December-2016 L Ahalada Rao V

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Placement Brochure 2019-20

Suyaradatta Education Foundation’s SURYADATTA INSTITUTE OF MANAGEMENT & MASS COMMUNICATION, SIMMC SURYADATTA INSTITUTE OF BUSINESS MANAGEMENT & TECHNOLOGY, SIBMT PGDM : Approved by AICTE, Govt. of Maharashtra & Recognized by Ministry of HRD, Govt. of India MBA : Affiliated to Savitribai Phule Pune University, approved by DTE & Recognized by Government of Maharashtra L AC E M E N T B R O C H U R E P L AC E M E N T B R O C H U R E 2019-2020 Enriching Careers & Enhancing Lives’ Since 1999 PLACEMENT BROCHURE 2019-20 Invitaon for Campus Recruitment Program Estd. 1999 | Suryadatta Education Foundation’s GROUP OF INSTITUTES ISO 9001 : 2015 Certified Institutes & Accredited by NVT-QC, ANAB & IAF Regd. Office : 2074, Sadashiv Peth, Vijayanagar Colony, Pune - 411030, Maharashtra, INDIA Bavdhan Pune Campus : Survey No. 342, Bavdhan, Pune - 411021, Maharashtra, INDIA Tel. No. : 020-67901300 M. 9881490036, 9763266829 Fax No. : 020-67901333 Email : [email protected] / [email protected] Website : www.suryadatta.org Ranked as A Category Top 50 Group of Institutes in India for 17 consecutive years by the Leading National Surveys Ref. No. : SEF/ SGI / Placements Date : October 2019 Dear Recruiter, Subject : (i) Invitaon for Campus Recruitment Drive for final placement of MBA / PGDM 2018-20 Batch (ii) Summer Internship for 2019-21 Batch We take pleasure in introducing - Suryadaa Group of Instutes established under the aegis of Suryadaa Educaon Foundaon in the year 1999 with the objecve of developing self movated leaders, to be successful in the challenging and vibrant global economy. Courses : We have students from Pan India who are pursuing two years Full Time Post Graduate Courses viz. -

Title: Further Discussion on the Motion of Thanks on the President's Address Moved by Meenakshi Lekhi and Seconded by Smt

an> Title: Further discussion on the motion of thanks on the president's address moved by Meenakshi Lekhi and seconded by Smt. Harsimrat Kaur Badal. HON. SPEAKER: The House will now take up Item No. 14 − Motion of Thanks on the President's Address. िजनके भी भाषण पेिसडट एडेस पर रह गए ह व े अभी ले कर द अभी जीरो ऑवर नह होगा, यह शाम को होगा *शी पशपु ित नाथ िसंह (धनबाद) ◌ः राÂपित जी का अिभभाषण सरकार के िकयाकलाप का आईना होता है िपछले 3 वष के अिभभाषण म िकय े गय े वायदे एक वष म या पगित हई और इस वष सरकार के या संकप ह, उसे रखा गया शी नरेद मोदी जी भारत क जन आकांाओ ं के पितिनिधव करते हए भारत के पधानमंती 2014 के मई माह म बने, िजस समय देश म आराजकता का माहौल था, देश म कई पकार के घोटाल म पवू क सरकार के मंती शािमल थे, मंती जेल म भी गय,े जनता को िवास म लेकर सरकार म भ ाचार होते रहे घोटालामुत शासन आए यह देश क जनता क सोच थी भारत का मान, समान दुिनया म बढ़े, देश म आतं रक सुरा बनी रहे, भय का वातावरण समा हो, नौजवान म िनराशा का भाव समा हो, ऐसे अनेक पहल ू िजसके चुनौती के प म माननीय पधानमंती शी नरेद मोदी जी को सामना करना था एक वष का कालखड बीतने पर देश के लोग म भरपरू िवास पदै ा करने का काम िकया देश ने सभी चुनौितय का सामना करते हए आग े बढ़ने का काम िकया देश का मान, समान बढ़ा, नौजवान म आशा क एक िकरण जागी और हमारे हाथ म रोज़गार िमलेगा, यह भाव पदै ा हआ माननीय पधानमंती जी शी नरेद मोदी ने नई सोच के साथ आग े बढ़ना पारंभ िकया तथा ऐितहािसक कदम उठाय े गये जन-धन योजना, कौशल िवकास, मुदा बक , गरीब के िलए बीमा योजना, गरै सरकारी कमचारय के िलए पशन योजना, कृ िष बीमा योजना के नए आयाम, पधानमंती कृ िष िसंचाई योजना से गरीब िकसान, यापारी, छोटे उमी के बीच नई िदशा देने का काम िकया साथ -

