Annual Report 2016 Contents

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

A Miraculous Ningguo City of China and Analysis of Influencing Factors of Competitive Advantage

www.ccsenet.org/jgg Journal of Geography and Geology Vol. 3, No. 1; September 2011 A Miraculous Ningguo City of China and Analysis of Influencing Factors of Competitive Advantage Wei Shui Department of Eco-agriculture and Regional Development Sichuan Agricultural University, Chengdu Sichuan 611130, China & School of Geography and Planning Sun Yat-Sen University, Guangzhou 510275, China Tel: 86-158-2803-3646 E-mail: [email protected] Received: March 31, 2011 Accepted: April 14, 2011 doi:10.5539/jgg.v3n1p207 Abstract Ningguo City is a remote and small county in Anhui Province, China. It has created “Ningguo Miracle” since 1990s. Its general economic capacity has been ranked #1 (the first) among all the counties or cities in Anhui Province since 2000. In order to analyze the influencing factors of competitive advantages of Ningguo City and explain “Ningguo Miracle”, this article have evaluated, analyzed and classified the general economic competitiveness of 61 counties (cities) in Anhui Province in 2004, by 14 indexes of evaluation index system. The result showed that compared with other counties (cities) in Anhui Province, Ningguo City has more advantages in competition. The competitive advantage of Ningguo City is due to the productivities, the effect of the second industry and industry, and the investment of fixed assets. Then the influencing factors of Ningguo’s competitiveness in terms of productivity were analyzed with authoritative data since 1990 and a log linear regression model was established by stepwise regression method. The results demonstrated that the key influencing factor of Ningguo City’s competitive advantage was the change of industry structure, especially the change of manufacture structure. -

Research Article Stability and Complexity Analysis of Temperature Index Model Considering Stochastic Perturbation

Hindawi Advances in Mathematical Physics Volume 2018, Article ID 2789412, 18 pages https://doi.org/10.1155/2018/2789412 Research Article Stability and Complexity Analysis of Temperature Index Model Considering Stochastic Perturbation Jing Wang Faculty of Science, Bengbu University, Bengbu 233030, China Correspondence should be addressed to Jing Wang; [email protected] Received 20 October 2017; Accepted 12 December 2017; Published 1 January 2018 Academic Editor: Giampaolo Cristadoro Copyright © 2018 Jing Wang. Tis is an open access article distributed under the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited. A temperature index model with delay and stochastic perturbation is constructed in this paper. It explores the infuence of parameters and stochastic factors on the stability and complexity of the model. Based on historical temperature data of four cities of Anhui Province in China, the temperature periodic variation trends of approximately sinusoidal curves of four cities are given, respectively. In addition, we analyze the existence conditions of the local stability of the temperature index model without stochastic term and estimate its parameters by using the same historical data of the four cities, respectively. Te numerical simulation results of the four cities are basically consistent with the descriptions of their historical temperature data, which proves that the temperature index model constructed has good ftting degree. It also shows that unreasonable delay parameter can make the model lose stability and improve the complexity. Stochastic factors do not usually change the trend in temperature, but they can cause high frequency fuctuations in the process of temperature evolution. -

