Annual Report 2016 16 Year of Operations

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Dixit-Pindyck and Arrow-Fisher-Hanemann-Henry Option Concepts in a Finance Framework

Dixit-Pindyck and Arrow-Fisher-Hanemann-Henry Option Concepts in a Finance Framework January 12, 2015 Abstract We look at the debate on the equivalence of the Dixit-Pindyck (DP) and Arrow-Fisher- Hanemann-Henry (AFHH) option values. Casting the problem into a financial framework allows to disentangle the discussion without unnecessarily introducing new definitions. Instead, the option values can be easily translated to meaningful terms of financial option pricing. We find that the DP option value can easily be described as time-value of an American plain-vanilla option, while the AFHH option value is an exotic chooser option. Although the option values can be numerically equal, they differ for interesting, i.e. non-trivial investment decisions and benefit-cost analyses. We find that for applied work, compared to the Dixit-Pindyck value, the AFHH concept has only limited use. Keywords: Benefit cost analysis, irreversibility, option, quasi-option value, real option, uncertainty. Abbreviations: i.e.: id est; e.g.: exemplum gratia. 1 Introduction In the recent decades, the real options1 concept gained a large foothold in the strat- egy and investment literature, even more so with Dixit & Pindyck (1994)'s (DP) seminal volume on investment under uncertainty. In environmental economics, the importance of irreversibility has already been known since the contributions of Arrow & Fisher (1974), Henry (1974), and Hanemann (1989) (AFHH) on quasi-options. As Fisher (2000) notes, a unification of the two option concepts would have the benefit of applying the vast results of real option pricing in environmental issues. In his 1The term real option has been coined by Myers (1977). -

Kit Del Cittadino

KIT DEL CITTADINO Guida ai servizi per nuovi residenti nel Comune di Cuneo BENVENUTO A CUNEO Siamo davvero lieti di accoglierti nella nostra comunità. Ricca di valori, di storia, immersa nel verde e circondata dalle montagne, Cuneo è una città a misura di donna, d’uomo e di bambino, accogliente, vivibile, dove crescere e stare bene. Questa guida è stata pensata per offrire uno strumento utile che consenta di avere tutte le informazioni sugli uffici e sui servizi erogati dal Comune a chi, come te, ha scelto o sceglierà in futuro di fare di Cuneo la propria casa. Casa non è solo un posto in cui abitare, casa è anche una comunità in cui essere e sentirsi integrato, in cui intessere relazioni e creare legami. Grazie di aver scelto Cuneo come tua casa. Federico Borgna Sindaco di Cuneo 4 Sommario ANAGRAFE ............................................................................................................................................................6 TRIBUTI .................................................................................................................................................................7 RACCOLTA DIFFERENZIATA DEI RIFIUTI ................................................................................................................8 RIFIUTI INGOMBRANTI .....................................................................................................................................8 AREE ECOLOGICHE ............................................................................................................................................8 -

Analysis of Employee Stock Options and Guaranteed Withdrawal Benefits for Life by Premal Shah B

Analysis of Employee Stock Options and Guaranteed Withdrawal Benefits for Life by Premal Shah B. Tech. & M. Tech., Electrical Engineering (2003), Indian Institute of Technology (IIT) Bombay, Mumbai Submitted to the Sloan School of Management in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Operations Research at the MASSACHUSETTS INSTITUTE OF TECHNOLOGY September 2008 c Massachusetts Institute of Technology 2008. All rights reserved. Author.............................................................. Sloan School of Management July 03, 2008 Certified by. Dimitris J. Bertsimas Boeing Professor of Operations Research Thesis Supervisor Accepted by . Cynthia Barnhart Professor Co-director, Operations Research Center 2 Analysis of Employee Stock Options and Guaranteed Withdrawal Benefits for Life by Premal Shah B. Tech. & M. Tech., Electrical Engineering (2003), Indian Institute of Technology (IIT) Bombay, Mumbai Submitted to the Sloan School of Management on July 03, 2008, in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Operations Research Abstract In this thesis we study three problems related to financial modeling. First, we study the problem of pricing Employee Stock Options (ESOs) from the point of view of the issuing company. Since an employee cannot trade or effectively hedge ESOs, she exercises them to maximize a subjective criterion of value. Modeling this exercise behavior is key to pricing ESOs. We argue that ESO exercises should not be modeled on a one by one basis, as is commonly done, but at a portfolio level because exercises related to different ESOs that an employee holds would be coupled. Using utility based models we also show that such coupled exercise behavior leads to lower average ESO costs for the commonly used utility functions such as power and exponential utilities. -

