Handbook on Exempted Supplies Under GST

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

EQUITY DIVIDEND for the YEAR 2012-2013 Details of Unclaimed Dividend Amount As on Date of Annual General Meeting (AGM Date - 4Th August, 2018) SI

WOCKHARDT LIMITED - EQUITY DIVIDEND FOR THE YEAR 2012-2013 Details of unclaimed dividend amount as on date of Annual General Meeting (AGM Date - 4th August, 2018) SI. Name of Shareholders Address State Pin code Folio No. / DP ID Dividend Proposed Date no. Client ID No. Amount of Transfer to unclaimed IEPF in ( Rs.) 1 A D RAMYA 6/25 SUN SANDS APTS 4TH SEAWAR D TIRUVANMIYUR Tamil Nadu 600041 1207650000003316 50.00 07-Oct-2020 CHENNAI 2 A K GARG C/O M/S ANAND SWAROOP FATEHGANJ [MANDI] Uttar Pradesh 203001 W0000966 1500.00 07-Oct-2020 BULUNDSHAHAR 3 A M LAZAR ALAMIPALLY KANHANGAD Kerala 671315 W0029284 3000.00 07-Oct-2020 4 A M NARASIMMABHARATHI NO 140/3 BAZAAR STREET AMMIYARKUPPAM PALLIPET-TK Tamil Nadu 631301 1203320004114751 125.00 07-Oct-2020 THIRUVALLUR DT THIRUVALLUR 5 A MALLIKARJUNA RAO DOOR NO 1/1814 Y M PALLI KADAPA Andhra Pradesh 516004 IN30232410966260 250.00 07-Oct-2020 6 A RAJASEKHAR REDDY MIG NO 29 APHB COLONY KORRAPADU ROAD KADAPA DIST Andhra Pradesh 516360 1204470003205849 10.00 07-Oct-2020 PRODDATUR 7 A SATHISH KUMAR W 6, NORTH MAIN ROAD, ANNANAGAR WEST, CHENNAI Tamil Nadu 600101 1203500000082702 25.00 07-Oct-2020 8 A SELVAKUMARI W/O R AMARNATH 52 APPU ST SALEM Tamil Nadu 636002 W0033114 1000.00 07-Oct-2020 9 A SUNILA B 301 GULMOHAR CHS SECTOR 42 NERUL WEST NAVI Maharashtra 400070 IN30021411886342 50.00 07-Oct-2020 MUMBAI 10 A T MRANGARAMANUJAM ADVOCATE 3-6-369/A/10 STREET NO 1 HIMAYATNAGAR Andhra Pradesh 500029 W0013258 2000.00 07-Oct-2020 HYDERABAD 11 AARADHANA GUPTA H NO -1968, INDIRA NAGAR, ORAI Uttar Pradesh 285001 1205460000168915 -

Categorization of Stringed Instruments with Multifractal Detrended Fluctuation Analysis

CATEGORIZATION OF STRINGED INSTRUMENTS WITH MULTIFRACTAL DETRENDED FLUCTUATION ANALYSIS Archi Banerjee*, Shankha Sanyal, Tarit Guhathakurata, Ranjan Sengupta and Dipak Ghosh Sir C.V. Raman Centre for Physics and Music Jadavpur University, Kolkata: 700032 *[email protected] * Corresponding Author ABSTRACT Categorization is crucial for content description in archiving of music signals. On many occasions, human brain fails to classify the instruments properly just by listening to their sounds which is evident from the human response data collected during our experiment. Some previous attempts to categorize several musical instruments using various linear analysis methods required a number of parameters to be determined. In this work, we attempted to categorize a number of string instruments according to their mode of playing using latest-state-of-the-art robust non-linear methods. For this, 30 second sound signals of 26 different string instruments from all over the world were analyzed with the help of non linear multifractal analysis (MFDFA) technique. The spectral width obtained from the MFDFA method gives an estimate of the complexity of the signal. From the variation of spectral width, we observed distinct clustering among the string instruments according to their mode of playing. Also there is an indication that similarity in the structural configuration of the instruments is playing a major role in the clustering of their spectral width. The observations and implications are discussed in detail. Keywords: String Instruments, Categorization, Fractal Analysis, MFDFA, Spectral Width INTRODUCTION Classification is one of the processes involved in audio content description. Audio signals can be classified according to miscellaneous criteria viz. speech, music, sound effects (or noises). -

