MENA • Edge Computing Opens New Opportunities for 5G • Operators Step up Data-Centre Investments

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report 2018

Pakistan Telecommunication Company Limited Company Telecommunication Pakistan PTCL PAKISTAN ANNUAL REPORT 2018 REPORT ANNUAL /ptcl.official /ptclofficial ANNUAL REPORT Pakistan Telecommunication /theptclcompany Company Limited www.ptcl.com.pk PTCL Headquarters, G-8/4, Islamabad, Pakistan Pakistan Telecommunication Company Limited ANNUAL REPORT 2018 Contents 01COMPANY REVIEW 03FINANCIAL STATEMENTS CONSOLIDATED Corporate Vision, Mission & Core Values 04 Auditors’ Report to the Members 129-135 Board of Directors 06-07 Consolidated Statement of Financial Position 136-137 Corporate Information 08 Consolidated Statement of Profit or Loss 138 The Management 10-11 Consolidated Statement of Comprehensive Income 139 Operating & Financial Highlights 12-16 Consolidated Statement of Cash Flows 140 Chairman’s Review 18-19 Consolidated Statement of Changes in Equity 141 Group CEO’s Message 20-23 Notes to and Forming Part of the Consolidated Financial Statements 142-213 Directors’ Report 26-45 47-46 ہ 2018 Composition of Board’s Sub-Committees 48 Attendance of PTCL Board Members 49 Statement of Compliance with CCG 50-52 Auditors’ Review Report to the Members 53-54 NIC Peshawar 55-58 02STATEMENTS FINANCIAL Auditors’ Report to the Members 61-67 Statement of Financial Position 68-69 04ANNEXES Statement of Profit or Loss 70 Pattern of Shareholding 217-222 Statement of Comprehensive Income 71 Notice of 24th Annual General Meeting 223-226 Statement of Cash Flows 72 Form of Proxy 227 Statement of Changes in Equity 73 229 Notes to and Forming Part of the Financial Statements 74-125 ANNUAL REPORT 2018 Vision Mission To be the leading and most To be the partner of choice for our admired Telecom and ICT provider customers, to develop our people in and for Pakistan. -

National Steel Bridge Alliance

NATIONAL STEEL BRIDGE ALLIANCE World’s Longest Bridge Spans Type of Bridge Page Suspension 1 Cable-stayed steel girder and truss 7 Cable-stayed prestressed concrete girder 13 Bridges with shop-fabricated PWS cables 16 Steel arch 19 Concrete arch 22 Cantilever truss 24 Continuous truss 27 Simple truss 29 Continuous steel plate- and box-girder 31 Prestressed concrete girder 35 Compiled by: Jackson Durkee, C.E., P.E. Consulting Structural Engineer 217 Pine Top Trail Bethlehem, Pennsylvania 18017 Note: Information has been taken from sources believed to be reliable but cannot be guaranteed. May 24, 1999 1 SUSPENSION BRIDGES Year Main Span Bridge Location Completed (ft) Design Engineer Superstructure Contractor Messina Strait Sicily - mainland Italy UD 10827 Stretto di Messina, SpA Akashi Strait1 Kobe-Naruto Route, Japan 1998 6532 Honshu-Shikoku Bridge Authority Izmit Bay Turkey UD 5538 Anglo Japanese Turkish Consortium Design engineer15 – Kvaerner, Enka, IHI, MHI, NKK Great Belt (East Bridge)5 Denmark 1998 5328 COWIConsult Coinfra SpA - SDEM Humber Hull, England 1981 4626 Freeman Fox British Bridge Builders Jiangyin1,5 Jiangyin, China 1999 4544 Highway Planning & Design Institute Kvaerner Cleveland Bridge - - Tongyi University - Jiangsu Shanghai Pujiang Cable Province - Mott MacDonald Tsing Ma2 Hong Kong 1997 4518 Mott MacDonald Kvaerner Cleveland Bridge Verrazano Narrows New York City 1964 4260 Ammann & Whitney American Bridge - Bethlehem - Harris Golden Gate San Francisco 1937 4200 Joseph B. Strauss, Charles Ellis Bethlehem - Roebling Höga -

