2016 10.19 Future EON Equity Story Backup

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Reservoir Released Waves As a Transient Riverine Pollution Mitigation Tool

Reservoir Released Waves as a Transient Riverine Pollution Mitigation Tool An examination of the feasibility of using waves of water released from a reservoir as a response to pollution spills. Simon DeSmet Submitted in accordance with the requirements for the degree of Doctor of Philosophy The University of Leeds School of Geography December 2014 - ii - The candidate confirms that the work submitted is his/her own and that appropriate credit has been given where reference has been made to the work of others. This copy has been supplied on the understanding that it is copyright material and that no quotation from the thesis may be published without proper acknowledgement. © 2014 The University of Leeds and Simon DeSmet - iii - Acknowledgements I have depended on God and faith to carry me though the preparation of this Thesis. A number of individuals have been of great assistance over the past few years. Firstly my two primary supervisors Dr Paul Kay and Dr Jonathan Carrivick have been immensely patient, taught me to write properly, vetted my ideas and have provided great wisdom and experience. Technical assistance with the Fluent software was provided by Dr Andy Sleigh and Dr Carl Gikeson. Access to the SORBY flume facility and input on ideas for the flume study were given by Dr Daniel Parsons and Dr Gareth Keevil. For help in designing the field study and collecting the data I would like to thank David Ashley, Rachel Gasior, Dr Pengfei Li, Dr Ben Gillespie and numerous individuals a the Environment Agency. Additionally I owe a thanks to Rachel Homer for assistance with statistics. -

South Yorkshire

INDUSTRIAL HISTORY of SOUTH RKSHI E Association for Industrial Archaeology CONTENTS 1 INTRODUCTION 6 STEEL 26 10 TEXTILE 2 FARMING, FOOD AND The cementation process 26 Wool 53 DRINK, WOODLANDS Crucible steel 27 Cotton 54 Land drainage 4 Wire 29 Linen weaving 54 Farm Engine houses 4 The 19thC steel revolution 31 Artificial fibres 55 Corn milling 5 Alloy steels 32 Clothing 55 Water Corn Mills 5 Forging and rolling 33 11 OTHER MANUFACTUR- Windmills 6 Magnets 34 ING INDUSTRIES Steam corn mills 6 Don Valley & Sheffield maps 35 Chemicals 56 Other foods 6 South Yorkshire map 36-7 Upholstery 57 Maltings 7 7 ENGINEERING AND Tanning 57 Breweries 7 VEHICLES 38 Paper 57 Snuff 8 Engineering 38 Printing 58 Woodlands and timber 8 Ships and boats 40 12 GAS, ELECTRICITY, 3 COAL 9 Railway vehicles 40 SEWERAGE Coal settlements 14 Road vehicles 41 Gas 59 4 OTHER MINERALS AND 8 CUTLERY AND Electricity 59 MINERAL PRODUCTS 15 SILVERWARE 42 Water 60 Lime 15 Cutlery 42 Sewerage 61 Ruddle 16 Hand forges 42 13 TRANSPORT Bricks 16 Water power 43 Roads 62 Fireclay 16 Workshops 44 Canals 64 Pottery 17 Silverware 45 Tramroads 65 Glass 17 Other products 48 Railways 66 5 IRON 19 Handles and scales 48 Town Trams 68 Iron mining 19 9 EDGE TOOLS Other road transport 68 Foundries 22 Agricultural tools 49 14 MUSEUMS 69 Wrought iron and water power 23 Other Edge Tools and Files 50 Index 70 Further reading 71 USING THIS BOOK South Yorkshire has a long history of industry including water power, iron, steel, engineering, coal, textiles, and glass. -

