Dexus (ASX: DXS) ASX Release

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

2021 Annual Report Dexus Releases Its 2021 Annual Report, Which Will Be Mailed to Security Holders Who Have Elected to Receive a Hard Copy in Mid-September 2021

Dexus (ASX: DXS) ASX release 17 August 2021 2021 Annual Report Dexus releases its 2021 Annual Report, which will be mailed to Security holders who have elected to receive a hard copy in mid-September 2021. Authorised by the Board of Dexus Funds Management Limited For further information please contact: Investors Media Rowena Causley Louise Murray Senior Manager, Investor Relations Senior Manager, Corporate Communications +61 2 9017 1390 +61 2 9017 1446 +61 416 122 383 +61 403 260 754 [email protected] [email protected] About Dexus Dexus (ASX: DXS) is one of Australia’s leading fully integrated real estate groups, managing a high-quality Australian property portfolio valued at $42.5 billion. We believe that the strength and quality of our relationships will always be central to our success and are deeply committed to working with our customers to provide spaces that engage and inspire. We invest only in Australia, and directly own $17.5 billion of office, industrial and healthcare properties, and investments. We manage a further $25.0 billion of office, retail, industrial and healthcare properties for third party clients. The group’s $14.6 billion development pipeline provides the opportunity to grow both portfolios and enhance future returns. Sustainability is integrated across our business, and our sustainability approach is the lens we use to manage emerging ESG risks and opportunities for all our stakeholders. Dexus is a Top 50 entity by market capitalisation listed on the Australian Securities Exchange and is supported by more than 30,000 investors from 23 countries. With over 35 years of expertise in property investment, funds management, asset management and development, we have a proven track record in capital and risk management and delivering superior risk-adjusted returns for investors. -

Discover All Participating American Express Delicious. Month Out

Discover all participating American Express delicious. Month Out 1 MARCH - 31 MARCH 2020 locations in the Sydney CBD. 1014 TEN FOURTEEN 12 MICRON 1821 HOTEL 360 BAR & DINING 710-722 GEORGE STREET 100 BARANGAROO AVENUE 122 PITT STREET 100 MARKET STREET HAYMARKET 2000 SYDNEY 2000 SYDNEY 2000 SYDNEY 2000 6 HEAD 1788 60 BUVETTE 678 KOREAN BBQ 89 SANDWICHES SHOP 10-11 60 MARTIN PLACE SHOP 34 NUMBER ONE DIXON SHOP F16 HUNTER CONNECTION CAMPBELL’S STORES SYDNEY 2000 1 DIXON STREET 7-13 HUNTER STREET THE ROCKS 2000 HAYMARKET 2000 SYDNEY 2000 A LA TURKO ABB AIR 1982 ADRIA BAR & GRILL ALBERTO’S LOUNGE LEVEL 2 WESTFIELD SYDNEY LEVEL 9 WORLD SQUARE GROUND LEVEL COCKLE BAY 17 ALBERTA STREET 450 GEORGE STREET 644 GEORGE ST WHARF SYDNEY 2000 SYDNEY 2000 SYDNEY 2000 201B SUSSEX ST SYDNEY 2000 ALEXANDER’S PATISSERIE ALFREDO ALL HANDS BREWING HOUSE ALPHA RESTAURANT LEVEL 6 MLC CENTRE 16 BULLETIN PLACE 22 THE PROMENADE 238 CASTLEREAGH STREET 19 MARTIN PLACE SYDNEY 2000 KING STREET WHARF SYDNEY 2000 SYDNEY 2000 SYDNEY 2000 ALSALAM ANASON ANGEL ANJAPPAR TOWN HALL SQUARE 79 LIVERPOOL STREET SHOP 5 125 PITT STREET 580 GEORGE STREET SYDNEY 2000 23 BARANGAROO AVENUE SYDNEY 2000 SYDNEY 2000 BARANGAROO 2000 APPETITIO PIZZA PASTA BAR ARIA RESTAURANT ARISUN ARISUN CHINATOWN 100 GEORGE STREET 1 MACQUARIE STREET 99 LIVERPOOL STREET SHOP 35 NUMBER ONE DIXON THE ROCKS 2000 SYDNEY 2000 SYDNEY 2000 1 DIXON STREET HAYMARKET 2000 ASH ST CELLAR ASSAMM ASSEMBLY BAR AT BANGKOK RESTAURANT 300 GEORGE STREET LEVEL LG QVB LEVEL 9 REGENT PLACE SHOP G11 CAPITOL SQUARE SYDNEY 2000 -