Sequential Compound Options and Investments Valuation

Sequential compound options and investments valuation Luigi Sereno Dottorato di Ricerca in Economia - XIX Ciclo - Alma Mater Studiorum - Università di Bologna Marzo 2007 Relatore: Prof. ssa Elettra Agliardi Coordinatore: Prof. Luca Lambertini Settore scienti…co-disciplinare: SECS-P/01 Economia Politica ii Contents I Sequential compound options and investments valua- tion 1 1 An overview 3 1.1 Introduction . 3 1.2 Literature review . 6 1.2.1 R&D as real options . 11 1.2.2 Exotic Options . 12 1.3 An example . 17 1.3.1 Value of expansion opportunities . 18 1.3.2 Value with abandonment option . 23 1.3.3 Value with temporary suspension . 26 1.4 Real option modelling with jump processes . 31 1.4.1 Introduction . 31 1.4.2 Merton’sapproach . 33 1.4.3 Further reading . 36 1.5 Real option and game theory . 41 1.5.1 Introduction . 41 1.5.2 Grenadier’smodel . 42 iii iv CONTENTS 1.5.3 Further reading . 45 1.6 Final remark . 48 II The valuation of new ventures 59 2 61 2.1 Introduction . 61 2.2 Literature Review . 63 2.2.1 Flexibility of Multiple Compound Real Options . 65 2.3 Model and Assumptions . 68 2.3.1 Value of the Option to Continuously Shut - Down . 69 2.4 An extension . 74 2.4.1 The mathematical problem and solution . 75 2.5 Implementation of the approach . 80 2.5.1 Numerical results . 82 2.6 Final remarks . 86 III Valuing R&D investments with a jump-di¤usion process 93 3 95 3.1 Introduction . -

Calibration Risk for Exotic Options

Forschungsgemeinschaft through through Forschungsgemeinschaft SFB 649DiscussionPaper2006-001 * CASE - Center for Applied Statistics and Economics, Statisticsand Center forApplied - * CASE Calibration Riskfor This research was supported by the Deutsche the Deutsche by was supported This research Wolfgang K.Härdle** Humboldt-Universität zuBerlin,Germany SFB 649, Humboldt-Universität zu Berlin zu SFB 649,Humboldt-Universität Exotic Options Spandauer Straße 1,D-10178 Berlin Spandauer http://sfb649.wiwi.hu-berlin.de http://sfb649.wiwi.hu-berlin.de Kai Detlefsen* ISSN 1860-5664 the SFB 649 "Economic Risk". "Economic the SFB649 SFB 6 4 9 E C O N O M I C R I S K B E R L I N Calibration Risk for Exotic Options K. Detlefsen and W. K. H¨ardle CASE - Center for Applied Statistics and Economics Humboldt-Universit¨atzu Berlin Wirtschaftswissenschaftliche Fakult¨at Spandauer Strasse 1, 10178 Berlin, Germany Abstract Option pricing models are calibrated to market data of plain vanil- las by minimization of an error functional. From the economic view- point, there are several possibilities to measure the error between the market and the model. These different specifications of the error give rise to different sets of calibrated model parameters and the resulting prices of exotic options vary significantly. These price differences often exceed the usual profit margin of exotic options. We provide evidence for this calibration risk in a time series of DAX implied volatility surfaces from April 2003 to March 2004. We analyze in the Heston and in the Bates model factors influencing these price differences of exotic options and finally recommend an error func- tional. -

