Constructing Probability Distributions Having a Unit Index of Dispersion

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Simulation of Moment, Cumulant, Kurtosis and the Characteristics Function of Dagum Distribution

264 IJCSNS International Journal of Computer Science and Network Security, VOL.17 No.8, August 2017 Simulation of Moment, Cumulant, Kurtosis and the Characteristics Function of Dagum Distribution Dian Kurniasari1*,Yucky Anggun Anggrainy1, Warsono1 , Warsito2 and Mustofa Usman1 1Department of Mathematics, Faculty of Mathematics and Sciences, Universitas Lampung, Indonesia 2Department of Physics, Faculty of Mathematics and Sciences, Universitas Lampung, Indonesia Abstract distribution is a special case of Generalized Beta II The Dagum distribution is a special case of Generalized Beta II distribution. Dagum (1977, 1980) distribution has been distribution with the parameter q=1, has 3 parameters, namely a used in studies of income and wage distribution as well as and p as shape parameters and b as a scale parameter. In this wealth distribution. In this context its features have been study some properties of the distribution: moment, cumulant, extensively analyzed by many authors, for excellent Kurtosis and the characteristics function of the Dagum distribution will be discussed. The moment and cumulant will be survey on the genesis and on empirical applications see [4]. discussed through Moment Generating Function. The His proposals enable the development of statistical characteristics function will be discussed through the expectation of the definition of characteristics function. Simulation studies distribution used to empirical income and wealth data that will be presented. Some behaviors of the distribution due to the could accommodate both heavy tails in empirical income variation values of the parameters are discussed. and wealth distributions, and also permit interior mode [5]. Key words: A random variable X is said to have a Dagum distribution Dagum distribution, moment, cumulant, kurtosis, characteristics function. -

A Two Parameter Discrete Lindley Distribution

Revista Colombiana de Estadística January 2016, Volume 39, Issue 1, pp. 45 to 61 DOI: http://dx.doi.org/10.15446/rce.v39n1.55138 A Two Parameter Discrete Lindley Distribution Distribución Lindley de dos parámetros Tassaddaq Hussain1;a, Muhammad Aslam2;b, Munir Ahmad3;c 1Department of Statistics, Government Postgraduate College, Rawalakot, Pakistan 2Department of Statistics, Faculty of Sciences, King Abdulaziz University, Jeddah, Saudi Arabia 3National College of Business Administration and Economics, Lahore, Pakistan Abstract In this article we have proposed and discussed a two parameter discrete Lindley distribution. The derivation of this new model is based on a two step methodology i.e. mixing then discretizing, and can be viewed as a new generalization of geometric distribution. The proposed model has proved itself as the least loss of information model when applied to a number of data sets (in an over and under dispersed structure). The competing mod- els such as Poisson, Negative binomial, Generalized Poisson and discrete gamma distributions are the well known standard discrete distributions. Its Lifetime classification, kurtosis, skewness, ascending and descending factorial moments as well as its recurrence relations, negative moments, parameters estimation via maximum likelihood method, characterization and discretized bi-variate case are presented. Key words: Characterization, Discretized version, Estimation, Geometric distribution, Mean residual life, Mixture, Negative moments. Resumen En este artículo propusimos y discutimos la distribución Lindley de dos parámetros. La obtención de este Nuevo modelo está basada en una metodo- logía en dos etapas: mezclar y luego discretizar, y puede ser vista como una generalización de una distribución geométrica. El modelo propuesto de- mostró tener la menor pérdida de información al ser aplicado a un cierto número de bases de datos (con estructuras de supra y sobredispersión). -

