The Moat Report Plus More! Q CLSA Recently Published the Moat Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Metro Pacific Investments Corporation and Subsidiaries

Metro Pacific Investments Corporation and Subsidiaries Consolidated Financial Statements December 31, 2019 and 2018 and Years Ended December 31, 2019, 2018 and 2017 and Independent Auditor’s Report SyCip Gorres Velayo & Co. Tel: (632) 891 0307 BOA/PRC Reg. No. 0001, 6760 Ayala Avenue Fax: (632) 819 0872 October 4, 2018, valid until August 24, 2021 1226 Makati City ey.com/ph SEC Accreditation No. 0012-FR-5 (Group A), Philippines November 6, 2018, valid until November 5, 2021 INDEPENDENT AUDITOR’S REPORT The Board of Directors and Stockholders Metro Pacific Investments Corporation Opinion We have audited the consolidated financial statements of Metro Pacific Investments Corporation and its subsidiaries (the Company), which comprise the consolidated statements of financial position as at December 31, 2019 and 2018, and the consolidated statements of comprehensive income, consolidated statements of changes in equity and consolidated statements of cash flows for each of the three years in the period ended December 31, 2019, and notes to the consolidated financial statements, including a summary of significant accounting policies. In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Company as at December 31, 2019 and 2018, and its consolidated financial performance and its consolidated cash flows for each of the three years in the period ended December 31, 2019 in accordance with Philippine Financial Reporting Standards (PFRSs). Basis for Opinion We conducted our audits in accordance with Philippine Standards on Auditing (PSAs). Our responsibilities under those standards are further described in the Auditor’s Responsibilities for the Audit of the Consolidated Financial Statements section of our report. -

Retirement Strategy Fund 2060 Description Plan 3S DCP & JRA

Retirement Strategy Fund 2060 June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA ACTIVIA PROPERTIES INC REIT 0.0137% 0.0137% AEON REIT INVESTMENT CORP REIT 0.0195% 0.0195% ALEXANDER + BALDWIN INC REIT 0.0118% 0.0118% ALEXANDRIA REAL ESTATE EQUIT REIT USD.01 0.0585% 0.0585% ALLIANCEBERNSTEIN GOVT STIF SSC FUND 64BA AGIS 587 0.0329% 0.0329% ALLIED PROPERTIES REAL ESTAT REIT 0.0219% 0.0219% AMERICAN CAMPUS COMMUNITIES REIT USD.01 0.0277% 0.0277% AMERICAN HOMES 4 RENT A REIT USD.01 0.0396% 0.0396% AMERICOLD REALTY TRUST REIT USD.01 0.0427% 0.0427% ARMADA HOFFLER PROPERTIES IN REIT USD.01 0.0124% 0.0124% AROUNDTOWN SA COMMON STOCK EUR.01 0.0248% 0.0248% ASSURA PLC REIT GBP.1 0.0319% 0.0319% AUSTRALIAN DOLLAR 0.0061% 0.0061% AZRIELI GROUP LTD COMMON STOCK ILS.1 0.0101% 0.0101% BLUEROCK RESIDENTIAL GROWTH REIT USD.01 0.0102% 0.0102% BOSTON PROPERTIES INC REIT USD.01 0.0580% 0.0580% BRAZILIAN REAL 0.0000% 0.0000% BRIXMOR PROPERTY GROUP INC REIT USD.01 0.0418% 0.0418% CA IMMOBILIEN ANLAGEN AG COMMON STOCK 0.0191% 0.0191% CAMDEN PROPERTY TRUST REIT USD.01 0.0394% 0.0394% CANADIAN DOLLAR 0.0005% 0.0005% CAPITALAND COMMERCIAL TRUST REIT 0.0228% 0.0228% CIFI HOLDINGS GROUP CO LTD COMMON STOCK HKD.1 0.0105% 0.0105% CITY DEVELOPMENTS LTD COMMON STOCK 0.0129% 0.0129% CK ASSET HOLDINGS LTD COMMON STOCK HKD1.0 0.0378% 0.0378% COMFORIA RESIDENTIAL REIT IN REIT 0.0328% 0.0328% COUSINS PROPERTIES INC REIT USD1.0 0.0403% 0.0403% CUBESMART REIT USD.01 0.0359% 0.0359% DAIWA OFFICE INVESTMENT -