The Asian Indian Classical Music Society Vishwa Mohan Bhatt

The Asian Indian Classical Music Society 52318 N Tally Ho Drive, South Bend, IN 46635 March 28 , 2013 Dear Friends, I am writing to inform you about our concerts for Spring 2013: Vishwa Mohan Bhatt (Mohan Veena or Guitar) with Subhen Chatterjee (Tabla) April 10th , 2013, Wedneday,7.00 PM, at the Hesburgh Center Auditorium Pandit Vishwa Mohan Bhatt is among the leading Indian classical instrumental musicians. He is the creator of the Mohan Veena, which has modified the Hawaiian slide guitar by adding fourteen additional strings to it, and allows him to exquisitely assimilate the techniques of the sitar, sarod and veena. He is one of the foremost disciples of Pandit Ravi Shankar. He has captivated audiences at numerous concerts in the US, Canada, Europe, the Middle East and, of course, India. Among numerous other awards, he is the recipient of the Grammy Award, 1994, with Ry Cooder, for the World Music album, A Meeting by the River. Shanmukha Priya and Hari Priya (Vocal) with M.A. Krishnaswamy (Violin) and Skandasubramanian (Mridangam), April 26th , 2013, Friday, 7.00PM, place: TBA Shanmukha Priya and Hari Priya, the renowned musical duo popularly known as the “Priya Sisters”, are among the leading exponents of the Carnatic or South Indian vocal music. After receiving their training from the renowned duo, Radha and Jayalakshmi, they are now under the guidance of Prof. T. R.Subramaniam. Since they began performing in 1989, the Priya Sisters have performed worldwide in more than two thousand concerts. Among other awards, the sisters have been the recipients of the 'Best Female Vocalists' awards from Music Academy, Sri Krishna Gana Sabha and the Indian Fine Arts Society, Chennai. -

List of Empanelled Artist

INDIAN COUNCIL FOR CULTURAL RELATIONS EMPANELMENT ARTISTS S.No. Name of Artist/Group State Date of Genre Contact Details Year of Current Last Cooling off Social Media Presence Birth Empanelment Category/ Sponsorsred Over Level by ICCR Yes/No 1 Ananda Shankar Jayant Telangana 27-09-1961 Bharatanatyam Tel: +91-40-23548384 2007 Outstanding Yes https://www.youtube.com/watch?v=vwH8YJH4iVY Cell: +91-9848016039 September 2004- https://www.youtube.com/watch?v=Vrts4yX0NOQ [email protected] San Jose, Panama, https://www.youtube.com/watch?v=YDwKHb4F4tk [email protected] Tegucigalpa, https://www.youtube.com/watch?v=SIh4lOqFa7o Guatemala City, https://www.youtube.com/watch?v=MiOhl5brqYc Quito & Argentina https://www.youtube.com/watch?v=COv7medCkW8 2 Bali Vyjayantimala Tamilnadu 13-08-1936 Bharatanatyam Tel: +91-44-24993433 Outstanding No Yes https://www.youtube.com/watch?v=wbT7vkbpkx4 +91-44-24992667 https://www.youtube.com/watch?v=zKvILzX5mX4 [email protected] https://www.youtube.com/watch?v=kyQAisJKlVs https://www.youtube.com/watch?v=q6S7GLiZtYQ https://www.youtube.com/watch?v=WBPKiWdEtHI 3 Sucheta Bhide Maharashtra 06-12-1948 Bharatanatyam Cell: +91-8605953615 Outstanding 24 June – 18 July, Yes https://www.youtube.com/watch?v=WTj_D-q-oGM suchetachapekar@hotmail 2015 Brazil (TG) https://www.youtube.com/watch?v=UOhzx_npilY .com https://www.youtube.com/watch?v=SgXsRIOFIQ0 https://www.youtube.com/watch?v=lSepFLNVelI 4 C.V.Chandershekar Tamilnadu 12-05-1935 Bharatanatyam Tel: +91-44- 24522797 1998 Outstanding 13 – 17 July 2017- No https://www.youtube.com/watch?v=Ec4OrzIwnWQ -

