Malaysia Real Estate Highlights

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

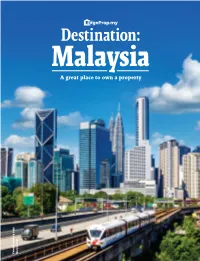

Destination: Malaysia a Great Place to Own a Property Complimentary Copy

Destination: Malaysia A great place to own a property Complimentary copy. Complimentary copy. for sale. Not Destination: Malaysia Contents Chapter 1 Chapter 2 Chapter 4 Why choose Malaysia? 4 A fertile land for 17 What to do before 42 economic growth you buy? More bang for your buck 5 Ease of property purchase 7 Chapter 5 Tropical weather and 8 Malaysia My Second Home 44 disaster-free land Low cost of living, 9 Chapter 6 high quality of life Thrilling treats & tracks 48 Easy to adapt and fit in 10 Must-try foods 51 Safe country 11 Must-visit places 55 Fascinating culture 12 Chapter 3 and delicious food Where to look? 22 Quality education 13 KL city centre: 24 Quality healthcare 14 Where the action is services Damansara Heights: 26 The Beverly Hills of Malaysia Cyberjaya: Model 30 smart city Useful contact numbers 58 Desa ParkCity: KL’s 32 to have in Malaysia most liveable community Mont’Kiara: Expats’ darling 34 Advertorial Johor Bahru: A residential 37 Maker of sustainable 20 hot spot next to Singapore cities — Sunway Property Penang Island: Pearl 40 The epitome of luxury 28 of the East at DC residensi A beach Destination: on one of the many pristine Malaysia islands of Sabah, Malaysia. PUBLISHED IN JUNE 26, 2020 BY The Edge Property Sdn Bhd (1091814-P) Level 3, Menara KLK, No 1 Jalan PJU 7/6, Mutiara Damansara, 47810 Petaling Jaya, Selangor, Malaysia MANAGING DIRECTOR/ EDITOR-IN-CHIEF — Au Foong Yee EDITORIAL — Contributing Editor Sharon Kam Assistant Editor Tan Ai Leng Preface Copy Editors James Chong, Arion Yeow Writers lessed with natural property is located ranging Chin Wai Lun, Rachel Chew, beauty, a multi-cul- from as low as RM350,000 for any Natalie Khoo, Chelsey Poh tural society, hardly residential property in Sarawak Photographers any natural disas- to almost RM2 million for a landed Low Yen Yeing, Suhaimi Yusuf, ters and relatively home on Penang Island. -

Real Estate Highlights Kuala Lumpur - Penang - Johor Bahru • 1St Half 2008

Research Real Estate Highlights Kuala Lumpur - Penang - Johor Bahru • 1st Half 2008 Contents Kuala Lumpur Hotel • Condominium Market 2 • Office Market 5 • Retail Market 8 • Hotel Market 10 Penang Property Market 12 Retail Johor Bahru Property Market 14 Residential Office Executive Summary Kuala Lumpur • The high end condominium market stabilised in the first half of 2008 in terms of take up, capital values and rentals. • Rentals and occupancies of prime offices continued to rise due to the current tight supply of good quality office buildings. • Several retail centres located at fringes of KL City are undergoing refurbishment works to remain competitive. • The performance of the hotel industry had been resilient attributed to high tourist arrivals and receipts, which led to the increase in average room rates and occupancies. Penang • Most of the high end condominium projects which are nearing completion have been sold, with prices being revised upwards. • The retail industry performed well with higher tourist arrivals in Penang. • The asking rentals of newly completed offices with better IT facilities are ranging from RM2.50 to RM3.50 per sq ft per month. Johor • The high end residential market is gaining momentum with the positive development of Iskandar Malaysia. • Prime retail centres continued to enjoy growth in rentals and occupancies. • Office sector remains healthy at an average occupancy of 70%. 2 Real Estate Highlights - Kuala Lumpur | Penang | Johor Bahru • 1st Half 2008 Knight Frank Figure 1 Projection of Cumulative Supply Kuala Lumpur High End Condominium Market for High End Condominium (2008 - 2010) Market Indications 30,000 The high end condominium market generally stabilised during the first six months of the year with one 25,000 notable new project, The Regent Residences (across Twin Towers), recording prices in excess of RM2,500 per sq ft. -

