GAMING GLOBAL a Report for British Council Nick Webber and Paul Long with Assistance from Oliver Williams and Jerome Turner

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Management Board REPORT on the CI GAMES S.A. Capital Group Activities 2018

Management Board REPORT on the CI GAMES S.A. Capital Group activities 2018 WARSAW, 3/28/2019 Dear Shareholders! Since the beginning of 2018, the whole CI Games Group has been undergoing significant changes that are the result of adoption and implementation of a strategy announced in June 2017, updated in December 2018, within which: • We significantly decreased the internal production studio of CI Games. The team previously composed of 100 persons now comprises of 30 experts. In majority, these are employees with many years of experience concerning production of shooter type games. • We established a strong 7-person team managing the Group, responsible for the implementation of the new strategy. The team is in majority composed of managers experienced in the field of video games. • Our internal studio is currently working on the next game of the SGW series – “Sniper Ghost Warrior Contracts” – this is being done with a significant support of external production studios contributing in the area of design, graphics and code. The game will be made available for consoles and PC in 2019. The Company has signed first distribution agreements for key territories such as Great Britain, France, Australia and Scandinavia, under which the distribution of “Sniper Ghost Warrior Contracts” will be carried out. • The result of careful selection of Partners is the cooperation started in June 2018 with high-end developer studio from New York, Defiant Studios, which is responsible for the production of “Lords of the Fallen 2” for consoles and PCs. Current works on “Lords of the Fallen 2” are progressing in line with the objectives set by the parties. -

The Poetics of Reflection in Digital Games

© Copyright 2019 Terrence E. Schenold The Poetics of Reflection in Digital Games Terrence E. Schenold A dissertation submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy University of Washington 2019 Reading Committee: Brian M. Reed, Chair Leroy F. Searle Phillip S. Thurtle Program Authorized to Offer Degree: English University of Washington Abstract The Poetics of Reflection in Digital Games Terrence E. Schenold Chair of the Supervisory Committee: Brian Reed, Professor English The Poetics of Reflection in Digital Games explores the complex relationship between digital games and the activity of reflection in the context of the contemporary media ecology. The general aim of the project is to create a critical perspective on digital games that recovers aesthetic concerns for game studies, thereby enabling new discussions of their significance as mediations of thought and perception. The arguments advanced about digital games draw on philosophical aesthetics, media theory, and game studies to develop a critical perspective on gameplay as an aesthetic experience, enabling analysis of how particular games strategically educe and organize reflective modes of thought and perception by design, and do so for the purposes of generating meaning and supporting expressive or artistic goals beyond amusement. The project also provides critical discussion of two important contexts relevant to understanding the significance of this poetic strategy in the field of digital games: the dynamics of the contemporary media ecology, and the technological and cultural forces informing game design thinking in the ludic century. The project begins with a critique of limiting conceptions of gameplay in game studies grounded in a close reading of Bethesda's Morrowind, arguing for a new a "phaneroscopical perspective" that accounts for the significance of a "noematic" layer in the gameplay experience that accounts for dynamics of player reflection on diegetic information and its integral relation to ergodic activity. -

L'expérience De Création De Jeux Vidéo En Amateur Travailler Son

Université de Liège Faculté de Philosophie et Lettres Département Médias, Culture et Communication L’expérience de création de jeux vidéo en amateur Travailler son goût pour l’incertitude Thèse présentée par Pierre-Yves Hurel en vue de l’obtention du titre de Docteur en Information et Communication sous la direction de Christine Servais Année académique 2019-2020 À Anne-Lyse, à notre aventure, à nos traversées, à nos horizons. À Charlotte, à tes cris de l’oie, à tes sourires en coin, à tes découvertes. REMERCIEMENTS Écrire une thèse est un acte pétri d’incertitudes, que l’auteur cherche à maîtriser, cadrer et contrôler. J’ai eu le bonheur d’être particulièrement bien accompagné dans cette pratique du doute. Seul face à mon document, j’étais riche de toutes les discussions qui ont jalonné mes années de doctorat. Je souhaite particulièrement remercier mes interlocuteurs pour leur générosité : - Christine Servais, pour sa direction minutieuse, sa franchise, sa bienveillance, ses conseils et son écoute. - Les membres du jury pour avoir accepté de me livrer leur analyse du présent travail. - Tous les membres du Liège Game Lab pour leur intelligence dans leur participation à notre collectif de recherche, pour leur capacité à échanger de manière constructive et pour leur humour sans égal. Merci au Docteure Barnabé (chercheuse internationale et coauteure de cafés-thèse fondateurs), au Docteure Delbouille (brillante sitôt qu’on l’entend), au Docteur Dupont (titulaire d’un double doctorat en lettres modernes et en élégance), au Docteur Dozo (dont le sens du collectif a tant permis), au futur Docteur Krywicki (prolifique en tout domaine), au futur Docteur Houlmont (dont je ne connais qu’un défaut) et au futur Docteur Bashandy (dont le vécu et les travaux incitent à l’humilité). -