1 June 8, 2020 to Members of The

June 8, 2020 To Members of the United Nations Human Rights Council Re: Request for the Convening of a Special Session on the Escalating Situation of Police Violence and Repression of Protests in the United States Excellencies, The undersigned family members of victims of police killings and civil society organizations from around the world, call on member states of the UN Human Rights Council to urgently convene a Special Session on the situation of human rights in the United States in order to respond to the unfolding grave human rights crisis borne out of the repression of nationwide protests. The recent protests erupted on May 26 in response to the police murder of George Floyd in Minneapolis, Minnesota, which was only one of a recent string of unlawful killings of unarmed Black people by police and armed white vigilantes. We are deeply concerned about the escalation in violent police responses to largely peaceful protests in the United States, which included the use of rubber bullets, tear gas, pepper spray and in some cases live ammunition, in violation of international standards on the use of force and management of assemblies including recent U.N. Guidance on Less Lethal Weapons. Additionally, we are greatly concerned that rather than using his position to serve as a force for calm and unity, President Trump has chosen to weaponize the tensions through his rhetoric, evidenced by his promise to seize authority from Governors who fail to take the most extreme tactics against protestors and to deploy federal armed forces against protestors (an action which would be of questionable legality). -

Pdf 8 Methodology Development, Ranking Digital Rights

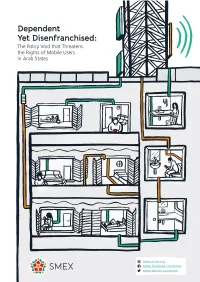

SMEX is a Beirut-based media development and digital rights organization working to advance self-regulating information societies. Our mission is to defend digital rights, promote open culture and local content, and encourage critical engagement with digital technologies, media, and networks through research, knowledge-sharing, and advocacy. Design, illustration concept, and layout are by Salam Shokor, with assistance from David Badawi. Illustrations are by Ahmad Mazloum and Salam Shokor. www.smex.org A 2018 Publication of SMEX Kmeir Building, 4th Floor, Badaro, Beirut, Lebanon © Social Media Exchange Association, 2018 This work is licensed under a Creative Commons Attribution-ShareAlike 4.0 International License. Acknowledgments Afef Abrougui conceptualized this research report and designed and oversaw execution of the methodology for data collection and review. Research was conducted between April and July 2017. Talar Demirdjian and Nour Chaoui conducted data collection. Jessica Dheere edited the report, with proofreading assistance from Grant Baker. All errors and omissions are strictly the responsibility of SMEX. This study would not have been possible without the guidance and feedback of Rebecca Mackinnon, Nathalie Maréchal, and the whole team at Ranking Digital Rights (www.rankingdigitalrights.org). RDR works with an international community of researchers to set global standards for how internet, mobile, and telecommunications companies should respect freedom of expression and privacy. The 2017 Corporate Accountability Index ranked 22 of the world’s most powerful such companies on their disclosed commitments and policies that affect users' freedom of expression and privacy. The methodology developed for this research study was based on the RDR/ CAI methodology. We are also grateful to EFF’s Katitza Rodriguez and Access Now’s Peter Micek, both of whom shared valuable insights and expertise into how our research might be transformed and contextualized for local campaigns. -

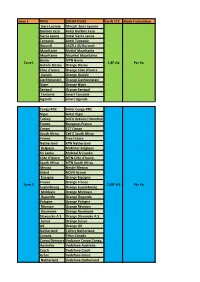

Zone 1 PAYS OPERATEURS Tarifs TTC Mode Facturation Siera

Zone 1 PAYS OPERATEURS Tarifs TTC Mode Facturation Siera Leonne Africell Siera Leonne Burkina Faso Airtel Burkina Faso Sierra Leone Airtel Sierra Leone Tanzanie Airtel Tanzanie Burundi LACELL SU Burundi Mauritanie Mattel Mauritania Mauritanie Mauritel Mauritanie Benin MTN Benin Zone1 1,8F cfa Par Ko Guinée Bissau Orange Bissau Côte d'Ivoire Orange Côte d'Ivoire Guinée Orange Guinée Liechteinstein Orange Liechteinstein Niger Orange Niger Senegal Orange Senegal Tanzanie Smart Tanzanie Uganda Smart Uganda Congo RDC Airtel Congo RDC Niger Airtel Niger Turkey AVEA Iletisim Hizmetleri A.S. (Aycell) Turkey France Bouygues France Congo CCT Congo South Africa Cell C South Africa France Free France Netherland KPN Netherland Belgique Mobistar Belgique Sri Lanka Mobitel Sri Lanka Côte d'Ivoire MTN Côte d'Ivoire South Africa MTN South Africa Mexico Nextel Mexico Island NOVA IsLand Espagne Orange Espagne France Orange France Zone 2 2,95F cfa Par Ko Luxembourg Orange Luxembourg Moldavie Orange Moldavie Ouganda Orange Ouganda Pologne Orange Pologne Réunion Orange Réunion Roumanie Orange Roumanie Slovensko A.S. Orange Slovensko A.S. Suisse Orange Suisse UK Orange UK Netherland Telfort Netherland Canada Telus Canada Congo DemocraticVodacom Congo Congo, Democratic Republic of the Australia Vodafone Australia Czech Vodafone Czech Grèce Vodafone Grèce Netherland Vodafone Netherland Belgique Base Belgique Belgacom Belgacom Benin Moov Benin Canada Rogiers Canada Canada Microcel Canada Swiss Com Swiss Com Côte d'Ivoire Moov Côte d'Ivoire Cap Vert Cap Vert Mobile -