1 BAB I PENDAHULUAN 1.1 Latar Belakang Seiring Dengan

BAB I PENDAHULUAN 1.1 Latar Belakang Seiring dengan perkembangan jaman dan teknologi, sikap dan perilaku masyarakat dalam mempergunakan waktu luangnya sangat bervariasi, banyak dari mereka menghabiskan waktunya berada di pusat – pusat hiburan seperti di mall, kafe,restoran dan pusat kebugaran . Dalam dunia hiburan , lifestyle menjadi semakin penting dan digemari di kalangan masyarakat, terutama diantaranya adalah kelompok remaja. Kelompok ini merasa harus selalu mengikuti tren yang ada. Maka dari itu dengan perkembangan gaya hidup, kelompok masyarakat ini memiliki kegemaran untuk selalu membeli barang atau jasa sesuai dengan merek yang sedang booming. Salah satu contoh dari lifestyle yang sedang booming sekarang ini yaitu hadirnya suatu Fitness center . Kebutuhan terhadap pusat kebugaran (Fitness center) saat ini bukan sekedar untuk berolahraga saja (fit) tetapi lebih dari itu, yakni mencari Fit & Fun. Hal ini telah menjadi bagian dari gaya hidup yang dapat mencerminkan identitas masing – masing individu. Mereka biasanya tidak hanya melakukan latihan (exercise) fisik, namun juga menyegarkan mata dan perasaannya. Contohnya melalui hiburan musik, kafe, dan shopping dengan teman. Tak mengherankan, belakangan di sejumlah pusat belanja kelas atas di Jakarta bermunculan pusat kebugaran berjaringan Internasional yang mencoba memadukan aktivitas kebugaran dengan hiburan. Pada tahun 2004, Celebrity Fitness membuka pusat kebugaran yang memadukan urusan olah tubuh dengan hiburan musik dan film di Plaza Indonesia Entertainment Center (EX), Jakarta -

Media Release Events & Happenings Go Shopping and Enjoy!

MEDIA RELEASE EVENTS & HAPPENINGS GO SHOPPING AND ENJOY! 1MALAYSIA YEAR END SALE 2015 (14 NOVEMBER 2015 – 3 JANUARY 2016) It’s the year-end school holidays and festive season. A time to take a break, celebrate, chill out, dine and SHOP! Yes, shop, and now say 1MYES for 1Malaysia Year End Sale. It’s the biggest sale bonanza of the year with BIG bargains, BIG offers and BIG rewards at shopping outlets nationwide for nearly two months. That’s not all. Expect special deals and price cuts during back-to-school sales, which will bring huge relief to moms and dads. Bring the whole family and enjoy a fun day of outing. There are also special rewards for tourists, such as tourist privilege cards, tax-free shopping, gift redemptions with purchases and GST refund at exit points. A long line-up of events and activities awaits everyone. It will be a fun time for all. Contests, promotions, prize galore, songs and dances, art and crafts, Christmas shopping, meet and greet Santa, New Year’s Eve party and much more will build up the momentum before curtains call to say goodbye to 2015, and hello 2016! Don’t miss out on the fun. In fact 1MYES extends right into the New Year. Check out 1MYES special offers, events and happenings throughout the country. PENANG 1st Avenue Year End Sale Shop & Win Shopper Rewards (14 Nov 2015 to 3 Jan 2016) – Stand a chance to win exclusive holiday packages from Royal Caribbean cruise for 2 with same-day purchases of RM100 & above in a single receipt. -

