Creating a European Skills Council for the Maritime Technology Sector” (2014-2016)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Evaluation of the Use of Recycled Vegetable Oil As a Collector Reagent in the Flotation of Copper Sulfide Minerals Using Seawater

recycling Article Evaluation of the Use of Recycled Vegetable Oil as a Collector Reagent in the Flotation of Copper Sulfide Minerals Using Seawater Felipe Arcos and Lina Uribe * School of Mining Engineering, University of Talca, Talca 3460000, Chile; [email protected] * Correspondence: [email protected]; Tel.: +56-220-1798 Abstract: Considering sustainable mining, the use of seawater in mineral processing to replace conventional water is an attractive alternative, especially in cases where this resource is limited. However, the use of this aqueous medium generates a series of challenges; specifically, in the seawater flotation process, it is necessary to adapt traditional reagents to the aqueous medium or to propose new reagents that achieve better performance and are environmentally friendly. In this research, the technical feasibility of using recycled vegetable oil (RVO) as a collector of copper sulfide minerals in the flotation process using seawater was studied. The study considered the analysis of the metallurgical indexes when different concentrations of collector and foaming reagent were used, considering as collectors the RVO, potassium amyl xanthate (PAX) and mixtures of these, in addition to the methyl isobutyl carbinol (MIBC) as foaming agent. In addition, it was evidenced that the best metallurgical indexes were achieved using 40 g/t of RVO and 15 g/t of MIBC, which corresponded to an enrichment ratio of 6.29, a concentration ratio of 7.01, a copper recovery of 90.06% and a selectivity index with respect to pyrite of 4.03 and with respect to silica of 12.89. Finally, in relation to the study of the RVO and PAX collector mixtures, it was found that a mixture of 60 g/t of RVO and 40 g/t of PAX in the absence of foaming agent presented the best results in terms of copper recovery (98.66%) and the selectivity index with respect to pyrite (2.88) and silica (14.65), improving Citation: Arcos, F.; Uribe, L. -

Greenhouse Gas Impact of Marginal Fossil Fuel Use

Greenhouse gas impact of marginal fossil fuel use Greenhouse gas impact of marginal fossil fuel use By: Arno van den Bos, Carlo Hamelinck Date: 12 November 2014 Project number: BIENL14773 © Ecofys 2014 by order of the European Oilseed Alliance (EOA), the European Biodiesel Board (EBB) and the European Vegetable Oil and Proteinmeal Industry (FEDIOL) ECOFYS Netherlands B.V. | Kanaalweg 15G | 3526 KL Utrecht| T +31 (0)30 662-3300 | F +31 (0)30 662-3301 | E [email protected] | I www.ecofys.com Chamber of Commerce 30161191 Summary Biofuels represent a major option to reduce greenhouse gas emissions from the transportation sector. When assessing the benefits of biofuels, they are compared to the fossil fuels they replace. In the framework of the European Renewable Energy Directive and the Fuel Quality Directive, this is done by comparing the lifecycle greenhouse gas emissions of biofuels to a ‘fossil comparator’. This fossil comparator is based on the average greenhouse gas intensity of fossil fuels brought on the EU transportation market. Unconventional oils such as extra heavy oil and bitumen (tar sands), kerogen oil (oil shale), light tight oil (shale oil), deep sea oil and synthetic products such as gas-to-liquids and coal-to-liquids, typically have higher carbon footprints than conventional oil mainly because the effort required to extract, refine and/or synthesize them is much larger than for conventional oil. As the share of these unconventional oil-based fuels gradually rises in the total fuel supply over time, the greenhouse gas footprint of the average fuel consumption also rises. Even for conventional oil production fields, because larger existing fields get depleted, the extraction efforts increase while smaller fields are taken in operation. -

Det Norske Veritas

DET NORSKE VERITAS Report Heavy fuel in the Arctic (Phase 1) PAME-Skrifstofan á Íslandi Report No./DNV Reg No.: 2011-0053/ 12RJ7IW-4 Rev 00, 2011-01-18 DET NORSKE VERITAS Report for PAME-Skrifstofan á Íslandi Heavy fuel in the Arctic (Phase 1) MANAGING RISK Table of Contents SUMMARY............................................................................................................................... 1 1 INTRODUCTION ............................................................................................................. 3 2 PHASE 1 OBJECTIVE..................................................................................................... 3 3 METHODOLOGY ............................................................................................................ 3 3.1 General ....................................................................................................................... 3 3.2 Arctic waters delimitation .......................................................................................... 3 3.3 Heavy fuel oil definition and fuel descriptions .......................................................... 4 3.4 Application of AIS data.............................................................................................. 5 3.5 Identifying the vessels within the Arctic.................................................................... 6 3.6 Identifying the vessels using HFO as fuel.................................................................. 7 4 TECHNICAL AND PRACTICAL ASPECTS OF USING HFO -