Lecture 2: Moments, Cumulants, and Scaling

Lecture 2: Moments, Cumulants, and Scaling Scribe: Ernst A. van Nierop (and Martin Z. Bazant) February 4, 2005 Handouts: • Historical excerpt from Hughes, Chapter 2: Random Walks and Random Flights. • Problem Set #1 1 The Position of a Random Walk 1.1 General Formulation Starting at the originX� 0= 0, if one takesN steps of size�xn, Δ then one ends up at the new position X� N . This new position is simply the sum of independent random�xn), variable steps (Δ N � X� N= Δ�xn. n=1 The set{ X� n} contains all the positions the random walker passes during its walk. If the elements of the{ setΔ�xn} are indeed independent random variables,{ X� n then} is referred to as a “Markov chain”. In a MarkovX� chain,N+1is independentX� ofnforn < N, but does depend on the previous positionX� N . LetPn(R�) denote the probability density function (PDF) for theR� of values the random variable X� n. Note that this PDF can be calculated for both continuous and discrete systems, where the discrete system is treated as a continuous system with Dirac delta functions at the allowed (discrete) values. Letpn(�r|R�) denote the PDF�x forn. Δ Note that in this more general notation we have included the possibility that�r (which is the value�xn) of depends Δ R� on. In Markovchain jargon,pn(�r|R�) is referred to as the “transition probability”X� N fromto state stateX� N+1. Using the PDFs we just defined, let’s return to Bachelier’s equation from the first lecture. -

STAT 830 Generating Functions

STAT 830 Generating Functions Richard Lockhart Simon Fraser University STAT 830 — Fall 2011 Richard Lockhart (Simon Fraser University) STAT 830 Generating Functions STAT 830 — Fall 2011 1 / 21 What I think you already have seen Definition of Moment Generating Function Basics of complex numbers Richard Lockhart (Simon Fraser University) STAT 830 Generating Functions STAT 830 — Fall 2011 2 / 21 What I want you to learn Definition of cumulants and cumulant generating function. Definition of Characteristic Function Elementary features of complex numbers How they “characterize” a distribution Relation to sums of independent rvs Richard Lockhart (Simon Fraser University) STAT 830 Generating Functions STAT 830 — Fall 2011 3 / 21 Moment Generating Functions pp 56-58 Def’n: The moment generating function of a real valued X is tX MX (t)= E(e ) defined for those real t for which the expected value is finite. Def’n: The moment generating function of X Rp is ∈ ut X MX (u)= E[e ] defined for those vectors u for which the expected value is finite. Formal connection to moments: ∞ k MX (t)= E[(tX ) ]/k! Xk=0 ∞ ′ k = µk t /k! . Xk=0 Sometimes can find power series expansion of MX and read off the moments of X from the coefficients of tk /k!. Richard Lockhart (Simon Fraser University) STAT 830 Generating Functions STAT 830 — Fall 2011 4 / 21 Moments and MGFs Theorem If M is finite for all t [ ǫ,ǫ] for some ǫ> 0 then ∈ − 1 Every moment of X is finite. ∞ 2 M isC (in fact M is analytic). ′ k 3 d µk = dtk MX (0). -

Moments & Cumulants

ECON-UB 233 Dave Backus @ NYU Lab Report #1: Moments & Cumulants Revised: September 17, 2015 Due at the start of class. You may speak to others, but whatever you hand in should be your own work. Use Matlab where possible and attach your code to your answer. Solution: Brief answers follow, but see also the attached Matlab program. Down- load this document as a pdf, open it, and click on the pushpin: 1. Moments of normal random variables. This should be review, but will get you started with moments and generating functions. Suppose x is a normal random variable with mean µ = 0 and variance σ2. (a) What is x's standard deviation? (b) What is x's probability density function? (c) What is x's moment generating function (mgf)? (Don't derive it, just write it down.) (d) What is E(ex)? (e) Let y = a + bx. What is E(esy)? How does it tell you that y is normal? Solution: (a) The standard deviation is the (positive) square root of the variance, namely σ if σ > 0 (or jσj if you want to be extra precise). (b) The pdf is p(x) = (2πσ2)−1=2 exp(−x2=2σ2): (c) The mgf is h(s) = exp(s2σ2=2). (d) E(ex) is just the mgf evaluated at s = 1: h(1) = eσ2=2. (e) The mfg of y is sy s(a+bx) sa sbx sa hy(s) = E(e ) = E(e ) = e E(e ) = e hx(bs) 2 2 2 2 = esa+(bs) σ =2 = esa+s (bσ) =2: This has the form of a normal random variable with mean a (the coefficient of s) and variance (bσ)2 (the coefficient of s2=2). -