Political Party Return for 2018-19

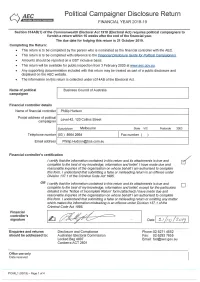

Political Party Disclosure Return FINANCIAL YEAR 2018-19 Section 314AB(1) of the Commonwealth Electoral Act 1918 (Electoral Act) requires political parties to furnish a return within 16 weeks after the end of the financial year. The due date for lodging this return is 21 October 2019. Completing the return: • This return is to be completed by the person who is appointed as the party’s agent with the AEC. • This return is to be completed with reference to the Financial Disclosure Guide for Political Parties. • Amounts should be reported on a GST inclusive basis. • This return will be available for public inspection from Monday 03 February 2020 at www.aec.gov.au. • Any supporting documentation included with this return may be treated as part of a public disclosure and displayed on the AEC website. • The information on this return is collected under s314AB of the Electoral Act. Name of political party Australian Labor Party (ALP) Party agent details Name of party agent Mr Paul Erickson Postal address of party agent 5/9 Sydney Avenue Suburb/town BARTON State ACT Postcode 2600 Telephone number 0261200800 Fax number Email address [email protected] Party agent’s certification I certify that the information contained in this return and its attachments is true and þ complete to the best of my knowledge, information and belief. I have made due and reasonable inquiries of the political party on whose behalf I am agent for the purposes of Part XX of the Electoral Act. I understand that submitting a false or misleading return is an offence under Division 137.1 of the Criminal Code Act 1995. -

Participating Law Firms

Participating Law Firms Contact List for the Summer Clerkship and Graduate Employment Program As at April 2010 ALLEN & OVERY DX: Level 7 Gold Fields House FAX: 02 9373 7710 1 Alfred St Phone: 02 9373 7711 Sydney NSW 2000 Email: [email protected] CONTACT: Sarah Harris SUMMER CLERKSHIP PROGRAM ONLY Submit applications online via www.allenovery.com/careers ATTORNEY GENERAL’S DEPARTMENT – NSW DX: 1227 Sydney Level 14 Swire House FAX: 02 8061 9370 10 Spring Street Phone: 02 8061 9240 Sydney NSW 2000 Email: [email protected] CONTACT: Veronica Chan SUMMER CLERKSHIP PROGRAM ONLY Hard copy of Law Employment Application Form to be sent directly to the firm Further information is available from the website: www.lawlink.nsw.gov.au/lpd AUSTRALIAN GOVERNMENT SOLICITOR (CANBERRA) 50 Blackall Street BARTON ACT 2600 FAX: 02 6253 7303 Phone: 02 6253 7152 Email: [email protected] CONTACT: Ms. Toni Magi (Senior Human Resources Advisor) SUMMER CLERKSHIP PROGRAM and GRADUATE EMPLOYMENT PROGRAM PLEASE NOTE: DO NOT USE NORMAL APPLICATION FORM Application Form available from the website: www.ags.gov.au Special AGS application form to be sent directly to AGS BAKER & McKENZIE DX: 218 Sydney Level 27, AMP Centre FAX: 02 9225 1595 50 Bridge Street Phone: 02 8922 0200 (Katie Evans) Sydney NSW 2000 02 8922 5708 (Vanessa Harris) Email: [email protected] Vanessa. [email protected] CONTACT: Ms. Kate Evans (HR Consultant) Ms. Vanessa Harris ( Organisational Development Manager) SUMMER CLERKSHIP PROGRAM ONLY Submit applications online via www.cvmail.com.au BLAKE DAWSON DX: 355 Sydney 35 Grosvenor Place FAX: 02 9258 6999 225 George Street Phone: 02 9258 5728 SYDNEY NSW 2000 02 9258 6924 E-mail: [email protected] Courier to: Level 35 Grosvenor Place 225 George Street Sydney NSW 2000 CONTACT: Ms. -

