Samsung C&T Corporation and Subsidiaries

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

KOREA Morning Focus

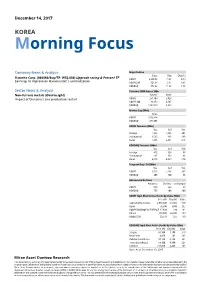

December 14, 2017 KOREA Morning Focus Company News & Analysis Major Indices Close Chg Chg (%) Hanwha Corp. (000880/Buy/TP: W56,000) Upgrade rating & Present TP ' KOSPI 2,480.55 19.55 0.79 Earnings to improve on Hanwha E&C s normalization KOSPI 200 326.18 2.11 0.65 KOSDAQ 772.22 11.82 1.55 Sector News & Analysis Turnover ('000 shares, Wbn) Non-ferrous metals (Overweight) Volume Value Impact of Glencore’s zinc production restart KOSPI 251,104 5,028 KOSPI 200 89,459 4,107 KOSDAQ 1,131,049 5,394 Market Cap (Wbn) Value KOSPI 1,613,324 KOSDAQ 274,605 KOSPI Turnover (Wbn) Buy Sell Net Foreign 1,443 1,648 -205 Institutional 1,585 886 698 Retail 1,945 2,461 -515 KOSDAQ Turnover (Wbn) Buy Sell Net Foreign 412 324 88 Institutional 285 192 93 Retail 4,695 4,869 -174 Program Buy / Sell (Wbn) Buy Sell Net KOSPI 1,513 1,206 307 KOSDAQ 206 120 86 Advances & Declines Advances Declines Unchanged KOSPI 566 244 67 KOSDAQ 733 408 100 KOSPI Top 5 Most Active Stocks by Value (Wbn) Price (W) Chg (W) Value Samsung Electronics 2,566,000 -39,000 570 Hynix 76,800 -1,000 265 KODEX KOSDAQ150 LEVERAGE 17,680 280 191 NCsoft 488,000 22,000 189 KODEX 200 32,670 255 160 KOSDAQ Top 5 Most Active Stocks by Value (Wbn) Price (W) Chg (W) Value SillaJen 89,100 1,100 319 New Pride 4,850 145 263 Celltrion Healthcare 93,100 6,100 231 TissueGene(Reg.S) 54,100 4,300 225 Celltrion 210,000 4,400 205 Note: As of December 13, 2017 Mirae Asset Daewoo Research Hanwha Corp. -

No 44 Fixed Income Strategies of Insurance Companies and Pension Funds

Committee on the Global Financial System CGFS Papers No 44 Fixed income strategies of insurance companies and pension funds Report submitted by a Working Group established by the Committee on the Global Financial System This Working Group was chaired by Peter Praet, Member of the European Central Bank’s Executive Board July 2011 JEL Classification: G22, G23, G28, M4 Copies of publications are available from: Bank for International Settlements Communications CH-4002 Basel, Switzerland E-mail: [email protected] Fax: +41 61 280 9100 and +41 61 280 8100 This publication is available on the BIS website (www.bis.org). © Bank for International Settlements 2011. All rights reserved. Brief excerpts may be reproduced or translated provided the source is cited. ISBN 92-9131-880-9 (print) ISBN 92-9197-880-9 (online) Preface In November 2010, the Committee on the Global Financial System (CGFS) established a Working Group to examine how insurance companies and pension funds are being affected by forthcoming accounting and regulatory changes in the current low-interest rate environment, and to investigate possible implications of changes in their investment strategies for the financial system. Over the coming years, accounting and regulatory changes could lead to reallocations of funding across financial instruments and sectors and encourage greater use of derivatives. The changes could also make it more difficult for insurance companies and pension funds to play their traditional role as global providers of long-term risk capital and accelerate the shifting of risks to households. The Working Group was chaired by Peter Praet of the National Bank of Belgium, now a Member of the European Central Bank’s Executive Board. -

