Central Europe 2012 Uncovering the Core

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Liberty Global Unveils Its Smallest, Most Environmentally-Friendly Set Top Box

LIBERTY GLOBAL UNVEILS ITS SMALLEST, MOST ENVIRONMENTALLY-FRIENDLY SET TOP BOX UPC Poland Becomes First Liberty Global Company to Launch New 4K Mini TV Box London, United Kingdom – August 24, 2020 Liberty Global plc (NASDAQ: LBTYA, LBTYB and LBTYK), one of the world’s leading converged video, broadband and communications companies, is today introducing its greenest-ever set top box, delivering a world-class viewing experience while dramatically reducing energy consumption and the use of plastics. Designed in-house by engineers at Liberty Global and manufactured by CommScope, the compact, multi- faceted 4K Mini TV Box combines a high-quality customer experience and rich choice of content with extremely low power consumption and a casing that’s partially made from recycled plastic. The 4K Mini TV Box will be available from today to UPC Poland customers and will be introduced in other Liberty Global markets in due course. SMALL IN SIZE – BUT BIG IN IMPACT Despite its small size, the media box gives customers complete control over their entertainment experience by providing access to the full spectrum of content including live TV, replay TV, on demand content and access to a range of in-built OTT apps, all in crystal-clear image quality up to 4K, combined with Dolby sound. Additionally, the 4K Mini TV Box also allows users to stream self-generated content from their phones direct to their TV and is operated by a Bluetooth-connected voice-enabled remote control. Built with a seamless user set-up experience in mind, the 4K Mini TV Box is powered by Liberty Global’s next generation TV platform, Horizon 4. -

Match Notes Internationaux De Strasbourg - Strasbourg, France 2021-05-23 - 2021-05-29 | $ 235,238

26/05/2021 SAP Tennis Analytics 1.4.9 MATCH NOTES INTERNATIONAUX DE STRASBOURG - STRASBOURG, FRANCE 2021-05-23 - 2021-05-29 | $ 235,238 1 0 win win 1 matches played 61 Sorana Shuai Cirstea (6) Zhang 45 ROMANIA CHINA 1990-04-07 Date of Birth 1989-01-21 Targoviste, Romania Residence Tianjin, China Right-handed (two-handed backhand) Plays Right-handed (two-handed backhand) 5' 9" (1.76 m) Height 5' 10" (1.77 m) 21 Career-High Ranking 23 $6,064,123 Career Prize Money $6,952,466 $233,024 Season Prize Money $160,240 1 / 2 Singles Titles YTD / Career 0 / 2 47-48 (QF: 2009 Roland Garros) Grand Slam W-L (best) 28-34 (QF: 2019 Wimbledon; 2016 Australian Open) 1-0 / 1-1 (Second round: 2021) YTD / Career STRASBOURG W-L 1-0 / 4-4 (Quarter-Finalist: 2020) (best) 12-6 / 242-252 YTD / Career W-L 1-7 / 178-200 6-1 / 83-77 YTD / Career Clay W-L 1-5 / 31-49 2-1 / 90-75 YTD / Career 3-Set W-L 0-1 / 51-49 3-1 / 56-46 YTD / Career TB W-L 0-1 / 42-45 Champion: Istanbul YTD Best Result Second round: Strasbourg https://dev.saptennis.com/media/mediaportal/#season/2021/events/0406/matches/LS009/apps/post-match-insights/match-notes/snapshots/58b5f… 1/8 26/05/2021 SAP Tennis Analytics 1.4.9 MATCH NOTES INTERNATIONAUX DE STRASBOURG - STRASBOURG, FRANCE 2021-05-23 - 2021-05-29 | $ 235,238 Sorana Shuai Cirstea Zhang Head To Head Record YEAR TOURNAMENT SURFACE ROUND WINNER SCORE/ RESULT TIME 2008 CUNEO CLAY 1r Sorana Cirstea 6-3 4-6 6-3 0m Ranking History TOP RANK YEAR-END YEAR TOP RANK YEAR-END 58 - 2021 35 - 69 86 2020 30 35 72 72 2019 31 46 33 86 2018 27 35 37 37 2017 23 36 81 81 2016 24 24 90 244 2015 61 186 21 93 2014 30 62 21 22 2013 51 51 26 27 2012 120 122 https://dev.saptennis.com/media/mediaportal/#season/2021/events/0406/matches/LS009/apps/post-match-insights/match-notes/snapshots/58b5f… 2/8 26/05/2021 SAP Tennis Analytics 1.4.9 MATCH NOTES INTERNATIONAUX DE STRASBOURG - STRASBOURG, FRANCE 2021-05-23 - 2021-05-29 | $ 235,238 Sorana Shuai Cirstea Zhang Tournament History CURRENT TOURNAMENT CURRENT TOURNAMENT 1r: d. -