DEXUS Property Group (ASX: DXS) ASX Release

DEXUS Property Group (ASX: DXS) ASX release 29 February 2016 31 December 2015 distribution DEXUS Property Group (DEXUS) advises that the distribution for the six months ended 31 December 2015 will be paid to Security holders today. DEXUS provides a copy of the letter to be sent to Security holders and the 2016 Half Year Review. For further information please contact: Investor relations Media relations Rowena Causley T: +61 2 9017 1390 Louise Murray T: +61 2 9017 1446 M: +61 416 122 383 M:+61 403 260 754 E: [email protected] E: [email protected] About DEXUS DEXUS Property Group is one of Australia’s leading real estate groups, investing directly in high quality Australian office and industrial properties. With $21.1 billion of assets under management, the Group also actively manages office, industrial and retail properties located in key Australian markets on behalf of third party capital partners. The Group manages an office portfolio of 1.8 million square metres located predominantly across Sydney, Melbourne, Brisbane and Perth and is the largest owner of office buildings in the Sydney CBD, Australia’s largest office market. DEXUS is a Top 50 entity by market capitalisation listed on the Australian Securities Exchange under the stock market trading code ‘DXS’ and is supported by more than 32,000 investors from 20 countries. With more than 30 years of expertise in property investment, development and asset management, the Group has a proven track record in capital and risk management, providing service excellence to tenants and delivering superior risk-adjusted returns for its investors. -

Original Return

Account Name Address 1: Street 1 Address 1: Street 2 Address 1: Street 3 Address 1: City AddressAddress 1: State/ProvinceAmount 1: ZIP/Postal Received CodeOther Receipts A.T. Kearney Australia Pty Ltd Level 5, MCA Building 140 George Street THE ROCKS NSW 2000 93500 Other Receipt Accenture Australia and New Zealand International House 3 Sussex Street BARANGAROO NSW 2000 93500 Other Receipt Adamantem Capital Level 27, Chifley Tower 2 Chifley Square SYDNEY NSW 2000 93500 Other Receipt AGL Energy Limited Locked Bag 1837 ST LEONARDS NSW 2065 93500 Other Receipt AIA Australia 509 St Kilda Road MELBOURNE VIC 3004 93500 Other Receipt Alcoa of Australia Limited PO Box 252 APPLECROSS WA 6953 93500 Other Receipt Allens Level 37, 101 Collins Street MELBOURNE VIC 3000 93500 Other Receipt Alumina Limited GPO Box 5411 MELBOURNE VIC 3001 93500 Other Receipt Amcor Limited 77 Berkeley Street HAWTHORN VIC 3122 93500 Other Receipt AMP Services GPO Box 4134 SYDNEY NSW 2001 93500 Other Receipt ANZ GPO Box 537E MELBOURNE VIC 3001 93500 Other Receipt Aon Level 33, 201 Kent Street SYDNEY NSW 2000 93500 Other Receipt APA Group PO Box R41 ROYAL EXCHANGE NSW 1225 93500 Other Receipt Ashurst GPO Box 9938 SYDNEY NSW 2001 93500 Other Receipt ATCO Australia Level 12, 2 Mill Street PERTH WA 6000 42854.16 Other Receipt Ausgrid Level 19, 24 Campbell Street HAYMARKET NSW 2000 93500 Other Receipt Australian Foundation Investment Company Level 21, 101 Collins Street MELBOURNE VIC 3000 93500 Other Receipt Australian Securities Exchange Level 6, 20 Bridge Street SYDNEY NSW 2000 -