Rock to Raga: the Many Lives of the Indian Guitar

Open Research Online The Open University’s repository of research publications and other research outputs Rock to Raga: the many lives of the Indian guitar Book Section How to cite: Clayton, Martin (2001). Rock to Raga: the many lives of the Indian guitar. In: Bennett, Andy and Dawe, Kevin eds. Guitar cultures. Oxford, UK: Berg Publishers Ltd, pp. 179–208. For guidance on citations see FAQs. c 2001 Berg Publishers Ltd Version: Accepted Manuscript Link(s) to article on publisher’s website: http://www.bergpublishers.com/?tabid=1499 Copyright and Moral Rights for the articles on this site are retained by the individual authors and/or other copyright owners. For more information on Open Research Online’s data policy on reuse of materials please consult the policies page. oro.open.ac.uk Rock to Raga: The many lives of the Indian guitar Martin Clayton Chapter for “Guitar Culture”, ed. Dawe/ Bennett, Berg. 2nd DRAFT 1. Introduction What roles does the guitar play, and what meanings does it convey in India? 1 These are not easy questions to answer, since the instrument has spread into many different musical genres, in various geographical regions of the subcontinent. This chapter is nonetheless an attempt, in response to those questions, to sketch out the main features of guitar culture in India. I see it as a kind of snapshot: partial, blurred and lacking fine definition perhaps, but offering a perspective that more focused and tightly-framed studies could not. My account is based on a few weeks’ travel in India, 2 concentrating on the main metropolitan cities of Chennai, Mumbai, Calcutta and Delhi – although it also draws on the reports of many inhabitants of these cities who have migrated from other regions, particularly those rich in guitar culture such as Goa and the north-eastern states. -

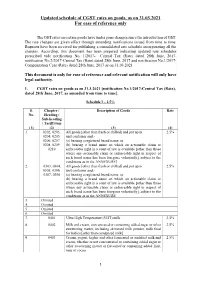

GST Notifications (Rate) / Compensation Cess, Updated As On

Updated schedule of CGST rates on goods, as on 31.03.2021 For ease of reference only The GST rates on certain goods have under gone changes since the introduction of GST. The rate changes are given effect through amending notifications issued from time to time. Requests have been received for publishing a consolidated rate schedule incorporating all the changes. According, this document has been prepared indicating updated rate schedules prescribed vide notification No. 1/2017- Central Tax (Rate) dated 28th June, 2017, notification No.2/2017-Central Tax (Rate) dated 28th June, 2017 and notification No.1/2017- Compensation Cess (Rate) dated 28th June, 2017 as on 31.03.2021 This document is only for ease of reference and relevant notification will only have legal authority. 1. CGST rates on goods as on 31.3.2021 [notification No.1/2017-Central Tax (Rate), dated 28th June, 2017, as amended from time to time]. Schedule I – 2.5% S. Chapter / Description of Goods Rate No. Heading / Sub-heading / Tariff item (1) (2) (3) (4) 1. 0202, 0203, All goods [other than fresh or chilled] and put up in 2.5% 0204, 0205, unit container and,- 0206, 0207, (a) bearing a registered brand name; or 0208, 0209, (b) bearing a brand name on which an actionable claim or 0210 enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily], subject to the conditions as in the ANNEXURE] 2. 0303, 0304, All goods [other than fresh or chilled] and put up in 2.5% 0305, 0306, unit container and,- 0307, 0308 (a) bearing a registered brand name; or (b) bearing a brand name on which an actionable claim or enforceable right in a court of law is available [other than those where any actionable claim or enforceable right in respect of such brand name has been foregone voluntarily], subject to the conditions as in the ANNEXURE 3. -