Photography Competition

Institution of Civil Engineers Yorkshire and Humber Photography Competition 2017 In 2018 the Institution of Civil Engineers (ICE) turns 200. Help us celebrate some of the civil engineering projects and schemes that have had the greatest impact on people’s lives over the past 200 years. The ICE Yorkshire and Humber photography competition is a showcase for the very best digital photography of the built environment in in the region and is open to both professional and amateur photographers. All the shortlisted entries will be used in a web gallery and form part of an exhibition in public spaces around the region, giving acknowledgements where they are used. There are also three cash prizes. How to enter To be in with a chance of winning, select one or more subjects from either of the lists of civil engineering projects below, and submit your image(s). Please see full conditions of entry. Does the image suitably capture the subject and emphasise the impact it has had on people’s lives? You may also wish to consider elements such as lighting, focus, composition and use of colour. Shortlisted entries will be displayed in a public exhibition, celebrating 200 years of civil engineering. Cash prizes to be won. Entry closes: 31 October 2017 Conditions of entry 1 Entry is open to ICE members and non-members. 2 The subject must be selected from either of the lists of projects below. 3 Images should be a minimum of 1,500x2,000 pixels, submitted in jpg format and named as follows: Name of image_first name of photographer_lastname.jpg e.g. -

Magna 34 2Pp Brochure.Q:Layout 1

To Let Warehouse/Industrial unit 29,543 sq ft unit 2 - magna 34 | Sheffield Road | Templeborough | S60 1DX unit 2 - magna 34 Coronation Bridge Bessemer Park AY W NA MAG Blackburn Meadows Fusion At MAGNA 34 I Magna C BUSINESS PARK K EMPLE RD L Halfpenny T E Bridge SHEF S FIEL D RO W AD A6178 A Y Locks Bottom A6178 M1 Locks FERRARS ROAD D OA M R Meadowhall S Templeborough E A A D D N O U W D Chapel Flat Dike ST LAWRENCE ROAD H MEADOWHALL A L SHOPPING L CENTRE W A Y ORBOROUGH RD Golf Course N Leisure Reservoirs Centre G R 34 A N G E L A631 A N HIGHGATE E Sheffield Road | Templeborough | S60 1DX VE A6178 I R D SHEFFIELD H IG LE ERN Location M1 F The property is located in Rotherham, South Yorkshire approximately 5 miles north east of Sheffield and has an urban population of 257,800. It benefits from excellent transport links in the form of the M1 and M18. The M1 provides direct access to the North (Leeds and Wakefield) and South (Nottingham, Milton Keynes and London). In Terms addition, the M18, accessed at Junction 32 of the M1, provides access to the Humberside Ports. The premises are available to let by way of a new lease on FRI terms to be agreed. An estate service Situation charge is also payable under the terms. The property is situated on the successful Magna Business Park development approx. 1.0 mile from J34 M1 giving excellent connectivity to Yorkshire, the Midlands and, via Rateable Value the M18 and M62, to the Humberside ports. -

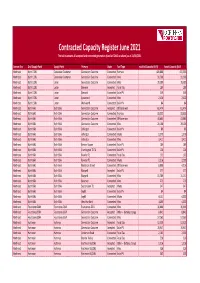

June 2021 This Table Contains All Accepted and Connected Generation (Sized at 72Kva Or Above) As at 31/06/2021

Contracted Capacity Register June 2021 This table contains all accepted and connected generation (sized at 72kVA or above) as at 31/06/2021 Licence Area Grid Supply Point Supply Point Primary Status Fuel Type Installed Capacity (kVA) Export Capacity (kVA) Northeast Blyth 132kV Generation Customer Generation Customer Connected Biomass 420,000 400,000 Northeast Blyth 132kV Generation Customer Generation Customer Connected Wind 31,500 31,500 Northeast Blyth 132kV Linton Generation Customer Connected Wind 78,580 78,580 Northeast Blyth 132kV Linton Denwick Accepted Fossil Gas 189 189 Northeast Blyth 132kV Linton Denwick Connected Solar PV 349 349 Northeast Blyth 132kV Linton Lynemouth Connected Wind 2,420 2,420 Northeast Blyth 132kV Linton Warkworth Connected Solar PV 84 84 Northeast Blyth 66kV Blyth 66kV Generation Customer Accepted Offshore wind 61,474 61,474 Northeast Blyth 66kV Blyth 66kV Generation Customer Connected Biomass 33,333 33,333 Northeast Blyth 66kV Blyth 66kV Generation Customer Connected Offshore wind 43,684 43,684 Northeast Blyth 66kV Blyth 66kV Generation Customer Connected Wind 28,106 28,106 Northeast Blyth 66kV Blyth 66kV Ashington Connected Solar PV 80 80 Northeast Blyth 66kV Blyth 66kV Ashington Connected Waste 1,379 1,379 Northeast Blyth 66kV Blyth 66kV Ashington Connected Wind 3,411 3,411 Northeast Blyth 66kV Blyth 66kV Benton Square Connected Solar PV 189 189 Northeast Blyth 66kV Blyth 66kV Cramlington T2 T4 Connected Solar PV 126 126 Northeast Blyth 66kV Blyth 66kV Fawdon T1 Connected Fossil Gas 135 135 Northeast -

