Chapter 8: Economic Development

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Official List of Public Waters

Official List of Public Waters New Hampshire Department of Environmental Services Water Division Dam Bureau 29 Hazen Drive PO Box 95 Concord, NH 03302-0095 (603) 271-3406 https://www.des.nh.gov NH Official List of Public Waters Revision Date October 9, 2020 Robert R. Scott, Commissioner Thomas E. O’Donovan, Division Director OFFICIAL LIST OF PUBLIC WATERS Published Pursuant to RSA 271:20 II (effective June 26, 1990) IMPORTANT NOTE: Do not use this list for determining water bodies that are subject to the Comprehensive Shoreland Protection Act (CSPA). The CSPA list is available on the NHDES website. Public waters in New Hampshire are prescribed by common law as great ponds (natural waterbodies of 10 acres or more in size), public rivers and streams, and tidal waters. These common law public waters are held by the State in trust for the people of New Hampshire. The State holds the land underlying great ponds and tidal waters (including tidal rivers) in trust for the people of New Hampshire. Generally, but with some exceptions, private property owners hold title to the land underlying freshwater rivers and streams, and the State has an easement over this land for public purposes. Several New Hampshire statutes further define public waters as including artificial impoundments 10 acres or more in size, solely for the purpose of applying specific statutes. Most artificial impoundments were created by the construction of a dam, but some were created by actions such as dredging or as a result of urbanization (usually due to the effect of road crossings obstructing flow and increased runoff from the surrounding area). -

2. Infrastructure

Lakes Region Comprehensive Economic Development Strategy 2. Infrastructure Infrastructure consists of the facilities and services necessary to support economic resources. Maintaining these services and facilities while planning for future needs, enables communities to direct future growth and development to areas with infrastructure. Community facilities and services protect and promote the health and safety of residents. The region has many locations suitable for expansion of commercial centers, however, services and facilities available vary by town as many are rural and do not have extensive developed infrastructure. Industrial Parks Several towns in the region have established a designated industrial park, listed in Table 2.1. The parks are currently (or have near-term future plans to be) serviced by public sewer and water. Manufacturing, light industry are generally located in these parks, along with some commercial facilities. Map 5 shows the location of each of these parks. Table 2.1: Industrial Parks in the Lakes Region Infrastructure Available* Name Town Water Gas Sewer Rail Highway Freudenburg Northfield U U U U I-93 Ashland Industrial Park Ashland Y N Y Y I-93 Belmont Industrial Park Belmont N N Y N Rt 140/I-93 Gilmanton S&G Industrial Park Gilmanton Y N Y N Rt 106 Nickerson Tilton N Y Y N Rt 132/I-93 Cormier Northfield U U U U I-93 Blouent Steel Northfield U U U U I-93 Pike Industries Northfield U U U U I-93 Franklin Industrial Park Franklin Y Y Y N Rt 3&11 O'Shea Industrial Park Laconia N Y Y N Rt 3 Whitten Industrial Park -

Water Quality Goal Technical Memo

Squam Lakes Watershed Plan Water quality goal technical memo Funding for this project was provided in part by a Watershed Assistance Grant from the NH Department of Environmental Services with Clean Water Act Section 319 funds from the U.S. Environmental Protection Agency. September 2019 Squam Lakes Watershed Plan Water Quality Goal Memo Purpose: This report summarizes the steps taken to determine a water quality goal for Squam Lake and Little Squam Lake for the Squam Lakes Watershed Management Plan. Partners, collaborators, and stakeholders worked together to review existing data and water quality model predictions to determine an in-lake water quality goal. The goal will be used to measure the success of the watershed management plan recommendations. Site Description The Squam Lakes Watershed (Figure 1), located in central New Hampshire, covers 36,644 acres. At the heart of the watershed is Squam Lake (6,762 acres) and Little Squam Lake (408 acres). The watershed is 20% open water. Of the land area, 85% is forested. There is minimal development in the Squam Lakes Watershed and along the shores of the Squam Lakes; less than 3% of the watershed is considered low density development, while high and medium density development are less than 0.1% of the total watershed area. There are 34 tributaries for the Squam River and Lakes. Water flows generally from east to west, from Squam Lake, through the Squam Channel, into Little Squam Lake, and through two miles of the Squam River until the lake impoundment in Ashland. Ultimately, the Squam River drains into the Pemigewasset River in Ashland. -