Kuala Lumpur, Melaka & Penang

Plan Your Trip 12 ©Lonely Planet Publications Pty Ltd Kuala Lumpur, Melaka & Penang “All you’ve got to do is decide to go and the hardest part is over. So go!” TONY WHEELER, COFOUNDER – LONELY PLANET THIS EDITION WRITTEN AND RESEARCHED BY Simon Richmond, Isabel Albiston Contents PlanPlan Your Your Trip Trip page 1 4 Welcome to Top Itineraries ...............16 Eating ............................25 Kuala Lumpur ................. 4 If You Like... ....................18 Drinking & Nightlife.... 31 Kuala Lumpur’s Top 10 ...6 Month By Month ........... 20 Entertainment ............ 34 What’s New ....................13 With Kids ....................... 22 Shopping ...................... 36 Need to Know ................14 Like a Local ................... 24 Explore Kuala Lumpur 40 Neighbourhoods Masjid India, Day Trips from at a Glance ................... 42 Kampung Baru & Kuala Lumpur ............. 112 Northern KL .................. 83 Bukit Bintang Sleeping ......................124 & KLCC .......................... 44 Lake Gardens, Brickfields & Bangsar .. 92 Melaka City.................133 Chinatown, Merdeka Square & Bukit Nanas ...67 Penang .........................155 Understand Kuala Lumpur 185 Kuala Lumpur Life in Kuala Lumpur ...197 Arts & Architecture .... 207 Today ........................... 186 Multiculturalism, Environment ................212 History ......................... 188 Religion & Culture ......200 Survival Guide 217 Transport .....................218 Directory A–Z ............. 222 Language ....................229 Kuala -

M.V. Solita's Passage Notes

M.V. SOLITA’S PASSAGE NOTES SABAH BORNEO, MALAYSIA Updated August 2014 1 CONTENTS General comments Visas 4 Access to overseas funds 4 Phone and Internet 4 Weather 5 Navigation 5 Geographical Observations 6 Flags 10 Town information Kota Kinabalu 11 Sandakan 22 Tawau 25 Kudat 27 Labuan 31 Sabah Rivers Kinabatangan 34 Klias 37 Tadian 39 Pura Pura 40 Maraup 41 Anchorages 42 2 Sabah is one of the 13 Malaysian states and with Sarawak, lies on the northern side of the island of Borneo, between the Sulu and South China Seas. Sabah and Sarawak cover the northern coast of the island. The lower two‐thirds of Borneo is Kalimantan, which belongs to Indonesia. The area has a fascinating history, and probably because it is on one of the main trade routes through South East Asia, Borneo has had many masters. Sabah and Sarawak were incorporated into the Federation of Malaysia in 1963 and Malaysia is now regarded a safe and orderly Islamic country. Sabah has a diverse ethnic population of just over 3 million people with 32 recognised ethnic groups. The largest of these is the Malays (these include the many different cultural groups that originally existed in their own homeland within Sabah), Chinese and “non‐official immigrants” (mainly Filipino and Indonesian). In recent centuries piracy was common here, but it is now generally considered relatively safe for cruising. However, the nearby islands of Southern Philippines have had some problems with militant fundamentalist Muslim groups – there have been riots and violence on Mindanao and the Tawi Tawi Islands and isolated episodes of kidnapping of people from Sabah in the past 10 years or so. -

Senarai Penerima (Fasa 2)

