 China Resources Pharmaceutical Group Ltd.(b) .......... 119,500 62,753 BRF SA, ADR(a) ........................................ 54,210 213,045 China Vanke Co. Ltd., Class A .......................... 67,300 289,157 Cia de Saneamento de Minas Gerais-COPASA .......... 52,947 150,091 China Vanke Co. Ltd., Class H .......................... 47,600 170,306 Duratex SA ............................................ 19,771 71,801 CITIC Ltd............................................... 239,000 186,055 Embraer SA(a).......................................... 56,573 90,887 Contemporary Amperex Technology Co. Ltd., Class A .... 1,700 92,204 Gerdau SA, ADR ...................................... -

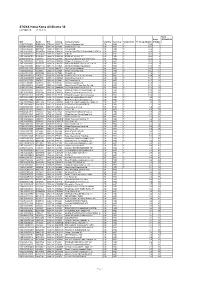

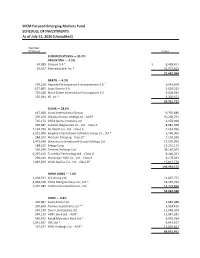

WCM Focused Emerging Markets Fund SCHEDULE of INVESTMENTS As of July 31, 2020 (Unaudited)

WCM Focused Emerging Markets Fund SCHEDULE OF INVESTMENTS As of July 31, 2020 (Unaudited) Number of Shares Value COMMON STOCKS — 91.0% ARGENTINA — 4.5% 49,089 Globant S.A.* $ 8,489,451 20,427 MercadoLibre, Inc.* 22,972,613 31,462,064 BRAZIL — 4.3% 724,230 Hapvida Participacoes e Investimentos S.A.1 9,043,504 637,865 Lojas Renner S.A. 5,029,212 735,180 Notre Dame Intermedica Participacoes S.A. 9,408,545 135,494 XP, Inc.* 6,300,471 29,781,732 CHINA — 28.6% 467,060 Airtac International Group 9,797,686 200,258 Alibaba Group Holding Ltd. - ADR* 50,268,763 735,174 ANTA Sports Products Ltd. 6,978,998 346,687 Autobio Diagnostics Co., Ltd. - Class A 8,082,568 2,134,296 By-health Co., Ltd. - Class A 7,654,996 3,532,000 Kingdee International Software Group Co., Ltd.* 9,768,906 288,105 Meituan Dianping - Class B* 7,129,590 1,473,420 Shenzhou International Group Holdings Ltd. 17,599,596 188,215 Silergy Corp. 11,291,122 556,290 Tencent Holdings Ltd. 38,160,505 4,297,415 TravelSky Technology Ltd. - Class H 8,266,021 294,444 Wuliangye Yibin Co., Ltd. - Class A 9,178,043 1,049,069 WuXi AppTec Co., Ltd. - Class H1 15,817,778 199,994,572 HONG KONG — 7.8% 2,418,531 AIA Group Ltd. 21,807,752 3,869,330 China Mengniu Dairy Co., Ltd.* 18,156,740 1,407,385 Techtronic Industries Co., Ltd. 14,719,896 54,684,388 INDIA — 9.8% 204,687 Asian Paints Ltd.