III(B)(A). COMMONWEALTH PARLIAMENTARY ASSOCIATION RELATED EVENTS from JUNE 2014 to JANUARY 2019

III(B)(a). COMMONWEALTH PARLIAMENTARY ASSOCIATION RELATED EVENTS FROM JUNE 2014 TO JANUARY 2019 PAN-COMMONWEALTH CONFERENCE OF COMMONWEALTH WOMEN PARLIAMENTARIANS AT LONDON FROM 25-29 JUNE, 2014. CPA Secretariat, London hosted Pan-Commonwealth Conference of CWP at London from 25-29 June, 2014. The theme of the Conference was “Women in the Post Millennium Development Goal Era”. 2. The Conference held discussions on the following topics: i. Funding and fighting an effective election campaign ii. A vision for the future of Gender Equality iii. Negotiating a better position for women and girls after 2015 iv. Gender and Social Policy – Making your mark v. The role for Women in the Post-MDG era vi. Women in decision making positions – The Board Room and beyond 3. Smt. Meenakashi Lekhi, MP (LS) and Ms. Bhavana (Patil) Gawali, MP (LS) participated in the Conference. Ms. Meenakashi Lekhi, MP (LS) also participated in CWP Steering Committee Meeting held on 28th June, 2014 in her capacity as CWP Steering Committee Member from CPA India Region and submitted a Regional Report. 4. An amount of Rs. 11,53,570/- has been spent on the airfare of the Members. Airfare in respect of Smt. Meenakashi Lekhim MP will be reimbursed by the CPA Secretariat, London. THE 60TH COMMONWEALTH PARLIAMENTARY CONFERENCE IN YAOUNDE, CAMEROON FROM 2 TO 10 OCTOBER, 2014 The 60th Commonwealth Parliamentary Conference was held in Yaounde, Cameroon from 2 to 10 October, 2014. An Indian Parliamentary Delegation led by Shri Pankaj Choudhary, Member of Parliament attended the Conference. The other member of the Delegation from India (Union) Branch was Shri Prem Das Rai, Member of Parliament. -

Brochure Dubbed 140909

Andhi Toofan Director : Chi Gurudutt Music : Vidyasagar Aaj Ka Krantiveer Year of release : 2008 Cast : Sudeep, Vaibhavi, Pooja Gandhi Director : Uday Shankar Synopsis : Kamanna (Doddanna) has brought up Ramanna (Sudeep) and Kittanna (Rockline Venkatesh) Music : Vidyasagar from childhood. All the three are efficient thieves. One fine day they all decide to give up their Year of release : 2001 profession of stealing and settle down in some other place. They are traveling in a lorry that develops mechanical defect in the midst of a forest on a dark night. Luckily, they find a house in the next Cast : Vijaykanth, Soundarya morning to live. This is the house of Kanaka (Vaibhavi). Her father is facing a difficult situation in front Synopsis : Vijaykant plays the role of a respected village elder Thavasi, whose word is law. He also of the village chieftain. The stay of trio in this house gives some relief and courage to the distressed plays the younger character too, that of Bhoopathy, Thavasi's son where he gets to romance - sing family. The trio - Kamanna and his two sons barge in to the chieftain's house to resolve the litigation further angers the village chieftain. and dance, and fight too. Soundarya, is cast as his fiance, whereas Jayasudha plays Thavasi's wife The trio decides to stay in this village thereafter doing cultivation. In a village fair, Ramanna ties the mangalasutra to Gayathri, daughter of and Nasser plays Pandy, Thavasi's brother-in-law and the villain of the piece. village chieftain. The village chieftain give up his harshness for the sake of his daughter Gayathri. -

