Dated December 1, 2020, for Series 2020A

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

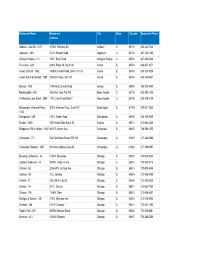

Copy of Chipotle Restuarant List

Restaurant Name Restaurant City State Zipcode Restaurant Phone Address Addison - Lake 53 - 1819 1078 N. Rohlwing Rd Addison IL 60101 630-282-7220 Algonquin - 399 412 N. Randall Road Algonquin IL 60102 847-458-1030 Arlington Heights - 131 338 E. Rand Road Arlington Heights IL 60004 847-392-8328 Fox Valley - 624 848 N. Route 59, Suite 106 Aurora IL 60504 630-851-3271 Aurora Orchard - 1462 1480 N Orchard Road, Suite 114-116 Aurora IL 60506 630-723-5004 Aurora Kirk & Butterfield - 1888 2902 Kirk Road, Unit 100 Aurora IL 60504 630-429-9437 Berwyn - 1753 7140 West Cermak Road Berwyn IL 60402 708-303-5049 Bloomingdale - 858 396 West Army Trail Rd. Bloomingdale IL 60108 630-893-2108 Fairfield and Lake Street - 2884 170 E Lake Street Suite C Bloomingdale IL 60108 630-529-5128 Bloomington Veterans Prkwy - 305 N. Veterans Pkwy., Suite 101 Bloomington IL 61704 309-661-7850 1035 Bolingbrook - 529 274 S. Weber Road Bolingbrook IL 60490 630-759-9359 Bradley - 2609 1601 Illinois State Route 50 Bradley IL 60914 815-932-3225 Bridgeview 87th & Harlem - 3047 8813 S. Harlem Ave Bridgeview IL 60455 708-598-1555 Champaign - 771 528 East Green Street, STE 101 Champaign IL 61820 217-344-0466 Champaign Prospect - 1837 903 West Anthony Drive #A Champaign IL 61820 217-398-0997 Broadway & Belmont - 36 3181 N. Broadway Chicago IL 60657 773-525-5250 Clybourn Commons - 42 2000 N. Clybourn Ave. Chicago IL 60614 773-935-5710 Orchard - 52 2256-58 N. Orchard Ave. Chicago IL 60614 773-935-6744 Jackson - 88 10 E. -

2020 Final Budget Book.Indb

456 PAGE INTENTIONALLY LEFT BLANK The Government Finance Offi cers Association of the United States and Canada (GFOA) presented a Distinguished Budget Presentation Award to the Illinois State Toll Highway Authority for the Annual Budget beginning January 2019. In order to receive this award, a governmental unit must publish a budget document that meets program criteria as a policy document, operations guide, fi nancial plan and communications device. For questions regarding the 2020 Budget Book, please contact: Michael Colsch Cathy Williams Sam Samra Chief Financial Offi cer Deputy Chief of Finance Capital Budget Manager Phone: 630-241-6800 TABLE OF CONTENTS TABLE OF CONTENTS Section Page Executive Lett er .......................................................................................................................................................................... 1 Executive Summary ................................................................................................................................................................... 3 Tollway Organization and Background ................................................................................................................................. 7 Revenue Sources and Underlying Assumptions ................................................................................................................. 13 Fund Structure ......................................................................................................................................................................... -