Achieve Your Vision

ACHIEVE YOUR VISION NE XT GEN ready CryENGINE® 3 The Maximum Game Development Solution CryENGINE® 3 is the first Xbox 360™, PlayStation® 3, MMO, DX9 and DX10 all-in-one game development solution that is next-gen ready – with scalable computation and graphics technologies. With CryENGINE® 3 you can start the development of your next generation games today. CryENGINE® 3 is the only solution that provides multi-award winning graphics, physics and AI out of the box. The complete game engine suite includes the famous CryENGINE® 3 Sandbox™ editor, a production-proven, 3rd generation tool suite designed and built by AAA developers. CryENGINE® 3 delivers everything you need to create your AAA games. NEXT GEN ready INTEGRATED CryENGINE® 3 SANDBOX™ EDITOR CryENGINE® 3 Sandbox™ Simultaneous WYSIWYP on all Platforms CryENGINE® 3 SandboxTM now enables real-time editing of multi-platform game environments; simul- The Ultimate Game Creation Toolset taneously making changes across platforms from CryENGINE® 3 SandboxTM running on PC, without loading or baking delays. The ability to edit anything within the integrated CryENGINE® 3 SandboxTM CryENGINE® 3 Sandbox™ gives developers full control over their multi-platform and simultaneously play on multiple platforms vastly reduces the time to build compelling content creations in real-time. It features many improved efficiency tools to enable the for cross-platform products. fastest development of game environments and game-play available on PC, ® ® PlayStation 3 and Xbox 360™. All features of CryENGINE 3 games (without CryENGINE® 3 Sandbox™ exception) can be produced and played immediately with Crytek’s “What You See Is What You Play” (WYSIWYP) system! CryENGINE® 3 Sandbox™ was introduced in 2001 as the world’s first editor featuring WYSIWYP technology. -

UPDATE NEW GAME !!! the Incredible Adventures of Van Helsing + Update 1.1.08 Jack Keane 2: the Fire Within Legends of Dawn Pro E

UPDATE NEW GAME !!! The Incredible Adventures of Van Helsing + Update 1.1.08 Jack Keane 2: The Fire Within Legends of Dawn Pro Evolution Soccer 2013 Patch PESEdit.com 4.1 Endless Space: Disharmony + Update v1.1.1 The Curse of Nordic Cove Magic The Gathering Duels of the Planeswalkers 2014 Leisure Suit Larry: Reloaded Company of Heroes 2 + Update v3.0.0.9704 Incl DLC Thunder Wolves + Update 1 Ride to Hell: Retribution Aeon Command The Sims 3: Island Paradise Deadpool Machines at War 3 Stealth Bastard GRID 2 + Update v1.0.82.8704 Pinball FX2 + Update Build 210613 incl DLC Call of Juarez: Gunslinger + Update v1.03 Worms Revolution + Update 7 incl. Customization Pack DLC Dungeons & Dragons: Chronicles of Mystara Magrunner Dark Pulse MotoGP 2013 The First Templar: Steam Special Edition God Mode + Update 2 DayZ Standalone Pre Alpha Dracula 4: The Shadow of the Dragon Jagged Alliance Collectors Bundle Police Force 2 Shadows on the Vatican: Act 1 -Greed SimCity 2013 + Update 1.5 Hairy Tales Private Infiltrator Rooks Keep Teddy Floppy Ear Kayaking Chompy Chomp Chomp Axe And Fate Rebirth Wyv and Keep Pro Evolution Soccer 2013 Patch PESEdit.com 4.0 Remember Me + Update v1.0.2 Grand Ages: Rome - Gold Edition Don't Starve + Update June 11th Mass Effect 3: Ultimate Collectors Edition APOX Derrick the Deathfin XCOM: Enemy Unknown + Update 4 Hearts of Iron III Collection Serious Sam: Classic The First Encounter Castle Dracula Farm Machines Championships 2013 Paranormal Metro: Last Light + Update 4 Anomaly 2 + Update 1 and 2 Trine 2: Complete Story ZDSimulator -