List of Successful Candidates

11 - LIST OF SUCCESSFUL CANDIDATES CONSTITUENCY WINNER PARTY Andhra Pradesh 1 Nagarkurnool Dr. Manda Jagannath INC 2 Nalgonda Gutha Sukender Reddy INC 3 Bhongir Komatireddy Raj Gopal Reddy INC 4 Warangal Rajaiah Siricilla INC 5 Mahabubabad P. Balram INC 6 Khammam Nama Nageswara Rao TDP 7 Aruku Kishore Chandra Suryanarayana INC Deo Vyricherla 8 Srikakulam Killi Krupa Rani INC 9 Vizianagaram Jhansi Lakshmi Botcha INC 10 Visakhapatnam Daggubati Purandeswari INC 11 Anakapalli Sabbam Hari INC 12 Kakinada M.M.Pallamraju INC 13 Amalapuram G.V.Harsha Kumar INC 14 Rajahmundry Aruna Kumar Vundavalli INC 15 Narsapuram Bapiraju Kanumuru INC 16 Eluru Kavuri Sambasiva Rao INC 17 Machilipatnam Konakalla Narayana Rao TDP 18 Vijayawada Lagadapati Raja Gopal INC 19 Guntur Rayapati Sambasiva Rao INC 20 Narasaraopet Modugula Venugopala Reddy TDP 21 Bapatla Panabaka Lakshmi INC 22 Ongole Magunta Srinivasulu Reddy INC 23 Nandyal S.P.Y.Reddy INC 24 Kurnool Kotla Jaya Surya Prakash Reddy INC 25 Anantapur Anantha Venkata Rami Reddy INC 26 Hindupur Kristappa Nimmala TDP 27 Kadapa Y.S. Jagan Mohan Reddy INC 28 Nellore Mekapati Rajamohan Reddy INC 29 Tirupati Chinta Mohan INC 30 Rajampet Annayyagari Sai Prathap INC 31 Chittoor Naramalli Sivaprasad TDP 32 Adilabad Rathod Ramesh TDP 33 Peddapalle Dr.G.Vivekanand INC 34 Karimnagar Ponnam Prabhakar INC 35 Nizamabad Madhu Yaskhi Goud INC 36 Zahirabad Suresh Kumar Shetkar INC 37 Medak Vijaya Shanthi .M TRS 38 Malkajgiri Sarvey Sathyanarayana INC 39 Secundrabad Anjan Kumar Yadav M INC 40 Hyderabad Asaduddin Owaisi AIMIM 41 Chelvella Jaipal Reddy Sudini INC 1 GENERAL ELECTIONS,INDIA 2009 LIST OF SUCCESSFUL CANDIDATE CONSTITUENCY WINNER PARTY Andhra Pradesh 42 Mahbubnagar K. -

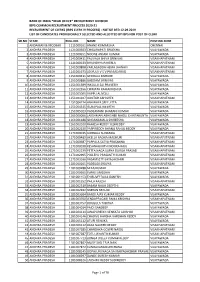

Clerks (Ibps Clerk Ix Process) - Notice Dtd 12.09.2019 List of Candidates Provisionally Selected and Allotted by Ibps for Post of Clerk

BANK OF INDIA *HEAD OFFICE* RECRUITMENT DIVISION IBPS COMMON RECRUITMENT PROCESS 2020-21 RECRUITMENT OF CLERKS (IBPS CLERK IX PROCESS) - NOTICE DTD 12.09.2019 LIST OF CANDIDATES PROVISIONALLY SELECTED AND ALLOTTED BY IBPS FOR POST OF CLERK SR.NO STATE ROLL.NO. NAME POSTING ZONE 1 ANDAMAN & NICOBAR 1111000161 ANAND KUMAR JHA CHENNAI 2 ANDHRA PRADESH 1121000303 CHIGURUPATI SRILEKHA VIJAYAWADA 3 ANDHRA PRADESH 1121000651 NOONE ANJANI KUMAR VIJAYAWADA 4 ANDHRA PRADESH 1141000411 PALIVALA SHIVA SRINIVAS VISAKHAPATNAM 5 ANDHRA PRADESH 1141000633 BHAVISHYA PAKERLA VISAKHAPATNAM 6 ANDHRA PRADESH 1141000808 YARLAGADDA HEMA JAHNAVI VISAKHAPATNAM 7 ANDHRA PRADESH 1141001673 JOSYULA V S V PRASADARAO VISAKHAPATNAM 8 ANDHRA PRADESH 1151000411 GEDDALA KISHORE VIJAYAWADA 9 ANDHRA PRADESH 1151000886 GADDAM SRINIVAS VIJAYAWADA 10 ANDHRA PRADESH 1151001389 INKOLLU SAI PRAVEEN VIJAYAWADA 11 ANDHRA PRADESH 1151002556 CHIMATA RAMAKRISHNA VIJAYAWADA 12 ANDHRA PRADESH 1151003005 VUPPU ALIVELU VIJAYAWADA 13 ANDHRA PRADESH 1151004107 GUNTUR ABHISHEK VISAKHAPATNAM 14 ANDHRA PRADESH 1151004274 ABHINAYA SREE JITTA VIJAYAWADA 15 ANDHRA PRADESH 1151004515 ISUKAPALLI KEERTHI VIJAYAWADA 16 ANDHRA PRADESH 1151005023 VADLAMANI BHARANI KUMAR VIJAYAWADA 17 ANDHRA PRADESH 1161000066 LAKSHMAN ABHISHEK NAIDU CHINTAKUNTA VIJAYAWADA 18 ANDHRA PRADESH 1161001188 SINGANAMALA SHIREESHA VIJAYAWADA 19 ANDHRA PRADESH 1161002020 RAMESH REDDY YESIREDDY VIJAYAWADA 20 ANDHRA PRADESH 1161002630 PAPPIREDDY BHANU RAHUL REDDY VIJAYAWADA 21 ANDHRA PRADESH 1171000015 GUBBALA SUNANDA VISAKHAPATNAM -