Procured Contracts February/13

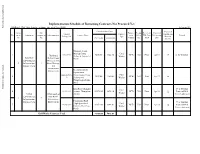

Implementation Schedule of Remaining Contracts Not Procured Yet Public Disclosure Authorized 1USD=6.3 CNY (based on the exchange rate as of Nov, 2012) February/13 Estimated Base Costs Expected Comp- Sub- Procure- Prequa- Review by Expected Contract Contract Construction No. onent Component component Sub-component Contract Name ment lifica- WB (Prior Bid Opening Remark Package No. Type Duration No. No. Mothod tion /Post) Date CNY10,000 USD10,000 (month) Wuxiaojie Storm Drainage Pump Civil 1 HSFS/S5/C1 7200.00 1142.86 NCB NO Prior Jan/13 17 in the bidding Huaishang Station & Associated Works Suburban District Flood Public Disclosure Authorized Works Environment Management & 3 Infrastructure 3 Storm Drainage Improvement and Infrastructure Reconstruction & Improvement Expansion of HSFS/S5/C6-N- Wangxiaogou Pump Civil 2 3478.00 552.06 NCB NO Post Apr/13 16 B Stations and Works Wangxiaogou Intake Ditch Public Disclosure Authorized Lilou Road (Donghai New Addition Civil 4 LZUI/S10/C1 Avenue - Huangshan 10572.00 1678.10 NCB NO Prior Apr/13 12 Project of Mid- Works Urban Urban(south of Avenue) Term Adjustment Environment Huai River) 2 3 Infrastructure Infrastructure Fengandong Road Improvement Improvement New Addition (High Speed Rail Civil 5 LZUI/S10/C2 10351.00 1643.02 NCB NO Prior Apr/13 12 Project of Mid- Culvert - Mid. Ring Works Term Adjustment Road) Civil Works Contracts Total 31601.00 5016.03 Public Disclosure Authorized Preparation of Rules and Operational Procedures for Mohekou Industrial Bid evaluation 6 C Zone (MIZ), and - 20 TA QCBS - Prior Aug/12 12 is in process Bidding Document to Select a Professional Technical Operator for MIZ Services, 4 Training and Study Tour Institutional & Financial Bid evaluation 7 E - 32 TA QBS - Prior Aug/12 12 Strengthening of is in process Utility Companies Strategy and Selection of Bengbu 8 F - 21 TA CQS - Prior Mar/13 7 Water Sector Development TA and Training Total - 73 Procured Contracts February/13 Review Estimated Cost Cost of Signed Contract Procure- Contract by WB Bid Opening Contract No. -

Huishang Bank Corporation Limited* 徽 商 銀 行 股 份 有 限

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. Huishang Bank Corporation Limited* 徽商銀行股份有限公司* (A joint stock company incorporated in the People’s Republic of China with limited liability) (Stock Code: 3698 and 4608 (Preference shares)) 2017 INTERIM RESULTS ANNOUNCEMENT The board of directors (the“ Board”) of Huishang Bank Corporation Limited (the “Bank”) is pleased to announce the unaudited interim results of the Bank and its subsidiaries for the six months ended June 30, 2017. This announcement, containing the full text of the 2017 Interim Report of the Bank, complies with the relevant content requirements of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited in relation to preliminary announcements of interim results. The printed version of the Bank’s 2017 Interim Report will be delivered to the holders of H Shares of the Bank and available for viewing on the websites of Hong Kong Exchanges and Clearing Limited at www.hkexnews.hk and of the Bank at www.hsbank.com.cn in September 2017. By order of the Board Huishang Bank Corporation Limited* Li Hongming Chairman Hefei, Anhui Province, China August 25, 2017 As at the date of this announcement, the board of directors of the Bank comprises Li Hongming, Wu Xuemin and Ci Yaping as executive directors; Zhang Feifei, Zhu Jiusheng, Qian Li, Lu Hui, Zhao Zongren, Qiao Chuanfu and Gao Yang as non-executive directors; Au Ngai Daniel, Dai Genyou, Wang Shihao, Zhang Shenghuai and Zhu Hongjun as independent non-executive directors. -

Analysis of Historic Rainfall Characteristics for Robust Wheat Cropping in North Anhui

Analysis of historic rainfall characteristics for robust wheat cropping in North Anhui Hui Su, Yibo Wu, Yulei Zhu, Youhong Song Anhui Agricultural University, School of Agronomy, Hefei, 233036. Corresponding email: [email protected] Abstract Northern part of Anhui is one of major wheat producing areas in China. The total amount of rainfall is sufficient for wheat season; however, it is unevenly distributed at the different growth stages, resulting in risk of yield losses. In order to optimise the cultivation in North Anhui, it is essential to characterise the rainfall pattern for wheat growth particularly in the critical period (i.e. the months of sowing and harvesting). By analysing the rainfall data from 1955 to 2017, this study characterised the rainfall pattern from six sites representing different regions of North Anhui. The frequency of continuous rainfall days during sowing and harvesting periods were quantified based on 63 years rainfall distribution. The characterisation of rainfall in six representative sites in North Anhui were able to be used to guide wheat sowing and harvesting, which could help farmers to make decisions and avoid likelihood of cropping risks. Key Words Winter wheat, rainfall pattern, sustainable cropping, China Introduction Huang-Huai-Hai plain is a major wheat production area in China (Yang, 2018). The northern part of Anhui province belongs to south Huang-Huai-Hai plain. The wheat sowing time normally varies 1 week before or after October 15 and harvesting is tightly closing to May 31 in the following year. The climate characteristics particularly rainfall distribution over the season are complicated in North Anhui as it is in the transitional zone between the North and South China. -