NORTHWEST COUNCIL of MAYORS TECHNICAL COMMITTEE Agenda

NORTHWEST MUNICIPAL CONFERENCE 1600 East Golf Road, Suite 0700 A Regional Association of Illinois Des Plaines, Illinois 60016 Municipalities and Townships (847) 296-9200 Fax (847) 296-9207 Representing a Population of Over One Million www.nwmc-cog.org MEMBERS NORTHWEST COUNCIL OF MAYORS Antioch Arlington Heights TECHNICAL COMMITTEE Bannockburn Agenda Barrington Bartlett Friday, April 23, 2021 Buffalo Grove Deer Park 8:30 a.m. Deerfield Via Zoom Video Conference Des Plaines Elk Grove Village https://us02web.zoom.us/j/88625528035?pwd=eEZ6N3k4L0RtcExsdlloYXZkM0xzU Evanston Fox Lake T09 Glencoe Meeting ID: 886 2552 8035 Glenview Grayslake Passcode: NW042321 Hanover Park Highland Park Hoffman Estates I. Call to Order Kenilworth Lake Bluff Lake Forest II. Approval of January 22, 2021 Meeting Minutes (Attachment A) Lake Zurich Libertyville Action Requested: Approval of minutes Lincolnshire Lincolnwood Morton Grove III. Agency Reports Mount Prospect Niles a. CMAP Report (Attachment B) Northbrook b. IDOT Highways Report (Attachment C) Northfield Northfield Township c. IDOT Local Roads Update (Attachment D) Palatine Park Ridge d. Illinois Tollway (Attachment E) Prospect Heights e. Cook County Department of Transportation and Highways Rolling Meadows Schaumburg (Attachment F) Skokie Streamwood f. Metra (Attachment G) Vernon Hills g. Pace (Attachment H) West Dundee Wheeling h. RTA Wilmette Action Requested: Informational Winnetka President Kathleen O’Hara IV. Northwest Council Surface Transportation Program Lake Bluff A. Current Program Update (Attachment I) Vice-President Staff will provide a brief overview of the current program, noting any Joan Frazier Northfield changes since the previous meeting. Action Requested: Informational/Discussion Secretary Dan Shapiro Deerfield B. Cost Increase Request – Village of Streamwood (Attachment J) Treasurer Staff recommends approval of the Village of Streamwood’s request for Ray Keller Lake Zurich $220,783 in Construction funding for the Park Ave Resurfacing project in FFY 2021. -

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Br

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Bruce Rauner Director David Gonzalez Acting Secretary Randall Director Mark Peterson Blankenhorn Director Jim Banks Director Jeff Redick Director Terry D’Arcy Director James Sweeney Director Earl S. Dotson Director Tom Weisner Pursuant to the requirements of the Authority’s By-Laws, Notice is hereby given of the Bo ard Meeting of the Authority to be held on Thursday, May 28, 2015 at 9:00 a.m. in the Boardroom of the Administration Building in Downers Grove, Illinois. Paula Wolff, Chair This meeting will be accessible to individuals with disabilities in compliance with Executive Order #5, and pertinent state and federal laws, upon notification of anticipated attendance. Persons with disabilities planning to attend and needing accommodations should contact the Americans with Disabilities Act Coordinator of The Illinois State Toll Highway Authority at (630) 241-6800, Ext. 1010 in advance of the meeting at 2700 Ogden Avenue, Downers Grove, IL, to inform of their anticipated attendance. There will be live feed Webcasting of the Board Meeting while in session. An audio file will be available five business days after the meeting at www.illinoistollway.com THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden, Downers Grove, IL 60515 BOARD MEETING AGENDA May 28, 2015 9:00 a.m. 1.0 CALL TO ORDER 2.0 ROLL CALL 3.0 PUBLIC COMMENT 4.0 CHAIR 1. Approval of the minutes of the Regular Board Meeting and Executive Session held April 23, 2015. 2. Review and approve Executive Session minutes for public release. -

2019 NCFPW Meeting Information General Schedule

2019 NCFPW Meeting Information Thank you for registering for the 2019 NCFPW Meeting! Here is some information on the meeting and the surrounding area. The meeting will be held at the Morton Arboretum in Lisle, IL, 25 miles from downtown Chicago. The Morton Arboretum is an internationally recognized nonprofit organization dedicated to the planting and conservation of trees. Its 1,700 acres hold more than 222,000 live plants representing nearly 4,300 species from around the world. https://www.mortonarb.org If you will be driving to the meeting, please inform the person at the gatehouse that you are with the North Central Forest Pest Workshop and they will let you in for free. General Schedule Monday 9/23/19 Meet and Greet/Afternoon Morton Arboretum exploration on your own Participants arriving early or staying on after the meeting can explore the grounds by car or on foot. Here are maps and directions to the Arboretum Grounds: https://www.mortonarb.org/visit-explore/plan-visit/maps-and-directions You can also join the troll hunt: https://www.mortonarb.org/events/troll-hunt We would also like to invite people arriving on Monday to take advantage of the Tram Tours which happen throughout the afternoon (schedule TBD) for which we will have vouchers for interested people (https://www.mortonarb.org/events/acorn-express-tram-tours).Please let us know on the registration form if you will be taking advantage of this so we know how many tickets to reserve. This will be followed by a Meet and Greet at the Visitor Center Sycamore Room (across the entryway from the main Visitor Center) from 5-7 pm. -