Annual Report 2010 Mission

sharpening our focus AnnuAl report 2010 Mission: to create long-term value for all its stakeholders Brand EssEncE: passion for better ways Brand spikEs • Driven • Driven to lead • Driven to excel • Driven to Serve corporatE ValuEs • passion • Innovation • professionalism • Integrity About the cover: Aboitiz equity Ventures, Inc. (AeV) has achieved unprecedented growth through the years, having expanded into power generation and distribution, banking and food. As it advances into another period filled with opportunities and challenges, AeV opts to sharpen its focus on its core strengths and maximize its potentials. TABLE OF CONTENTS 02 Financial Highlights Report to Stockholders 04 From your Chairman and President & CEO Results of Operations 08 Power 14 Financial Services 18 Food 20 Transport 22 From your Chief Financial Officer 25 From your Chief Risk Management Officer 26 Risk Management Report 28 From your Chief Compliance Officer 29 Corporate Governance Report FEATURES 42 CitySavings prepares to take on Luzon 44 Running the good race 46 Sustainability Statement 48 CSR: Helping people help themselves 50 Board of Directors / Board Committees 52 Corporate Officers 54 Operating Unit Heads 55 Management Directory 56 Location of Operations 57 Corporate Structure 58 Audit Committee Report 59 Statement of Management Responsibility 60 Independent Auditors’ Report 62 Consolidated Financial Statement The complete Securities & Exchange Commission Form 20-IS (Information Statement) and Annual Report is inside the CD inserted at the inside back cover -

SEC FORM 17-A (ANNUAL REPORT) (B) Has Been Subject to Such Filing Requirements for the Past 90 Days

April 16, 2012 March 19, 2012 MS. JANET ENCARNACION Head, Disclosure Department Philippine Stock Exchange, Inc. Tower One and Exchange Plaza Ayala Triangle, Ayala Avenue, Makati City Dear Ms. Encarnacion: We file herewith a copy of SEC Form 17-A (Annual Report 2011) of Aboitiz Equity Ventures, Inc. (AEV). Also enclosed is the cover letter for AEV’s SEC Form 17-A addressed to the Securities and Exchange Commission. Thank you. Very truly yours, ABOITIZ EQUITY VENTURES, INC. By M. JASMINE S. OPORTO Corporate Secretary COVER SHEET C E 0 2 5 3 6 S.E.C. Registration Number A B O I T I Z E Q U I T Y V E N T U R E S , I N C . ( Company's Full Name ) A B O I T I Z C O R P O R A T E C E N T E R G O V . M A N U E L C U E N C O A V E . K A S A M B A G A N , C E B U C I T Y ( Business Address: No. Street City / Town / Province ) CATHERINE R. ATAY (032) 411-1800 Contact Person Company Telephone Number ANNUAL REPORT 2011 1 2 3 1 1 7 - A 0 5 2 1 Month Day FORM TYPE Month Day Fiscal Year Annual Meeting Secondary License Type, if Applicable S E C Dept. Requiring this Doc Amended Articles Number/Section 10,054 x Total No. of Stockholders Domestic Foreign - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - To be accomplished by SEC Personnel concerned File Number LCU Document I.D. -

2015 SMPHI Annual Report

SUSTAINING GROWTH, DELIVERING VALUE 10th Floor, OneE-com Center Harbor Drive, Mall of Asia Complex Pasay City 1300, Philippines Email: [email protected] www.sminvestments.com 2 IFC Our Business Philosophy 2 Business Highlights & Impact 6 Financial Highlights 7 Shareholder Value SM INVESTMENTS CORPORATION SM INVESTMENTS OUR BUSINESS PHILOSOPHY 8 Ten-Year Performance Overview 10 Our Business Footprint 12 Message to Shareholders SM Investments Corporation is the Philippines’ largest 14 President’s Report publicly-listed holding company that holds a group of sustainable businesses in retail, property and financial services. The Group thrives on leadership, innovation 18 RETAIL OPERATIONS and highly synergistic operations. • THE SM STORE Our Vision is to build world-class businesses that are • SM Markets catalysts for development in the communities we serve. Our long history of sustained growth is an indication of our ability to deliver value for all our stakeholders through sound financial management, leadership, innovation, long-term sustainability efforts and a comprehensive development program for all our host communities. Through our interests and activities, Our Mission is to strive to be a good corporate citizen by partnering with our host communities in providing consistently high standards of service to our customers, look after the welfare of our employees, and deliver sustainable returns to our shareholders at all times, upholding the highest standards of corporate governance in all our businesses. 28 PROPERTY Over the years, we have been committed to sustaining • Malls our growth, in creating value and delivering quality • Residences products and services that our millions of customers aspire for. We are here to serve. -