Post-Paid Autoroamtm

Post-Paid AutoroaMtM Using yoUr Post-Paid Mobile overseas Optus AutoRoam™ lets you stay in touch while you’re travelling through some of the most popular overseas destinations. Post-Paid autoroam™ gives you these great benefits: • Stay in touch with your family and friends even when you are on holidays, day or night. • There’s no need for expensive hotel phones or the inconvenience of public phones. • Your mobile number doesn’t change, which means your contacts can call you without having to remember another number. • Callers in Australia are only charged for a national call to you while you are overseas. • Depending on your overseas carrier, you can screen your incoming calls and divert those you don’t want to answer to voicemail.# as an optus Post-Paid customer, you can: • SMS ‘A’ to 321 and VoiceMail will call you back (standard roaming charges apply)~ or • Access VoiceMail by calling +61 4 1100 0321 (standard roaming charges apply) • For general or billing enquiries while overseas, please call Optus Customer Care on +61 2 8082 5678. (50¢ per call). Optus Customer Care is open from 8am – 7pm (AEST) Mon to Fri and 9am – 5pm (AEST) on Saturdays. • And for faults with your mobile phone, you can call +61 2 8082 2642 for assistance. The Mobile Technical Support Centre is open 24 hours a day, 7 days a week. For your convenience, all your overseas charges are billed back to your Optus account in Australian dollars. ConvenienCe of data roaMing While the ability to use your regular data services overseas is convenient, it’s good to know how data is charged when roaming. -

Bridge Alliance and the Global M2M Association Collaborate to Drive Worldwide Growth in M2M and Internet of Things Markets

EMBARGOED For release on February 17, 2016, 10am CET Bridge Alliance and the Global M2M Association collaborate to drive worldwide growth in M2M and Internet of Things markets The new partnership between both organizations will focus on the joint provision of their advanced Multi-Domestic Service across 77 markets worldwide The Multi-Domestic Service, a single global connectivity management platform and common eUICC SIM solution, embraces the GSMA Remote SIM Provisioning specification – the world’s first alliance-to-alliance remote provisioning of an eUICC SIM. The joint service will be demonstrated by the GMA and Bridge Alliance at the Mobile World Congress 2016, Innovation City, Stand A11 in Hall 3 Bridge Alliance and the Global M2M Association (GMA) today announce their new partnership and the live demonstration of their advanced Multi-Domestic Service, a single global connectivity management platform including an eUICC SIM, which can be used in 77 markets throughout their combined footprints. The Multi-Domestic Service will be demonstrated in conjunction with the Samsung KNOX Enterprise Billing capabilities by AIS and Taiwan Mobile on behalf of Bridge Alliance, and the GMA at the Mobile World Congress 2016, Innovation City, Stand A11 in Hall 3. The partnership will provide a seamless customer experience with worldwide coverage and superior quality of service, allowing device manufacturers, enterprises, and service providers to easily deploy their Internet of Things (IoT) and Machine-to-Machine (M2M) services. The Multi- Domestic Service is a global solution to address the local opportunities for higher bandwidth applications and new business models. It significantly reduces barriers for enterprises, keeping total cost of ownership low while maximizing quality of service. -