Waterways & Standing Water

Waterways & Standing Water Headlines • Sheffield’s rivers and the quality of their waters have undergone vast improvements in recent decades, resulting in a substantial increase in biodiversity. • The current ecological status of Sheffield’s rivers is variable; assessments conducted by the Environment Agency show that most stretches are of an overall moderate status. Quality improves with increasing distance from central industrialised areas. • Otter and several fish species have now returned to the Don as a result of improving water quality and the installation of fish passes. Twenty-six out of 31 species of fish historically found on the Don have now recolonised the river. • Reservoirs, such as Redmires, have proved hugely important for many species of breeding birds including curlew, golden plover and snipe. • Local ponds provide important habitats for species such as great crested newts and dragonflies and many have benefitted from recent restoration work. Dragonfly diversity has significantly increased, partly due to improvements in water quality and associated emergent waterside vegetation. • Threats to Sheffield’s waterways and wetlands include pollution, physical modification of the river and invasive species. Non-native invasive species which have a stronghold on Sheffield’s river systems include Japanese knotweed, Himalayan balsam, signal crayfish and American mink. • Several organisations are involved in the ownership and management of the waterways and there are successful examples of partnership working. Key non-native invasive plants are the focus of ongoing conservation management aimed to control their spread. European otter © Andy Rouse/2020VISION 49 Introduction As a historically industrial city, Sheffield has always been known as a City of Rivers 1. -

Blackburn Meadows Wastewater Treatment Works

35 Int. J. Water, Vol.X, No. X, pp. XXX, XXX Blackburn Meadows wastewater treatment works Rui Lima Gab. 23, lnstituto Politécnico de Bragança, Escola Superior de Tecnologia e de Gestão, Campus de Santa Apolónia, Apartado 134, 5301-857 Bragança, Portugal. E-mai1: [email protected] Robert Bachmann Department of Chemical and Process Engineering, Sheffield University, Mappin Street, Sheffield, S1 3JD, UK. E-mail: [email protected] Abstract: Blackbum Meadows wastewater treatment works is situated in Sheffield, the fourth largest city in England, in the county of South Yorkshire. This treatment plant has a fluidized bed incinerator in order to treat and dispose the sludge. This paper gives a brief overview of the various stages and processes involved in effluent treatment at Blackbum Meadows and assesses the sludge disposal operation. Keywords: Sewage treatment plant; sludge dewatering; sludge incineration; wastewater. Reference to this paper should be made as follows: Lima, R. and Bachmann, R. (2002) 'Blackbum Meadows wastewater treatment works', Int. J. Water, Vol. 2, No. I, pp. 35-39. 1 Introduction The Blackburn Meadows works is one of the largest in South Yorkshire and discharges treated sewage from a population of 444,000 into the River Don. The present dry weather flow (DWF) is 136,000 m3 per day, which is more than the rate of flow in the River Don upstream of the discharge in dry weather. The incoming sewage comes from the Don Valley interceptor sewer, Tinsley and Blackburn Valley. 2 The new Don Valley interceptor sewer The original combined sewerage system that ran through Sheffield had become overloaded due to an increase in population, increased water consumption and increased industrial activity. -