Economic Environmentenvironment

Investor Presentation 3Q 2017 Your Success is our Business Legal Disclaimer This presentation and the information contained herein as well as the materials distributed herewith ("Presentation") are the sole and exclusive property of China Banking Corporation (“China Bank”) and shall only be used for the purpose intended herein. None of the information contained in this Presentation constitutes a solicitation, offer, opinion, or recommendation by China Bank to buy or to sell any securities or financial instrument or to provide any investment service or investment advice. The information contained in this Presentation is based on carefully selected sources believed to be reliable but no representation or warranty as to its accuracy or completeness is made. All statements in this Presentation, other than statements of historical facts, that address activities, events, or developments that China Bank expects or anticipates will or may occur in the future (including but not limited to projections, targets, estimates and business plans) are forwardlooking statements. China Bank’s actual results or developments may differ materially from those expressed or implied in these forward-looking statements as a result of various factors and uncertainties, including but not limited to price fluctuations, actual demand, exchange rate fluctuations, market shares, competition, changes in legal, financial and regulatory frameworks, international economic and financial market conditions, political risks, cost estimates, and other risks and factors beyond our control. Your use of the Presentation shall be at your sole risk and you shall form your own conclusions as to the reliability of any information presented and as to any conclusions to be drawn therefrom. -

AP List of Top 100 Stockholders As of March 31, 2020

April 13, 2020 PHILIPPINE STOCK EXCHANGE, INC. PSE Tower, 5th Avenue corner 28th Street, Bonifacio Global City, Taguig City Attention: Ms Janet A. Encarnacion Head, Disclosure Dept. PHILIPPINE DEALING & EXCHANGE CORP. Market Regulatory Services Group 29th Floor, BDO Equitable Tower 8751 Paseo de Roxas, Makati City Attention: Atty. Marie Rose M. Magallen-Lirio Head - Issuer Compliance & Disclosure Dept. ABOITIZ POWER CORPORATION LIST OF TOP 100 STOCKHOLDERS AS OF MARCH 31, 2020 NAME HOLDINGS PERCENTAGE 1 ABOITIZ EQUITY VENTURES INC. 5,657,530,774 76.88% 2 PCD NOMINEE CORPORATION FILIPINO 1,028,832,249 13.98% 3 PCD NOMINEE CORPORATION FOREIGN 389,177,197 5.29% 4 BAUHINIA MANAGEMENT INC. 18,109,100 0.25% 5 PORTOLA INVESTORS INC. 13,634,856 0.19% 6 HAWK VIEW CAPITAL INC. 13,633,657 0.19% 7 SAN FERNANDO ELECTRIC LIGHT AND POWER CO. INC. 7,931,034 0.11% 8 PARRAZ DEVELOPMENT CORPORATION 7,827,522 0.11% 9 DOMINUS CAPITAL INC. 7,241,050 0.10% 10 FMK CAPITAL PARTNERS INC. 6,538,000 0.09% 11 SABIN M. ABOITIZ 5,667,406 0.08% 12 IKER M. ABOITIZ 5,465,100 13 ABOITIZ & COMPANY INC. 5,360,000 0.07% 14 DANIELE MANAGEMENT & DEVELOPMENT CORPORATION 5,234,949 0.07% 15 DANEL C. ABOITIZ 4,528,696 0.06% 16 ARRAYANES CORPORATION 4,146,243 0.06% 17 RAMON ABOITIZ FOUNDATION INC. 3,900,000 0.05% Page 1 of 5 18 TRIS MANAGEMENT CORPORATION 3,130,359 0.04% 19 TINKERBELL MANAGEMENT CORPORATION 3,042,454 0.04% 20 CAL MANAGEMENT CORPORATION 3,036,798 0.04% 21 ANNABELLE OSMENA ABOITIZ 2,920,035 0.04% 22 GITANA MANAGEMENT & DEV'T. -

