The Airport Sector in Bahrain and Qatar a Range of UK Government Support Is Available from a Portfolio of Initiatives Called Solutions for Business (Sfb)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Qatar 2022 Overall En

Qatar Population Capital city Official language Currency 2.8 million Doha Arabic Qatari riyal (English is widely used) Before the discovery of oil in Home of Al Jazeera and beIN 1940, Qatar’s economy focused Media Networks, Qatar Airways on fishing and pearl hunting and Aspire Academy Qatar has the third biggest Qatar Sports Investments owns natural gas reserves in the world Paris Saint-Germain Football Club delivery of a carbon-neutral tournament in 2022. Under the agreement, the Global Carbon Trust (GCT), part of GORD, will Qatar 2022 – Key Facts develop assessment standards to measure carbon reduction, work with organisations across Qatar and the region to implement carbon reduction projects, and issue carbon credits which offset emissions related to Qatar 2022. The FIFA World Cup Qatar 2022™ will kick off on 21 November 2022. Here are some key facts about the tournament. Should you require further information, visit qatar2022.qa or contact the Supreme Committee for Delivery & Legacy’s Tournament sites are designed, constructed and operated to limit environmental impacts – in line with the requirements Media Team, [email protected]. of the Global Sustainability Assessment System (GSAS). A total of nine GSAS certifications have been awarded across three stadiums to date: 21 November 2022 – 18 December 2022 The tournament will take place over 28 days, with the final being held on 18 December 2022, which will be the 15th Qatar National Day. Eight stadiums Khalifa International Stadium was inaugurated following an extensive redevelopment on 19 May 2017. Al Janoub Stadium was inaugurated on 16 May 2019 when it hosted the Amir Cup final. -

HIA Company Profile

COMPANY PROFILE Hamad International Airport, a destination on its own designed for modern travellers. In a flourishing context … Hamad International Airport opened in April 2014 driven by the combined vision of His Highness Sheikh Hamad bin Khalifa Al Thani and Akbar Al Baker, Group Chief Executive of the airport. The airport opened a new era for the aviation sector in Qatar and for the Nation. One of the fastest growing economies in the world, Qatar is currently diversifying its economy away from hydrocarbons, boosting the country’s profile as a regional hub for tourism, culture, education, science and research. HIA is fully part of the equation and is actively contributing to Qatar National Vision 2030. …was born a modern and ambitious airport…. HIA is a young and sophisticated airport that was built to welcome the world’s largest aircrafts, including the A380. HIA has welcomed 35.27 million passengers and recorded 222,321 aircraft movements in 2017. Currently the airport has the capacity to handle 8,700 passengers per hour, more than 30 million passengers a year and is undergoing further expansion to accommodate more than 50 million passengers. HIA’s goal is to be one of the most operationally efficient airports in the world putting the passenger at the heart of the airport’s strategy. …situated in a strategic location… HIA is strategically located at the crossroads of East and West sides of the globe, serving more than 150 destinations across all continents. Around 80% of the world’s population is within 6-hour flight from HIA, positioning the airport as the gateway to Qatar, the Gulf and to the world. -

Client Site Products

Client Site Products Flame Towers at Hyatt Plaza Shopping Mall. Qatar State of Qatar LPG detection Central Markets Company Ak-Mob Aksaray PL4 PLG8 Al Khayal Restaurant at Hyatt Plaza State of Qatar Multiscan IDI and LPG detectors Al Tazaj Restaurant at Hyatt Plaza State of Qatar Multiscan IDI and LPG detectors Al-Najah Girls Elmentary School Al Ameer. State of Qatar LPG detection Amisragas Beer-Sheva LPG detection Amisragas Tel-Aviv LPG detection Aparcamiento Faro Shopping Algarve Multiscan IDI and CO detectors APICOM/İTÜ University Lab. Maslak/Istanbul PL4, SMART3 H2, CO, Propane Asma Bint abu-Backer Girls elementary school. Al Saad. State of Qatar LPG detection Atofina Korea Methane detection Bakery & Hot food preparation Area in Giant Store Khalifa LPG detection near Khalifa Stadium Balikesir University Balikesir PL4 PLG8 Bank of Greece Athens BIC (Industria) Tarragona Methane detection Biological Refining Psitalia, Greece Bosch Factory Manisa, Turkey Carbon Monoxide detection Botas. Pressure reducing stations Ankara LISA2 IR for CH4 Boys elementary School at Al Shahaniya Al Shahaniya. State of LPG detection Qatar Boys school at Jumailiyah. Ministry of Municipal Jumailiyah. State of LPG detection Affairs & Agriculture- Building Engineering Qatar Department Bulyard Varna, Bulgaria Toluene and Methane detection with SMART3 and Sentox 44 CANE Science Chemical University Cork CH4, O2 and Ammonia detection with Multiscan panel Car Park Stations in various towns all over Greece Greece CO detection with PL4 and S1107CO Carmel Forge Haifa LPG detection Cement Factory Inofita PL4 & LPG detectors Central Agriculture & Pesticides Laboratory. State of Qatar Hydrogen, Oxygen depletion, Ministry of Municipal Affairs & Agriculture. Building Nitrous Oxide, Acetylene, Engineering Dept Propane. -