Buffalo Grove, Illinois (AMP) 56 W. Dundee Road Buffalo Grove,IL

Buffalo Grove, Illinois (AMP) ** Note - Google Maps may be unreliable for this location. From Southwest: Take 290 West to RT. 53 North. Exit at RT. 68 56 W. Dundee Road Dundee Rd. Go east on Dundee Rd to 56 W. Dundee Rd. which is just west of Buffalo Grove Rd. North side of road across Buffalo Grove,IL 60089 from Citi Bank. From the South via 294: Take 294 North and exit at Willow Rd. (Palatine Rd.). Go west to RT. 21 Milwaukee Ave. Go north on RT. 21 Milwaukee to Dundee Rd. Go west on Dundee Rd. to 56 W. which is past RT. 83. On North side of road across from Citi Bank. From East via Edens 94: Take Edens north and exit at Dundee Rd. Go west to 56W. Map Carbondale, Illinois (AMP) From US-51 S - turn left onto W Walnut St. The location is on the left in the Eastgate Shopping Center. From US-51 N - 628 E. Walnut St turn right onto W Walnut St. The location is on the left in the Eastgate Shopping Center. Carbondale,IL 62901 Map Chicago (Michigan Ave), Illinois (AMP) Take US-41S which becomes I-94E. Take the W Jackson Blvd exit (51F). Turn left on W Jackson Blvd. Turn right on S 332 S. Michigan Ave. Michigan Ave. Suite 410 Map Chicago,IL 60604 Franklin Park, Illinois (AMP) From 294 S - (This route has tolls). From 294S, take the IL-19 exit towards Irving Park Rd. Keep right at the fork, following 9507 Grand Ave the signs for IL-19/Irving Park Road. -

Village of Mundelein

M U N DEL E I N FOR B U S I NESS. FOR L I FE. 35 MILES NORTHWEST OF CHICAGO EASY ACCESS TO DOWNTOWN CHICAGO AND THREE AIRPORTS W E LCOME T O M UNDE L EIN, I LLI NOI S — VILLAGE OF BUSINE SS MINDE D … F O R W ARD THI NKI N G MUNDELEIN INCORPORATED 1909 The Village of Mundelein, a vibrant and progressive community of nearly 32,000 residents, AN AWARD WINNING has a rather simple approach to economic development—we are on YOUR team and we COMMUNITY are committed to doing everything we can to help your business succeed. Mundelein is situated in the center of beautiful Lake County, Illinois—one of the strongest areas GOVERNOR’S HOMETOWN of commercial and industrial growth in the nation, with excellent housing, recreational, AWARD WINNER educational, and business opportunities. TOP 100 SAFEST CITIES IN AMERICA—RANKED 38 Mundelein is a full-service community with municipal services second to none. The Village provides fire and police protection, water delivery, wastewater treatment, building RECIPIENT NEW URBANISM inspection, engineering design and inspection, street maintenance, and economic CNU MERIT AWARD FOR MASTER REDEVELOPMENT development assistance. Each department’s highest priority is providing exceptional IMPLEMENTATION PLAN customer service. Plus, Mundelein’s award-winning schools, Park and Recreation programs and library services offer residents numerous leisure, recreational, and enrichment options. CALEA ACCREDITED— THE GOLD STANDARD IN PUBLIC If you are seeking assistance relocating or expanding your business, we can answer SAFETY ACCREDITATION your questions and offer advice in the areas of economic development, site selection, MUNDELEIN PARK AND engineering, finance, demographics, construction, and marketing, to name just a few. -