World Bank Document

CONFORMED COPY LOAN NUMBER 4597 CHA Public Disclosure Authorized Loan Agreement (Huai River Pollution Control Project) between PEOPLE’S REPUBLIC OF CHINA and Public Disclosure Authorized INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT Dated September 24, 2001 LOAN NUMBER 4597 CHA Public Disclosure Authorized LOAN AGREEMENT AGREEMENT, dated September 24, 2001, between PEOPLE'S REPUBLIC OF CHINA (the Borrower) and INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT (the Bank). WHEREAS (A) the Borrower, having satisfied itself as to the feasibility and priority of the project described in Schedule 2 to this Agreement (the Project), has requested the Bank to assist in the financing of the Project; (B) the Project will be carried out by the Borrower's Provinces of Anhui and Shandong (collectively, the Project Provinces and individually, a Project Province) with the Borrower’s assistance and, as part of such assistance, the Borrower will make the proceeds of the loan provided for in Article II of this Agreement (the Loan) available to each of the Project Provinces, as set forth in this Agreement; and WHEREAS the Bank has agreed, on the basis, inter alia, of the foregoing, to extend the Loan to the Borrower upon the terms and conditions set forth in this Agreement and in the Project Agreement of even date herewith between the Bank and the Public Disclosure Authorized Project Provinces (the Project Agreement); NOW THEREFORE the parties hereto hereby agree as follows: ARTICLE I General Conditions; Definitions Section 1.01. The "General Conditions Applicable to Loan and Guarantee Agreements for Single Currency Loans" of the Bank, dated May 30, 1995, as amended through October 6, 1999 (the General Conditions), constitute an integral part of this Agreement. -

Provenance of the Zhou Dynasty Bronze Vessels Unearthed from Zongyang County, Anhui Province, China: Determined by Lead Isotopes and Trace Elements

Provenance of the Zhou Dynasty Bronze Vessels Unearthed from Zongyang County, Anhui Province, China: Determined by Lead Isotopes and Trace Elements Yanjie Wang ( [email protected] ) Anhui University https://orcid.org/0000-0002-5768-5464 Guofeng Wei Anhui University Qiang Li Anhui University Xiaoping Zheng Wenzhou Party Institute of Cultural Relics and Archaeology Danchun Wang Anhui Museum Research Article Keywords: Bronze vessels, Mining and smelting, Lead isotopes, Trace elements, Provenance Posted Date: June 17th, 2021 DOI: https://doi.org/10.21203/rs.3.rs-176870/v1 License: This work is licensed under a Creative Commons Attribution 4.0 International License. Read Full License Version of Record: A version of this preprint was published at Heritage Science on August 20th, 2021. See the published version at https://doi.org/10.1186/s40494-021-00566-5. Page 1/20 Abstract Thirteen Zhou Dynasty bronze vessels and two slags from Zongyang County along the north bank of the Yangtze River in Anhui were analyzed by LA-MC-ICP-MS and EDXRF. The results of the lead isotope analysis showed that there were two kinds of lead materials in the Zongyang bronzes. Class which could have originated from the Wannan region were mainly used in the Western Zhou and the following Spring and Autumn periods; while Class , possibly from the local mines in Zongyang County, were mainly present in the Warring States period. Such a shift in the ore material sources is also revealed by the analysis of the trace elements of the Zongyang bronzes. With reference to relevant historical documents, it can be inferred that the transformation of the bronze material sources could be related to the changes of the political situation during the Zhou Dynasty. -