Descriptive Statistics

IMGD 2905 Descriptive Statistics Chapter 3 Summarizing Data Q: how to summarize numbers? • With lots of playtesting, there is a lot of data (good!) • But raw data is often just a pile of numbers • Rarely of interest, or even sensible Summarizing Data Measures of central tendency Groupwork 4 3 7 8 3 4 22 3 5 3 2 3 • Indicate central tendency with one number? • What are pros and cons of each? Measure of Central Tendency: Mean • Aka: “arithmetic mean” or “average” =AVERAGE(range) =AVERAGEIF() – averages if numbers meet certain condition Measure of Central Tendency: Median • Sort values low to high and take middle value =MEDIAN(range) Measure of Central Tendency: Mode • Number which occurs most frequently • Not too useful in many cases Best use for categorical data • e.g., most popular Hero group in http://pad3.whstatic.com/images/thumb/c/cd/Find-the-Mode-of-a-Set-of-Numbers- Heroes of theStep-7.jpg/aid130521-v4-728px-Find-the-Mode-of-a-Set-of-Numbers-Step-7.jpg Storm =MODE() Mean, Median, Mode? frequency Mean, Median, Mode? frequency Mean, Median, Mode? frequency Mean, Median, Mode? frequency Mean, Median, Mode? frequency Mean, Median, Mode? mean median modes mode mean median frequency no mode mean (a) median (b) frequency mode mode median median (c) mean mean frequency frequency frequency (d) (e) Which to Use: Mean, Median, Mode? Which to Use: Mean, Median, Mode? • Mean many statistical tests that use sample ‒ Estimator of population mean ‒ Uses all data Which to Use: Mean, Median, Mode? • Median is useful for skewed data ‒ e.g., income data (US Census) or housing prices (Zillo) ‒ e.g., Overwatch team (6 players): 5 people level 5, 1 person level 275 ₊ Mean is 50 - not so useful since no one at this level ₊ Median is 5 – perhaps more representative ‒ Does not use all data. -

Asymptotic Theory for Statistics Based on Cumulant Vectors with Applications

UC Santa Barbara UC Santa Barbara Previously Published Works Title Asymptotic theory for statistics based on cumulant vectors with applications Permalink https://escholarship.org/uc/item/4c6093d0 Journal SCANDINAVIAN JOURNAL OF STATISTICS, 48(2) ISSN 0303-6898 Authors Rao Jammalamadaka, Sreenivasa Taufer, Emanuele Terdik, Gyorgy H Publication Date 2021-06-01 DOI 10.1111/sjos.12521 Peer reviewed eScholarship.org Powered by the California Digital Library University of California Received: 21 November 2019 Revised: 8 February 2021 Accepted: 20 February 2021 DOI: 10.1111/sjos.12521 ORIGINAL ARTICLE Asymptotic theory for statistics based on cumulant vectors with applications Sreenivasa Rao Jammalamadaka1 Emanuele Taufer2 György H. Terdik3 1Department of Statistics and Applied Probability, University of California, Abstract Santa Barbara, California For any given multivariate distribution, explicit formu- 2Department of Economics and lae for the asymptotic covariances of cumulant vectors Management, University of Trento, of the third and the fourth order are provided here. Gen- Trento, Italy 3Department of Information Technology, eral expressions for cumulants of elliptically symmetric University of Debrecen, Debrecen, multivariate distributions are also provided. Utilizing Hungary these formulae one can extend several results currently Correspondence available in the literature, as well as obtain practically Emanuele Taufer, Department of useful expressions in terms of population cumulants, Economics and Management, University and computational formulae in terms of commutator of Trento, Via Inama 5, 38122 Trento, Italy. Email: [email protected] matrices. Results are provided for both symmetric and asymmetric distributions, when the required moments Funding information exist. New measures of skewness and kurtosis based European Union and European Social Fund, Grant/Award Number: on distinct elements are discussed, and other applica- EFOP3.6.2-16-2017-00015 tions to independent component analysis and testing are considered. -