Bil. Nama Syarikat No. Lesen Code Bank Negeri Fasa 1 SPRING TRAVEL SERVICES SDN BHD 2198 35-CIMB Bank Berhad JOHOR 2 2 JE TRAVEL SDN BHD 5357 33-Public Bank Berhad/ Public Finance Berhad JOHOR 2 3 CHENG YUE HOLIDAYS SDN BHD 5429 29-OCBC Bank Berhad JOHOR 2 4 SALSABILA AFLAH TOURS & TRAVEL SDN BHD 7570 27-Malayan Banking Berhad JOHOR 2 5 KW LIM TRAVEL NETWORK SDN BHD 8733 24-Hong Leong Bank Berhad/ Hong Leong Finance JOHOR 2 6 ISMA HOLIDAYS SDN BHD 8310 27-Malayan Banking Berhad JOHOR 2 7 MGM TRAVEL & TOURS SDN BHD 8996 24-Hong Leong Bank Berhad/ Hong Leong Finance JOHOR 2 8 HAPPY EXPRESS TRAVEL SDN BHD 7871 33-Public Bank Berhad/ Public Finance Berhad JOHOR 2 9 HENG TRAVEL & TOURS SDN BHD 9475 33-Public Bank Berhad/ Public Finance Berhad JOHOR 2 10 SITTY TRAVEL SDN BHD 5943 24-Hong Leong Bank Berhad/ Hong Leong Finance JOHOR 2 11 3J TRAVEL & TOURS MANAGEMENT SDN BHD 5104 18-RHB Bank Berhad JOHOR 2 12 TRANSINEX TRAVEL & TOUR (M) SDN BHD 4902 12-Alliance Bank Berhad JOHOR 2 13 HONG LI INTERNATIONAL TRAVEL SDN BHD 9780 33-Public Bank Berhad/ Public Finance Berhad JOHOR 2 14 M99 TRAVEL SDN BHD 8809 33-Public Bank Berhad/ Public Finance Berhad JOHOR 2 15 JACKSTAR HOLIDAYS SDN BHD 10061 27-Malayan Banking Berhad JOHOR 2 16 NUR FIRNAS TRAVEL & TOURS SDN BHD 9903 27-Malayan Banking Berhad JOHOR 2 17 ALWANI ZAFIRAH SERVICES & HOLIDAY 8297 24-Hong Leong Bank Berhad/ Hong Leong Finance JOHOR 2 18 MEGA TOP HOLIDAY & TRANSPORT SDN BHD 4406 27-Malayan Banking Berhad JOHOR 2 19 MEGAWORLD HOLIDAY SDN BHD 6406 35-CIMB Bank Berhad JOHOR 2 20 COLA HOLIDAYS -

Street Food – 11 Bästa Tipsen

PubliceradPublicerad november januari 20172014 KUALA LUMPUR Street food – 11 bästa tipsen ✔ Takbarer ✔ Petronas ✔ Tempel ✔ Nattliv twin towers ✔ Moskéer ✔ Forsränning ✔ Restauranger ✔ Nattmarknad ✔ Golf ✔ Chinatown ✔ Ekoparken 2 KUALA LUMPUR Här frodas kulturer, nattliv och mat uala Lumpur känns ofta som den ut någon annan plats på jorden med samma otippade vinnaren ingen hade räknat kulinariska variationsrikedom och kvalitet vad Kmed. Många ser staden som en gäller vardagsmat som vanligt folk äter. Det praktisk mellanlandning. För mig är staden andra området är shoppingen. Från den mest snarare ett slutmål, en hel värld i sig, en plats överflödiga lyx till fynd som tillhör Asiens allra som alltid är snäppet intressantare än man billigaste. först trodde. Här finns gott om nyheter av vitt skilda slag. I ingen annan stad lyser de stora asiatiska Ta bara det nya vassa konstmuseet Ilham, kulturerna sida vid sida på samma sätt. Fler än flodpromenaden River of Life eller leden med en överraskad besökare bokar om sitt plan för hängbroar genom KL Forest Eco Park som nu kunna stanna kvar här några extra dagar. möjliggör en djungelvandring mitt i stan. Asien strålar samman i Kuala Lumpur. Staden är Huvudstaden i det muslimska Malaysia har en mosaik plats för alla trosinriktningar och tankesätt. De av så många stora grupperna malajer, kineser och indier möjligheter. samsas med varandra som smakerna och Mat, shopping, kryddorna i den inhemska currygrytan Laksa. wellness, Denna ovanligt mångkulturella stad präglas aktiviteter, av en tolerans som fungerar och tycks leda nattliv och vidare. Stämningen är omisskännligt trivsam. kulturupp levelser. Här På två områden sticker Kuala Lumpur känner man ut. -