Commercial Profile 2020

COMMERCIAL PROFILE 2020 COMMERICAL PROFILE Recently completed commercial Upcoming projects 2020 projects ( 2020) Brookfield Properties 32 Carrington St. Sydney 2000 Our Commercial Projects division consists of a large team of experienced fixing tilers & trades people that assure an excellent 7 level building refurbishment service for a wide variety of projects. We have over 22 years of experience in the industry. Our tilers are qualified to lay a District Dining wide range of tiles including porcelain, ceramics, mosaics, natural stone, stone panels, claddings, mechanically fixed stone, Parramatta Square – Parramatta 2150 Zurich Workplace concrete and stone polishing. Ceramic tiling, natural stone & waterproofing application 118 Mount St. Sydney 2000 to commercial kitchen & restaurant dining floor & walls Waterproofing, ceramic tiling, acoustic underlay & natural We understand that there are a number of factors that go towards achieving the complete commercial stone installation refurbishment package from tender stage to final handover. We believe our exceptional service can Hyatt Regency Heinemann Duty Free ensure the highest level of quality of work is presented. Our team can tender all documentation to all 162 Sussex St. Sydney 2000 Sydney International Airport Mascot NSW 2020 factors of satisfaction at any professional level. Floor tiling & acoustic underlay installed in 487 rooms as part of hotel refurbishment Natural stone & ceramic tiling to general floor area AEMC (Australian Energy Market Commission) L15 – 60 Castlereagh St. Sydney -

SECURITY HOLDER REVIEW Welcome to DEXUS Property Group’S 2010 Security Holder Review

2010 DEXUS Property Group SECURITY HOLDER REVIEW WELCOME TO DEXUS PROpeRTY GROup’S 2010 SECURITY HOLdeR ReVIew This Security Holder Review forms part of DEXUS Property Group’s (ASX: DXS) annual reporting suite which is explained in more detail on the inside back cover. All amounts are A$ unless otherwise specified. Cover: Governor Phillip & Macquarie Tower Complex, 1 Farrer Place and 1 Bligh Street, Sydney, NSW This page: Governor Phillip & Macquarie Tower Complex, 1 Farrer Place, Sydney, NSW OUR VISION To be the market leading owner, manager, developer of superior quality properties, in office and industrial in Australia and industrial in the US west coast, providing world‑class property solutions and optimal outcomes for our stakeholders. OuR VISION 1 ThIRD PARTY PROPERTY Funds MANAgeMenT 28 OuR STRATegy – 2010 OBJECTIVes 2 CORPORATE RESPONSIBILITY AND 30 And ACHIEVEMenTS SUSTAINABILITY HIGHLIGHTS ABOUT DEXUS 4 OUR STAKEHOLDERS 32 OUR PEOPLE 34 OuR PORTFOLIO 6 OUR ENVIRONMENT 40 FINANCIAL HIghLIghTS 8 FINANCIAL SUMMARY 44 LeTTER FROM The ChAIR 10 InVesTOR InfORMATION 46 ChIef ExeCUTIVE OffICER’S RepORT 11 GLOSSARY 51 PORTFOLIO PERFORMANCE DIRECTORY 52 Office 16 Industrial – Australia 20 RepORTIng STRUCTURE Industrial – UNITED STATES 24 Industrial – Europe 27 OUR STRATEGY 2010 OBJECTIVes And ACHIEVEMENTS OWN WORLD-CLASS QUALITY PORTFOLIO STRATEGIC LOCATIONS IN AUSTRALIA AND THE US MARKET LEADER IN OFFICE AND INDUSTRIAL FINANCIAL STRENGTH ACTIVE CAPITAL MANAGEMENT 2010 objectives n Continued focus on high quality Australian office assets -