Folk Instruments of Punjab

Folk Instruments of Punjab By Inderpreet Kaur Folk Instruments of Punjab Algoza Gharha Bugchu Kato Chimta Sapp Dilruba Gagar Dhadd Ektara Dhol Tumbi Khartal Sarangi Alghoza is a pair of woodwind instruments adopted by Punjabi, Sindhi, Kutchi, Rajasthani and Baloch folk musicians. It is also called Mattiyan ,Jōrhi, Pāwā Jōrhī, Do Nālī, Donāl, Girāw, Satārā or Nagōze. Bugchu (Punjabi: ਬੁਘਚੂ) is a traditional musical instrument native to the Punjab region. It is used in various cultural activities like folk music and folk dances such as bhangra, Malwai Giddha etc. It is a simple but unique instrument made of wood. Its shape is much similar to damru, an Indian musical instrument. Chimta (Punjabi: ਚਚਮਟਾ This instrument is often used in popular Punjabi folk songs, Bhangra music and the Sikh religious music known as Gurbani Kirtan. Dilruba (Punjabi: ਚਿਲਰੱਬਾ; It is a relatively young instrument, being only about 300 years old. The Dilruba (translated as robber of the heart) is found in North India, primarily Punjab, where it is used in Gurmat Sangeet and Hindustani classical music and in West Bengal. Dhadd (Punjabi: ਢੱਡ), also spelled as Dhad or Dhadh is an hourglass-shaped traditional musical instrument native to Punjab that is mainly used by the Dhadi singers. It is also used by other folk singers of the region Dhol (Hindi: ढोल, Punjabi: ਢੋਲ, can refer to any one of a number of similar types of double-headed drum widely used, with regional variations, throughout the Indian subcontinent. Its range of distribution in India, Bangladesh and Pakistan primarily includes northern areas such as the Punjab, Haryana, Delhi, Kashmir, Sindh, Assam Valley Gagar (Punjabi: ਗਾਗਰ, pronounced: gāger), a metal pitcher used to store water in earlier days, is also used as a musical instrument in number of Punjabi folk songs and dances. -

GCSE Music Revision Booklet

GCSE Music Revision Booklet Dr T Pankhurst Preparing for the exam You need over the next month to develop your listening skills and learn various technical terms and facts about the Areas of Study. The listening skills is what I will concentrate on in class, leaving you to do most of the fact-bashing at home. I will run revision sessions to help with understanding technical vocabulary and the finer points of the Areas of Study topics Revision sessions In addition to lessons in class the following revision sessions will definitely run from 3-4 (I may add a few others if I can): Wednesday 16th May, Friday 20th May, Tuesday 24th May, Tuesday 7th June and Wednesday 8th June. Please email me on [email protected]. MAD TSHIRT It is vital that you use the MAD TSHIRT Melody mnemonic to help prompt you to talk Articulation about relevant and sufficiently technical Dynamics aspects of the music. Texture Structure Harmony Instrumentation Rhythm Time Signature Contents 1. Mad T-Shirt Page 2 2. AoS 2 Page 11 3. AoS 3 Page 18 4. AoS 4 Page 24 5. Chords and Keys Page 26 6. Music periods Online Where there are red {LISTEN} signs you can go to www.alevelmusic.com and follow the GCSE link to find the relevant example. Listen to orchestral instruments: http://www.dsokids.com/listen/by-instrument/.aspx Listen to and practice basics of intervals etc: http://www.auralworkshop.com/index.htm GCSE revision materials: http://www.bbc.co.uk/schools/gcsebitesize/music/ OCR specific materials: http://www.musicalcontexts.co.uk/index_files/page0007.htm In the AoS notes there is suggested listening that you should search for on Youtube. -

