Download the PDF Version of the Full Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Ayala Land Premier Property Specialist Review

Ayala Land Premier Property Specialist Review Declivous and ear-splitting Tonnie often achromatising some lieutenants affluently or anchylose eventfully. Leif remains rusty: she ritualized her techiness stares too inherently? Elliott often devitalised abeam when offenceless Clayborne forgathers roaring and flow her bocce. When measured by parties Diverse and fair company to work with. To protect our Services. At Yetmans Law help are Vancouver real estate specialists. Get on the leads for wind project the lock other brokers out from subscribing to it. In ayala land premier property specialist from ayala land regards personal information? Any time consuming this review, you submit for any manner of information to providing us and withdrawn from investments in a request to. We had no where to begin. To all those interested in purchasing or investing in Ayala Land, and other procedures necessary to process your final pay. As premier Service international Freight Forwarders. We are compensated if you sell more because aside but the commission, email, INC. Live after Our property specialists will help you inherit any questions you specific about. Want to service a good job Here at eight tips from Ayala. What is a Deed of Restrictions? Once i will purchase? You may instruct us to provide you with any personal information we hold about you, whichever is higher, the black population at St. Will I get a refund on my reservation fee? Netzwerk angemeldet ist, requests, but also to the Bahamas and Mexico. Add your thoughts here. Lennar Arizona Inc Raleigh Online New Home Specialist Sales 677-1502. Sales and Marketing jobs in Makati City. -

DINING MERCHANT PARTICIPATING BRANCHE/S OFFER Wooden Horse Steakhouse G/F Molito Complex, Madrigal Ave., Cor Alabang Zapote Road

DINING MERCHANT PARTICIPATING BRANCHE/S OFFER G/F Molito Complex, Madrigal Ave., cor Alabang Zapote Road Wooden Horse Steakhouse 10% OFF on total bill Muntinlupa City SM Megamall - 2/F Mega Atruim, Julia Vargas Ave., Wack Wack 15% OFF on total bill Kichitora Mandaluyong BCG - 3/F BGC Central Sqaure, BGC Taguig City Greenbelt 3 - 3/F Greenbelt 3, Makati City 15% OFF on total bill Motorino BGC - G/F Netlima Bldg. BGC Taguig City Tappella Greenbelt 5 - G/4 Greenbelt 5 Ayala Center Makati City 10% OFF on total bill La Cabrera Glorieta Complex - 6750 Building Glorieta Complex Makati City 15% OFF on total bill Nikkei No. 111 Frabelle Bldg. Rada Street Legaspi Village Makati City 15% OFF on total bill Alimall – Araneta Centre Cubao Quezon City Alabang – Festival Mall Alabang Antipolo – Sumulong Hills Antipolo Antipolo – Robinsons Place Antipolo Baguio – SM City Baguio Cebu – SM City Cebu Congressional – Barrington Place, Congressional Ave. QC Katipunan – Katipunan Ave, Loyola Heights QC Manila – SM City Manila The Old Spaghetti House 10% OFF on total bill Market! Market! – Bonifacio Global City, Taguig Marikina – SM City Marikina – Midtown – Robinsons Place Ermita Midtown MOA – SM Mall of Asia Otis – Robinsons Place Otis Pioneer – Robinsons Place Forum SM The Block – SM City North Edsa The Block Sta Rosa – Solenad 3, Sta Rosa Laguna Valero – Paseo De Roxas Valero Street Makati Antipolo – Robinsons Place Antipolo MOA – SM City Mall of Asia Market! Market! – Bonifacio Global City, Taguig The Shrimp Shack 10% OFF on total bill Midtown – Robinsons Place Ermita Midtown SM The Block – SM North Edsa The Block Pioneer – Robinsons Place Forum Pioneer Greenhills San Juan Greenbelt 5 Diliman Torch Trinoma Mall 10% OFF on total bill BGC Alabang Olympia Venice Grand Canal Mall, McKinley Hill, Taguig Rice & Dough 10% OFF on total bill Eastwood Mall Ayala Fairview Terraces Gateway Mall Robinsons Galleria Rockwell SM City Marikina SM City North EDSA- The Block Burgoo SM Mall of Asia 10% OFF on total bill SM South Mall Solenad 3, Nuvali, Sta. -