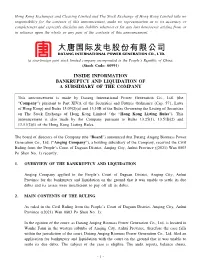

Inside Information Bankruptcy and Liquidation of a Subsidiary of the Company

Hong Kong Exchanges and Clearing Limited and The Stock Exchange of Hong Kong Limited take no responsibility for the contents of this announcement, make no representation as to its accuracy or completeness and expressly disclaim any liability whatsoever for any loss howsoever arising from or in reliance upon the whole or any part of the contents of this announcement. (a sino-foreign joint stock limited company incorporated in the People’s Republic of China) (Stock Code: 00991) INSIDE INFORMATION BANKRUPTCY AND LIQUIDATION OF A SUBSIDIARY OF THE COMPANY This announcement is made by Datang International Power Generation Co., Ltd. (the “Company”) pursuant to Part XIVA of the Securities and Futures Ordinance (Cap. 571, Laws of Hong Kong) and Rules 13.09(2)(a) and 13.10B of the Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited(the “Hong Kong Listing Rules”). This announcement is also made by the Company pursuant to Rules 13.25(1), 13.51B(2) and 13.51(2)(l) of the Hong Kong Listing Rules. The board of directors of the Company (the “Board”) announced that Datang Anqing Biomass Power Generation Co., Ltd. (“Anqing Company”), a holding subsidiary of the Company, received the Civil Ruling from the People’s Court of Daguan District, Anqing City, Anhui Province ((2021) Wan 0803 Po Shen No. 1) recently. 1. OVERVIEW OF THE BANKRUPTCY AND LIQUIDATION Anqing Company applied to the People’s Court of Daguan District, Anqing City, Anhui Province for the bankruptcy and liquidation on the ground that it was unable to settle its due debts and its assets were insufficient to pay off all its debts. -

Huangshan Hongcun Two Day Tour

! " # Guidebook $%&' Hefei Overview Hefei, capital of Anhui Province, is located in the middle part of China between the Yangtze River and the Huaihe River and beside Chaohu Lake. It occupies an area of 7,029 square kilometers of which the built-up urban area is 838.52 square kilometers. With a total population of about five million, the urban residents number about 2.7 million. As the provincial seat, the city is the political, economic, cultural, commercial and trade, transportation and information centre of Anhui Province as well as one of the important national scientific research and education bases. $% !() Hefei Attractions *+, The Memorial Temple Of Lord Bao The full name of this temple is the Memorial Temple of Lord Bao Xiaoshu. It was constructed in memory of Bao Zheng, who is idealized as an upright and honest official and a political reformer in the Song Dynasty. Xiaoshu is Lord Bao's posthumous name that was granted by Emperor Renzhong of the Song Dynasty in order to promote Lord Bao's contribution to the country. Former Residence of Li Hongzhang Lord Bao 1 -./01 Former Residence of Li Hongzhang Former Residence of Li Hongzhang is located on the Huaihe Road (the mid-section) in Hefei. It was built in the 28th year of the reign of Emperor Guangxu of the Qing Dynasty. The entire building looks magnificent with carved beams and rafters. It is the largest existing and best preserved former residence of a VIP in Hefei and is a key cultural relic site under the protection of Anhui Provincial Government. -

Supplementary Information Authors

Supplementary Information Authors: Xiaowei Song a,b, Yongpei Haoa,c* Manuscript title: Vehicular emission inventory and reduction scenario analysis in the Yangtze River Delta, China Table S1: Vehicular emission standards implementation timetable in the Yangtze River Delta, China Table S2: The survival rates of vehicles Table S3: Annual average vehicle kilometers travelled data for each vehicle category in the YRD (km) Table S4: The predicted value of vehicle kilometers travelled (km/year) Table S5: Vehicle categories in China corresponding with those in COPERT Ⅳ Table S6: The sulfur content limit in gasoline and diesel in the Yangtze River Delta (mg/kg) Table S7: Vehicular emission standards implementation timetable Table S8: The emission factors of hybrid and natural gas vehicles Table S9: The single vehicle emissions in well-to-tank phase in 2020 (g/km) Table S1. Vehicular emission standards implementation timetable in the Yangtze River Delta, China. Vehicle State I State II State III State IV State Regions types V Shanghai PC, LDV 1999 2003 2008 2010 2014 BUS, HDT 2001 2005 2008 2013 / MC 2002 2004 2009 / / Nanjing PC, LDV 2000/2001 2004/2006 2008 2011 / BUS, HDT 2001 2005 2008 2013 / MC 2002 2004 2010 / / Hangzhou PC, LDV 2000/2001 2004/2006 2008 2011 / BUS, HDT 2001 2005 2008 2013 / MC 2002 2004 2010 / / Other cities PC, LDV 2000/2001 2004/2006 2008 2012 / BUS, HDT 2001 2005 2008 2015 / MC 2002 2004 2010 / / PC: passenger car, LDV: light-duty vehicle, BUS: bus, HDT: heavy-duty truck, MC: motorcycle. Table S2. The survival rates of -