Innovative, Sustainable Processing Solutions for the Palm Oil Industry Stay Ahead

Alfa Laval in brief Alfa Laval is a leading global provider of specialized products and engineered solutions. Our equipment, systems and services are dedicated to helping customers to optimize the performance of their processes. Time and time again. We help our customers to heat, cool, separate and transport products such as oil, water, chemicals, beverages, foodstuffs, From fruit to food - and beyond starch and pharmaceuticals. Solutions Our worldwide organization works closely with customers in almost 100 countries to help them Innovative, sustainable processing solutions for the palm oil industry stay ahead. that add value In response to challenges facing players in the competitive palm oil milling, refining and fats modification industry, Alfa Laval has developed a range of innovative solutions that offer sustainable alternatives to traditional technology. The solutions have one thing in common – they add value. PFT00521EN 1208 D3 PRO, Aldec, MBR, PAPX, PANX, VHE ECO, CompaBloc, SoftColumn, SoftColumn Dual-Strip, SoftFlex, TocoBoost, Iso-Mix, Iso-Mix, VHE ECO, CompaBloc, SoftColumn, SoftColumn Dual-Strip, SoftFlex, TocoBoost, PANX, D3 PRO, Aldec, MBR, PAPX, trademarks owned by Alfa Laval Corporate AB, Sweden. (AGT) are Treatment Ageratec and Advanced Glycerol and owned by Alfa Laval Corporate AB, Sweden. © 2012 Laval. Alfa Laval is a trademark registered Palm oil processing 2 A versatile partner who Maximum uptime Global services thinks outside the box for your operation - close to you Palm oil supply chain: The innovative Alfa Laval way to sustainable, high yield palm oil extraction, refining, fats modification and biodiesel production t Wherever you are, Alfa Laval’s palm oil competence centres, sales offices and service centres are never far away Micronutrients eatmen tion Enrichment processes Tocotrienols tr ca erol erifi t yc st gl v. -

Vegetable Oil Processing

Pollution Prevention and Abatement Handbook WORLD BANK GROUP Effective July 1998 Vegetable Oil Processing Industry Description and Practices to 5,000 mg/l). Seed dressing and edible fat and oil processing generate approximately 10–25 m3 The vegetable oil processing industry involves of wastewater per metric ton (t) of product. Most the extraction and processing of oils and fats from of the solid wastes (0.7–0.8 t/t of raw material), vegetable sources. Vegetable oils and fats are which are mainly of vegetable origin, can be pro- principally used for human consumption but are cessed into by-products or used as fuel. Molds also used in animal feed, for medicinal purposes, may be found on peanut kernels, and aflatoxins and for certain technical applications. The oils may be present. and fats are extracted from a variety of fruits, seeds, and nuts. The preparation of raw materi- Pollution Prevention and Control als includes husking, cleaning, crushing, and con- ditioning. The extraction processes are generally Good pollution prevention practices in the indus- mechanical (boiling for fruits, pressing for seeds try focus on the following main areas: and nuts) or involve the use of solvent such as hexane. After boiling, the liquid oil is skimmed; Prevent the formation of molds on edible after pressing, the oil is filtered; and after solvent materials by controlling and monitoring air extraction, the crude oil is separated and the sol- humidity. vent is evaporated and recovered. Residues are Use citric acid instead of phosphoric acid, conditioned (for example, dried) and are repro- where feasible, in degumming operations. -

Influence of Vegetable Oils on Ph Profile During Processing Of

cess Pro ing d & o o T F e c f h o a a a oo Poe eo 2 n l o a l n o r Journal of Food DOI: 10.4172/2157-7110.1000756 g u y o J Processing & Technology ISSN: 2157-7110 Research Article Open Access Influence of Vegetable Oils on pH Profile during Processing of Semidry Fermented Buffalo Meat Sausage Irfan Khan1 and Saghir Ahmad2* Department of Post-Harvest Engineering and Technology, Aligarh Muslim University, Aligarh, Uttar Pradesh, 202002, India Abstract The experiments were conducted to deduce the effect of lactic acid fermentation and smoking on the pH of semidry fermented Buffalo meat sausage incorporated with different vegetable oils viz., Canola oil, Safflower oil and olive oil with levels of 15%, 20%, 25% individually. The aim was to replace the buffalo white fat with the different levels of vegetable oils (Canola oil, Safflower oil and olive oil) to make a product healthier for human beings as the taken vegetable oils contain good amount of monounsaturated fatty acids, polyunsaturated fatty acids, tocopherols, phytosterols and polyphenols. As the problems related to overdose of saturated fat become prevalent in the society particularly in urban people viz., cardiovascular diseases (atherosclerosis, arteriosclerosis), type-2 diabetes mellitus, polycystic ovary etc. Three samples with each vegetable oil were prepared by taking 15%, 20% and 25% substitution level in the laboratory. The fermentation of Buffalo meat sausage was performed with the bacterial strains of Lactobacillus plantarum MTCC 1407 and Lactobacillus brevis MTCC1750 in the batch process at 22°C temperature for 48 hrs. -