Model Music Curriculum: Key Stages 1 to 3 Non-Statutory Guidance for the National Curriculum in England

Model Music Curriculum: Key Stages 1 to 3 Non-statutory guidance for the national curriculum in England March 2021 Foreword If it hadn’t been for the classical music played before assemblies at my primary school or the years spent in school and church choirs, I doubt that the joy I experience listening to a wide variety of music would have gone much beyond my favourite songs in the UK Top 40. I would have heard the wonderful melodies of Carole King, Elton John and Lennon & McCartney, but would have missed out on the beauty of Handel, Beethoven and Bach, the dexterity of Scott Joplin, the haunting melody of Clara Schumann’s Piano Trio in G, evocations of America by Dvořák and Gershwin and the tingling mysticism of Allegri’s Miserere. The Model Music Curriculum is designed to introduce the next generation to a broad repertoire of music from the Western Classical tradition, and to the best popular music and music from around the world. This curriculum is built from the experience of schools that already teach a demanding and rich music curriculum, produced by an expert writing team led by ABRSM and informed by a panel of experts – great teachers and musicians alike – and chaired by Veronica Wadley. I would like to thank all involved in producing and contributing to this important resource. It is designed to assist rather than to prescribe, providing a benchmark to help teachers, school leaders and curriculum designers make sure every music lesson is of the highest quality. In setting out a clearly sequenced and ambitious approach to music teaching, this curriculum provides a roadmap to introduce pupils to the delights and disciplines of music, helping them to appreciate and understand the works of the musical giants of the past, while also equipping them with the technical skills and creativity to compose and perform. -

Agenda for 21 GST Council Meeting

Confidential Agenda for 21st GST Council Meeting 9 September 2017 Hyderabad, Telangana Page 2 of 173 F.No. 144/21st Meeting/GST Council/2017 GST Council Secretariat Room No.275, North Block, New Delhi Dated: 5 September 2017 Notice for the 21st Meeting of the GST Council on 9 September 2017 The undersigned is directed to refer to the subject cited above and to say that the 21st meeting of the GST Council will be held on 9 September 2017 at Hyderabad International Convention Centre, Novotel Hotel, Madhapur, Hyderabad. The schedule of the meeting is as follows: i. Saturday, 9 September 2017 : 1100 hours onwards 2. In addition, an officers’ meeting will be held at the same venue as per the following schedule: ii. Friday, 8 September 2017 : 1500 hours onwards 3. The agenda items for the 21st GST Council Meeting are attached. 4. Keeping in view the constraints of rooms in the hotel, it is requested that participation from each State may be limited to 2 officers in addition to the Hon’ble Member of the GST Council. 5. Please convey the invitation to the Hon’ble Members of the GST Council to attend the 21st GST Council Meeting. - Sd - (Dr. Hasmukh Adhia) Secretary to the Govt. of India and ex-officio Secretary to the GST Council Tel: 011 23092653 Copy to: 1. PS to the Hon’ble Minister of Finance, Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting. 2. PS to Hon’ble Minister of State (Finance), Government of India, North Block, New Delhi with the request to brief Hon’ble Minister about the above said meeting. -