Proceedings+Of+The+8Th+ Scheduling+And+Planning+

ICAPS 2014 ! ! Proceedings+of+the+8th+ Scheduling+and+Planning+Applications+Workshop+ + Edited+By:+ Gabriella+Cortellessa,+Mark+Giuliano,+Riccardo+Rasconi+and+Neil+Yorke@Smith+ + Portsmouth,*New*Hampshire,*USA*5*June*22,*2014* * Organizing*Committee* Gabriella(Cortellessa! ISTC&CNR,!Italy! Mark(Giuliano( Space!Telescope!Science!Institute,!USA!! Riccardo(Rasconi! ISTC&CNR,!Italy! Neil(Yorke6Smith( American!University!of!Beirut,!Lebanon,!and!University!of!Cambridge,!UK! ! Program*Committee* Laura(Barbulescu,!Carnegie!Mellon!University,!USA!! Anthony(Barrett,!Jet!Propulsion!Laboratory,!USA!! Mark(Boddy,!Adventium,!USA!! Luis(Castillo,!University!of!Granada,!Spain!! Gabriella(Cortellessa,!ISTC&CNR,!Italy! Riccardo(De(Benedictis,!ISTC&CNR,!Italy!! Minh(Do,!SGT!Inc.,!NASA!Ames,!USA!! Simone(Fratini,!ESA&ESOC,!Germany!! Mark(Giuliano,!Space!Telescope!Science!Institute,!USA! Christophe(Guettier,!SAGEM,!France!! Patrik(Haslum,!NICTA,!Australia!! Nicola(Policella,!ESA&ESOC,!Germany!! Riccardo(Rasconi,!ISTC&CNR,!Italy! Bernd(Schattenberg,!University!of!Ulm,!Germany!! Tiago(Vaquero,!University!of!Toronto,!Canada!! Ramiro(Varela,!University!of!Oviedo,!Spain!! Gérard(Verfaillie,!ONERA,!France!! Neil(Yorke6Smith,!American!University!of!Beirut,!Lebanon!and!University!of!Cambridge,!UK! Terry(Zimmerman,!University!of!Washington!–!Bothell,!USA! ! ! ! ! ! ! ! ! ! ! ! ! ! Foreword! ! Application!domains!that!entail!planning!and!scheduling!(P&S)!problems!present!a!set!of!compelling!challenges! to!the!AI!planning!and!scheduling!community,!from!modeling!to!technological!to!institutional!issues.!New!real& -

Retail of Food Products in the Baltic States

RETAIL OF FOOD PRODUCTS IN THE BALTIC STATES FLANDERS INVESTMENT & TRADE MARKET SURVEY Retail of food products in the Baltic States December 2019 Flanders Investment & Trade Vilnius Retail of Food Products in the Baltic States| December 2019 1 Content Executive summary ................................................................................................................................. 3 Overview of the consumption market Baltic States ................................................................................ 4 Economic forecasts for the Baltic States ............................................................................................. 4 Lithuania .......................................................................................................................................... 4 Latvia ............................................................................................................................................... 5 Estonia ............................................................................................................................................. 6 Structure of distribution and market entry in the Baltic States ............................................................ 13 Structure ............................................................................................................................................ 13 Market entry ..................................................................................................................................... 14 Key -