Innovation in Processing & Reformulation of Vegetable Oils & Fats

FEDIOL Nutrition Factsheet Innovation in processing and reformulation of vegetable oils and fats Within the global context of health, diet and physical activity, the vegetable oils and fats sector is actively working on healthy solutions for the EU food market . Despite different national diets in the EU, which present I lowering Trans Fatty Acids (TFA), a variety of challenges for reformulating options, I lowering Saturated Fatty Acids (SAFA) and the industry has worked over the last 10 years towards I increasing Mono- and Polyunsaturated Fatty Acids achieving the following goals : (MUFA, PUFA) Evolution of the vegetable oils and fats content in TFA, SAFA, PUFA and MUFA from 1998-2008 45 The vegetable oils and fats industry is committed to 40 35 deliver formulations with an improved nutritional 30 s i s a 25 b profile to the food industry t a 20 F % 15 I Significant improvements have been achieved in 10 the last 10 years in reducing TFA and SAFA, and 5 0 increasing MUFA and PUFA 1998 2003 2008 Years I The vegetable oils and fats industry and food ––– MUFA ––– PUFA ––– SAFA ––– TFA producers have to overcome technical challenges Results to deliver food products with the same I The average TFA content in vegetable oils and fats functionalities and sensory properties has decreased over the last 10 years from 5.3 to 1% on fat basis, which corresponds to a relative decrease I Raw materials and innovative processes are in of 81%. constant development with a clear cost impact I A slight increase of SAFA can be observed from The vegetable oils and fats industry will continue 1998 to 2003, followed by a decrease from 2003 to 2008 reaching 27.3% of total fat. -

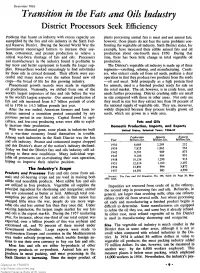

Transition in the Fats and Oils Industry

December 1958 Transition in the Tats and Oils Industry District Processors Seek Efficiency Problems that haunt an industry with excess capacity are plants processing animal fats is meat and not animal fats, exemplified by the fats and oils industry in the Sixth Fed however, those plants do not face the same problems con eral Reserve District. During the Second World War the fronting the vegetable oil industry. Sixth District states, for Government encouraged farmers to increase their soy example, have increased their edible animal fats and oil bean, cottonseed, and peanut production to relieve a production about one-fourth since 1950. During that critical war-born shortage of fats and oils. Processors time, there has been little change in total vegetable oil and manufacturers in the industry found it profitable to production. buy more and better equipment to handle the larger sup The District’s vegetable oil industry is made up of three plies. Researchers worked unceasingly to find substitutes segments—crushing, refining, and manufacturing. Crush for those oils in critical demand. Their efforts were suc ers, who extract crude oil from oil seeds, perform a dual cessful and many states over the nation found new oil operation in that they produce two products from the seeds crops—the bread of life for this growing industry. —oil and meal. Sold principally as a high protein feed Phenomenal growth records were made in vegetable for animals, meal is a finished product ready for sale on oil production. Nationally, we shifted from one of the the retail market. The oil, however, is in crude form, and world’s largest importers of fats and oils before the war needs further processing. -