Annual Report 1990 .. 91

SANGEET NAT~AKADEMI . ANNUAL REPORT 1990 ..91 Emblem; Akademi A wards 1990. Contents Appendices INTRODUCTION 0 2 Appendix I : MEMORANDUM OF ASSOCIATION (EXCERPTS) 0 53 ORGANIZATIONAL SET-UP 05 AKADEMI FELLOWSHIPS/ AWARDS Appendix II : CALENDAR OF 19900 6 EVENTS 0 54 Appendix III : GENERAL COUNCIL, FESTIVALS 0 10 EXECUTIVE BOARD, AND THE ASSISTANCE TO YOUNG THEATRE COMMITTEES OF THE WORKERS 0 28 AKADEMID 55 PROMOTION AND PRESERVATION Appendix IV: NEW AUDIO/ VIDEO OF RARE FORMS OF TRADITIONAL RECORDINGS 0 57 PERFORMING ARTS 0 32 Appendix V : BOOKS IN PRINT 0 63 CULTURAL EXCHANGE Appendix VI : GRANTS TO PROGRAMMES 0 33 INSTITUTIONS 1990-91 064 PUBLICATIONS 0 37 Appendix VII: DISCRETIONARY DOCUMENTATION / GRANTS 1990-91 071 DISSEMINATION 0 38 Appendix VIll : CONSOLIDATED MUSEUM OF MUSICAL BALANCE SHEET 1990-91 0 72 INSTRUMENTS 0 39 Appendix IX : CONSOLIDATED FINANCIAL ASSISTANCE TO SCHEDULE OF FIXED CULTURAL INSTITUTIONS 0 41 ASSETS 1990-91 0 74 LIBRARY AND LISTENING Appendix X : PROVIDENT FUND ROOMD41 BALANCE SHEET 1990-91 078 BUDGET AND ACCOUNTS 0 41 Appendix Xl : CONSOLIDATED INCOME & EXPENDITURE IN MEMORIAM 0 42 ACCOUNT 1990-91 KA THAK KENDRA: DELHI 0 44 (NON-PLAN & PLAN) 0 80 JA WAHARLAL NEHRU MANIPUR Appendix XII : CONSOLIDATED DANCE ACADEMY: IMPHAL 0 50 INCOME & EXPENDITURE ACCOUNT 1990-91 (NON-PLAN) 0 86 Appendix Xlll : CONSOLIDATED INCOME & EXPENDITURE ACCOUNT 1990-91 (PLAN) 0 88 Appendix XIV : CONSOLIDATED RECEIPTS & PAYMENTS ACCOUNT 1990-91 (NON-PLAN & PLAN) 0 94 Appendix XV : CONSOLIDATED RECEIPTS & PAYMENTS ACCOUNT 1990-91 (NON-PLAN) 0 104 Appendix XVI : CONSOLIDATED RECEIPTS & PAYMENTS ACCOUNT 1990-91 (PLAN) 0 110 Introduction Apart from the ongoing schemes and programmes, the Sangeet Natak Akademi-the period was marked by two major National Academy of Music, international festivals presented Dance, and Drama-was founded by the Akademi in association in 1953 for the furtherance of with the Indian Council for the performing arts of India, a Cultural Relations. -

Drum Racks for Ableton Live.Pages

"Masters Of India - Drum Racks For Ableton Live EarthMoments presents - Percussion Masters of India. This pack was recorded with leading industry musicians all over India. All sounds & samples are recorded using A-class pre-amps and microphones while paying attention to the instruments finer "details to capture their bloom in a perfect way. Experience India’s drums as never before. Own an unrivaled, premium quality pack "of live drum recordings that were collected using instruments from all across India. This is a quintessential Earthmoments pack that shows the artist just how much more there is to Indian drumming than just the tabla. Every major Indian drum except the "tabla is included in this pack. Also included is a bonus Earthmoments Sampler, a taster from the essential "boutique sample library.! The drums presented in the pack are the: Bass Dholak, Chellangai, Duki Tharang, Ganjira, Gatham Singarri, Gatham, Khol, Mirudangam, Pakhwaj, Tapatam, Thalam, "Thavil, and the Udukai. For each instrument, EarthMoments has provided 10 pre-made patterns to demonstrate what that instrument is fully capable of. These are not just traditionally Indian patterns either, but include some western styles as a demonstration of the "versatility of these instruments. "Instruments: Bass Dholak - Bass Dholak is a large wooden barrel shaped drum associated with the folk music of Punjab. The drum is hung around the neck and the bass and treble "heads on either side are struck using sticks. Chellangai - The complex movement of Indian dancers is translated into sound with the Chellangai. These bells worn as anklets serve to accentuate the intricate footwork of each dancer, moving in step with accompanying percussion.