Paper 12 Ed Bramley.Pdf

WFD – Taking the next step forward in joined up thinking Ed Bramley Environmental Regulation Manager, Yorkshire Water, Western House, Halifax Rd., Bradford, West Yorkshire, BD6 2LZ Tel No: 01274 804 095 Email: [email protected] Introduction The River Don is the main river in South Yorkshire - rising in the Pennines, and flowing eastwards for 70 miles, through the major conurbation of Sheffield. In the late 1980’s, the Don was one of the most polluted rivers in Europe – mainly as a result of discharges from sewage treatment works and the sewerage system, the many steel foundries in the area and the coal mining and processing industries. Over the last 25 years, the Don has been transformed into a largely clean river that supports a thriving fish population. There are even occasional sightings of salmon in the lower reaches of the river. And yet, the river remains fragile. In July 2006, following a summer thunderstorm after a hot dry spell, there was a major fish kill on the river. Questions were asked in Parliament as a result. The Environment Agency is still recording episodes of poor water quality downstream of the main Sheffield sewage works. To understand why there is still occasional poor water quality in the river Don, including the root causes of the fish kill, and what might be done to prevent a repetition, Yorkshire Water is carrying out a comprehensive study of the River Don. This will include significant fieldwork - allied to comprehensive modelling of the sewerage network, sewage treatment works and the river system in an integrated and detailed manner. -

M1 J28 to 35A Smart Motorway Updated Operating Regime Environmental Assessment Report (SGAR5)

M1 J28 to 35a Smart Motorway Updated Operating Regime Environmental Assessment Report (SGAR5) October 2015 1043319/ENV/PCF/2/001 Working on behalf of Highways England Document Control Document Title M1 J28 to 35a Smart Motorway Updated Operating Regime Environmental Assessment Report Author Mouchel Owner Highways England Distribution Andy Kirk (Highways England, Project Manager) Phil Barton (Mouchel, Project Director) Bill Scourfield (Mouchel, Project Manager) M1 J28 to 35a Smart Motorway Mailbox All present on the Reviewer List Document Status Final Record of Issue Version Status Author Date Checked Date Authorised Date A Draft Various 01/07/14 R. Atuah 07/07/15 A. Thornhill 07/07/15 B Draft Various 13/07/15 R. Atuah 13/07/15 A. Thornhill 13/07/15 C Draft R. Atuah 13/08/15 R. Atuah 13/08/15 A. Thornhill 13/08/15 D Draft R. Atuah 17/08/15 R. Atuah 17/08/15 A. Thornhill 17/08/15 E Draft R. Atuah 28/09/15 R. Atuah 28/09/15 A. Thornhill 28/09/15 F Final R. Atuah 19/10/15 R. Atuah 19/10/15 A. Thornhill 19/10/15 Reviewer List Name Role Andy Kirk Highways England (Project Manager) Richard Bernhardt Highways England (Regional Environmental Advisor) Approvals Name Signature Title Date of Version Issue Tony Turton Project Senior Responsible Officer (SRO) The original format of this document is copyright to Highways England 1 This page is intentionally left blank. 2 Table of Contents 1 Introduction ............................................................................................................ 7 1.1 Project Overview ............................................................................................... 7 1.2 Need for an Environmental Assessment .......................................................... -

Sheffield & Rotherham DAB

Small-scale radio multiplex licence Application form – Part A (public) Name of applicant (i.e. the body corporate that will hold the licence): Sheffield & Rotherham DAB Ltd Multiplex licence area being applied for (note this must be a small-scale multiplex area currently being advertised by Ofcom): Sheffield & Rotherham Contact details for Ofcom: Name: Chris Hurst Email: [email protected] Address: 68 Carter Knowle Road, Sheffield, England, S7 2DX Publication date: 1 September 2020 Small-scale radio multiplex licence: application form (Part A) 2 Extent of proposed coverage area 2.1 Provide a summary, fully consistent with the more detailed information about transmission sites supplied separately in Part B, of the coverage area proposed to be achieved by your technical plan. This should include a description of the target area you are seeking to serve within the advertised licence area, and also any areas you are aiming to serve outside the advertised licence area for this small-scale radio multiplex service. (You may refer to your coverage prediction in the response you provide): Sheffield is the most geographically diverse city in England. It is roughly one third urban, one third rural and one third in the Peak District. The topography is famous for presenting challenges when it comes to broadcast coverage. Lying in the eastern foothills of the Pennines, the city nestles in a natural amphitheatre created by several hills and the confluence of five rivers. Accordingly, much of the city’s urban housing is built on hillsides, with the city centre beneath, isolated by a ring of hills. -