Ironshore Inc

IRONSHORE INC. Editorial Contact: FOR IMMEDIATE RELEASE L. Gaye Torrance TorranceCo New York, New York (212) 691-5810 cell: (862) 215-7631 [email protected] IRONSHORE APPOINTS DENNIS MAHONEY AND ERIC SIMONSON TO SERVE ON ITS BOARD OF DIRECTORS Hamilton, Bermuda, February 2, 2012 – Ironshore Inc. announced that Dennis L. Mahoney and Eric A. Simonson have been appointed to its Board of Directors. Mr. Mahoney is the former Chairman and Chief Executive Officer of Aon Global in London. Mr. Simonson most recently was Senior Vice President and Chief Investment Officer of Allstate Insurance Company and served as Chairman and President of Allstate Investments, LLC, based in Northbrook, Illinois. “We are pleased to welcome Dennis and Ric as the newest directors to join the Ironshore Board,” said Kevin H. Kelley, Chief Executive Officer of Ironshore Inc. “Both are seasoned insurance industry leaders that will bring a depth of experience and wealth of insight to Ironshore as it builds upon its growing global platform.” Mr. Mahoney is a forty-two year veteran of the broking industry and past President of the Insurance Institute of London. During his years with Aon and its predecessor company, he served in a number of senior leadership roles in retail, wholesale and reinsurance. Prior to his retirement from Aon in 2010, Mr. Mahoney served as Chairman of Aon Global. He also serves as a Director of ACORD the global insurance standards organization. Mr. Simonson’s thirty-five year insurance industry career includes his most recent position as executive and member of the Allstate Corporation’s senior management team at the company’s U.S.- based headquarters. -

FTSE Korea 30/18 Capped

2 FTSE Russell Publications 19 August 2021 FTSE Korea 30/18 Capped Indicative Index Weight Data as at Closing on 30 June 2021 Index weight Index weight Index weight Constituent Country Constituent Country Constituent Country (%) (%) (%) Alteogen 0.19 KOREA Hyundai Engineering & Construction 0.35 KOREA NH Investment & Securities 0.14 KOREA AmoreG 0.15 KOREA Hyundai Glovis 0.32 KOREA NHN 0.07 KOREA Amorepacific Corp 0.65 KOREA Hyundai Heavy Industries 0.29 KOREA Nong Shim 0.08 KOREA Amorepacific Pfd. 0.08 KOREA Hyundai Marine & Fire Insurance 0.13 KOREA OCI 0.17 KOREA BGF Retail 0.09 KOREA Hyundai Merchant Marine 1.02 KOREA Orion 0.21 KOREA BNK Financial Group 0.18 KOREA Hyundai Mipo Dockyard 0.15 KOREA Ottogi 0.06 KOREA Celltrion Healthcare 0.68 KOREA Hyundai Mobis 1.53 KOREA Paradise 0.07 KOREA Celltrion Inc 2.29 KOREA Hyundai Motor 2.74 KOREA Posco 1.85 KOREA Celltrion Pharm 0.24 KOREA Hyundai Motor 2nd Pfd. 0.33 KOREA Posco Chemical 0.32 KOREA Cheil Worldwide 0.14 KOREA Hyundai Motor Pfd. 0.21 KOREA Posco International 0.09 KOREA CJ Cheiljedang 0.3 KOREA Hyundai Steel 0.33 KOREA S1 Corporation 0.13 KOREA CJ CheilJedang Pfd. 0.02 KOREA Hyundai Wia 0.13 KOREA Samsung Biologics 0.92 KOREA CJ Corp 0.11 KOREA Industrial Bank of Korea 0.22 KOREA Samsung C&T 0.94 KOREA CJ ENM 0.15 KOREA Kakao 3.65 KOREA Samsung Card 0.08 KOREA CJ Logistics 0.12 KOREA Kangwon Land 0.23 KOREA Samsung Electro-Mechanics 0.81 KOREA Coway 0.36 KOREA KB Financial Group 1.78 KOREA Samsung Electronics 25.36 KOREA Daewoo Engineering & Construction 0.12 KOREA KCC Corp 0.12 KOREA Samsung Electronics Pfd. -