Submissions to Public Consultation on New RTÉ Service Proposals

Roinn Cumarsáide, Fuinnimh agus Acmhainní Nádúrtha Department of Communications, Energy and Natural Resources Submissions to Public Consultation on New RTÉ Service Proposals Publication Date: 23rd February 2011 Contents Page 1 Submissions ...........................................................................................................4 2 Professor Paolo Bartoloni ......................................................................................5 3 Seo O'Catháin........................................................................................................6 4 Comhluadar..........................................................................................................12 5 Community Television Association.....................................................................14 6 Conradh na Gaeilge..............................................................................................17 7 David Costigan.....................................................................................................19 8 EIRCOM..............................................................................................................20 9 FIG .......................................................................................................................22 10 Football Association of Ireland......................................................................26 11 French Teachers Association of Ireland ........................................................27 12 Gael Linn.......................................................................................................28 -

Broadband Coverage in Europe Final Report 2009 Survey Data As of 31 December 2008

Ref. Ares(2013)3033573 - 11/09/2013 Broadband Coverage in Europe Final Report 2009 Survey Data as of 31 December 2008 DG INFSO 80106 December 2009 IDATE 1 Development of Broadband Access in Europe Table of contents 1. Methodological notes .......................................................................................................................................5 2. Executive summary ..........................................................................................................................................7 3. European benchmark .......................................................................................................................................9 3.1. EU-27 + Norway & Iceland at the end of 2008........................................................................................ 9 3.1.1. Fixed broadband subscriber bases and penetration.................................................................... 9 3.1.2. DSL coverage and penetration.................................................................................................. 11 3.1.3. Cable modem coverage and penetration .................................................................................. 18 3.1.4. FTTH subscribers...................................................................................................................... 24 3.1.5. Satellite solutions ...................................................................................................................... 25 3.1.6. 3G coverage and take-up......................................................................................................... -

The UPC Holding Group

The UPC Holding Group Combined Financial Statements December 31, 2020 The UPC Holding Group TABLE OF CONTENTS Page Number PART I Forward-looking Statements............................................................................................................................................ I-1 Business............................................................................................................................................................................ I-2 Risk Factors...................................................................................................................................................................... I-20 PART II Independent Auditors’ Report.......................................................................................................................................... II-1 Combined Balance Sheets as of December 31, 2020 and 2019....................................................................................... II-3 Combined Statements of Operations for the Years Ended December 31, 2020, 2019 and 2018.................................... II-5 Combined Statements of Comprehensive Earnings (Loss) for the Years Ended December 31, 2020, 2019 and 2018... II-6 Combined Statements of Equity (Deficit) for the Years Ended December 31, 2020, 2019 and 2018............................. II-7 Combined Statements of Cash Flows for the Years Ended December 31, 2020, 2019 and 2018 .................................. II-10 Notes to Combined Financial Statements....................................................................................................................... -

GOLDBERG, GODLES, WIENER & WRIGHT April 22, 2008

LAW OFFICES GOLDBERG, GODLES, WIENER & WRIGHT 1229 NINETEENTH STREET, N.W. WASHINGTON, D.C. 20036 HENRY GOLDBERG (202) 429-4900 JOSEPH A. GODLES TELECOPIER: JONATHAN L. WIENER (202) 429-4912 LAURA A. STEFANI [email protected] DEVENDRA (“DAVE”) KUMAR HENRIETTA WRIGHT THOMAS G. GHERARDI, P.C. COUNSEL THOMAS S. TYCZ* SENIOR POLICY ADVISOR *NOT AN ATTORNEY April 22, 2008 ELECTRONIC FILING Marlene H. Dortch, Secretary Federal Communications Commission 445 12th Street, SW Washington, DC 20554 Re: Broadband Industry Practices, WC Docket No. 07-52 Dear Ms. Dortch: On April 21, on behalf of Vuze, Inc. (“Vuze”), the undersigned e-mailed the attached material to Aaron Goldberger and Ian Dillner, both legal advisors to Chairman Kevin J. Martin. The material reflects the results of a recent study conducted by Vuze, in which Vuze created and made available to its users a software plug-in that measures the rate at which network communications are being interrupted by reset messages. The Vuze plug-in measures all network interruptions, and cannot differentiate between reset activity occurring in the ordinary course and reset activity that is artificially interposed by a network operator. While Vuze, therefore, has drawn no firm conclusions from its network monitoring study, it believes the results are significant enough to raise them with network operators and commence a dialog regarding their network management practices. Accordingly, Vuze has sent the attached letters to four of the network operators whose rate of reset activity appeared to be higher than that of many others. While Vuze continues to believe that Commission involvement in this Marlene H. -