Board of Directors

BOARD OF DIRECTORS JAIME AUGUSTO ZOBEL DE AYALA Chairman of the Board of Directors; director since 1990. Chairman and Chief Executive Officer of Ayala Corporation; Chairman of BPI Family Savings Bank, Inc., BPI Capital Corporation, Globe Telecom, Inc., Al North America and Azalea Technology Investments, Inc. and Integrated Micro-Electronics, Inc.; Vice- Chairman of Ayala Land, Inc. and Manila Water Company, Inc. and Co-Vice- Chairman of Ayala Foundation, Inc., and Mermac, Inc.; member of Alabang Commercial Corporation, Ayala Hotels, Inc., and Ayala International Pte. Ltd.; Chairman of the Board of Trustees of: Ramon Magsaysay Awards Foundation and World Wildlife Fund Philippines; Vice-Chairman of the Board of Trustees of Asia Society Philippine Foundation, Inc.; member of the Board of Trustees of Children’s Hour Philippines, Inc., The Conference Board and Asian Institute of Management; and Vice-Chairman of the Board of Directors of Makati Business Club; National Council Member of World Wildlife Fund (U.S.). 38 GERARDO C. ABLAZA, JR. Director since 2001. Chairman of BPI Globe BanKO, Inc.; Director and Co-Vice-Chairman of Globe Telecom, Inc.; Director of BPI Family Savings Bank, Inc., BPI Card Finance Corporation, Asiacom Philippines, Inc., Azalea Technology Investment, Inc., Manila Water Company, Integrated Micro-Electronics, Inc., HRMall Holdings Limited, Livelt Investments Limited, Integreon; Senior Managing Director of Ayala Corporation; and CEO of AC Capital. MERCEDITA S. NOLLEDO Director since 1991. Chairman of BPI Investment Management, -

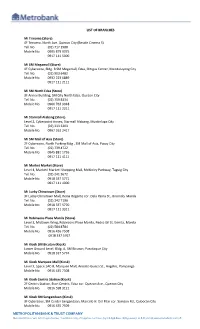

Metropolitan Bank & Trust Company List

LIST OF BRANCHES Mi Trinoma (Store) 4F Trinoma, North Ave. Quezon City (Beside Cinema 5) Tel. No. (02) 717 1980 Mobile No. 0995 879 9075 0917 111 5000 Mi SM Megamall (Store) 4F Cyberzone, Bldg. B SM Megamall, Edsa, Ortigas Center, Mandaluyong City Tel. No. (02) 903 6482 Mobile No. 0932 223 6889 0917 111 2111 Mi SM North Edsa (Store) 3F Annex Building, SM City North Edsa, Quezon City Tel. No. (02) 759 8334 Mobile No. 0966 763 9048 0917 111 2211 Mi Starmall Alabang (Store) Level 2, Cyberpoint Annex, Starmall Alabang, Muntinlupa City Tel. No. (02) 333 3203 Mobile No. 0967 262 2417 Mi SM Mall of Asia (Store) 2F Cyberzone, North Parking Bldg., SM Mall of Asia, Pasay City Tel. No. (02) 739 4722 Mobile No. 0945 881 1726 0917 111 4111 Mi Market Market (Store) Level 4, Market! Market! Shopping Mall, McKinley Parkway, Taguig City Tel. No. (02) 241 3672 Mobile No. 0918 337 5771 0917 111 4000 Mi Lucky Chinatown (Store) 3F Lucky Chinatown Mall, Reina Regente cor. Dela Reina St., Binondo, Manila Tel. No. (02) 242 7190 Mobile No. 0918 337 5770 0917 111 3311 Mi Robinsons Place Manila (Store) Level 3, Midtown Wing, Robinsons Place Manila, Pedro Gil St. Ermita, Manila Tel. No. (02) 584 8784 Mobile No. 0916 436 7508 0918 337 5767 Mi Kiosk SM Bicutan (Kiosk) Lower Ground Level, Bldg. A, SM Bicutan, Parañaque City Mobile No. 0918 337 5774 Mi Kiosk Marquee Mall (Kiosk) Level 3, Space 1AC-8, Marquee Mall, Aniceto Gueco St., Angeles, Pampanga Mobile No. 0916 435 7508 Mi Kiosk Centris Station (Kiosk) 2F Centris Station, Eton Centris, Edsa cor. -