Revista Electrónica: Actas Y Comunicaciones

1 Revista electrónica anual: Actas y Comunicaciones Instituto de Historia Antigua y Medieval Facultad de Filosofía y Letras Universidad de Buenos Aires Volumen 1 - 2005 ISSN: 1669-7286 http://www.filo.uba.ar/contenidos/investigacion/institutos/historiaantiguaymedieval/publicaciones.htm Actas y comunicaciones Del instituto de Historia antigua y medieval VOLUMEN 1 - 2005 ______________________________________________________________________ ARNALDO MOMIGLIANO Y LA HISTORIOGRAFÍA ITALIANA DEL SIGLO XX Hugo Zurutuza Universidad de Buenos Aires Fecha de recepción: febrero 2005 Fecha de aceptación: abril 2005 RESUMEN Los Contributi representan más de medio siglo de una tarea que se condensa en un rasgo historiográfico característico: el conocimiento crítico de la Antigüedad tiene que acompañarse de una frecuentación de la historiografía contemporánea e incorporar los problemas culturales de toda las épocas. Es así que decide instalar tanto el diálogo entre paganos, judíos y cristianos durante la Antigüedad como la inserción de la tradición judía en la vida política e intelectual de la Italia contemporánea. ABSTRACT The Contributi represent more than half century is a task that is condensed into a feature characteristic of historiography: the critical knowledge of antiquity must be accompanied by an attendance of contemporary historiography and incorporate cultural issues throughout the ages. This is how you choose to install both the dialogue between pagans, Jews and Christians in antiquity as the insertion of the Jewish tradition in the intellectual and political life of contemporary Italy PALABRAS CLAVES Arnaldo Momigliano – historiografía – Antigüedad Clásica - Fascismo KEY WORDS Arnaldo Momigliano – historiography – Classic Antiquity - Fascism * Conferencia presentada en el II Encuentro de Actualización y Discusión en Historia Antigua y Medieval” “Cuestiones historiográficas y representaciones históricas. -

Model Risk in the Pricing of Exotic Options

Model Risk in the Pricing of Exotic Options Jacinto Marabel Romo∗ José Luis Crespo Espert† [email protected] [email protected] Abstract The growth experimented in recent years in both the variety and volume of structured products implies that banks and other financial institutions have become increasingly exposed to model risk. In this article we focus on the model risk associated with the local volatility (LV) model and with the Vari- ance Gamma (VG) model. The results show that the LV model performs better than the VG model in terms of its ability to match the market prices of European options. Nevertheless, both models are subject to significant pricing errors when compared with the stochastic volatility framework. Keywords: Model risk, exotic options, local volatility, stochastic volatil- ity, Variance Gamma process, path dependence. JEL: G12, G13. ∗BBVA and University Institute for Economic and Social Analysis, University of Alcalá (UAH). Mailing address: Vía de los Poblados s/n, 28033, Madrid, Spain. The content of this paper represents the author’s personal opinion and does not reflect the views of BBVA. †University of Alcalá (UAH) and University Institute for Economic and Social Analysis. Mail- ing address: Plaza de la Victoria, 2, 28802, Alcalá de Henares, Madrid, Spain. 1 Introduction In recent years there has been a remarkable growth of structured products with embedded exotic options. In this sense, the European Commission1 stated that the use of derivatives has grown exponentially over the last decade, with over-the- counter transactions being the main contributor to this growth. At the end of December 2009, the size of the over-the-counter derivatives market by notional value equaled approximately $615 trillion, a 12% increase with respect to the end of 2008. -