Priority Dining (Selected Partners Outlets) Listing

Priority Dining (Selected Partners Outlets) listing No. Brand Outlet Locations Start Date End Date 1. W Hotel Kuala Lumpur, No. 121, Jalan Ampang, 1 January 2019 30 June 2019 WOOBAR Kuala Lumpur, 50450 Malaysia 2. W Hotel Kuala Lumpur, No. 121, Jalan Ampang, 1 January 2019 30 June 2019 WET® Deck Kuala Lumpur, 50450 Malaysia 3. W Hotel Kuala Lumpur, No. 121, Jalan Ampang, 1 January 2019 30 June 2019 Yen Kuala Lumpur, 50450 Malaysia 4. W Hotel Kuala Lumpur, No. 121, Jalan Ampang, 1 January 2019 30 June 2019 Flock Kuala Lumpur, 50450 Malaysia 5. Banyan Tree Hotel, Level 59, No.2, Jalan Conlay, 1 January 2019 30 June 2019 Vertigo 50450 Kuala Lumpur, Wilayah Persekutuan, Malaysia 6. Banyan Tree Hotel, Level 53, No.2, Jalan Conlay, 1 January 2019 30 June 2019 Altitude 50450 Kuala Lumpur, Wilayah Persekutuan, Malaysia 7. Banyan Tree Hotel, Lobby, No.2, Jalan Conlay, 1 January 2019 30 June 2019 Bake By Banyan 50450 Kuala Lumpur, Wilayah Persekutuan, Tree Malaysia 8. Four Seasons Hotel Kuala Lumpur, 145, Jalan 1 January 2019 30 June 2019 Yun House Ampang, 50450 Kuala Lumpur, Malaysia 9. The Lounge at Four Seasons Hotel Kuala Lumpur, 145, Jalan 1 January 2019 30 June 2019 Four Seasons Ampang, 50450 Kuala Lumpur, Malaysia 10. Four Seasons Hotel Kuala Lumpur, 145, Jalan 1 January 2019 30 June 2019 Bar Trigona Ampang, 50450 Kuala Lumpur, Malaysia 11. Pool Bar and Four Seasons Hotel Kuala Lumpur, 145, Jalan 1 January 2019 30 June 2019 Grill Ampang, 50450 Kuala Lumpur, Malaysia 12. 163, Fraser Place Kuala Lumpur, 10, Jalan Perak, 1 January 2019 30 June 2019 Skillet at 163 Kuala Lumpur, 50450 Kuala Lumpur, Wilayah Persekutuan Kuala Lumpur, Malaysia Standard Chartered Bank Malaysia Berhad (115793-P) Priority Dining (Selected Partners Outlets) listing May 2019 13. -

Malaysia Real Estate Highlights

RESEARCH REAL ESTATE HIGHLIGHTS 1ST HALF 2016 KUALA LUMPUR PENANG JOHOR BAHRU KOTA KINABALU HIGHLIGHTS KUALA LUMPUR HIGH END CONDOMINIUM MARKET The residential market continues to remain lacklustre with lower volume and value of transactions recorded. ECONOMIC AND MARKET INDICATORS Limited project completions and new Malaysia’s economy expanded at a launches of high end condominiums / slower pace in 2015 with Gross Domestic residences during the review period. Product (GDP) growing at an annual rate of 5.0% (2014: 6.0%). For 2016, the Government has trimmed the country’s Growing pressure on rentals amid GDP growth forecast to 4 - 4.5% due to strong supply pipeline (existing and the volatility in crude oil prices and other new completions) and a challenging economic challenges. GDP continued rental market while prices in to moderate in the first quarter of 2016, the secondary market generally posting 4.2% growth, its slowest since continue to remain resilient. 3Q2009 (4Q2015: 4.5%), driven by domestic demand. Private consumption expanded by 5.3% while private Developers adopt innovative ‘push investment moderated to 2.2%. marketing’ strategies to boost Headline inflation for April 2016 registered at sales of selected projects and 2.1%. It is expected to be lower at 2% to 3% improve revenue. this year, compared to an earlier projection Aria of 2.5% to 3.5% and will continue to remain stable in 2017. (432 units) and The Residences at The Meanwhile, labour market conditions St. Regis Kuala Lumpur (160 units). continued to weaken with more retrenchment of workers, particularly in By the second half of 2016, the scheduled the manufacturing, mining and services completions of another five projects will sectors. -