List of Winning Candidated Final for 16Th

Leading/Winning State PC No PC Name Candidate Leading/Winning Party Andhra Pradesh 1 Adilabad Rathod Ramesh Telugu Desam Andhra Pradesh 2 Peddapalle Dr.G.Vivekanand Indian National Congress Andhra Pradesh 3 Karimnagar Ponnam Prabhakar Indian National Congress Andhra Pradesh 4 Nizamabad Madhu Yaskhi Goud Indian National Congress Andhra Pradesh 5 Zahirabad Suresh Kumar Shetkar Indian National Congress Andhra Pradesh 6 Medak Vijaya Shanthi .M Telangana Rashtra Samithi Andhra Pradesh 7 Malkajgiri Sarvey Sathyanarayana Indian National Congress Andhra Pradesh 8 Secundrabad Anjan Kumar Yadav M Indian National Congress Andhra Pradesh 9 Hyderabad Asaduddin Owaisi All India Majlis-E-Ittehadul Muslimeen Andhra Pradesh 10 Chelvella Jaipal Reddy Sudini Indian National Congress Andhra Pradesh 11 Mahbubnagar K. Chandrasekhar Rao Telangana Rashtra Samithi Andhra Pradesh 12 Nagarkurnool Dr. Manda Jagannath Indian National Congress Andhra Pradesh 13 Nalgonda Gutha Sukender Reddy Indian National Congress Andhra Pradesh 14 Bhongir Komatireddy Raj Gopal Reddy Indian National Congress Andhra Pradesh 15 Warangal Rajaiah Siricilla Indian National Congress Andhra Pradesh 16 Mahabubabad P. Balram Indian National Congress Andhra Pradesh 17 Khammam Nama Nageswara Rao Telugu Desam Kishore Chandra Suryanarayana Andhra Pradesh 18 Aruku Deo Vyricherla Indian National Congress Andhra Pradesh 19 Srikakulam Killi Krupa Rani Indian National Congress Andhra Pradesh 20 Vizianagaram Jhansi Lakshmi Botcha Indian National Congress Andhra Pradesh 21 Visakhapatnam Daggubati Purandeswari -

National Impact of Organ India Programmes

Parashar Foundation D - 119, Defence Colony, New Delhi 110 024. Tel: +91 11 41838382 ‘Parashar Foundation’ [hereinafter referred to as Foundation] was formed vide Trust Deed dated 24th January, 2005. The Trust was settled by Late Ashok Parashar, in the memory of his late mother Damyanti Parashar, with the philanthropy of ‘doing for the others’. The Foundation was granted registration u/s 12A and initial exemption certificate u/s 80G on 24th August 2005. Donations to the Trust continue to qualify for exemption u/s 80G of the Income Tax Act, 1961, vide Letter No.DIT[E]/2007-2008/P-976/3087 dated 31/12/2007, continuing in perpetuity as per the amendment made vide Finance (No.2) Act 2009 w.e.f. 01.10.2009. The Foundation has been formed with the objective of providing healthcare to the needy, educating and improving the fate of the poor, under-privileged and general population, for serving humanity and for the well-being of the people in general. As is clear from Clauses (a) to (kk) of para 7 of the Trust Deed, the objects of the said Foundation are provision of financial assistance, medical facilities and education, etc. for the benefit of the poor, needy, under privileged and the general population, irrespective of caste, religion or community. The Trustees have utilized the contributions made to the Trust by its settler and donors towards rendering help for educational and medical purposes to needy people and also in giving donations to various institutions engaged in similar charitable and philanthropic activities. Since 2013, the Foundation has focused on creating awareness on Organ Donation under ORGAN (Organ Receiving & Giving Awareness Network) India. -