Static Replication of Exotic Options Andrew Chou JUL 241997 Eng

Static Replication of Exotic Options by Andrew Chou M.S., Computer Science MIT, 1994, and B.S., Computer Science, Economics, Mathematics, Physics MIT, 1991 Submitted to the Department of Electrical Engineering and Computer Science in partial fulfillment of the requirements for the degree of Doctor of Philosophy at the MASSACHUSETTS INSTITUTE OF TECHNOLOGY June 1997 () Massachusetts Institute of Technology 1997. All rights reserved. Author ................. ......................... Department of Electrical Engineering and Computer Science April 23, 1997 Certified by ................... ............., ...... .................... Michael F. Sipser Professor of Mathematics Thesis Supervisor Accepted by .................................. A utlir C. Smith Chairman, Department Committee on Graduate Students .OF JUL 241997 Eng. •'~*..EC.•HL-, ' Static Replication of Exotic Options by Andrew Chou Submitted to the Department of Electrical Engineering and Computer Science on April 23, 1997, in partial fulfillment of the requirements for the degree of Doctor of Philosophy Abstract In the Black-Scholes model, stocks and bonds can be continuously traded to replicate the payoff of any derivative security. In practice, frequent trading is both costly and impractical. Static replication attempts to address this problem by creating replicating strategies that only trade rarely. In this thesis, we will study the static replication of exotic options by plain vanilla options. In particular, we will examine barrier options, variants of barrier options, and lookback options. Under the Black-Scholes assumptions, we will prove the existence of static replication strategies for all of these options. In addition, we will examine static replication when the drift and/or volatility is time-dependent. Finally, we conclude with a computational study to test the practical plausibility of static replication. -

Gli Italiani Sanno Morire»

“CONTEMPORANEA”, 2015, n. 2, pp. 245-266 (Editore Il Mulino) The definitive version is available publisher's home MASSIMO BAIONI «Gli italiani sanno morire». Una collana storica per le guerre del fascismo Nel 1934 la casa editrice Oberdan Zucchi di Milano annunciava l’esordio de La centuria di ferro, una collana di storia che sin dal titolo faceva presagire l’impianto delle cento agili biografie che avrebbero dovuto comporla. Caso paradigmatico della crescente militarizzazione della cultura, che negli anni Trenta si estese rapidamente anche agli studi storici, La centuria di ferro ambiva a qualificarsi come uno strumento di informazione in cui la veste divulgativa e la cifra ideologica si saldavano con eguale chiarezza d’intenti. L’obiettivo era quello di creare «una piccola enciclopedia del nostro Risorgimento», inteso volpianamente come un processo «in cammino». Dagli anni della prima guerra dell’indipendenza e dello statuto albertino fino al tempo presente, i volumi avrebbero dovuto documentare la genealogia della «grandezza» e della «supremazia politica» dell’Italia fascista, facendo risaltare l’apporto dato all’«immancabile destino» da uomini di pensiero e di azione, «di ogni classe e di ogni levatura»1. È noto che durante il Ventennio l’ipertrofia dei richiami al passato fu parte integrante dell’autorappresentazione del fascismo e insieme del processo di ri-nazionalizzazione degli italiani avviato dal regime. Sul terreno della divulgazione storica, anche a fronte delle nuove esigenze poste dalla società di massa, le iniziative furono perciò rilevanti e variamente articolate: tuttavia non si può dire che abbiano ricevuto un’attenzione storiografica paragonabile a quella che ha riguardato la produzione scientifica e l’organizzazione degli studi2. -

ANTONIO CEFALY 1852 Set

ANTONIO CEFALY 1852 set. 21 - 1928 giu. 12 SOMMARIO INTRODUZIONE.......................................................................................................................................2 ELENCO DEI FASCICOLI........................................................................................................................3 1. Corrispondenza, 1867 gen. 25 - 1928 giu. 12 .........................................................................................3 2. Fascicoli per argomento, 1852 set. 21 - 1928 mag. 3 .............................................................................9 INVENTARIO..........................................................................................................................................10 1. Corrispondenza, 1867 gen. 25 - 1928 giu. 12 ...................................................................................10 2. Fascicoli per argomento, 1852 set. 21 - 1928 mag. 3 .....................................................................134 INDICI ....................................................................................................................................................176 Fondo Antonio Cefaly INTRODUZIONE 1850, 10 novembre. Nasce a Cortale da Fortunato e dalla nobile Elisabetta Bevilacqua. 1871. È consigliere comunale di Cortale. 1873-1883. È sindaco di Cortale e, dal 1875, consigliere provinciale di Catanzaro. 1882-1895. È deputato, appartenente al gruppo "Liberale progressista". 1898, 17 novembre. È nominato senatore per la terza categoria -