Merrimack Valley

Aì Im Aì !"`$ ?{ Aù ?x Ij ?¬ ?¬ Im Ai AÔ Aù AÔ ?x ?v !"b$ Ij AÔ AÙ Aä ?¸ !"`$ ?¨ Im AÕ A£ CÚ ?{ ?x A¢ AÖ Ij ?} ?} ?v Il ?} Aõ A¡ ?} Il Ae AÑ ?} AÙ AÑ fg ?¸ ?} ?} Aù Aä !"b$ A¡ !"`$ ?} Ij AÕ A¤ CÓ ?} CÒ Ij ?¸ AÑ ?} ?} C¹ ?{ #V Im Aõ ?¨ AÑ Aý AÙ Ij AÖ fgA B C D AÕ E F G 4 Lake Winnipesaukee d . Merrymeeting Lake Greenough Pond R ALTON BAY STATE FOREST ROLLINS STATE PARK F R A N K L I N 0 K F R A N K L I N B E L M O N T h B E L M O N T e t N 1 9 PAGE STATE FOREST a o . u Sondogardy Pond Aä 8 r r o Crystal Lake 1 th s NNOORRTTHH FFIIEE LLDD N 6 y S O N w a I . R SSAA LLIISS BB UURRYY E GG I O 6 an H r R E t STATE FOREST NURSERY R m Palmer Pond 3 S l i g 4 E S i 3v . K E G e S A K C e L A . N L k 7 n Marsh Pond 3r t 5 1 MEADOW POND STATE FOREST a r . R-11 N Suncook River F R s M o Tucker Pond 1 New Pond MERRIH MACK VALLEY REGION r Chalk Pond 3 r d Stevens Brook AÑ e o 1 t 5 1 h Forest Pond 4 u Lyford Pond . h AYERS STATE FOREST 4 0 Marchs Pond ?§ H e Shellcamp Pond n fg m r S U T T O N B i t n Merrymeeting River S U T T O N g 6 A a d a . -

Page Pond History and Guide

Page Pond and Forest A History and Guide Daniel Heyduk Acknowledgements Thanks are due to the people of Meredith, the Land and Community Heritage Investment Program (LCHIP), the Trust for Public Land, and the Meredith Conservation Commission for the acquisition of the Page Pond and Forest property. Thanks also to John and Nancy Sherman for the donation of a conservation easement on their land, which expands to over 600 acres the total conserved area accessible to the public. The Meredith Conservation Commission supported this project, reviewed drafts and gave guidance. John Moulton and John Sherman helped with information and suggestions. The Trust for Public Land shared maps. Richard Boisvert of the New Hampshire Division of Historical Resources contributed photos and described his excavation on Stonedam Island. Ralph Pisapia contributed photos. Paula Wanzer proofread the text. Peter Miller provided his research on Dudley Leavitt and the Page Brook sawmill. Vikki Fogg of the Meredith Town Assessing Department showed me historic tax records. Steve Taylor gave information on sheep. The Meredith Historical Society provided access to old maps. Rick Van de Poll identified natural communities. The Peabody Museum and Mount Kearsarge Indian Museum were very helpful. Dedication: to Harold Wyatt, who energetically researched Meredith history. Daniel Heyduk, Ph.D., resides in Meredith with his wife Beverly. An anthropologist and historian, he is a member of the Meredith Conservation Commission and a Forest Steward for the New England Forestry Foundation and the Society for the Protection of New Hampshire Forests. His The Hersey Mountain Forest: A Background History describes a conservation property in New Hampton and Sanbornton. -