Base Prospectus Dated 25 June 2012 CITIGROUP INC. (Incorporated In

Base Prospectus dated 25 June 2012 CITIGROUP INC. (incorporated in Delaware) and CITIGROUP FUNDING INC. (incorporated in Delaware) and CITIGROUP GLOBAL MARKETS FUNDING LUXEMBOURG S.C.A. (incorporated as a corporate partnership limited by Shares (société en commandite par actions) under Luxembourg law and registered with the Register of Trade and Companies of Luxembourg under number B169 199) each an issuer under the Citi U.S.$30,000,000,000 Global Medium Term Note and Certificate Programme Notes and Certificates issued by Citigroup Funding Inc. only will be unconditionally and irrevocably guaranteed by CITIGROUP INC. (incorporated in Delaware) Under the Global Medium Term Note and Certificate Programme (the Programme) described in this Base Prospectus, (i) each of Citigroup Inc. (Citigroup Inc.) and Citigroup Funding Inc. (CFI) may from time to time issue notes (the Notes) and certificates (the Certificates and, together with the Notes, the Securities) and (ii) Citigroup Global Markets Funding Luxembourg S.C.A. (CGMFL and, together with Citigroup Inc. and CFI, the Issuers and each an Issuer) may from time to time issue Notes (but not Certificates), in each case subject to compliance with all relevant laws, regulations and directives. References herein to the relevant Issuer shall be construed as whichever of Citigroup Inc., CFI or CGMFL is the issuer or proposed issuer of the relevant Notes, in the case of CGMFL, Citigroup Inc., or CFI, or Securities in the case of CFI and Citigroup Inc. The aggregate principal amount of Notes outstanding will not at any time exceed U.S.$30,000,000,000 (or the equivalent in other currencies), subject to any increase described herein. -

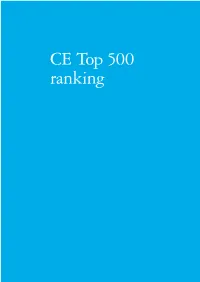

CE Top 500 Ranking

CE Top 500 ranking Central Europe Top 500 2014 43 Rank Company name Country Industry* Revenues from Revenues Net income Net income LY sales change (%) change (%) Rank 2013 2013-2012 2013 2013-2012 1 PKN Orlen Poland E&R 27,037.2 -5.8% -26.1 -106.4% 1 2 MOL Hungary E&R 18,121.1 -5.5% -65.1 -112.0% 2 3 ŠKODA AUTO Czech Republic Mfg 10,311.2 -1.4% 454.4 -25.7% 3 4 Metinvest Ukraine Mfg 9,619.0 -1.3% 294.4 -14.7% 4 5 DTEK Ukraine E&R 8,721.6 8.9% 313.1 -45.8% 7 6 ČEZ Czech Republic E&R 8,344.0 -2.6% 1,353.1 -15.3% 6 7 Energorynok Ukraine E&R 8,033.1 0.8% 4.7 10.1% 8 8 Jeronimo Martins Polska Poland CB&T 7,806.4 13.0% N/A N/A 12 9 PGNiG Poland E&R 7,627.7 11.1% 480.4 -1.8% 13 10 PGE Poland E&R 7,158.6 -1.7% 1,044.1 25.6% 10 11 Naftogaz of Ukraine Ukraine E&R 7,010.8 -25.8% -1,176.6 -10.6% 5 12 RWE Supply & Trading CZ Czech Republic E&R 6,920.8 -4.0% 923.1 -55.4% 11 13 Lotos Poland E&R 6,791.1 -14.2% 29.3 -90.4% 9 14 Volkswagen Slovakia Slovakia Mfg 6,524.3 -1.0% 45.4 -73.3% 14 15 Orlen Lietuva Lithuania E&R 6,067.3 -3.2% N/A N/A 16 16 AUDI Hungaria Motor Hungary Mfg 5,856.3 5.8% 314.4 -6.0% 19 17 AGROFERT Czech Republic Mfg 5,825.9 10.5% 215.6 -10.2% 20 18 KGHM Poland E&R 5,725.5 -10.3% 731.9 -28.2% 15 19 Petrom Romania E&R 5,477.1 -7.2% 1,091.8 23.2% 18 20 GE Infrastructure CEE Hungary Mfg 5,187.5 3.2% 463.6 -33.0% 22 21 Ukrzaliznytsia Ukraine CB&T 4,796.9 -6.2% 51.2 -40.4% 21 22 Slovnaft Slovakia E&R 4,738.1 2.0% 35.1 -32.4% 23 23 Lotos Paliwa Poland E&R 4,666.7 0.0% N/A N/A 24 24 Tauron Poland E&R 4,543.2 -23.2% 330.1 13.5% 17 25 Kia Motors -