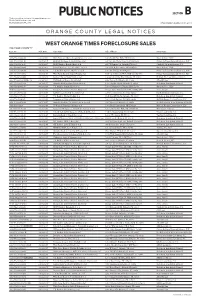

PUBLIC NOTICES SECTION B Find Your Notices Online At: Orangeobserver.Com, Floridapublicnotices.Com and Businessobserverfl.Com THURSDAY, AUGUST 10, 2017

PUBLIC NOTICES SECTION B Find your notices online at: OrangeObserver.com, FloridaPublicNotices.com and BusinessObserverFL.com THURSDAY, AUGUST 10, 2017 ORANGE COUNTY LEGAL NOTICES WEST ORANGE TIMES FORECLOSURE SALES ORANGE COUNTY Case No. Sale Date Case Name Sale Address Firm Name 2016-CA-010947-O 08/10/2017 Wells Fargo vs. Alberto Joseph Greaves etc et al Lot 1, North Pine Hills, PB X Pg 107 Brock & Scott, PLLC 2014-CA-010192-O 08/11/2017 Suntrust Mortgage vs. Bank D Ngo et al Lot 32, Lake Gloria Preserve, PB 41 Pg 18 Phelan Hallinan Diamond & Jones, PLC 2014-CA-011052-O 08/11/2017 HSBC Bank vs. Braulio Marte et al 8155 Wellsmere Cir, Orlando, FL 32835 Clarfield, Okon & Salomone, P.L. 2015-CA-006594-O 08/11/2017 Central Mortgage vs. Jeffrey Stine etc et al Lot 2, Blk D, Sweetwater, PB 13 PG 64 Brock & Scott, PLLC 2016-CA-010076-O 08/14/2017 U.S. Bank vs. Kevin L Mueller etc et al Lot 1, Park Ridge, PB O Pg 100 Phelan Hallinan Diamond & Jones, PLC 2016-CA-000507-O 08/14/2017 Wells Fargo Bank vs. Daniel Regala et al Unit 5-207, Visconti West, ORB 8253 Pg 1955 Phelan Hallinan Diamond & Jones, PLC 2015-CA-0083190O 08/14/2017 Andover Cay vs. David Molina et al 4339 Andover Cay Blvd, Orlando, FL 32825 Di Masi, The Law Offices of John L. 2015-CA-009749-O Div. 34 08/14/2017 PNC Bank vs. Sharon Wright et al 4918 Cortez Dr, Orlando, FL 32808 Albertelli Law 2013-CA-008254-O 08/14/2017 Deutsche Bank vs. -

Arnaldo Momigliano Y La Historiografía Italiana Del Siglo XX

A Arnaldo Momigliano y la historiografía italiana del siglo XX Zurutuza, Hugo Revista :Actas y comunicaciones del Instituto de Historia Antigua y Medieval 2005, 1 Artículo 1 Revista electrónica anual: Actas y Comunicaciones Instituto de Historia Antigua y Medieval Facultad de Filosofía y Letras Universidad de Buenos Aires Volumen 1 - 2005 ISSN: 1669-7286 http://www.filo.uba.ar/contenidos/investigacion/institutos/historiaantiguaymedieval/publicaciones.htm ACTAS Y COMUNICACIONES DEL INSTITUTO DE HISTORIA ANTIGUA Y MEDIEVAL VOLUMEN 1 - 2005 ______________________________________________________________________ ARNALDO MOMIGLIANO Y LA HISTORIOGRAFÍA ITALIANA DEL SIGLO XX Hugo Zurutuza Universidad de Buenos Aires RESUMEN Los Contributi representan más de medio siglo de una tarea que se condensa en un rasgo historiográfico característico: el conocimiento crítico de la Antigüedad tiene que acompañarse de una frecuentación de la historiografía contemporánea e incorporar los problemas culturales de toda las épocas. Es así que decide instalar tanto el diálogo entre paganos, judíos y cristianos durante la Antigüedad como la inserción de la tradición judía en la vida política e intelectual de la Italia contemporánea. ABSTRACT The Contributi represent more than half century is a task that is condensed into a feature characteristic of historiography: the critical knowledge of antiquity must be accompanied by an attendance of contemporary historiography and incorporate cultural issues throughout the ages. This is how you choose to install both the dialogue