Annual Report of the Officers of the Town of Ashland, for the Fiscal Year

ANNUAL REPORT... Town of Ashland New Hampshire Photo by J. Gordon Lasher 1968 **«*^«wt7 of New HoBop^hir, Libra ry Dates To Remember January 1 Fiscal Year Begins March 4 Meeting -Supervisors of Checklist 7:00-9:00 P.M. At Town Office March 8 Meeting -Supervisors of Checklist 7:00-9:00 P.M. At Town Office March 10 Meeting - Supervisors of Checklist 7:00-9:00 P.M. At Town Office March 11 ANNUAL TOWN MEETING March 31 Motor Vehicle Registration expires April 1 All property both real and personal, assessed to owner this date. April 15 Last day to file inventory to be eligible to make claim to abatement. RSA 77:14 Last day for veterans to file for tax exemptions. Last day for veterans to pay in full real and personal taxes to be eligible for exemptions. May 1 Dog tax due. Licenses available from Town Clerk. Bicycle plates due. Licenses available at Town Office from Chief of Police. December 1 Unpaid real and personal taxes commence drawing in- December 31 Fiscal Year Closes SELECTMEN'S MEETING: Tuesday evenings at 7:00 P.M. at Town Office. Photo on Cover—Centennial Activity 1968 ! Annual Report of the Oflficers of the TOWN OF ASHLAND Bring This Report to Town Meeting With You For the Fiscal Year Ending December 31 1968 Selectmen's Letter 3 Highlights 1968 6 Sewer Construction Report 7 Town Officials and Boards 10 Minutes of 1968 Town Meeting 12 Town Warrant 16 Budget for 1969 19 Statement of Appropriations & Taxes Assessed 23 Summary of Inventory 25 State Tax Audit 26 Payroll Record 1968 47 Detailed Statement of Appropriations & Expenditures -

Meeting Materials

Posted 11/15/2020 1:15pm MEETING MATERIALS Chair: K. Theoharides BOARD OF DIRECTORS’ MEETING Vice-Chair: J. Carroll Secretary: A. Pappastergion Board Members: To be Held Virtually on November 18, 2020 C. Cook Pursuant to Governor Baker’s March 12, 2020 Order K. Cotter P. Flanagan Suspending Certain Provisions of the Open Meeting Law J. Foti B. Peña H. Vitale WebEx Meeting Link J. Walsh https://mwra.webex.com/mwra/onstage/g.php?MTID=ebd7cda84b0bf867cbca2feceaf8d5f3a J. Wolowicz Meeting number (access code): 173 509 7117 Meeting Password: 1118 Time: 1:00 p.m. REVISED AGENDA I. APPROVAL OF MINUTES II. REPORT OF THE CHAIR III. REPORT OF THE EXECUTIVE DIRECTOR IV. WASTEWATER POLICY & OVERSIGHT A. Contract Awards 1. Power Purchase Agreement and Site License for a Photovoltaic System and Battery Storage at Deer Island Treatment Plant: Distributed Solar Development, Contract S591 B. Contract Amendments/Change Orders 1. Agency-Wide Technical Assistance Consulting Services: Kleinfelder Northeast, Inc., Contract 7604 Amendment 2 2. Chelsea Creek Headworks Upgrade: BHD/BEC JV 2015, A Joint Venture, Contract 7161, Change Order 43 3. Prison Point CSO Facility Improvements – Design, CA and RE Services: Arcadis, US, Contract 7359, Amendment 4 4. Piping Relocation at the Pelletizing Plant: Walsh Construction Company II, LLC, Contract 7173, Change Order 2 Meeting of the MWRA Board of Directors, November 18, 2020 Page 2 V. WATER POLICY & OVERSIGHT A. Information 1. Update on Lead and Copper Rule Compliance - Fall 2020 2. Update on the Status of Water Supply Protection Efforts B. Contract Awards 1. Quabbin Maintenance Building Design, Construction Administration and Resident Engineering Services: The Robinson Green Beretta Corporation, Contract 7677 2. -

Stocking Report, May 14, 2021

Week Ending May 14, 2021 Town Waterbody Acworth Cold River Alstead Cold River Amherst Souhegan River Andover Morey Pond Antrim North Branch Ashland Squam River Auburn Massabesic Lake Barnstead Big River Barnstead Crooked Run Barnstead Little River Barrington Nippo Brook Barrington Stonehouse Pond Bath Ammonoosuc River Bath Wild Ammonoosuc River Belmont Pout Pond Belmont Tioga River Benton Glencliff Home Pond Bethlehem Ammonoosuc River Bristol Newfound River Brookline Nissitissit River Brookline Spaulding Brook Campton Bog Pond Carroll Ammonoosuc River Columbia Fish Pond Concord Merrimack River Danbury Walker Brook Danbury Waukeena Lake Derry Hoods Pond Dorchester South Branch Baker River Dover Cocheco River Durham Lamprey River Week Ending May 14, 2021 Town Waterbody East Kingston York Brook Eaton Conway Lake Epping Lamprey River Errol Clear Stream Errol Kids Pond Exeter Exeter Reservoir Exeter Exeter River Exeter Little River Fitzwilliam Scott Brook Franconia Echo Lake Franconia Profile Lake Franklin Winnipesaukee River Gilford Gunstock River Gilsum Ashuelot River Goffstown Piscataquog River Gorham Peabody River Grafton Mill Brook Grafton Smith Brook Grafton Smith River Greenland Winnicut River Greenville Souhegan River Groton Cockermouth River Groton Spectacle Pond Hampton Batchelders Pond Hampton Taylor River Hampton Falls Winkley Brook Hebron Cockermouth River Hill Needle Shop Brook Hill Smith River Hillsborough Franklin Pierce Lake Kensington Great Brook Week Ending May 14, 2021 Town Waterbody Langdon Cold River Lee Lamprey River -