Pianeta Distribuzione 2012

PL Documento in versione interattiva: www.largoconsumo.info/072012/CitatiPia2012.pdf SOMMARIO INTERATTIVO DI PIANETA DISTRIBUZIONE 2012 Per l'acquisto del fascicolo, o di sue singole parti, rivolgersi al servizio Diffusione e Abbonamenti [email protected] Tel. 02.3271.646 Fax. 02.3271840 LE FONTI DI QUESTO PERCORSO DI LETTURA E SUGGERIMENTI PER L'APPROFONDIMENTO DEI TEMI: Pianeta Distribuzione Osservatorio D'Impresa Rapporto annuale sul grande dettaglio internazionale Leggi le case history di comunicazioni d'impresa Un’analisi ragionata delle politiche e delle strategie di sviluppo dei grandi gruppi di Aziende e organismi distributivi internazionali, food e non food e di come competono con la attivi distribuzione locale a livello di singolo Paese. Tabelle, grafici, commenti nei mercati considerati in giornalistici, interviste ai più accreditati esponenti del retail nazionale e questo internazionale, la rappresentazione fotografica delle più importanti e recenti Percorso di lettura strutture commerciali in Italia e all’estero su Pianeta Distribuzione. selezionati da Largo Consumo http://www.intranet.largoconsumo.info/intranet/Articoli/PL/VisualizzaPL.asp (1 di 16)09/11/2009 11.46.44 PL Pianeta Distribuzione, fascicolo 7/2012, n°pagina 0, lunghezza n.d. Tipologia: Breve Spese fisse sempre più pesanti per gli italiani dal 1992 Notizie in corso - Negli ultimi venti anni la spesa delle famiglie destinata ai Proposte editoriali sugli consumi obbligati (bollette, affitti, servizi bancari e assicurativi, carburanti, stessi argomenti: spese sanitarie, trasporti, eccetera) è aumentata di oltre 7 punti percentuali passando dal 32,3% sul totale dei consumi del 1992 al 39,5% del 2011. È il dato più significativo che emerge da un'analisi dell'Ufficio Studi Confcommercio sull'evoluzione e l'incidenza delle spese obbligate sui consumi delle famiglie. -

Edible Insects

1.04cm spine for 208pg on 90g eco paper ISSN 0258-6150 FAO 171 FORESTRY 171 PAPER FAO FORESTRY PAPER 171 Edible insects Edible insects Future prospects for food and feed security Future prospects for food and feed security Edible insects have always been a part of human diets, but in some societies there remains a degree of disdain Edible insects: future prospects for food and feed security and disgust for their consumption. Although the majority of consumed insects are gathered in forest habitats, mass-rearing systems are being developed in many countries. Insects offer a significant opportunity to merge traditional knowledge and modern science to improve human food security worldwide. This publication describes the contribution of insects to food security and examines future prospects for raising insects at a commercial scale to improve food and feed production, diversify diets, and support livelihoods in both developing and developed countries. It shows the many traditional and potential new uses of insects for direct human consumption and the opportunities for and constraints to farming them for food and feed. It examines the body of research on issues such as insect nutrition and food safety, the use of insects as animal feed, and the processing and preservation of insects and their products. It highlights the need to develop a regulatory framework to govern the use of insects for food security. And it presents case studies and examples from around the world. Edible insects are a promising alternative to the conventional production of meat, either for direct human consumption or for indirect use as feedstock.