![Arxiv:2102.01459V2 [Math.PR] 4 Mar 2021 H EHDO UUAT O H OMLAPPROXIMATION NORMAL the for CUMULANTS of METHOD the .Bud Ihfiieymn Oet.Pofo Hoe](https://docslib.b-cdn.net/cover/6755/arxiv-2102-01459v2-math-pr-4-mar-2021-h-ehdo-uuat-o-h-omlapproximation-normal-the-for-cumulants-of-method-the-bud-ih-ieymn-oet-pofo-hoe-2076755.webp)

Arxiv:2102.01459V2 [Math.PR] 4 Mar 2021 H EHDO UUAT O H OMLAPPROXIMATION NORMAL the for CUMULANTS of METHOD the .Bud Ihfiieymn Oet.Pofo Hoe

THE METHOD OF CUMULANTS FOR THE NORMAL APPROXIMATION HANNA DORING,¨ SABINE JANSEN, AND KRISTINA SCHUBERT Abstract. The survey is dedicated to a celebrated series of quantitave results, developed by the Lithuanian school of probability, on the normal approximation for a real-valued random 1+γ j−2 variable. The key ingredient is a bound on cumulants of the type |κj (X)|≤ j! /∆ , which is weaker than Cram´er’s condition of finite exponential moments. We give a self-contained proof of some of the “main lemmas” in a book by Saulis and Statuleviˇcius (1989), and an accessible introduction to the Cram´er-Petrov series. In addition, we explain relations with heavy-tailed Weibull variables, moderate deviations, and mod-phi convergence. We discuss some methods for bounding cumulants such as summability of mixed cumulants and dependency graphs, and briefly review a few recent applications of the method of cumulants for the normal approxima- tion. Mathematics Subject Classification 2020: 60F05; 60F10; 60G70; 60K35. Keywords: cumulants; central limit theorems and Berry-Esseen theorems; large and moderate deviations; heavy-tailed variables. Contents 1. Introduction...................................... ................................... 2 1.1. Aims and scope of the article........................... ......................... 2 1.2. Cumulants........................................ ............................... 3 1.3. Short description of the “main lemmas” . ....................... 4 1.4. How to bound cumulants .............................. ......................... -

The Need to Measure Variance in Experiential Learning and a New Statistic to Do So

Developments in Business Simulation & Experiential Learning, Volume 26, 1999 THE NEED TO MEASURE VARIANCE IN EXPERIENTIAL LEARNING AND A NEW STATISTIC TO DO SO John R. Dickinson, University of Windsor James W. Gentry, University of Nebraska-Lincoln ABSTRACT concern should be given to the learning process rather than performance outcomes. The measurement of variation of qualitative or categorical variables serves a variety of essential We contend that insight into process can be gained purposes in simulation gaming: de- via examination of within-student and across-student scribing/summarizing participants’ decisions for variance in decision-making. For example, if the evaluation and feedback, describing/summarizing role of an experiential exercise is to foster trial-and- simulation results toward the same ends, and error learning, the variance in a student’s decisions explaining variation for basic research purposes. will be greatest when the trial-and-error stage is at Extant measures of dispersion are not well known. its peak. To the extent that the exercise works as Too, simulation gaming situations are peculiar in intended, greater variances would be expected early that the total number of observations available-- in the game play as opposed to later, barring the usually the number of decision periods or the game world encountering a discontinuity. number of participants--is often small. Each extant measure of dispersion has its own limitations. On the other hand, it is possible that decisions may Common limitations are that, under ordinary be more consistent early and then more variable later circumstances and especially with small numbers if the student is trying to recover from early of observations, a measure may not be defined and missteps. -