Privilegedlifestyle

SingTel-UOB Platinum Card Exclusive privileged lifestyle Live it up with smaller bills and sweeter benefits Up to 3% rebate on Free card for life Redeem free phones your SingTel bills with your SMART$ Bridge DataRoam Enjoy Free registration and 10% off monthly subscription with 12-month sign-up of Your travel essential. Bridge DataRoam! Bridge Bridge Bridge 5 15 40 One flat rate across DataRoam DataRoam DataRoam One-time Asia Pacific. Registration Waived Waived Waived Monthly Subscription $24.00 $48.00 $96.00 Monthly Subscription $21.60 $43.20 $86.40 (Promotional Rate) Bundled Value 5MB 15MB 40MB Bridge DataRoam is applicable for usage across the 10 countries of the Bridge Alliance member networks which include: Australia - Optus, Hong Kong - CSL, India - Airtel, Indonesia - Telkomsel, Korea - SK Telecom, Macau - CTM, Malaysia - Maxis, Philippines - Globe, Taiwan - Taiwan Mobile, Thailand - AIS. To subscribe, please visit any hello! store. Terms and Conditions • Valid till 31 Oct 2008 • 10% discount on subscription is applicable with 12 months Bridge DataRoam5, Bridge DataRoam15 or Bridge DataRoam40 contract • For usage beyond the data bundle, subscribers will be charged the prevailing data roaming rate • Bridge DataRoam price plan is only applicable for usage when roaming overseas on Bridge Alliance member networks. If you are logged on to a non-Bridge Alliance member network, the prevailing data roaming charges Enjoy up to 90% will apply • Early termination charges apply on unfulfilled 12 months Bridge savings on your DataRoam5, Bridge -

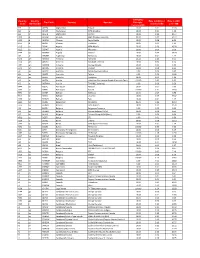

Country Code Country ISO Number Tap Code Country Operator

Charging Country Country Rate in USD per Rate in USD Tap Code Country Operator Principle Code ISO Number increment kb per 1 MB increment kb +93 af AFGEA Afghanistan Etisalat 10.00 0.11 11.18 +93 af AFGAR Afghanistan MTN (Areeba) 10.00 0.01 1.30 +93 af AFGTD Afghanistan Roshan 10.00 0.10 10.27 +355 al ALBAM Albania AMC (Telekom Albania) 50.00 0.49 10.13 +355 al ALBEM Albania Eagle Mobile 10.00 0.08 8.02 +355 al ALBVF Albania Vodafone 10.00 0.01 1.13 +213 dz DZAA1 Algeria ATM-Mobilis 20.00 0.20 10.28 +213 dz DZAWT Algeria Wataniya 10.00 0.00 0.30 +244 ao AGOMV Angola Movicel 10.00 0.14 13.99 +54 ar ARGTM Argentina Telefonica 10.00 0.01 1.42 +374 am ARM01 Armenia Armentel 10.24 0.10 9.65 +374 am ARMKT Armenia Karabakh Telecom 10.00 0.08 8.24 +374 am ARMOR Armenia Orange (Ucom) 10.00 0.01 1.09 +374 am ARM05 Armenia VivaCell 10.00 0.08 8.24 +61 au AUSOP Australia Optus Communications 1.00 0.00 0.33 +61 au AUSTA Australia Telstra 1.00 0.02 21.02 +61 au AUSVF Australia Vodafone 10.00 0.01 1.10 +43 at AUTCA Austria Hutchison Drei Austria GmbH (Connect- One/ Orange) 100.00 0.83 8.53 +43 at AUTMM Austria T MOBILE (telering) 1.00 0.00 0.58 +994 az AZEAC Azerbaijan Azercell 10.00 0.07 7.00 +994 az AZEBC Azerbaijan Bakcell 100.00 1.71 17.50 +973 bh BHRBT Bahrain BATELCO 10.00 0.07 6.98 +973 bh BHRST Bahrain Viva STC 10.00 0.19 19.02 +973 bh BHRMV Bahrain Zain 10.00 0.01 1.17 +880 bd BGDBL Bangladesh Banglalink 50.00 0.49 10.10 +375 by BLRMD Belarus MDC Velcom 10.00 0.12 12.78 +32 be BELTB Belgium Belgacom-Proximus 1.00 0.00 0.62 +32 be BELMO Belgium -