FTSE Publications

2 FTSE Russell Publications 28 October 2020 FTSE Philippines USD Net Tax Index Indicative Index Weight Data as at Closing on 27 October 2020 Constituent Index weight (%) Country Constituent Index weight (%) Country Constituent Index weight (%) Country Aboitiz Power 1.55 PHILIPPINES JG Summit Holdings 6.55 PHILIPPINES Semirara Mining and Power 0.48 PHILIPPINES Alliance Global 1.11 PHILIPPINES Jollibee Foods 2.48 PHILIPPINES SM Investments 16.27 PHILIPPINES Ayala Corporation 8.63 PHILIPPINES LT Group 1.16 PHILIPPINES SM Prime Hldgs 10.52 PHILIPPINES Ayala Land 9.44 PHILIPPINES Manila Electric 2.7 PHILIPPINES Universal Robina 4.26 PHILIPPINES Bank of The Philippine Islands 4.65 PHILIPPINES Megaworld 1.25 PHILIPPINES BDO Unibank 6.27 PHILIPPINES Metro Pacific Investments 1.97 PHILIPPINES Bloomberry Resorts 0.9 PHILIPPINES Metropolitan Bank & Trust 2.63 PHILIPPINES DMCI Holdings 0.65 PHILIPPINES PLDT 4.32 PHILIPPINES Globe Telecom 2.08 PHILIPPINES Puregold Price Club 1.44 PHILIPPINES GT Capital Holdings 1.51 PHILIPPINES San Miguel 1.28 PHILIPPINES International Container Terminal Service 4.37 PHILIPPINES San Miguel Food and Beverage 1.52 PHILIPPINES Source: FTSE Russell 1 of 2 28 October 2020 Data Explanation Weights Weights data is indicative, as values have been rounded up or down to two decimal points. Where very small values are concerned, which would display as 0.00 using this rounding method, these weights are shown as <0.005. Timing of data Constituents & Weights are generally published in arrears and contain the data as at the most recent quarter-end. However, some spreadsheets are updated on a more frequent basis. -

Sec Form 20-Is Information Statement Pursuant to Section 20 of the Securities Regulation Code

ANNUAL REPORT 2010 FINANCIAL SUMMARY (In Million Pesos) 2007 2008 2009 % change Re-presented* Re-presented* (‘09 vs ‘08) For the Year Revenues 31,205 35,862 46,230 29% Operating Profit Operating profit from ordinary activities 2,902 2,340 7,527 222% Equity in net earnings of associates 3,987 3,625 4,322 19% Other income (charges) 1,178 309 (688) -323% Income before income tax 8,068 6,275 11,160 78% Provision for income tax (1,212) (978) (1,206) 23% Income before minority interest 6,856 5,297 9,955 88% Minority interest (1,035) (1,176) (1,648) Net income attributable to Equity Holders of the parent 5,821 4,121 8,307 102% At Year End Total Assets 65,908 75,715 143,281 89% Total Liabilities 18,812 29,059 88,639 205% Minority Interest 8,811 8,861 9,945 12% Equity Attributable to Equity Holders of the Parent 38,285 37,795 44,697 18% EBITDA 9,387 8,607 15,639 82% Per Share (in pesos) Earnings 1.02 0.73 1.49 104% Book Value 6.72 6.78 8.09 19% Cash Dividend (Common) 0.20 0.61 0.27 -56% Financial Ratios Current Ratio 2.42 1.90 0.79 Debt-to-Equity Ratio 0.40 0.62 1.62 Net Debt-to-Equity Ratio (0.14) 0.08 1.28 * Dec 2007 and 2008 Profit & Loss figures now consider the revenues & expenses of the ATS disposal group due to the aborted ATS sale in 2009. -

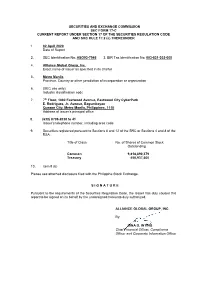

SECURITIES and EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 of the SECURITIES REGULATION CODE and SRC RULE 17.2 (C) THEREUNDER