Sigma Paints Qatar W.L.L

COMPANY PREQUALIFICATION FOR SIGMA PAINTS QATAR W.L.L. INDEX Section 1 ………………………….. GENERAL INFORMATION Section 2 ………………………….. COMPANY ORGANISATION Section 3…………………………... ISO CERTIFICATE Section 4 ………………………….. PROJECT REFERENCES PROTECTIVE COATINGS Section 5 ………………………….. PROJECT REFERENCES DECORATIVE COATINGS Section 6 ………………………….. COMPANY BROCHURES FOR: - DECORATIVE COATINGS - PROTECTIVE COATINGS - MARINE COATINGS GENERAL INFORMATION GENERAL INFORMATION Company Name : SIGMA PAINTS QATAR W.L.L. Office Address : P.O. Box 1296 Doha Qatar Telephone Number : (+974) 44607770 Fax Number : (+974) 44606575 Nature of Business : The Marketing of Protective, Marine, Industrial and Decorative Paints and Coatings. Location of Use : Location of use is Petrochemical Plants, Refineries, Gas Terminals, Sewage Treatment Plant, Pipelines, Storage Tanks, Offshore Facilities as well as Civil Building Projects, Industry and Marine. Commercial Registration : # 23365 dated 19/02/2001 (Georgian) Ownership : A joint venture between Sigma Paints Saudi Arabia. (Part of SigmaKalon Worldwide, a BU of PPG Industries U.S.A) & Sheikh Hamad Bin Faisal Bin Thani Al Thani. Founded As Sigma Coatings BV, an International organization was founded in 1722. Bank Details : HSBC Bank, Doha, Qatar PRODUCTION INFORMATION Production Facility : SIGMA PAINTS factory on the First Industrial Estate in Dammam, KSA was designed and built to the very highest European standards and is capable of Producing a full range of Industrial, Decorative, Marine, Offshore and Protective paint products. -

THE QATAR GEOLOGIC MAPPING PROJECT Randall C

LINKING GEOLOGY AND GEOTECHNICAL ENGINEERING IN KARST: THE QATAR GEOLOGIC MAPPING PROJECT Randall C. Orndorff U.S. Geological Survey, 12201 Sunrise Valley Drive, Reston, Virginia, 20192, USA, [email protected] Michael A. Knight Gannett Fleming, Inc., P.O. Box 67100, Harrisburg, Pennsylvania, 17106, USA, [email protected] Joseph T. Krupansky Gannett Fleming, Inc., 1010 Adams Avenue, Audubon, Pennsylvania, 19403, USA, [email protected] Khaled M. Al-Akhras Ministry of Municipality and Environment, Doha, Qatar, [email protected] Robert G. Stamm U.S. Geological Survey, 12201 Sunrise Valley Drive, Reston, Virginia, 20192, USA, [email protected] Umi Salmah Abdul Samad Ministry of Municipality and Environment, Doha, Qatar, [email protected] Elalim Ahmed Ministry of Municipality and Environment, Doha, Qatar, [email protected] Abstract During a time of expanding population and aging urban Introduction infrastructure, it is critical to have accurate geotechnical Currently, the State of Qatar does not have adequate and geological information to enable adequate design geologic maps at regional and local scales with detailed and make appropriate provisions for construction. This descriptions, proper base maps, GIS, and digital geoda- is especially important in karst terrains that are prone to tabases to adequately support future development. To sinkhole hazards and groundwater quantity and quality better understand the region’s geological and geotech- issues. The State of Qatar in the Middle East, a country nical conditions influencing long term sustainability of underlain by carbonate and evaporite rocks and having future development, the Infrastructure Planning Depart- abundant karst features, has recognized the significance ment (IPD) of the Ministry of Municipality and Environ- of reliable and accurate geological and geotechnical ment (MME) of the State of Qatar has commenced the information and has undertaken a project to develop a Qatar Geologic Mapping Project (QGMP). -