NP Key Contacts.Pdf

IGP Network Partners: Key Contacts Region: Americas Country / Territory IGP Network Partner IGP Contact Email Type IGP Regional Coordinator Mr. Michael Spincemaille [email protected] Argentina SMG LIFE Mr. Nicolas Passet [email protected] Partner Brazil MAPFRE Vida S.A. Ms. Débora Nunes Santos [email protected] Partner Canada Manulife Financial Corporation Mr. Kajan Ramanathan [email protected] Partner Chile MAPFRE Chile Ms. Nathalie Gonzalez [email protected] Partner Colombia MAPFRE Colombia Ms. Ingrid Olarte Pérez [email protected] Partner Costa Rica MAPFRE Costa Rica Mr. Armando Sevilla [email protected] Partner Dominican Republic (Life) MAPFRE BHD Mrs. Alejandra Quirico [email protected] Partner Dominican Republic (Health) MAPFRE Salud ARS, S. A. Mr. Christian Wazar [email protected] Partner Ecuador MAPFRE Atlas * Mr. Carlos Zambrano [email protected] Correspondent El Salvador MAPFRE Seguros El Salvador S.A. Mr. Daniel Acosta González [email protected] Partner French Guiana Refer to France - - Partner Guadeloupe Refer to France - - Partner Guatemala MAPFRE Guatemala Mr. Luis Pedro Chavarría [email protected] Partner Honduras MAPFRE Honduras Mr. Carlos Ordoñez [email protected] Partner Martinique Refer to France - - Partner Mexico Seguros Monterrey New York Life Ms. Paola De Uriarte [email protected] Partner Nicaragua MAPFRE Nicaragua Mr. Dany Lanuza Flores [email protected] Partner Panama MAPFRE Panama Mr. Manuel Rodriguez [email protected] Partner Paraguay MAPFRE Paraguay Mr. Sergio Alvarenga [email protected] Partner Peru MAPFRE Peru Mr. Ramón Acuña Huerta [email protected] Partner Saint Martin Refer to France - - Partner Saint Barthélemy Refer to France - - Partner Saint Pierre & Miquelon Refer to France - - Partner United States Prudential Insurance Company of America Mr. -

Posco International Corporation

POSCO INTERNATIONAL CORPORATION Sustainability Report 2019 About This Report The 2019 POSCO INTERNATIONAL Sustainability Report, the forth annual publication, illustrate the Company’s performance fulfill- ing its economic, social, and environmental responsibility. POSCO INTERNATIONAL aims to transparently disclose its sustainability management activities for the year 2019 and communicate with wide-ranging stakeholders. Reporting Guidelines Global Reporting Initiative(GRI) Standards: Core Option Reporting Period January 1, 2019 ~ December 31, 2019 * 2017 ~ H1 of 2020 for a portion of the performance data Reporting Scope Economy: On a consolidated basis in accordance with the K-IFRS 〮 Society & Environment: POSCO INTERNATIONAL Headquarters, 〮 POSCO SPS1), and overseas worksites (Myanmar, Indonesia, and Uzbekistan) Areas where major operations are based: Republic of Korea 〮 1) This refers to the STS Division, the TMC Division and the Plate Fabrication Division that were split off as subsidiaries in April 2020. Reporting Cycle Annually(publication of the most recent report: 2019) Assurance Financial data: Earnst & Young Han Young 〮 Non-financial data: DNV GL 〮 Contact Details Address: 165 Convensia-daero(POSCO Tower-Songdo), Yeonsu-gu, Incheon, Republic of Korea Tel: +82-2-759-2861 Department in charge: Sustainability Management Section E-mail: [email protected] POSCO INTERNATIONAL CORPORATION Sustainability Report 2019 03 Global CSR Activities 01 We Make Sustainability 02 Sustainability Management Strategy 102 Global CSR Overview -