Malaysia Real Estate Highlights

RESEARCH REAL ESTATE HIGHLIGHTS 1ST HALF 2015 KUALA LUMPUR PENANG JOHOR BAHRU KOTA KINABALU KUALA LUMPUR HIGH END CONDOMINIUM MARKET (MPC) meeting in May in an effort to support economic growth and domestic HIGHLIGHTS consumption. • Softening demand in the SUPPLY & DEMAND high-end condominium With the completion of seven notable segment amid a cautious projects contributing an additional market. 1,296 units [includes projects that are physically completed but pending Madge Mansions issuance of Certificate of Completion • Lower volume of transactions and Compliance (CCC)], the cumulative expected to come on-stream. The KL in 1Q2015. supply of high end condominiums in City locality will account for circa 35% Kuala Lumpur stands at 39,610 units. (1,310 units) of the new supply; followed • Developers with niche high by Mont’ Kiara / Sri Hartamas with Approximately 45% (582 units) of the new 34% (1,256 units); KL Sentral / Pantai / end residential projects in KL completions are located in the Ampang Damansara Heights with 20% (734 units); City review products, pricing Hilir / U-Thant area, followed by some and the remaining 11% (425 units) from and marketing strategies in 26% (335 units) in the locality of KL City; the locality of Ampang Hilir / U-Thant. a challenging market with 16% (204 units) from the locality of KL lacklustre demand, impacted Sentral / Pantai / Damansara Heights Notable projects slated for completion by a general slowdown in the area; and 14% (175 units) from the Mont’ in KL City include Face Platinum Suites, economy, tight lending Kiara / Sri Hartamas locality. Le Nouvel, Mirage Residences as well as guidelines, weaker job market the delayed project of Crest Jalan Sultan The three completions in Ampang Hilir amongst other reasons. -

Precipice 2010 Itinerary Group 1

PRECIPICE 2010 ITINERARY (26th February – 5th March) GROUP 1 www.cms.ac.in 1 SRILANKAN AIRLINES BLR‐CMB‐KUL‐CMB‐BLR Flight Dep Date Route Dep Arr Arr Date 1 UL172G 26FEB BLRCMB 2105 2230 26FEB 2 UL312G 27FEB CMBKUL 0720 1320 27FEB 3 UL316G 05MAR KULCMB 0910 1010 05MAR 4 UL171G 05MAR CMBBLR 1840 2005 05MAR 26 FEB 2010 BANGALORE 1700hrs Report at Bangalore International Airport (Carry an extra pair of clothes, after all, YOU are going to SRILANKA as well.) 2105hrs Depart to Colombo via UL172 2230hrs Arrival at Colombo International Airport 2230hrs Transfer to Hotel 2300hrs Arrival at Hotel 27 FEB 2010 KUALA LUMPUR 0400hrs Transfer to Colombo International Airport 0720hrs Departure from Colombo International Airport.. 1320hrs Arrival at KLIA Complete immigrations and Customs formalities. 1430hrs Depart for Hotel Grand Seasons . Enroute a snack box will be handed over to you . 1530hrs Welcome Reception at Grand Seasons. Check into your rooms. 1730hrs Sight‐seeing and shopping at own leisure. 1930hrs Dinner at Gateway of India Overnight at The Grand Seasons 28 FEB 2010 KUALA LUMPUR/KUALA PERLIS 0730 to 1030hrs Breakfast at Grand Seasons 1030 to 1300 leisure time and check out of hotel . 1330hrs Lunch at Gateway of India, KL 1530hrs City tour of Kuala Lumpur 2000hrs Dinner at the Gateway of India, KL 2200hrs Meet and Transfer to Kuala Perlis 01 MARCH 2010 LANGKAWI 0600hrs Transfer to the Ferry Terminal 0830hrs Arrival at Langkawi Ferry terminal. 0900hrs Breakfast at Palace D’ India. Transfer to the Berjaya Langkawi Resort & Spa. 1230hrs Lunch at The Palace D’ India & British Raj.