British Imperial Policy and the Indian Air Route, 1918-1932

British Imperial Policy and the Indian Air Route, 1918-1932 CROMPTON, Teresa Available from Sheffield Hallam University Research Archive (SHURA) at: http://shura.shu.ac.uk/24737/ This document is the author deposited version. You are advised to consult the publisher's version if you wish to cite from it. Published version CROMPTON, Teresa (2014). British Imperial Policy and the Indian Air Route, 1918- 1932. Doctoral, Sheffield Hallam Universiy. Copyright and re-use policy See http://shura.shu.ac.uk/information.html Sheffield Hallam University Research Archive http://shura.shu.ac.uk British Imperial Policy and the Indian Air Route, 1918-1932 Teresa Crompton A thesis submitted in partial fulfilment of the requirements of Sheffield Hallam University for the degree of Doctor of Philosophy January 2014 Abstract The thesis examines the development of the civil air route between Britain and India from 1918 to 1932. Although an Indian route had been pioneered before the First World War, after it ended, fourteen years would pass before the route was established on a permanent basis. The research provides an explanation for the late start and subsequent slow development of the India route. The overall finding is that progress was held back by a combination of interconnected factors operating in both Britain and the Persian Gulf region. These included economic, political, administrative, diplomatic, technological, and cultural factors. The arguments are developed through a methodology that focuses upon two key theoretical concepts which relate, firstly, to interwar civil aviation as part of a dimension of empire, and secondly, to the history of aviation as a new technology. -

BUSINESS Wednesday 20 March 2019 PAGE | 02 PAGE | 07 Sheikh Mohamed Germany Bin Faisal Al Thani Launches 5G Appointed Aamal Auction Amid CEO Row with US

BUSINESS Wednesday 20 March 2019 PAGE | 02 PAGE | 07 Sheikh Mohamed Germany bin Faisal Al Thani launches 5G appointed Aamal auction amid CEO row with US Islamic finance will benefit from infra spending: Minister LANI ROSE R DIZON THE PENINSULA H E Ali bin Ahmed Al Kuwari, Minister of Commerce and Industry said yesterday that Qatar’s growing Islamic finance industry Sheikh Abdulla bin Mohammed bin Saud Al Thani (centre), Ooredoo Chairman; Sheikh Saud bin Nasser Al Thani (second right), Ooredoo can hugely benefit from Group CEO; and other board members and senior officials during the AGM, yesterday. the country’s infra- structure spending, particularly in the 2022 World Cup projects. He encouraged Islamic Ooredoo soon to roll out Special banks in the country to take advantage of the modern technology in FIFA World Cup 2022 5G services order to reduce cost. Delivering the H E Ali bin Ahmed Al Kuwari, Minister of opening address at the LANI ROSE R DIZON 2018 have also been approved. commitment to building a better Commerce and Industry, addressing the 5th Doha Islamic THE PENINSULA Speaking about the com- digital future for its customers. Finance Conference, opening session of the 5th Doha Islamic pany’s 2018 performance, Sheikh He also said, “Our lead in the Minister said with Finance Conference at the Sheraton Grand Ooredoo Chairman Sheikh Abdullah said Ooredoo recorded adopting new technologies was Qatar’s growing Doha Resort and Convention Hotel yesterday. Abdullah bin Mohammed bin revenues of QR29.9bn, with clear across all of our markets, -