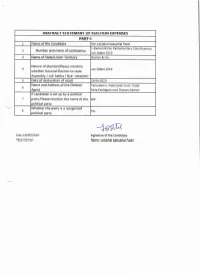

ABSTRACT STATEMENT of ELECTION EXPENSES Name Of

ABSTRACT STATEMENT OF ELECTION EXPENSES PART. L Name of the Candidate Shri Lalubhai babubhai Patel 1-Daman & Diu Parliamentary Constituency 2 Number and name of costituency Lok Sabha 2019 3 Name of State/Union Territory Daman & Diu Nature of election(Please mention 4 Lok Sabha 2019 whether General Election to state Assembly / Lok Sabha / Bye - election) 5 Date of declaration of result 23-05-2019 Name and Address of the Election Tarunaben L Patel,Sabri Kutir, Patel 6 Agent Falia,Kachigo ffi, na ni Da ma n, Daman lf candidate is set up by a political 7 party,Please mention the name of the BJP political party Whether the party is a recognised 8 Yes political party Date -I4/0G12019 Signature of the Candidate P lace-Da ma n Name: Lalubhai babubhai Patel t PART.II: ABSTRCT OF STATEMENT OF ETECTION EXPENDITURE OF CANDIDATE s.NO Particulars Amount Amount Amount Total Election incurred/aut incurre dla incurred/au expenditure horized by uthorized thorized by (31+(41+(sl candidate or by Political Other [in his election Party(in Rs| Rsl agent(in Rsl 1 2 3 4 5 6 Expenses in Public Meeting, Rally,procession etc:-1.a: Expenses in Public meetihB,Rally,procession etc (other than I 8,75,937 35,000 with Star Campaigners of the Political Party)(Enclose as per 88,550 10,00,597 Schedule -1) 1.b :Expenses in Public Meeting, Rally,procession etc with the Star Campaigner (i.e other than those for general L,34,775 party propaganda)(Enclose as per Schedule-2) 1,34,775 Campaign materials other than those used in public meeting ,rally,procession etc mentioned in -

Download Brochure

Celebrating UNESCO Chair for 17 Human Rights, Democracy, Peace & Tolerance Years of Academic Excellence World Peace Centre (Alandi) Pune, India India's First School to Create Future Polical Leaders ELECTORAL Politics to FUNCTIONAL Politics We Make Common Man, Panchayat to Parliament 'a Leader' ! Political Leadership begins here... -Rahul V. Karad Your Pathway to a Great Career in Politics ! Two-Year MASTER'S PROGRAM IN POLITICAL LEADERSHIP AND GOVERNMENT MPG Batch-17 (2021-23) UGC Approved Under The Aegis of mitsog.org I mitwpu.edu.in Seed Thought MIT School of Government (MIT-SOG) is dedicated to impart leadership training to the youth of India, desirous of making a CONTENTS career in politics and government. The School has the clear § Message by President, MIT World Peace University . 2 objective of creating a pool of ethical, spirited, committed and § Message by Principal Advisor and Chairman, Academic Advisory Board . 3 trained political leadership for the country by taking the § A Humble Tribute to 1st Chairman & Mentor, MIT-SOG . 4 aspirants through a program designed methodically. This § Message by Initiator . 5 exposes them to various governmental, political, social and § Messages by Vice-Chancellor and Advisor, MIT-WPU . 6 democratic processes, and infuses in them a sense of national § Messages by Academic Advisor and Associate Director, MIT-SOG . 7 pride, democratic values and leadership qualities. § Members of Academic Advisory Board MIT-SOG . 8 § Political Opportunities for Youth (Political Leadership diagram). 9 Rahul V. Karad § About MIT World Peace University . 10 Initiator, MIT-SOG § About MIT School of Government. 11 § Ladder of Leadership in Democracy . 13 § Why MIT School of Government. -