Commercial Monitor June 2016

City of Sydney Town Hall House Commercial Monitor 456 Kent Street Sydney NSW 2000 June 2016 0 / City of Sydney Commercial Monitor June 2016 Commercial Monitor The City of Sydney Commercial Development Monitor provides up to date information on commercial development in the City of Sydney Local Government Area (LGA). It complements the City Residential Monitor which covers the residential market in ten village areas of the City. The village areas are: • CBD and Harbour; • Chinatown and CBD South; • Crown and Baptist Streets; • Glebe Point Road; • Green Square and City South; • Harris Street; • King Street; • Macleay Street and Woolloomooloo; • Oxford Street; and • Redfern Street. The commercial monitor reports on two separate geographies: (1) the combined village areas of CBD & Harbour and Chinatown & CBD South (2) the remaining eight village areas combined. Information on commercial projects is mapped, tabulated, graphed and described based on the status of developments at the end of the reporting period. Developments are grouped by the following categories: • Completed – commercial developments that have completed construction within five years of the report date. • Commenced – commercial developments that are currently under construction but have yet to be completed at the report date. • Approved – commercial developments that have been approved by relevant authorities but have yet to commence at the report date. • Lodged – commercial developments that have been submitted for approval but have not yet been approved by the relevant authority at the report date. Trends in approvals, completions, office vacancies and absorption of office space are also provided. 1 / City of Sydney Commercial Monitor June 2016 Commercial Floor Space Trends Approximately 238,992m² of commercial floor space was completed across the LGA over the past twelve months. -

Participating Law Firms

Participating Law Firms Contact List for the Summer Clerkship and Graduate Employment Program As at June 2010 ALLENS ARTHUR ROBINSON DX: Deutsche Bank Place FAX: 02 9373 5333 Cnr Hunter & Phillip St Phone: 02 9373 4735 Sydney NSW 2000 Email: [email protected] CONTACT: Claire Bourke (Graduate Resourcing Consultant) SUMMER CLERKSHIP PROGRAM ONLY Submit applications online via www.aar.com.au/careers ALLEN & OVERY DX: Level 7 Gold Fields House FAX: 02 9373 7710 1 Alfred St Phone: 02 9373 7711 Sydney NSW 2000 Email: [email protected] CONTACT: Sarah Harris SUMMER CLERKSHIP PROGRAM ONLY Submit applications online via www.allenovery.com/careers ATTORNEY GENERAL’S DEPARTMENT – NSW DX: 1227 Sydney Level 14 Swire House FAX: 02 8061 9370 10 Spring Street Phone: 02 8061 9240 Sydney NSW 2000 Email: [email protected] CONTACT: Veronica Chan SUMMER CLERKSHIP PROGRAM ONLY Hard copy of Law Employment Application Form to be sent directly to the firm Further information is available from the website: www.lawlink.nsw.gov.au/lpd AUSTRALIAN GOVERNMENT SOLICITOR (CANBERRA) 50 Blackall Street BARTON ACT 2600 FAX: 02 6253 7303 Phone: 02 6253 7152 Email: [email protected] CONTACT: Ms. Toni Magi (Senior Human Resources Advisor) SUMMER CLERKSHIP PROGRAM and GRADUATE EMPLOYMENT PROGRAM PLEASE NOTE: DO NOT USE NORMAL APPLICATION FORM Application Form available from the website: www.ags.gov.au Special AGS application form to be sent directly to AGS BAKER & McKENZIE DX: 218 Sydney Level 27, AMP Centre FAX: 02 9225 1595 50 Bridge Street Phone: 02 8922 0200 (Katie Evans) Sydney NSW 2000 02 8922 5708 (Vanessa Harris) Email: [email protected] Vanessa. -