475 Ethics Ordinance List As of April 2018

475 Ethics Ordinance List as of April 2018 CITY OF CHICAGO 475 Ethics Ordinance List of Vendors who have received from City of Chicago payments totaling $10,000 or more in any 12 consecutive months period over the past four reporting years VENDOR NAME VENDOR ADDRESS "D" CONSTRUCTION, INC. 1488 S BROADWAY, COAL CITY, IL 60416 100 CLUB OF CHICAGO 875 N MICHIGAN AVENUE SUITE 1351, CHICAGO, IL 60611 1100 EAST 47TH STREET LLC 32 NORTH DEAN STREET , ENGLEWOOD , NJ 07361 1140 NORTH BRANCH DEVELOPMENT LLC 701 W ERIE ST, CHICAGO, IL 60610 1200 MADISON RACINE LLC 912 WEST LAKE STREET, CHICAGO, IL 60607 1300 ASTOR TOWER P O BOX #661095, CHICAGO, IL 60666 1319 S SPAULDING LLC OR CHICAGO TITLE INSURANCE ACCT#029036254-002, CHICAGO, IL 60601 1325 S. STATE STREET LLC 2000 N RACINE AVE, CHICAGO, IL 60614 1330 W FULTON LLC 1040 W RANDOLPH ST, CHICAGO, IL 60607 1515 N HALSTED LLC 211 N CLINTON ST STE 3S, CHICAGO, IL 60661 1600 E. 53RD STREET LLC 32 NORTH DEAN STREET, ENGLEWOOD, NJ 07631 1625 S. CLARK ST LLC C/O DLA PIPER LLP, 203 N LASALLE ST STE. 1900, CHICAGO, IL 60602 1642 N BESLY LLC 1040 W RANDOLPH ST, CHICAGO, IL 60607 18TH STREET. DEVELOPMENT. CORP. 1839 S CARPENTER ST, CHICAGO, IL 60608 1K FULTON LLC. 1040 WEST RANDOLPH STREET, CHICAGO, IL 60607 2109 S HALSTED LLC 155 N PFINGSTEN RD STE 370, DEERFIELD, IL 60015 2600 IRVING LLC 1728 MAPLE AVE, NORTHBROOK, IL 60062 2715 NMA LLC 3215 WEST FULLERTON PKWY, CHICAGO, IL 60647 2736 W. -

2015 Bureau, Lasalle, Marshall, Putnam, and Stark Counties Natural Hazards Mitigation Plan

2015 Bureau, LaSalle, Marshall, Putnam, and Stark Counties Natural Hazards Mitigation Plan Prepared by: North Central Illinois Council of Governments Ottawa, Illinois 2015 Bureau, LaSalle, Marshall, Putnam, and Stark Counties Natural Hazards Mitigation Plan Prepared by: North Central Illinois Council of Governments 613 West Marquette Street Ottawa, Illinois 61350 www.ncicg.org August 2015 NCICG Planning Team Nora Fesco, Executive Director Kevin Lindeman, Economic Development District Director Benjamin Wilson, Community Development Director Kendall Cramer, Community Development Coordinator Table of Contents Executive Summary ................................................................................................................... ES-1 – ES5 Chapter 1: Introduction ......................................................................................................................... 1-1 Background ............................................................................................................................................ 1-1 County Demographics .......................................................................................................................... 1-5 Participating Communities and Local Match ........................................................................................ 1-6 Planning Process ................................................................................................................................... 1-7 Public Participation .............................................................................................................................. -