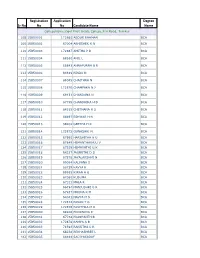

Sr No Registration No Application No Candidate Name Degree Name

Registration Application Degree Sr No No No Candidate Name Name CollegeName:Govt First Grade College,B.H.Road, Tumkur 108 15B50001 172865 ABDUR RAHMAN BCA 109 15B50002 67004 ABHISHEK K N BCA 110 15B50003 172867 AMITHA P R BCA 111 15B50004 68160 ANIL L BCA 112 15B50005 66843 ANNAPURNA B R BCA 113 15B50006 84819 BINDU N BCA 114 15B50007 69045 CHAITHRA N BCA 115 15B50008 172870 CHAMPAKA N J BCA 116 15B50009 69131 CHANDANA N BCA 117 15B50010 67785 CHANDRIKA H D BCA 118 15B50011 64315 CHETHANA H S BCA 119 15B50012 66697 ESHWAR H N BCA 120 15B50013 68202 GEETHA H R BCA 121 15B50014 172872 GUNASHRI N BCA 122 15B50015 67995 HARSHITHA H U BCA 123 15B50016 67849 HEMANTHARAJU V BCA 124 15B50017 67539 HEMAVATHI G K BCA 125 15B50018 64237 JAGRUTHI D S BCA 126 15B50019 67578 JAYALAKSHMI N BCA 127 15B50020 69084 KALPANA S BCA 128 15B50021 66739 KAVYA K BCA 129 15B50022 69165 KIRAN A G BCA 130 15B50023 67080 KUSUMA BCA 131 15B50024 67333 MALA R BCA 132 15B50025 66494 MANJUSHRI G R BCA 133 15B50026 67937 MOUNA K M BCA 134 15B50027 64041 NAVYA M S BCA 135 15B50028 172874 PAVAN T G BCA 136 15B50029 172876 PAVITHRA M D BCA 137 15B50030 69208 POORNIMA R BCA 138 15B50031 67738 PRASHANTH B BCA 139 15B50032 172878 RAMYA S B BCA 140 15B50033 71593 RANJITHA C R BCA 141 15B50034 68238 REKHASHREE L BCA 142 15B50035 64444 SADIYASADAF BCA 143 15B50036 172884 SAIPRIYA S BCA 144 15B50037 66611 SHARADA P N BCA 145 15B50038 64080 SHILPA A L BCA 146 15B50039 67670 SRINIVAS P S BCA 147 15B50040 63865 SUBHASHCHANDRABOSE R BCA 148 15B50041 62238 SUDARSHAN R BCA 149 15B50042 172887 SWAROOP M BCA 150 15B50043 67881 TEJASWINI K T BCA 151 15B50044 172889 THANUJA BCA 152 15B50045 172892 VASANTHKUMAR R BCA 153 15B50046 172895 VINAY K P BCA 154 15B50047 66912 YASHAVANTHA K B BCA 155 15B50048 66553 YASHODHA Y BCA 156 15B50049 63983 YOGEESH H V BCA CollegeName:Bapuji F.G.C. -

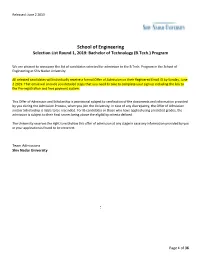

School of Engineering Selection List 2019

Released: June 2 2019 School of Engineering Selection List Round 1, 2019: Bachelor of Technology (B.Tech.) Program We are pleased to announce the list of candidates selected for admission to the B.Tech. Program in the School of Engineering at Shiv Nadar University. All selected candidates will individually receive a formal Offer of Admission on their Registered Email ID by Sunday, June 2 2019. That email will provide you detailed steps that you need to take to complete your sign up including the link to the Pre-registration and fees payment system. This Offer of Admission and Scholarship is provisional subject to verification of the documents and information provided by you during the Admission Process, when you join the University. In case of any discrepancy, the Offer of Admission and/or Scholarship is liable to be rescinded. For IB candidates or those who have applied using predicted grades, the admission is subject to their final scores being above the eligibility criteria defined. The University reserves the right to withdraw this offer of admission at any stage in case any information provided by you in your application is found to be incorrect. Team Admissions Shiv Nadar University ‘ Page 1 of 36 Released: June 2 2019 List of Candidates Selected in Round 1 of B.Tech. Program Names are in Candidate ID order. Amount Payable Scholarship Candidate ID Name Final Stream - First Offered Instalment(₹) 2019SNU2445866 Dhruv Gupta Mechanical Engineering B 3,26,500 2019SNU2445870 Rohit R Mechanical Engineering B 3,26,500 2019SNU2445888 Aarushi