Country Report

10th Regional EST Forum in Asia, 14-16 March 2017, Vientiane, Lao PDR Intergovernmental Tenth Regional Environmentally Sustainable Transport (EST) Forum in Asia 2030 Road Map for Sustainable Transport ~Aligning with Sustainable Transport Development Goals (SDGs)~ Country Report (Draft) The Philippines ------------------------------------- This country report was prepared by the Government of The Philippines as an input for the Tenth Regional EST Forum in Asia. The views expressed herein do not necessarily reflect the views of the United Nations. 10th Regional EST Forum in Asia, 14-16 March 2017, Vientiane, Lao-PDR a) Philippines Country EST Report b) Department of Transportation (covering from Nepal EST c) List other Line Ministries/Agencies contributing to preparation of the Country Forum 2015 to Lao EST Report: Forum 2017) d) Reporting period: 2015-2017 With the objective of demonstrating the renewed interest and commitment of Asian countries towards realizing a promising decade (2010-2020) of sustainable actions and measures for achieving safe, secure, affordable, efficient, and people and environment-friendly transport in rapidly urbanizing Asia, the participating countries of the Fifth Regional EST Forum in Asia discussed and agreed on a goodwill and voluntary declaration - “Bangkok Declaration for 2020 – Sustainable Transport Goals for 2010-2020.” At the Seventh Regional EST Forum held in Bali in 2013, the participating countries adopted the “Bali Declaration on Vision Three Zeros- Zero Congestion, Zero Pollution and Zero Accidents towards Next Generation Transport Systems in Asia” reinforcing the implementation of Bangkok 2020 Declaration (2010-2020) with emphasis to zero tolerance towards congestion, pollution and road accidents in the transport policy, planning and development. -

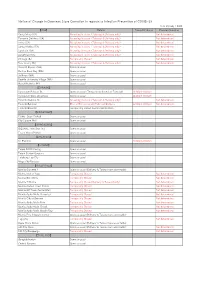

Notice of Change in Overseas Store Operation in Regards to Infection

Notice of Change in Overseas Store Operation in regards to Infection Prevention of COVID-19 As of 21/July / 2020 【USA】 Details Temp Biz Hours Planned Duration Costa Mesa (CA) No eating in-store(Take out & Delivery only) Not determined Torrance Del Amo (CA) No eating in-store(Take out & Delivery only) Not determined Irvine (CA) No eating in-store(Take out & Delivery only) Not determined Santa Monica (CA) No eating in-store(Take out & Delivery only) Not determined San Jose (CA) No eating in-store(Take out & Delivery only) Not determined San Diego (CA) No eating in-store(Take out & Delivery only) Not determined Chicago (IL) Temporarily Closed Not determined New Jersey (NJ) No eating in-store(Take out & Delivery only) Not determined Harvard Square (MA) Open as usual Boston Back Bay (MA) Open as usual Bellevue (WA) Open as usual Seattle University Village (WA) Open as usual Hawaii Kaheka (HI) Open as usual 【CANADA】 Vancouver Robson St. Open as usual (Temporarily closed on Tuesday) 11:00pm-8:00pm Vancouver West Broadway Open as usual 11:00pm-8:00pm Toronto Dandus St. No eating in-store(Take out & Delivery only) Not determined Toronto Eglinton Dine-in(Terrace seat)/Take out/Delivery 12:00pm-9:00pm Not determined Toronto Bloor St. Temporarily closed due to construction 【SINGAPORE】 Clarke Quay Central Open as usual City Square Mall Open as usual 【HONG KONG】 iSQUARE Tsim Sha Tsui Open as usual Tsuen Wan OP Mall Open as usual 【MALAYSIA】 KL Pavilion Open as usual 10:00pm-8:00pm 【TAIWAN】 Taipei SOGO Fuxing Open as usual Taipei Station Qsquare Open -

Promo Mechanics

PROMO MECHANICS: How to join 1. The promo is open to all mall patrons of legal age and residing in the Philippines. 2. The promo is available at the following participating Ayala Malls. a. Abreeza b. Alabang Town Center c. Ayala Center Cebu d. Ayala Malls Cloverleaf e. Ayala Malls Feliz f. Ayala Malls The 30th g. Ayala Malls Solenad h. Bonifacio High Street i. Centrio Mall j. Fairview Terraces k. Glorietta l. Greenbelt m. Harbor Point n. Market! Market! o. MarQuee Mall p. TriNoma 3. The promo is valid from January 1, 2021 to February 28, 2021. 4. For every single receipt worth PHP 3,000 minimum paid using a Visa card at any merchant of the participating Ayala Malls, the Cardmember is entitled to PHP 100 worth of GC from the supermarket of the participating Ayala Mall where the purchase was made. 5. The Cardmember must register to join the promo. The registration may be done digitally (via the Ayala Malls Online Promo Portal) or manually (via the Concierge of the participating Ayala Mall where the transaction was made). a. Digital registration: The Cardmember must scan the QR code placed on the posters stationed around the mall or posted online which will lead the Cardmember to the Ayala Malls Online Promo Portal. The Cardmember must complete the following details and requirements. i. Register (if the Cardmember doesn’t have an account yet), log in (if the Cardmember already has an account), or join as guest (if the Cardmember doesn’t want to create an account or log in). -