2014 Big Data Analytics Conference Attendance List

2014 Big Data Analytics Conference Attendance List ID Name Company Name Registration Class 2014 Big Data Analytics Conference 258295 Mandar, Adkar Legal And General America Member 01. Registration Fees 156 258018 Bryan, L. Anderson Soldier Valley, LLC Supplier Vendor Guest Attendee 6 256443 Ted, Antkowiak XtLytics Supplier Vendor LIMRA Staff 13 63587 Thomas, Ashley Gen Re Member Member Registration Fee 111 254541 Rob, Baldwin Lincoln Financial Group Member Non-Member Registration Fee 4 158939 Reena, Batra State Farm Insurance Member Spouse/Guest Registration Fee 2 123377 Tracy, Bayer Prudential Member Supplier Vendor/Other 20 246701 Molly, L. Bennard AXA Member 251999 Myrelle, Berena MetLife Member 32123 Stuart, L. Bergman Gerber Life Insurance Company Member 237291 Michael, Bernstein Acxiom Corporation Supplier Vendor 142447 Andrew, W Blank State Farm Insurance Member 245801 Linda, Boncek MetLife Member 200693 Brian, Bonti American Family Insurance Member 64515 Gregory, A Brandner Munich American Reassurance Company Member 154474 Sarah, Bray Sun Life Financial Member 258015 Bradley, Brooks WellPoint, Inc. Member 25298 Philip, M. Brown LIMRA LIMRA Staff 258789 Daniel, Buch New York Life Member 259380 Scott, Busse PwC Supplier Vendor 4771 Rose, M. Cahill Acxiom Corporation Supplier Vendor 170592 Kari-Ann, Casale Prudential Member 255396 Frankie, Chai MetLife Member 210551 Tha, L. Chan John Hancock Member 255833 Regina, Chang Epsilon Supplier Vendor 243763 Dan, Cheng Gerber Life Insurance Company Member 143102 Mathew, Clegg Amica Life Insurance Member 259449 Louis, Cloutier Syntell, Inc. Supplier Vendor 255834 Sheila, Colclasure Acxiom Corporation Supplier Vendor 245489 Chris, Condon Bankers Life Member 201974 Christopher, Cooney RBC Insurance Member 257822 Jason, Culp Farm Bureau Life Member 224582 Nirav, Dagli Spinnaker Analytics Supplier Vendor 188244 Bruce, Dahlquist Clinical Reference Laboratory Supplier Vendor 235791 Charles, DeFilippo NFP Insurance Services, Inc. -

Holdings-Report.Pdf

The Fund is a closed-end exchange traded management Investment company. This material is presented only to provide information and is not intended for trading purposes. Closed-end funds, unlike open-end funds are not continuously offered. After the initial public offering, shares are sold on the open market through a stock exchange. Changes to investment policies, current management fees, and other matters of interest to investors may be found in each closed-end fund's most recent report to shareholders. Holdings are subject to change daily. PORTFOLIO HOLDINGS FOR THE KOREA FUND as of July 31, 2021 *Note: Cash (including for these purposes cash equivalents) is not included. Security Description Shares/Par Value Base Market Value (USD) Percent of Base Market Value SAMSUNG ELECTRONICS CO 793,950 54,183,938.27 20.99 SK HYNIX INC COMMON 197,500 19,316,452.95 7.48 NAVER CORP COMMON STOCK 37,800 14,245,859.60 5.52 LG CHEM LTD COMMON STOCK 15,450 11,309,628.34 4.38 HANA FINANCIAL GROUP INC 225,900 8,533,236.25 3.31 SK INNOVATION CO LTD 38,200 8,402,173.44 3.26 KIA CORP COMMON STOCK 107,000 7,776,744.19 3.01 HYUNDAI MOBIS CO LTD 26,450 6,128,167.79 2.37 HYUNDAI MOTOR CO 66,700 6,030,688.98 2.34 NCSOFT CORP COMMON STOCK 8,100 5,802,564.66 2.25 SAMSUNG BIOLOGICS CO LTD 7,230 5,594,175.18 2.17 KB FINANCIAL GROUP INC 123,000 5,485,677.03 2.13 KAKAO CORP COMMON STOCK 42,700 5,456,987.61 2.11 HUGEL INC COMMON STOCK 24,900 5,169,415.34 2.00 SAMSUNG 29,900 4,990,915.02 1.93 SK TELECOM CO LTD COMMON 17,500 4,579,439.25 1.77 KOREA INVESTMENT 53,100 4,427,115.84 -