Locke Lake Board President

Soccer Previews: See pages B1, B2, and B3 THURSDAY, AUGUST 24, 2017 COVERING ALTON, BARNSTEAD, & NEW DURHAM - WWW.SALMONPRESS.COM FREE Selectmen discuss use of highway funds BY DAVID ALLEN ed surplus of $80 mil- David Kerr to develop carefully. flail mowers is also tured alive and relocat- Contributing Writer lion in last year’s state some options for use Meanwhile Kerr temporarily out of ser- ed to another location BARNSTEAD — The budget to distribute of the money and bring gave the board a brief vice for minor repairs. far from culverts and Barnstead Board of Se- to towns and cities ac- those to a future board update on highway Kerr called on a beaver roads. lectmen faced an un- cording to the existing meeting for consider- department activity. trapper to capture a The board has ad- usual situation at its formula for state high- ation. The state does One of the department beaver whose dam was vertised for private Tuesday, Aug. 15, meet- way aid, which is based not require an imme- trucks broke down re- threatening a culvert contractors to help ing. It is one they share on a combination of a diate decision by the cently, and is currently too small to handle with snow removal with their select board town’s population and town, and board mem- being inspected for the the potential overflow this winter because of colleagues in neighbor- its road mileage. bers thought it best to level of damage. One during a heavy storm. staff shortages. The ing towns. The money comes consider their options of the department’s The beaver was cap- SEE BARNSTEAD, PAGE A12 The New Hampshire with a few strings at- Legislature was able tached: it cannot be to find $36 million for used to replace local a one-time infusion of tax dollars already funds into local town committed to highway and city highway work, and it gives some funding. -

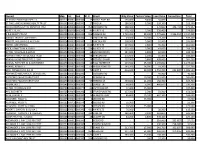

2018 Property Assessment Data

Owner1 Map Lot Sub St. # Street Bldg Value Feature Value Land Value Current Use Total 17 STONE POST ROAD SPE LLC 000210 000014 000000 17 STONE POST RD 196,800 9,400 54,800 - 261,000 27 PINE LANE NOMINEE REALTY TRUST 000240 000018 000000 27 PINE LN 180,500 8,900 339,100 - 528,500 359 COXBOROUGH RD NOMINEE TRST 000250 000008 000000 359 COXBORO RD 180,500 - 279,600 184,733 275,367 40 RT 113, LLC 000236 000108 000000 40 NH RT 113 176,200 3,200 350,400 - 529,800 A & B REALTY TRUST 000231 000013 000000 106 PAUGUS RD 1,733,300 88,100 4,479,600 2,986,192 3,314,808 ABBIATI TRUSTEE, ANTHONY J. 000235 000009 000000 71 FINISTERE RD 49,000 10,500 779,700 - 839,200 ABBOTT, WILLIAM G & ALICIA M 000224 000007 000000 21 LINCOLN RD 268,900 5,000 62,900 - 336,800 ABEAR, JONATHAN D. 000212 000011 000000 1118 NH RT 175 114,500 2,300 46,100 - 162,900 ABER, KENNETH M & EMILY 000227 000032 000001 738 NH RT 175 352,100 3,000 43,600 - 398,700 ACTON, NICHOLAS & BONNI 000245 000023 000000 33 WILDWOOD DR 284,000 3,800 50,900 - 338,700 ADAMS FAMILY REVOCABLE TRUST 000227 000046 000000 98 SARGENT RD 274,600 2,500 56,300 - 333,400 ADAMS LIVING TRUST DEC 5 1991 000235 000007 000000 28 POTATO ISLAND 137,900 5,800 438,000 - 581,700 ADAMS, FLETCHER W & ADRIENNE E 000241 000007 000000 10 TALL TIMBER DR 119,500 15,900 1,139,600 - 1,275,000 ADAMS, ROBERT S 000229 000022 000000 66 PERCH POND RD 149,200 14,300 59,200 - 222,700 ADIE, DONALD M & JILL M 000244 000013 000000 76 US RT 3 416,600 39,500 1,752,700 222,280 1,986,520 ADVANCED MECHANICAL DEVICES INC 000250 000033 000000 COXBORO RD - - 40,300 - 40,300 AGOSTINO PALMIERI IRR TRUST 000240 000035 000000 PERKINS LN - 19,500 321,500 - 341,000 AGOSTINO PALMIERI IRR TRUST 000240 000009 000000 59 PERKINS LN 459,800 21,200 158,400 - 639,400 AHERN, INA J. -