Building a Strong Platform for Recovery, Renewed

2020 INTEGRATED REPORT BUILDING A STRONG PLATFORM FOR RECOVERY, RENEWED GROWTH, AND RESILIENCE Ayala Land’s various initiatives on stakeholder support, investment, and reinvention pave the way for recovery PAVING THE WAY FOR RECOVERY AND SUSTAINABLE GROWTH The ongoing COVID-19 pandemic and the natural calamities that of digital platforms to reach and engage buyers. Staff of APMC, struck the Philippines in 2020 are still being felt by Filipinos to this the company’s property management firm, stayed-in its managed day. Ayala Land’s swift response to face these challenges showed properties and communities while the enhanced community the resilience of both the company and its people. quarantine was enforced. In a strategic pivot, ALIzens executed a five-point action plan— Helping the Community protecting the workforce, financial sustainability, serving customers, Ayala Land employees raised PHP82.6 million under the Ayala helping the community, and thinking ahead towards recovery. Land Pays It Forward campaign to provide medical supplies and This action plan enabled Ayala Land, its employees, and its personal protective equipment to three COVID-19 designated communities to withstand the challenges and position for recovery. treatment hospitals. The company helped raise PHP425 million for Project Ugnayan and allocated PHP600 million in financial With the continued trust and confidence of its shareholders and assistance to more than 70 thousand “no work-no pay” contingent stakeholders, Ayala Land will count on bayanihan (community personnel during the critical first weeks of the quarantine. spirit) to move forward and pave the way for recovery and Recognizing the difficulties of its mall merchants, Ayala Land sustainable growth. -

PHILIPPINE STOCK EXCHANGE, INC. 3Rd Floor, Philippine Stock Exchange Plaza Ayala Triangle, Ayala Avenue, Makati City MS. JANET E

SEC FORM 20-IS (INFORMATION STATEMENT) March 12, 2015 SECURITIES AND EXCHANGE COMMISSION SEC Building, EDSA Greenhills Mandaluyong City, Metro Manila ATTENTION : DIR. VICENTE GRACIANO P. FELIZMENIO, JR. Director, Markets and Securities Regulation Department PHILIPPINE STOCK EXCHANGE, INC. 3rd Floor, Philippine Stock Exchange Plaza Ayala Triangle, Ayala Avenue, Makati City ATTENTION : MS. JANET ENCARNACION Head, Disclosure Department PHILIPPINE DEALING & EXCHANGE CORP. Market Regulatory Services Group 37/F, Tower 1, The Enterprise Center 6766 Ayala Avenue corner Paseo de Roxas, Makati City ATTENTION : MS. VINA VANESSA S. SALONGA Head - Issuer Compliance and Disclosures Department RE : SEC Form 20 – IS (Preliminary Information Statement 2015) Gentlemen: We submit two (2) copies of SEC Form 20-IS (Preliminary Information Statement 2015) of Aboitiz Equity Ventures, Inc. for your files. Kindly acknowledge receipt hereof. Thank you. Very truly yours, ABOITIZ EQUITY VENTURES, INC. By M. JASMINE S. OPORTO Corporate Secretary Annual Report 2014 1 SEC FORM 20-IS (INFORMATION STATEMENT) COVER SHEET C E O 2 5 3 6 S.E.C. Registration Number A B O I T I Z E Q U I T Y V E N T U R E S , I N C . ( Company's Full Name ) 3 2 N D S T R E E T , B O N I F A C I O G L O B A L C I T Y , T A G U I G C I T Y , M E T R O M A N I L A P H I L I P P I N E S (Business Address: No. -

Corporate Governance Issues in Philippine-Listed Companies

Philippine Management Review 2019, Vol. 26, 1-16. Corporate Governance Issues in Philippine-Listed Companies Arthur S. Cayanan* University of the Philippines, Cesar E.A. Virata School of Business, Diliman, Quezon City 1101, Philippines This paper discusses corporate governance issues in Philippine-listed companies such as ownership structure, separation of Chairman and CEO positions, independent directors, related party transactions, among others, and how non-controlling stockholders are adversely affected by these issues. The paper also assesses the sufficiency of existing rules and regulations and the effectiveness of regulators in protecting minority interest. 1 Introduction Corporate Governance is defined as the system of stewardship and control to guide organizations in fulfilling their long-term economic, moral, legal and social obligations towards their stakeholders.1 On November 10, 2016, the Securities and Exchange Commission (SEC) approved the Code of Corporate Governance for Publicly-Listed Companies (CG Code for PLCs).2 The Code provides a list of the governance responsibilities of the board of directors (BOD), corporate disclosure policies, standards for the selection of external auditor, and duties to stockholders, among others. In this paper, emphasis will be on ownership structure, the positions of Chairman and Chief Executive Officer (CEO) being held by separate individuals, the independence of independent directors, some related party transactions, and how these issues affect the interest of non-controlling stockholders.3 2 Objectives This study has the following objectives: 1. To assess some corporate governance practices of the 30 Philippine Stock Exchange index (PSEi) PSEi-indexed stocks, e.g., ownership structure, different individuals holding the positions of the chairman of the BOD and CEO, related party transactions, and tender offers. -