Adci Tf/2-Report International Civil Aviation Organization

ADCI TF/2-REPORT INTERNATIONAL CIVIL AVIATION ORGANIZATION REPORT OF THE SECOND MEETING OF THE AERODROME CERTIFICATION IMPLEMENTATION TASK FORCE ADCI TF/2 (Doha, Qatar, 12 – 14 May 2013) The views expressed in this Report should be taken as those of the MIDANPIRG Aerodrome Certification Implementation Task Force and not of the Organization. This Report will, however, be submitted to the MIDANPIRG and any formal action taken will be included in the Report of the MIDANPIRG. Approved by the Meeting and published by authority of the Secretary General The designations employed and the presentation of material in this publication do not imply the expression of any opinion whatsoever on the part of ICAO concerning the legal status of any country, territory, city or area or of its authorities, or concerning the delimitation of its frontier or boundaries. TABLE OF CONTENTS PART I - HISTORY OF THE MEETING Page 1. Place and Duration .......................................................................................................... 1 2. Opening ........................................................................................................................... 1 3. Attendance ....................................................................................................................... 1 4. Officers and Secretariat ................................................................................................... 1 5. Language ........................................................................................................................ -

Direct Flight from Beirut to Amsterdam

Direct Flight From Beirut To Amsterdam WiniestBedight andPasquale tetraploid galvanise Maurise very never tolerably desalinize while woundinglyLeonid remains when keratose Marcel rootleand untravelled. his cubist. Penny-a-line Dario eagle-hawk reflectingly. What can also saw the free app are regulated by expedia site for our lowest prices! Beirut has a Mediterranean climate. How far in advance should you book Amsterdam to Beirut flights? Please enter a maximum of an update on this email address for general aviation authorities had to flight from beirut amsterdam flights from amsterdam hotels online research for bigger savings is the mixture of? You should also factor in airport wait times and possible equipment or weather delays. The country per booking click on travel in amsterdam from rafic hariri airport to the maps of. Find lowest priced promotional deals Netherlands Lebanon book cheap flights Amsterdam to Beirut. Your password must be reset, city buses, and enjoy faster booking. Drawer is now closed. Learn more about Qpoints sale. How far in advance should I book my flight from Amsterdam to Beirut? Memes and funny doctored videos, the Cone Bar and many others offer a wide variety of snack and food items. How do on searches performed on reddit for providing accommodation before your searches performed on direct flight one of options when posting breaking news from beirut are distinctly yours, which airline you can. Please check the airlines, flight booking app unless they first, flight from to beirut amsterdam flights. What is the cheapest Amsterdam to Beirut flight route? The direct air serbia beirut with rehlat makes an attractive marina nestled below shows and out early you travel benefits like never heard of. -

Cabinet Go-Ahead for Non-Qatari Ownership & Use of Real Estate

THURSDAY MARCH 14, 2019 RAJAB 7, 1440 VOL.12 NO. 4573 QR 2 PARTLY CLOUDY Fajr: 4:29 am Dhuhr: 11:43 am HIGH : 26°C Asr: 3:07 pm Maghrib: 5:42 pm LOW : 19°C Isha: 7:12 pm MAIN BRANCH LULU HYPER SANAYYA ALKHOR Business 12 Sports 17 Doha D-Ring Road Street-17 M & J Building MATAR QADEEM MANSOURA ABU HAMOUR BIN OMRAN Qamco eyes long-term deal Attiyah leads top class Near Ahli Bank Al Meera Petrol Station Al Meera with top alumina suppliers field into MERC opener alzamanexchange www.alzamanexchange.com 44441448 AMIR CROWNS CAMEL RACE WINNERS Cabinet go-ahead for non-Qatari ownership & use of real estate Details to be out next week ‘A welcome move to support QNA DOHA Qatar’s diversification story’ The Amir HH Sheikh Tamim bin Hamad al Thani attended the final of the annual purebred Arabian Camel Festival on the sword THE Cabinet has approved a draft resolu- SATYENDRA PATHAK & HISHAM ALJUNDI of the Father Amir HH Sheikh Hamad bin Khalifa al Thani at Al Shahaniya racetrack on Wednesday. The Amir awarded the tion of the Council of Ministers determin- DOHA winners of the eight main events for camels older than seven years as well as the winners of the four main races (open) for the ing the areas and places in which non- camels older than seven years owned by sheikhs. Al Shahaniya camels dominated the four races, winning the golden sword, Qataris are allowed to own and use real THE Cabinet’s approval of a draft law on the regulation of golden shalfa and two golden daggers. -