Annual Report 2017 Financial Highlights

To access the digital version, please visit our Annual Report microsite at: http://mobily.im/annualreport-en Rising to the Challenge Annual Report 2017 Financial Highlights Operational Cash Flow (EBITDA–CAPEX) Deleveraging (Net Debt and Net Debt / EBITDA) (SAR million) (SAR million) +60.8% -9.3% 2,000 14,000 13,993 12,687 12,000 12,527 1,378 10,000 1,000 857 8,000 6,000 3.5x 3.5x 0 4.26x 4,000 (543) 2,000 -1,000 0 2015* 2016 2017 2015* 2016 2017 Net Debt Net Debt/EBITDA This year was an important turning point for Mobily, in which the Revenues EBITDA and EBITDA Margin Company developed and articulated a new corporate strategy for growth (SAR million) (SAR million) to 2019 and beyond. -9.7% -10.4% 15,000 5,000 14,424 4,000 12,569 4,069 10,000 11,351 3,000 3,646 32% 2,941 2,000 32% 5,000 1,000 20% 0 0 2015* 2016 2017 2015* 2016 2017 EBITDA EBITDA Margin Net Income/(Loss) (SAR million) 0 -200 (214) -400 -600 (709) -800 -1,000 (1,093) -1,200 2015* 2016 2017 *FY 2015 figures are not IFRS. 2017 at A Glance Table of Contents Company Profile 2x5 MHz 01 04 Governance new spectrum acquisition About Mobily 08 Board of Directors 48 Vision and Values 09 Executive Management 58 Chairman’s Statement 10 Related Party Transactions 60 Rising to the Challenge 12 Compensation and Remuneration 61 Geographic Footprint 14 About Mobily 62 Achievements and Awards 16 Important Events 65 Shareholder Information and Key Forward-looking Statements 66 18 Announcements Social Responsibility 67 46 Shareholders 68 Mobily Elite fourth-batch recruits Dividend Policy 70 -

AT&T and Bridge Alliance Collaborate to Strengthen Global Connected

NEWS RELEASE AT&T and Bridge Alliance Collaborate to Strengthen Global Connected Car Leadership 2/28/2017 BARCELONA, Spain, Feb. 28, 2017 /PRNewswire/ -- AT&T* and members of Bridge Alliance have formed a long-term agreement to extend their global connected car leadership to new territories.Bridge Alliance is a leading group of mobile carriers in Asia Pacic, the Middle East and Africa. Today, AT&T connects more than 11 million cars in the United States and abroad. Together, the two organizations expect to grow the number of connected cars on the road."Teaming with members of Bridge Alliance helps simplify global deployments with local operator networks in these regions," said Chris Penrose, President, Internet of Things Solutions, AT&T. "This is huge for our automotive customers. It gives them an opportunity to access customers in countries which collectively cover nearly 30% of the world's population." This collaboration sets forth the framework to extend the geographic coverage AT&T could provide to automotive manufacturers looking to enhance their infotainment oerings in the growth markets served by members of Bridge Alliance. This will help the 22 global automotive and long-haul truck brands that AT&T works with create an improved driving experience for their global customer base.For the customers collectively served by Bridge Alliance, this helps to give them access to solutions like Wi-Fi hotspots, internet radio and live trac. Until now, these features have been more dicult for automotive manufacturers to implement globally. "Our collaboration with AT&T is based on the alignment and integration of processes, platforms and propositions. -

Using Intrinsic Values in Advertising Campaign: a Social Awareness Approach Associ

مجلة العمارة والفنون والعلوم اﻻنسانية - المجلد الخامس - العدد الرابع والعشرون نوفمبر 2020 Using Intrinsic Values in Advertising Campaign: A Social Awareness Approach Associ. Prof. Dr. Aliaa Turafy Associate Professor in Advertising, Mass Communication Department, Faculty of Al- Alsun & Mass Communication, Misr International University [email protected] Abstract: Materialistic values have become the primary status of most Egyptian society. This may be due to their attempts to satisfy some of their needs by owning things. Many institutions have been able to take advantage of this trend as a mean of selling points, and even using the idea of the ego. Nowadays, the concept of corporate responsibility has been widespread and it can be defined as "the foundation voluntarily by material, or moral contributions undertaken according to the response of the needs and expectations of its internal and external audiences". In addition, most institutions rely on advertising to advertise their products, services, or ideas. Accordingly, the importance of this research is attempting to add intrinsic values in advertising campaign design taking it as an advantage to play a social awareness role and achieve the communicative goals of the advertiser. Intrinsic values represent the value or meaning of the thing in itself, and the fundamental human values that emanate from the individual himself/herself and are not valuables, whereas these values serve the human benefit. The research aims to develop a strategy to help advertising campaigns use the intrinsic values which include social, personal, and environmental values in design of advertising campaign to achieve; first the advertiser’s aims and second the community service of the institution maintaining the moral framework as a social awareness edge for the target audience.