It's Meant to Be Played

Issue 10 $3.99 (where sold) THE WAY It’s meant to be played Ultimate PC Gaming with GeForce All the best holiday games with the power of NVIDIA Far Cry’s creators outclass its already jaw-dropping technology Battlefi eld 2142 with an epic new sci-fi battle World of Warcraft: Company of Heroes Warhammer: The Burning Crusade Mark of Chaos THE NEWS Notebooks are set to transform Welcome... PC gaming Welcome to the 10th issue of The Way It’s Meant To Be Played, the he latest must-have gaming system is… T magazine dedicated to the very best in a notebook PC. Until recently considered mainly PC gaming. In this issue, we showcase a means for working on the move or for portable 30 games, all participants in NVIDIA’s presentations, laptops complete with dedicated graphic The Way It’s Meant To Be Played processing units (GPUs) such as the NVIDIA® GeForce® program. In this program, NVIDIA’s Go 7 series are making a real impact in the gaming world. Latest thing: Laptops developer technology engineers work complete with dedicated The advantages are obvious – gamers need no longer be graphic processing units with development teams to get the are making an impact in very best graphics and effects into tied to their desktop set-up. the gaming world. their new titles. The games are then The new NVIDIA® GeForce® Go 7900 notebook rigorously tested by three different labs GPUs are designed for extreme HD gaming, and gaming at NVIDIA for compatibility, stability, and hardware specialists such as Alienware and Asus have performance to ensure that any game seen the potential of the portable platform. -

The Otaku Phenomenon : Pop Culture, Fandom, and Religiosity in Contemporary Japan

University of Louisville ThinkIR: The University of Louisville's Institutional Repository Electronic Theses and Dissertations 12-2017 The otaku phenomenon : pop culture, fandom, and religiosity in contemporary Japan. Kendra Nicole Sheehan University of Louisville Follow this and additional works at: https://ir.library.louisville.edu/etd Part of the Comparative Methodologies and Theories Commons, Japanese Studies Commons, and the Other Religion Commons Recommended Citation Sheehan, Kendra Nicole, "The otaku phenomenon : pop culture, fandom, and religiosity in contemporary Japan." (2017). Electronic Theses and Dissertations. Paper 2850. https://doi.org/10.18297/etd/2850 This Doctoral Dissertation is brought to you for free and open access by ThinkIR: The University of Louisville's Institutional Repository. It has been accepted for inclusion in Electronic Theses and Dissertations by an authorized administrator of ThinkIR: The University of Louisville's Institutional Repository. This title appears here courtesy of the author, who has retained all other copyrights. For more information, please contact [email protected]. THE OTAKU PHENOMENON: POP CULTURE, FANDOM, AND RELIGIOSITY IN CONTEMPORARY JAPAN By Kendra Nicole Sheehan B.A., University of Louisville, 2010 M.A., University of Louisville, 2012 A Dissertation Submitted to the Faculty of the College of Arts and Sciences of the University of Louisville in Partial Fulfillment of the Requirements for the Degree of Doctor of Philosophy in Humanities Department of Humanities University of Louisville Louisville, Kentucky December 2017 Copyright 2017 by Kendra Nicole Sheehan All rights reserved THE OTAKU PHENOMENON: POP CULTURE, FANDOM, AND RELIGIOSITY IN CONTEMPORARY JAPAN By Kendra Nicole Sheehan B.A., University of Louisville, 2010 M.A., University of Louisville, 2012 A Dissertation Approved on November 17, 2017 by the following Dissertation Committee: __________________________________ Dr. -