Supporting Information

Yorkshire Water Services Limited Blackburn Meadows Sludge Treatment Facility (STF) Application for Environmental Permit Variation March 2021 Permit Reference: EPR/CP3897LT/V005 Yorkshire Water Services Limited Blackburn Meadows Sludge Treatment Facility (STF) Application for Environmental Permit Variation March 2021 Permit Reference: EPR/CP3897LT/V005 Document Structure Non-technical Summary Section I: Environmental Permit Application Forms Part A Part C2 Part C3 Part F1 (including letter of authorisation) Section II: Technical Description Section III: Supporting Information Section IV: Figures Figure 1: Site Location Plan Figure 2: Installation Layout Figure 3: Principal Emission Points Figure 4: Drainage Plan Section V: Appendices Appendix 1: Relevant Offences Appendix 2: Technical Competence Appendix 3: ISO14001 certificate Appendix 4: Quality and Environmental Policy Appendix 5: Site Condition Report Appendix 6: BAT Assessment Appendix 7: Review of Air Quality Risk Assessment Appendix 8: Odour Impact Assessment Appendix 9: Noise Impact Assessment Appendix 10: Odour Management Plan Appendix 11: Secondary Containment Risk Assessment Application for Environmental Permit Variation Blackburn Meadows STF Sign-off Sheet Yorkshire Water Services Ltd Sign-off Sheet Project Name Environmental Permitting Support Project No 41527729 0301 Report Reference 41527729 0301 - 01 Revision Date Description Author Check Review 01 31/03/2021 FINAL E. Stewart P. Smith P. Duncan Disclaimer This document entitled Blackburn Meadows Sludge Treatment Facility (STF) Application for Environmental Permit Variation was prepared by Stantec for the account of Yorkshire Water (the “Client”). Any reliance on this document by any third party is strictly prohibited. The material in it reflects Stantec’s professional judgment considering the scope, schedule and other limitations stated in the document and in the contract between Stantec and the Client. -

Industrial Railway Record

INDUSTRIAL RAILWAY RECORD The Quarterly Journal of the INDUSTRIAL RAILWAY SOCIETY COMBINED INDEX SECOND EDITION Volumes 1 to 16 1962 – 2007 RECORD No.1 to No.189 Assembled & Edited by Vic Bradley On behalf of the Combo Index Production Team for the benefit of all readers of this magazine. CORRECTIONS, GLITCHES, ERRORS and OMISSIONS are kept to a minimum but may still inevitably occur in a work of this nature. If you spot anything that you think needs attention, PLEASE DO SEND details of this to us ideally by email addressed to v.bradley[at]virgin.net www.irsociety.co.uk IRRNDX20.doc updated 22-Mar-2008 INTRODUCTION and ACKNOWLEDGEMENTS This “Combo Index” has been assembled by combining the contents of the sixteen separate indexes originally created, for each individual volume, over a period of some 45 years by a number of different people each using different technologies. Only in recent times have computers been used for indexing but, even for these, the computer files could not be traced with the exception of those for volumes 14 to 16. It has therefore been necessary to create digital versions of 13 original indexes using “Optical Character Recognition” (OCR), which has not proved easy due to the relatively poor print, and extremely small text (font) size, of some of the indexes in particular. Thus the OCR results have required extensive proof-reading. Very fortunately, a team of volunteers to assist in the project appeared out of the E-mail Group Internet Chat Site which is hosted by the IRS, and a special thankyou is certainly due to Richard Bowen, David Kitching, Martin Murray, Ken Scanes and John Scotford who each handled OCR and proofing of several indexes, to complete digital recovery of the individual published index texts for Volumes 1 to 13.