New Hampshire Fish Consumption Guidelines

ARD-EHP-25 2020 New Hampshire Fish Consumption Guidelines Fish and shellfish are an important part of a healthy diet. They are a good source of low fat protein and contain nutrients like omega-3 fatty acids, a key nutrient for brain development. NHDES offers these fish consumption guidelines to educate the public regarding certain contaminants that have been analyzed in fish tissues. There are other contaminants that may be present in the environment that have not been analyzed, nor are they included in this advisory. Mercury analysis has been completed for a variety of the most common freshwater fish species, however not all species or waterbodies have been analyzed for mercury and the other contaminants listed in the advisory (fish sampled to date include 26 species, >230 waterbodies, ~4,000 fish). Mercury does not break down in the environment. Nearly all fish and shellfish have traces of mercury, and fish from some freshwater sources may also contain polychlorinated biphenyls (PCBs) or dioxin. Small amounts of mercury can damage a brain starting to form or grow. That is why babies and young children are at most risk. PCBs and dioxins are man-made organic chemicals which do not readily break down in the environment. They are taken up and may accumulate in fish. PCBs and dioxins have been shown to cause a variety of harmful health effects such as cancer as well as non-cancer health effects involving immune, reproductive, nervous and endocrine systems. Risks from mercury, PCBs and dioxin in fish and shellfish depend on the amount of fish and shellfish eaten and the levels of these contaminants in the fish and shellfish. -

Hazard Mitigation Plan Update, 2015

Town of Holderness, New Hampshire Hazard Mitigation Plan Update, 2015 Prepared by the: Holderness Hazard Mitigation Update Committee Pemigewasset River flooding in Holderness along NH Rte. 175, April 2011 Credit: http://farm7.staticflickr.com/6079/6092948164_57ea16a060_z.jpg January 2015 Intentionally left blank. Town of Holderness, New Hampshire Hazard Mitigation Plan Update January 2015 With Assistance from: Lakes Region Planning Commission 103 Main Street, Suite #3 Meredith, NH 03253 Phone: (603) 279-8171 Fax: (603) 279-0200 www.lakesrpc.org Funding for this plan was provided by the NH Department of Safety, Homeland Security and Emergency Management, and with matching funds provided by the Lakes Region Planning Commission. THE LAKES REGION PLANNING COMMISSION Tamworth Sandwich Freedom Holderness Effingham A Moultonborough s h Ossipee la n d or r b Tuftonboro Hebron r e ar te t H a en w e C g d ri B n Meredith to Alexandria p Bristol m a H W olfeboro w e N Laconia Gilford Danbury Hill Sanbornton Alton F r a Tilton Belmont n k l Andover i n Gilmanton Northfield Barnstead LRPC COMMISSIONERS 2013-2014 Alexandria Belmont Effingham Hebron Moultonborough Sandwich Janet Towse Vacant Theresa Swanick Mitch Manseau Herbert Farnham Toby Eaton Barbara Perry Alton Bridgewater Franklin Hill New Hampton Tamworth Robert Daniels Vacant Tony Giunta Vacant Dr. George Luciano Patricia Farley Andover Bristol Freedom Holderness Northfield Tilton John Cotton Steve Favorite Jean Marshall Robert Snelling Wayne Crowley Joseph Jesseman Douglas Read Ashland Center Harbor Gilford Laconia Ossipee Tuftonboro Gordon McCormack, Jr. Maureen Criasia John Morgenstern Dean Anson, II Dr. Patricia Jones Dan Duffy Warren Hutchins Roger terKuile Stephen Wingate Barnstead Danbury Gilmanton Meredith Sanbornton Wolfeboro David Kerr Charlotte McIver Stanley O.