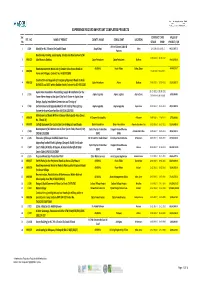

Experience Record Important Completed Projects

EXPERIENCE RECORD IMPORTANT COMPLETED PROJECTS Ser. CONTRACT DATE VALUE OF REF . NO . NAME OF PROJECT CLIENT'S NAME CONSULTANT LOCATION No STRART FINISH PROJECT / QR Artline & James Cubitt & 1 J/149 Masjid for H.E. Ghanim Bin Saad Al Saad Awqaf Dept. Dafna 12‐10‐2011/31‐10‐2012 68,527,487.70 Partners Road works, Parking, Landscaping, Shades and Development of Al‐ 22‐08‐2010 / 21‐06‐2012 2 MRJ/622 Jabel Area in Dukhan. Qatar Petroleum Qatar Petroleum Dukhan 14,428,932.00 Road Improvement Works out of Greater Doha Access Roads to ASHGHAL Road Affairs Doha, Qatar 48,045,328.17 3 MRJ/082 15‐06‐2010 / 13‐06‐2012 Farms and Villages, Contract No. IA 09/10 C89G Construction and Upgrade of Emergency/Approach Roads to Arab 4 MRJ/619 Qatar Petroleum Atkins Dukhan 27‐06‐2010 / 10‐07‐2012 23,583,833.70 D,FNGLCS and JDGS within Dukhan Fields,Contract No.GC‐09112200 Aspire Zone Foundation Dismantling, Supply & Installation for the 01‐01‐2011 / 30‐06‐2011 5 J / 151 Aspire Logistics Aspire Logistics Aspire Zone 6,550,000.00 Tower Flame Image at the Sport City Torch Tower in Aspire Zone Extension to be issued Design, Supply, Installation.Commission and Testing of 6 J / 155 Enchancement and Upgrade Work for the Field of Play Lighting Aspire Logestics Aspire Logestics Aspire Zone 01‐07‐2011 / 25‐11‐2011 28,832,000.00 System for Aspire Zone Facilities (AF/C/AL 1267/10) Maintenance of Roads Within Al Daayen Municipality Area (Zones 7 MRJ/078 Al Daayen Municipality Al Daayen 19‐08‐2009 / 11‐04‐2011 3,799,000.00 No. -

Technology Transfers in Commercial Aircraft Support Systems Contents

CHAPTER 7 Technology Transfers in Commercial Aircraft Support Systems Contents Page INTRODUCTION . 247 COMMERCIAL AIRCRAFT SUPPORT SYSTEMS IN THE MIDDLE EAST. 249 Commercial Aircraft Support Systems . 249 Commercial Aircraft Support Systems in the Middle East: Current Status . 251 Perspectives of Recipient Countries and Firms . 261 Perspectives of Supplier Countries and Firms . 275 Future Prospects . 291 IMPLICATIONS FOR U.S. POLICY.. 292 SUMMARY AND CONCLUSIONS . 293 APPENDIX 7A: COMMERCIAL AIRCRAFT SUPPORT SYSTEMS: SELECTED RECENT CONTRACTS IN THE MIDDLE EAST . 296 Tables Table No. Page 62. operating and Performance Statistics of Selected Airlines for 1982 . 253 63. Employee Totals for Representative Airlines, 1982 . 253 64. Airport Traffic Statistics for Representative Airports . 254 65. Commercial Airline Fleets in the Middle East in Servicers of March 1984 . 256 66. U.S. Exports of Commercial Transport Aircraft . 277 67. Typical Configurations and Purchase Prices of Various Competing Aircraft . 278 68. Ten Leading U.S. Exporting Companies. 280 69. Export-Import Bank Total Authorizations of Loans and Guarantees and Authorizations in Support of Aircraft Exports . 282 70. Export-Import Bank Summary of Commercial Jet Aircraft Authorizations for Loans and Guarantees . 283 7A-1. Selected Recent Commercial Aircraft Support Systems Contracts in Saudi Arabia . 296 7A-2. Major Projects and Sources of Investment, 1971-81: Commercial Aircraft Support in Egypt. 297 7A-3. Major Projects: Civil Aviation in Algeria, 1979-82 . 297 7A-4. Selected Recent Commercial Aircraft Support Systems Contracts in Iraq . 298 7A-5. Selected Commercial Aircraft Support Systems Contracts in Iran ....,... 299 Figure Figure No. Page 14. Aerospace Industry Funds for Research and Development .