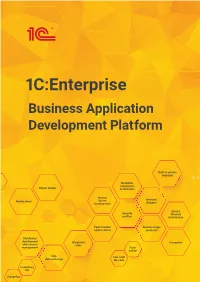

1С:Enterprise HTTP Services Data Processing Model

Application merging In-app messenger with voice and video calls Business Automated components REST API System Flexible analytics log user interface management User settings Data Debugging visualization and performance analytics Seamless Distributed cross-platform Mobile platform databases capability Object-based 1С:Enterprise HTTP services data processing model External Multitenancy data sources Business Application Data access control for individual records JSON Development Platform Thin client Web services Multi-language localization Web client Event alerts Data changelog Git integration Built-in system language Metadata- responsive Report builder architecture Role-based Domain access Interface restrictions Mobile client Driven Development designer HTTP, REST, Intelligent FTP, SMTP, POP3, Auto-generated Service reporting system Security IMAP, OData user interfaces Oriented Cloud profiles Architecture applications Business logic Business composer processes Fault-tolerant Business logic server cluster composer Data Distributed aggregation development Integration Encryption with version tools management Form builder Translation tools Installation XML Low-code Query builder and update data exchange No-code tools In-memory DB Full-text search Changelog Rapid development platform for custom-built business automation solutions Scalable, reliable, efficient, cross-platform, cloud, mobile, desktop 1C:Enterprise is a platform that enables the rapid creation of business automation products. Thousands of off-the-shelf applications have already been developed on the platform. Their functionality can be further customized and expanded using the platform’s development environment. 1C:Enterprise has a low barrier of entry for new developers and lay users thanks to its simple interfaces and visual editing paradigm. Applications developed on the platform easily scale from one to thousands of users and integrate with other 1C and third-party solutions to meet growing business needs. -

Online Media Business Models: Lessons from the Video Game Sector

Komorowski, M and Delaere, S. (2016). Online Media Business Models: Lessons from the Video Game Sector. Westminster Papers in Communication and Culture, 11(1), 103–123, DOI: http://dx.doi. org/10.16997/wpcc.220 RESEARCH ARTICLE Online Media Business Models: Lessons from the Video Game Sector Marlen Komorowski and Simon Delaere imec-SMIT, Vrije Universiteit, Brussels, BE Corresponding author: Marlen Komorowski ([email protected]) Today’s media industry is characterized by disruptive changes and business models have been acknowledged as a driving force for success. Current business model research manages only to grasp static descriptions while in reality media managers are struggling with the dynamics of the industry. This article aims to close this gap by investigating a new paradigm of online media business models. Based on three video game case studies of the massively multiplayer online role-playing game genre, this article explores a novel theoretical approach to explain the changes that can be made within business models. The article highlights the importance of changing processes within online media business models and emphasises that the video game sector is at the forefront of business innovation. Finally, it demonstrates that online media business model change is in a trade-off paradigm between capturing or offering potentially higher value per player vs. accessing a potentially larger player-base. Key words: Media industry; business model; process; disruption; video game sector Introduction Today’s media industry is characterized by disruptive transformations shaped by digitization. Digitization is not only generating new business opportunities but threatens traditional commercialization strategies and is proving highly unpredictable with regards to future market development. -

EA and Crytek Recruit Players Into Free Trial for Crysis Wars

EA and Crytek Recruit Players Into Free Trial for Crysis Wars New Players Can Experience the Critically-Acclaimed Multiplayer Action GameFree from April 9- April 17 and Get the Complete Crysis CompilationCrysis Maximum EditionStarting May 5 REDWOOD CITY, Calif., Apr 09, 2009 (BUSINESS WIRE) -- Electronic Arts Inc. (NASDAQ:ERTS) and Crytek GmbH announced the start of a free trial period for Crysis Wars(R)*, the multiplayer game for Crysis Warhead(R), the award-winning first-person shooter originally released last Fall. Starting today, gamers can play all of Crysis Wars** online for free including each of the game's three action-packed multiplayer modes and all 23 maps. The free trial period runs until Friday, April 17, 2009. This trial is designed to give players a sample of the signature action and visuals that only the Crysis(R) series delivered. For those players that want more than just a sample, EA and Crytek will release Crysis(R) Maximum Edition, a compilation of all three Crysis games in one box (Crysis, Crysis Warhead and Crysis Wars). Available beginning May 5th for the MSRP of $39.99, Crysis Maximum Edition is the ultimate Crysis experience. "When Crysis Wars was released seven months ago, one of our biggest goals was to be able to deliver continued support to our growing multiplayer community," said Cevat Yerli, CEO and President of Crytek. "We think we have delivered on that promise, not only by releasing new content, fixes and our powerful MOD SDK, but also by continuing to offer these types of free trials." Crysis Wars supports matches for up to 32 players and contains three distinct gameplay modes; InstantAction, frenetic deathmatch enhanced by the power of the nanosuit, PowerStruggle, a hardcore team-based mode and TeamInstantAction, a mix of fast-paced action in a team-based environment. -