019/98 1998 Election of Clearing Member Director

30 - 32 Grosvenor Street Sydney NSW 2000 Australia Telephone (02) 9256 0555 Facsimile (02) 9256 0426 To: Clearing Members 19/98 No: 1998 Election of Clearing Member Director on SFECH Board As Clearing Members will be aware, two of the positions on the Board of the Sydney Futures Exchange Clearing House Board are held by elected representatives of Clearing Members. These Directors hold office for two years and retire by rotation in alternate years. They are eligible to stand for re-election, but the incumbent director has decided not to stand again this year. Accordingly nominations are now sought for this position. Persons wishing to stand for election must be a Director, Partner or Employee of a Clearing Member. They must be nominated by one Clearing Member and seconded by another Clearing Member. A list of Clearing Members together with a nomination form is attached. The nomination form must be signed by the candidate as well as his/her employer and the nominator and seconder. Candidates may provide information in support of their nomination for inclusion with the ballot papers if they wish. The information provided should not exceed two A4 size pages in length. The nominations, with original signatures together with any supporting information, should be forwarded to reach the Secretary of SFECH no later than close of business on Thursday, 9 April 1998. Ballot papers will be forwarded to all Clearing Members and these must then be returned to the Secretary of by 5.00 pm on Wednesday, 29 April 1998. SYDNEY FUTURES EXCHANGE CLEARING HOUSE PTY LIMITED 1998 ELECTION OF DIRECTORS NOMINATION OF CLEARING MEMBER CANDIDATE DIRECTOR I................................................................................................................................................. -

VCLP Partnership List

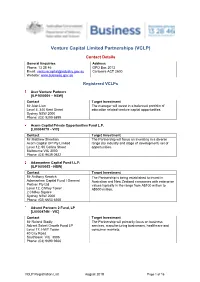

Venture Capital Limited Partnerships (VCLP) Contact Details General Enquiries Address Phone: 13 28 46 GPO Box 2013 Email: [email protected] Canberra ACT 2600 Website: www.business.gov.au Registered VCLPs Acer Venture Partners [ILP1600005 – NSW] Contact Target Investment Mr Alan Liao The manager will invest in a balanced portfolio of Level 4, 346 Kent Street education related venture capital opportunities. Sydney NSW 2000 Phone: (02) 9299 6899 Acorn Capital Private Opportunities Fund L.P. [L0000407X - VIC] Contact Target Investment Mr Matthew Sheehan The Partnership will focus on investing in a diverse Acorn Capital GP Pty Limited range (by industry and stage of development) set of Level 12, 90 Collins Street opportunities. Melbourne VIC 3000 Phone: (03) 9639 0522 Adamantem Capital Fund I.L.P. [ILP1600053 - NSW] Contact Target Investment Mr Anthony Kerwick The Partnership is being established to invest in Adamantem Capital Fund I General Australian and New Zealand companies with enterprise Partner Pty Ltd values typically in the range from A$100 million to Level 12, Chifley Tower A$500 million. 2 Chifley Square Sydney NSW 2000 Phone: (02) 6653 6508 Advent Partners 2 Fund, LP [L0000474N - VIC] Contact Target Investment Mr Roland Stadly The Partnership will primarily focus on business Advent Select Growth Fund LP services, manufacturing businesses, healthcare and Level 17, HWT Tower consumer markets. 40 City Road Southbank VIC 3006 Phone: (03) 9690 9566 VCLP Registration List August 2018 Page 1 of 16 Allegro Funds II, LP [ILP0000073 - NSW] Contact Target Investment Ms Jennifer Cheung The manager is seeking to make private equity Allegro Funds II, General Partner LP investments in mid-market businesses in Australia and Level 1, Plaza Building New Zealand experiencing financial, operational or 95 Pitt Street market-related dislocation with enterprise values of up Sydney NSW 2000 to $100 million.