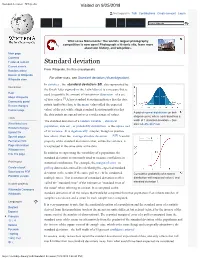

Standard Deviation - Wikipedia Visited on 9/25/2018

Standard deviation - Wikipedia Visited on 9/25/2018 Not logged in Talk Contributions Create account Log in Article Talk Read Edit View history Wiki Loves Monuments: The world's largest photography competition is now open! Photograph a historic site, learn more about our history, and win prizes. Main page Contents Featured content Standard deviation Current events Random article From Wikipedia, the free encyclopedia Donate to Wikipedia For other uses, see Standard deviation (disambiguation). Wikipedia store In statistics , the standard deviation (SD, also represented by Interaction the Greek letter sigma σ or the Latin letter s) is a measure that is Help used to quantify the amount of variation or dispersion of a set About Wikipedia of data values.[1] A low standard deviation indicates that the data Community portal Recent changes points tend to be close to the mean (also called the expected Contact page value) of the set, while a high standard deviation indicates that A plot of normal distribution (or bell- the data points are spread out over a wider range of values. shaped curve) where each band has a Tools The standard deviation of a random variable , statistical width of 1 standard deviation – See What links here also: 68–95–99.7 rule population, data set , or probability distribution is the square root Related changes Upload file of its variance . It is algebraically simpler, though in practice [2][3] Special pages less robust , than the average absolute deviation . A useful Permanent link property of the standard deviation is that, unlike the variance, it Page information is expressed in the same units as the data. -

Moments and Generating Functions

Moments and Generating Functions September 24 and 29, 2009 Some choices of g yield a specific name for the value of Eg(X). 1 Moments, Factorial Moments, and Central Moments • For g(x) = x, we call EX the mean of X and often write µX or simply µ if only the random variable X is under consideration. { S, the number of successes in n Bernoulli trials with success parameter p, has mean np. { The mean of a geometric random variable with parameter p is 1=p. { The mean of a exponential random variable with parameter β is β. { A standard normal random variable has mean 0. • For g(x) = xm, EXm is called the m-th moment of X. { If X is a Bernoulli random variable, then X = Xm. Thus, EXm = EX = p. R 1 m { For a uniform random variable on [0; 1], the m-th moment is 0 x dx = 1=(m + 1). { The third moment for Z, a standard normal random, is 0. The fourth moment, 1 Z 1 z2 1 z2 1 Z 1 z2 4 4 3 2 EZ = p z exp − dz = −p z exp − + 3z exp − dz 2π −∞ 2 2π 2 −∞ −∞ 2 = 3EZ2 = 3 3 z2 u(z) = z v(t) = − exp − 2 0 2 0 z2 u (z) = 3z v (t) = z exp − 2 { For T , an exponential random variable, we integrate by parts Z 1 1 1 Z 1 m m m m−1 ET = t exp −(t/β) dt = t exp −(t/β) + mt exp −(t/β) dt 0 β 0 0 Z 1 1 = βm tm−1 exp −(t/β) dt = mβET m−1 0 β u(t) = tm v(t) = exp −(t/β) 0 m−1 0 1 u (t) = mt v (t) = β exp −(t/β) Thus, by induction, we have that ET m = βmm!: 1 • If g(x) = (x)k, where (x)k = x(x−1) ··· (x−k +1), then E(X)k is called the k-th factorial moment. -

Population Dispersion

AccessScience from McGraw-Hill Education Page 1 of 7 www.accessscience.com Population dispersion Contributed by: Francis C. Evans Publication year: 2014 The spatial distribution at any particular moment of the individuals of a species of plant or animal. Under natural conditions organisms are distributed either by active movements, or migrations, or by passive transport by wind, water, or other organisms. The act or process of dissemination is usually termed dispersal, while the resulting pattern of distribution is best referred to as dispersion. Dispersion is a basic characteristic of populations, controlling various features of their structure and organization. It determines population density, that is, the number of individuals per unit of area, or volume, and its reciprocal relationship, mean area, or the average area per individual. It also determines the frequency, or chance of encountering one or more individuals of the population in a particular sample unit of area, or volume. The ecologist therefore studies not only the fluctuations in numbers of individuals in a population but also the changes in their distribution in space. See also: POPULATION DISPERSAL. Principal types of dispersion The dispersion pattern of individuals in a population may conform to any one of several broad types, such as random, uniform, or contagious (clumped). Any pattern is relative to the space being examined; a population may appear clumped when a large area is considered, but may prove to be distributed at random with respect to a much smaller area. Random or haphazard. This implies that the individuals have been distributed by chance. In such a distribution, the probability of finding an individual at any point in the area is the same for all points (Fig.