STOXX Asia 100 Last Updated: 03.07.2017

STOXX Asia 100 Last Updated: 03.07.2017 Rank Rank (PREVIOU ISIN Sedol RIC Int.Key Company Name Country Currency Component FF Mcap (BEUR) (FINAL) S) KR7005930003 6771720 005930.KS KR002D Samsung Electronics Co Ltd KR KRW Y 256.2 1 1 JP3633400001 6900643 7203.T 690064 Toyota Motor Corp. JP JPY Y 128.5 2 2 TW0002330008 6889106 2330.TW TW001Q TSMC TW TWD Y 113.6 3 3 JP3902900004 6335171 8306.T 659668 Mitsubishi UFJ Financial Group JP JPY Y 83.5 4 4 HK0000069689 B4TX8S1 1299.HK HK1013 AIA GROUP HK HKD Y 77.2 5 5 JP3436100006 6770620 9984.T 677062 Softbank Group Corp. JP JPY Y 61.7 6 7 JP3735400008 6641373 9432.T 664137 Nippon Telegraph & Telephone C JP JPY Y 58.7 7 8 CNE1000002H1 B0LMTQ3 0939.HK CN0010 CHINA CONSTRUCTION BANK CORP H CN HKD Y 58.2 8 6 TW0002317005 6438564 2317.TW TW002R Hon Hai Precision Industry Co TW TWD Y 52.6 9 12 HK0941009539 6073556 0941.HK 607355 China Mobile Ltd. CN HKD Y 52.0 10 10 JP3890350006 6563024 8316.T 656302 Sumitomo Mitsui Financial Grou JP JPY Y 48.3 11 15 INE040A01026 B5Q3JZ5 HDBK.BO IN00CH HDFC Bank Ltd IN INR Y 45.4 12 13 JP3854600008 6435145 7267.T 643514 Honda Motor Co. Ltd. JP JPY Y 43.3 13 14 JP3435000009 6821506 6758.T 682150 Sony Corp. JP JPY Y 42.3 14 17 JP3496400007 6248990 9433.T 624899 KDDI Corp. JP JPY Y 42.2 15 16 CNE1000003G1 B1G1QD8 1398.HK CN0021 ICBC H CN HKD Y 41.1 16 19 JP3885780001 6591014 8411.T 625024 Mizuho Financial Group Inc. -

Certain Cold-Rolled Steel Flat Products from the Republic of Korea: Final Results of Antidumping Duty Administrative Review; 2018-2019

This document is scheduled to be published in the Federal Register on 07/29/2021 and available online at federalregister.gov/d/2021-16172, and onBILLINGgovinfo.gov CODE: 3510-DS-P DEPARTMENT OF COMMERCE International Trade Administration [A-580-881] Certain Cold-Rolled Steel Flat Products from the Republic of Korea: Final Results of Antidumping Duty Administrative Review; 2018-2019 AGENCY: Enforcement and Compliance, International Trade Administration, Department of Commerce. SUMMARY: The Department of Commerce (Commerce) determines that certain cold-rolled steel flat products (cold-rolled steel) from the Republic of Korea were not sold in the United States at prices below normal value during the period of review (POR), September 1, 2018, through August 31, 2019. DATES: Applicable [INSERT DATE OF PUBLICATION IN THE FEDERAL REGISTER]. FOR FURTHER INFORMATION CONTACT: Michael J. Heaney, George McMahon, or Marc Castillo, AD/CVD Operations, Office VI, Enforcement and Compliance, International Trade Administration, U.S. Department of Commerce, 1401 Constitution Avenue, NW, Washington, DC 20230; telephone: (202) 482-4475, (202) 482-1167, or (202) 482-5019, respectively. SUPPLEMENTARY INFORMATION: Background On January 25, 2021, Commerce published the Preliminary Results of this administrative review.1 We invited interested parties to comment on the Preliminary Results. Between February 24, and March 5, 2021, Commerce received timely filed case briefs and rebuttal briefs from United States Steel Corporation (U.S. Steel), additional domestic parties,2 Hyundai Steel 1 See Certain Cold Rolled Steel Flat Products from the Republic of Korea: Preliminary Results of Antidumping Duty Administrative Review; 2018-2019, 86 FR 6871 (January 25, 2021) (Preliminary Results), and accompanying Preliminary Decision Memorandum (PDM). -