EA and Crytek Launches Crysis Warhead in North America and Europe

EA and Crytek Launches Crysis Warhead in North America and Europe The Next Installment of the Award-Winning Crysis Franchise Arrives at Retail Stores This Week REDWOOD CITY, Calif., Sep 16, 2008 (BUSINESS WIRE) -- Electronic Arts Inc. (NASDAQ:ERTS) and Crytek GmbH announced today that Crysis Warhead(R), the next installment in the award-winning Crysis(R) franchise, has shipped to retailers in North America and Europe and will hit store shelves and participating digital download services starting September 18, 2008 exclusively for the PC. Containing a new single player campaign featuring Crytek's trademark open-ended gameplay and stunning visuals along with Crysis Wars(R), the exciting new multiplayer suite for the Crysis universe, Crysis Warhead is a tremendous value at only $29.99 and does not require the original Crysis to play. "The launch of Crysis Warhead marks a significant milestone for the entire Crytek family," said Cevat Yerli, CEO and President of Crytek. "The team at Crytek Hungary has delivered a dynamic and intense single player experience more than worthy of the Crysis franchise, while the multiplayer team in Frankfurt has revisited and extended multiplayer in the Crysis universe with Crysis Wars. They are both great representations of our studio's core values of technical excellence, craftsmanship and quality." "Crytek is a world-class partner and quickly becoming one of the most formidable independent developers in the industry," said David DeMartini, Senior Vice President and General Manager of EA Partners. "Crysis was one of the best games of last year and we are thrilled to have the opportunity to bring Crysis Warhead, a game that actually improves upon Crysis' core experience, to the largest possible audience on a global stage." Crysis Warhead takes place alongside the events of last year's critical hit, with players experiencing the explosive battles against waves of challenging enemies on the other side of the island through the eyes and nanosuit of the bold and aggressive Sergeant "Psycho" Sykes. -

Folha De Rosto ICS.Cdr

“For when established identities become outworn or unfinished ones threaten to remain incomplete, special crises compel men to wage holy wars, by the cruellest means, against those who seem to question or threaten their unsafe ideological bases.” Erik Erikson (1956), “The Problem of Ego Identity”, p. 114 “In games it’s very difficult to portray complex human relationships. Likewise, in movies you often flit between action in various scenes. That’s very difficult to do in games, as you generally play a single character: if you switch, it breaks immersion. The fact that most games are first-person shooters today makes that clear. Stories in which the player doesn’t inhabit the main character are difficult for games to handle.” Hideo Kojima Simon Parkin (2014), “Hideo Kojima: ‘Metal Gear questions US dominance of the world”, The Guardian iii AGRADECIMENTOS Por começar quero desde já agradecer o constante e imprescindível apoio, compreensão, atenção e orientação dos Professores Jean Rabot e Clara Simães, sem os quais este trabalho não teria a fruição completa e correta. Um enorme obrigado pelos meses de trabalho, reuniões, telefonemas, emails, conversas e oportunidades. Quero agradecer o apoio de família e amigos, em especial, Tia Bela, João, Teté, Ângela, Verxka, Elma, Silvana, Noëmie, Kalashnikov, Madrinha, Gaivota, Chacal, Rita, Lina, Tri, Bia, Quelinha, Fi, TS, Cinco de Sete, Daniel, Catarina, Professor Albertino, Professora Marques e Professora Abranches, tanto pelas forças de apoio moral e psicológico, pelas recomendações e conselhos de vida, e principalmente pela amizade e memórias ao longo desta batalha. Por último, mas não menos importante, quero agradecer a incessante confiança, companhia e aceitação do bom e do mau pela minha Twin, Safira, que nunca me abandonou em todo o processo desta investigação, do meu caminho académico e da conquista da vida e sonhos.