Study on the Spatial-Temporal Pattern Evolution and Countermeasures of Regional Coordinated Development in Anhui Province, China

Current Urban Studies, 2020, 8, 115-128 https://www.scirp.org/journal/cus ISSN Online: 2328-4919 ISSN Print: 2328-4900 Study on the Spatial-Temporal Pattern Evolution and Countermeasures of Regional Coordinated Development in Anhui Province, China Yizhen Zhang1,2*, Weidong Cao1,2, Kun Zhang3 1School of Geography and Tourism, Anhui Normal University, Wuhu, China 2Urban and Regional Planning Research Center of Anhui Normal University, Wuhu, China 3College of Tourism, Huaqiao University, Quanzhou, China How to cite this paper: Zhang, Y. Z., Cao, Abstract W. D., & Zhang, K. (2020). Study on the Spatial-Temporal Pattern Evolution and Regional coordinated development was an important measure to resolve new Countermeasures of Regional Coordinated contradictions in the new era, and it has gradually become a hotspot in geog- Development in Anhui Province, China. raphy research. At three time points of 2010, 2013, and 2017, by constructing Current Urban Studies, 8, 115-128. an evaluation index system for the city comprehensive competitiveness, the https://doi.org/10.4236/cus.2020.81005 entropy method and the coupling coordination model were used to study the Received: March 2, 2020 coordinated development pattern of cities in Anhui Province. Moreover, we Accepted: March 27, 2020 tried to raise the issue of regional coordinated development in Anhui Prov- Published: March 30, 2020 ince and corresponding countermeasures. The results showed that the com- Copyright © 2020 by author(s) and prehensive competitiveness of cities in Anhui Province has strong spatio- Scientific Research Publishing Inc. temporal heterogeneity. The spatial development pattern with Hefei as the This work is licensed under the Creative core was more obvious. -

Quantitative Analysis of Burden of Infectious Diarrhea Associated with Floods in Northwest of Anhui Province, China: a Mixed Method Evaluation

Quantitative Analysis of Burden of Infectious Diarrhea Associated with Floods in Northwest of Anhui Province, China: A Mixed Method Evaluation Guoyong Ding1, Ying Zhang2, Lu Gao1, Wei Ma1, Xiujun Li1, Jing Liu1, Qiyong Liu3, Baofa Jiang1* 1 Department of Epidemiology and Health Statistics, School of Public Health, Shandong University, Jinan City, Shandong Province, P.R. China, 2 School of Public Health, China Studies Centre, The University of Sydney, New South Wales, Australia, 3 National Institute for Communicable Disease Control and Prevention, China CDC, Beijing City, P.R. China Abstract Background: Persistent and heavy rainfall in the upper and middle Huaihe River of China brought about severe floods during the end of June and July 2007. However, there has been no assessment on the association between the floods and infectious diarrhea. This study aimed to quantify the impact of the floods in 2007 on the burden of disease due to infectious diarrhea in northwest of Anhui Province. Methods: A time-stratified case-crossover analysis was firstly conducted to examine the relationship between daily cases of infectious diarrhea and the 2007 floods in Fuyang and Bozhou of Anhui Province. Odds ratios (ORs) of the flood risk were quantified by conditional logistic regression. The years lived with disability (YLDs) of infectious diarrhea attributable to floods were then estimated based on the WHO framework of the calculating potential impact fraction in the Burden of Disease study. Results: A total of 197 infectious diarrheas were notified during the exposure and control periods in the two study areas. The strongest effect was shown with a 2-day lag in Fuyang and a 5-day lag in Bozhou.