Korean Multinationals Show Solid Recovery After Global Crisis

Korean multinationals show solid recovery after global crisis Report dated November 16, 2010 EMBARGO: The contents of this report must not be quoted or summarized in the print, broadcast or electronic media before November 16, 2010, 10:00 a.m. Seoul; 1 a.m. GMT, and 9:00 p.m. November 15, 2010, New York. Seoul and New York, November 16, 2010 The Institute of International Affairs of the Graduate School of International Studies (GSIS) at Seoul National University in Seoul, and the Vale Columbia Center on Sustainable International Investment (VCC) at Columbia University in New York, are releasing the first annual report on leading Korean multinationals. The research for this report was conducted in 2010 and covers the period 2007 to 2009. 1 Highlights The Republic of Korea (henceforth ‘Korea’), the 11 th largest economy in the world, has now become one of the leading investors abroad. The number and the size of the corporate giants that dominate the economy have increased over the years, boosting and diversifying their investments around the world. Korea’s multinational enterprises ranked by their foreign assets (see table 1 below) show about USD 93 billion in assets held abroad. 2 Samsung Electronics Co., Ltd. (SEC), a member of a leading Korean conglomerate, ranked 1 st with slightly over USD 18 billion, followed by another top conglomerate member, LG Electronics, with over USD 10 billion dollars. Hyundai Heavy Industries Co., Ltd, and DSME Co., Ltd, had foreign assets of over USD 8 billion each and LG Display had over USD 6 billion. The top five firms together accounted for just over half of the total foreign assets of the top 20 companies. -

Samsung Heavy Industries

SHI SUSTAINABILITY REPORT 2015 SAMSUNG HEAVY INDUSTRIES OVERVIEW Message from the CEO Company Profile Management Philosophy Business Introduction Business Operation Process Governance Stakeholder Communication Aspect Boundary Materiality Test 1 Overview Message from the CEO Samsung Heavy Industries, which has shown continuous growth and remarkable development through turning countless adversities into valuable opportunities, now prepares for an even bigger leap forward on the basis of its decisive innovations. Dear Stakeholders, who trust and value Samsung Heavy Industries, Samsung Heavy Industries (hereinafter referred to as SHI), which has successfully executed various projects in shipbuilding and offshore fields since its foundation in 1974, consistently endeavors to reflect the voices of its stakeholders, including clients, subcontractors, employees, and local communities. Moreover, as a global industry leader, SHI is investing much effort in building reliable and eco-friendly ships and offshore production facilities. 2015 has been by far the most difficult business year for SHI due to significant challenges, such as the global economic recession, low oil prices, and a series of trials & errors in executing offshore projects. Despite such difficult conditions, however, SHI employees endeavored to maintain safety and quality as well as comply with delivery schedule by showing concerted commitment and dedication, thereby transforming the crisis into opportunities. th Not only has SHI promoted the importance of safety awareness by announcing January 19 as the official Safety Awareness Day, but it has also received the highest level of recognition in the Safety Assessment Evaluation, conducted by ExxonMobil, for 6 consecutive years. Moreover, SHI significantly improved quality by enforcing its 10 Quality Rule Implementation Check on a weekly basis for flawless delivery.