SECURITIES AND EXCHANGE COMMISSION SEC FORM 17-C CURRENT REPORT UNDER SECTION 17 OF THE SECURITIES REGULATION CODE AND SRC RULE 17.2 (c) THEREUNDER 1. 02 April 2020 Date of Report 2. SEC Identification No: ASO93-7946 3. BIR Tax Identification No: 003-831-302-000 4. Alliance Global Group, Inc. Exact name of issuer as specified in its charter 5. Metro Manila Province, Country or other jurisdiction of incorporation or organization 6. (SEC use only) Industry classification code 7. 7th Floor, 1880 Eastwood Avenue, Eastwood City CyberPark E. Rodriguez, Jr. Avenue, Bagumbayan Quezon City, Metro Manila, Philippines, 1110 Address of issuer’s principal office 8. (632) 8709-2038 to 41 Issuer’s telephone number, including area code 9. Securities registered pursuant to Sections 8 and 12 of the SRC or Sections 4 and 8 of the RSA: Title of Class No. of Shares of Common Stock Outstanding Common 9,818,890,379 Treasury 450,937,600 10. Item 9 (b) Please see attached disclosure filed with the Philippine Stock Exchange. S I G N A T U R E Pursuant to the requirements of the Securities Regulation Code, the Issuer has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized. ALLIANCE GLOBAL GROUP, INC. By: DINA D. INTING Chief Financial Officer, Compliance Officer and Corporate Information Officer 4/3/2020 Request for extension to file SEC Form 17-A CR01662-2020 The Exchange does not warrant and holds no responsibility for the veracity of the facts and representations contained in all corporate disclosures, including financial reports. -

Securities and Exchange Commission

COVER SHEET SEC Registration Number 1 6 3 4 2 Company Name S M I N V E S T M E N T S C O R P O R A T I O N A N D S U B S I D I A R I E S Principal Office (No./Street/Barangay/City/Town/Province) 1 0 t h F l o o r , O n e E - C o m C e n t e r , H a r b o r D r i v e , M a l l o f A s i a C o m p l e x , C B P - 1 A , P a s a y C i t y 1 3 0 0 Form Type Department requiring the report Secondary License Type, If Applicable 1 7 - A COMPANY INFORMATION Company’s Email Address Company’s Telephone Number/s Mobile Number – 8857-0100 – Annual Meeting Fiscal Year No. of Stockholders Month/Day Month/Day 1,260 (as of March 31, 2021) 04/28 12/31 CONTACT PERSON INFORMATION The designated contact person MUST be an Officer of the Corporation Name of Contact Person Email Address Telephone Number/s Mobile Number Mr. Frederic C. DyBuncio – 8857-0100 – Contact Person’s Address th 10 Floor, One E-Com Center, Harbor Drive, Mall of Asia Complex, CBP-1A, Pasay City 1300 Note: In case of death, resignation or cessation of office of the officer designated as contact person, such incident shall be reported to the Commission within thirty (30) calendar days from the occurrence thereof with information and complete contact details of the new contact person designated. -

Diversification Strategies of Large Business Groups in the Philippines

Philippine Management Review 2013, Vol. 20, 65‐82. Diversification Strategies of Large Business Groups in the Philippines Ben Paul B. Gutierrez and Rafael A. Rodriguez* University of the Philippines, College of Business Administration, Diliman, Quezon City 1101, Philippines This paper describes the diversification strategies of 11 major Philippine business groups. First, it reviews the benefits and drawbacks of related and unrelated diversification from the literature. Then, it describes the forms of diversification being pursued by some of the large Philippine business groups. The paper ends with possible explanations for the patterns of diversification observed in these Philippine business groups and identifies directions for future research. Keywords: related diversification, unrelated diversification, Philippine business groups 1 Introduction This paper will describe the recent diversification strategies of 11 business groups in the Philippines. There are various definitions of business groups but in this paper, these are clusters of legally distinct firms with a managerial relationship, usually by virtue of common ownership. The focus on business groups rather than on individual firms has to do with the way that business firms in the Philippines are organized and managed. Businesses that are controlled and managed by essentially the same set of principal owners are often organized as separate corporations, not as separate divisions within the same firm, as is often the case in American corporations like General Electric, Procter and Gamble, or General Motors (Echanis, 2009). Moreover, studies on emerging markets have pointed out that business groups often occupy dominant positions in the business landscape in markets like India, Korea, Indonesia, Thailand, and the Philippines (Khanna & Palepu, 1997; Khanna & Yafeh, 2007).