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Br

THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden Avenue Downers Grove, Illinois 60515 Governor Bruce Rauner Director Joseph N. Gomez Secretary Randall Blankenhorn Director David Gonzalez Director James Banks Director Craig B. Johnson Director Corey B.Brooks Director Nick Sauer Director Earl S. Dotson, Jr. Director James Sweeney Pursuant to the requirements of the Authority’s By-Laws, Notice is hereby given of the Regular Board Meeting of the Authority to be held on Wednesday, March 23, 2016 at 9:00 a.m. in the Boardroom of the Administration Building in Downers Grove, Illinois. Robert J. Schillerstrom, Chairman This meeting will be accessible to individuals with disabilities in compliance with Executive Order #5, and pertinent state and federal laws, upon notification of anticipated attendance. Persons with disabilities planning to attend and needing accommodations should contact the Americans with Disabilities Act Coordinator of The Illinois State Toll Highway Authority at (630) 241-6800, Ext. 1010 in advance of the meeting at 2700 Ogden Avenue, Downers Grove, IL, to inform of their anticipated attendance. There will be live feed Webcasting of the Board Meeting while in session. A video file will be available five business days after the meeting at www.illinoistollway.com. THE ILLINOIS STATE TOLL HIGHWAY AUTHORITY Administration Building 2700 Ogden, Downers Grove, IL 60515 BOARD OF DIRECTORS MEETING AGENDA March 23, 2016 9:00 a.m. 1.0 CALL TO ORDER / PLEDGE OF ALLEGIANCE 2.0 ROLL CALL 3.0 PUBLIC COMMENT 4.0 CHAIRMAN 1. Approval of the Minutes of the Regular Board of Directors Meeting held February 25, 2016. -

East Branch Dupage River Watershed & Resiliency Plan

East Branch DuPage River Watershed & Resiliency Plan (DRAFT) Prepare, React and Recover February 2015 y eg He at a tr lth S & & W ip e h l s lb r e e i d n a g e L I n f r a s t y r t u e c i t c u o r e S & & E y nv om iro on nm Ec ent Prepared For DuPage County Stormwater Management By: Hey and Associates, Inc. Birchline Planning, LLC. Camiros, Ltd. Contents 1. Executive Summary .................................................................................................. 1 2. Glossary ..................................................................................................................... 2 2.1. Agencies/Stakeholders .......................................................................................... 2 2.2. Acts/Ordinances/Programs .................................................................................. 4 2.3. Terms ..................................................................................................................... 5 2.4. Watersheds, Subwatersheds and River Reaches................................................... 7 3. Introduction .............................................................................................................. 9 3.1. Watershed Planning Overview .............................................................................. 9 3.1.1. What is Watershed Planning? .................................................................................. 9 3.1.2. Watershed Planning for the East Branch DuPage River .........................................10 3.1.3. Resilience -

Bicycle Plan

CITY OF BATAVIA BICYCLE PLAN April 23, 2007 City of Batavia, Illinois League of Illinois Bicyclists 100 N. Island Avenue 2550 Cheshire Drive Batavia, IL 60510 Aurora, IL 60504 (630) 879-1424 (630) 978-0583 Table of Contents 1 Introduction 1 2 Public and Agency Involvement 2 Batavia Bicycle Plan Advisory Committee 2 Public Input 2 Agency Involvement 2 3 Bikeway Types in the Batavia Plan 3 AASHTO Guide 3 Trails 3 Sidepaths 3 Bike Lanes 5 Shared Bike/Parking Lanes 5 “Sharrows” Pavement Markings 6 Signal Activation by Bikes 6 Bicycle Level of Service 7 On-road Bikeway Liability 7 4 Guidelines for Bikeway Recommendations 8 General 8 Strategic 8 Selecting Bikeway Type 8 5 Bikeway Network Recommendations 10 Existing Conditions 10 Road Network Recommendations 11 Priority and Implementation Readiness 12 Recommendations for Existing Trails 12 Recommendations for New Trails and Links 17 Recommendations for Spot Improvements 20 6 Safe Routes to School 21 Method and Common Barriers 21 General Recommendations 21 School-specific Information 22 7 Other Recommendations 27 Bicycle Parking 27 Education 28 Encouragement 29 Enforcement 29 8 Plan Implementation – Other Issues 31 Implementation Funding 31 Policies and Ordinances 31 Committee and Staff Time 32 Appendices 33 1 Introduction The City of Batavia has as a goal to obtain the designation of "Bicycle Friendly Community" recognized by the League of American Bicyclists for its residents and visitors. Already, Batavia is recognized as an attraction for cyclists, with off-road bikeways including the Fox River Trail and the Illinois Prairie Path and popular destinations including the Fox River and Fermilab.