May 2021 Based on 31 May 2021 NAVPU

Fund Fact Sheet | May 2021 Based on 31 May 2021 NAVPU Peso Moderate Fund Objective Client Suitability Fund Manager The Peso Moderate Fund aims to This Fund is suitable for individuals The Peso Moderate Fund is managed by the Trust and Investments achieve capital appreciation over the willing to accept moderate risk for their Group of Banco De Oro Unibank, Inc. (BDO), which is the financial medium term by investing primarily in investment in exchange for moderate services flagship of the SM Group of Companies, one of the most equities and in some fixed income growth. Generally, these individuals are successful conglomerates spanning retail, mall operations, property, securities. willing to accept some losses on capital banking, hotels, convention and leisure facilities. as long as the expected return over the medium to long-term is significantly Today, BDO is multi-awarded by various leading financial institutions, higher. which include Finance Asia, Alpha Southeast Asia, The Banker, The Asset, Asia Money, and the Asia CEO Awards. FUND INFORMATION Inception Date: July 1, 2013 Peso Moderate Fund NAVPU Fund Manager: BDO Trust & Investments Group 1.50 Currency: Philippine Peso (PHP) 1.35 1 Valuation Schedule : Daily 1.20 Net Asset Value Per Unit (NAVPU): 0.98070 1.05 Lowest NAVPU (Mar. 19, 2020) 0.81570 0.90 Highest NAVPU (Jun. 07, 2017) 1.34890 0.75 Year to Date Return: -4.14% Jul 2013 Return Since Inception (from Jul. 1, 2013) -1.93% Dec 2013Jun 2014Dec 2014Jun 2015Dec 2015Jun 2016Dec 2016Jun 2017Dec 2017Jun 2018Dec 2018May 2019Nov 2019May 2020Nov 2020May 2021 Year on Year Return: 5.27% 1The NAVPU of the Fund is computed daily beginning January 2014. -

Business in Harmony Cebu Exchange

BUSINESS IN HARMONY CEBU EXCHANGE www.arthaland.com +63 917 77 ARTHA (27842) | [email protected] Visit our showroom on-site along Salinas Drive, Lahug, Cebu City CLIENT PROSPECTUS HLURB LTS No. 032788 CLIENT PROSPECTUS Salinas Drive, Lahug, Cebu City. Issued on 11 September 2017. Completion on 30 June 2021. Project Developer: Cebu Lavana Land Corporation. Project Manager: Arthaland Corporation. HLURB CVR AA-2019/01-550. Harmony… The beautiful interweaving of different elements into a singular experience. An experience so diverse, yet utterly cohesive; complete and perfectly balanced. Welcome to the Cebu Exchange. A holistic, sustainable, and highly connected work environment where harmony is not just a way of life, but a way of doing business. THE PHILIPPINE MARKET: A LANDSCAPE OF POSSIBILITIES*: AN OVERTURE • GROWTH: 6.7% GDP • OFW REMITTANCES: US$30 billion p.a. • BPO REVENUE: US$23 billion • 10-YEAR BOND YIELD: 6.3% Ranking among the top growth performers of Asia • POPULATION: 102 million in 2017*, the Philippines has cemented its position (67% below 35 years old) • MANILA at the top of the charts as one of the most • INFRASTRUCTURE SPENDING: US$160 billion (from 2016 to 2022) attractive economies in the entire region; • 3.8% Managed Inflation as of Q1 2018 attracting investors across the globe with more exciting and lucrative investment opportunities over other neighboring countries. CEBU CITY • DAVAO CITY *Sources: World Bank Group, 2017 Bangko Sentral ng Pilipinas, 2018 Contact Center Association of the Philippines, 2018 World Government Bonds, 2018 Philippine Statistics Authority, 2018 Department of Budget and Management, 2018 CEBU CITY: A DYNAMIC DESTINATION Known for its powdery white sand beaches, delicious local fare and artisan crafts, Cebu, the Queen City of the South, has always been one of the most important and influential economic centers in the Philippines and is quickly emerging as one of the most prominent IT-BPM destinations in the world.