Assessment of Vessel Requirements for the U.S. Offshore Wind Sector

Assessment of Vessel Requirements for the U.S. Offshore Wind Sector Prepared for the Department of Energy as subtopic 5.2 of the U.S. Offshore Wind: Removing Market Barriers Grant Opportunity 24th September 2013 Disclaimer This Report is being disseminated by the Department of Energy. As such, the document was prepared in compliance with Section 515 of the Treasury and General Government Appropriations Act for Fiscal Year 2001 (Public Law 106-554) and information quality guidelines issued by the Department of Energy. Though this Report does not constitute “influential” information, as that term is defined in DOE’s information quality guidelines or the Office of Management and Budget's Information Quality Bulletin for Peer Review (Bulletin), the study was reviewed both internally and externally prior to publication. For purposes of external review, the study and this final Report benefited from the advice and comments of offshore wind industry stakeholders. A series of project-specific workshops at which study findings were presented for critical review included qualified representatives from private corporations, national laboratories, and universities. Acknowledgements Preparing a report of this scope represented a year-long effort with the assistance of many people from government, the consulting sector, the offshore wind industry and our own consortium members. We would like to thank our friends and colleagues at Navigant and Garrad Hassan for their collaboration and input into our thinking and modeling. We would especially like to thank the team at the National Renewable Energy Laboratory (NREL) who prepared many of the detailed, technical analyses which underpinned much of our own subsequent modeling. -

Guidelines for the Selection and Operation of Jack-Ups in the Marine Renewable Energy Industry

www.RenewableUK.com Guidelines for the Selection and Operation of Jack-ups in the Marine Renewable Energy Industry Issue 2: 2013 RUK13-019-02 2 Industry guidance aimed at jack-up owners operators, developers and contractors engaged in site-investigation, construction, operation and maintenance of offshore wind and marine energy installations. Acknowledgements RenewableUK acknowledges the time, effort, experience and expertise of all those who have contributed to this document. This Issue 2 of these guidelines was prepared for RenewableUK by London Offshore Consultants. This was in consultation with key consultees listed at the end of this document, RenewableUK members and key industry stakeholders. Status of this Document RenewableUK Health and Safety Guidelines are intended to provide information on particular technical, legal or policy issues relevant to the core membership base of RenewableUK. Their objective is to provide industry-specific guidance, for example where current information could be considered absent or incomplete. Health and Safety Guidelines are likely to be subject to review and updating, and so the latest version of the guidelines must be referred to. Attention is also drawn to the disclaimer below. Disclaimer The contents of these guidelines are intended for information and general guidance only, and do not constitute advice, are not exhaustive and do not indicate any specific course of action. Detailed professional advice should be obtained before taking or refraining from action in relation to any of the contents of this guide, or the relevance or applicability of the information herein. RenewableUK is not responsible for the content of external websites included in these guidelines and, where applicable, the inclusion of a link to an external website should not be understood to be an endorsement of that website or the site’s owners (or its products/services). -

UMITED STATES DEPARTMENT of AÖRICULTURE Agriculture

UMITED STATES DEPARTMENT OF AÖRICULTURE Agriculture Information Bulletin No. 37 Washingtffli, D. C. Issued April 1951 LISTS OF PUBLICATIONS AND PATENTS BUREAU OF AGRICULTURAL AND INDUSTRIAL CHEMISTRY AGRICULTURAL RESEARCH ADMINISTRATION U. S. DEPARTMENT OF AGRICULTURE Issued during fiscal year ended June 30, 1950 Compiled By T. D. Jarrell / CONTENTS Page PUBLICATIONS Northern Regional Research Laboratory ...... 1 Southern Regional Research Laboratory •«•... • • . • • 4 Eastern Regional Research Laboratory •«•••.••••••...••• 9 Western Elegional Research Laboratory • . • . • . « * • . • • • • • . 16 Agricultural Chemical Research Division ................. 20 Naval Stores Research Division ••••••••• 22 Enzyme Research Division • • • • . • • . ... • . • • .••... 23 Pharmacology Laboratory . • • . • . .... • • . • . • • .24 Fruit and Vegetable Chemistry Laboratory ..•.••••••..•••• 25 Natural Rubber Extracticm and Processing Investigations . ... 25 Allergen Research Division 26 Microbiology itesearch Division ........ 26 Biologically Active Chemical Conçounds Division .26 General . 27 UltlTED STATES PATEÎIT8 29 Further information on the jmblications listed herein may be obtained by writing to the division or laboratory concerned. PUBLICATIONS NORTHERN REGIONAL RESEARCH LAB(»ATORY 825 North University Street Peoria 5, Illinois RESEARCH Evaluation of fibrous agricultural residues for structural building board prod- ucts* III, A process for the manufacture of high-grade products from wheat straw. By E. C. Lathrop and T. R. Naffziger. TAPPI (Tech. Assoc. Pulp and Paper Indus.) 32(7): 319-330, 1949. Agricultural residues in plastics. III. Evaluation of residue flours as fillers in thermosetting phenolics. By T. F. Clark. Mod. Plastics 26(12): 111-116, 164«165. 1949. Agricultural residue flours as extenders in phenolic resin glues for plywood. By R. V. Williamson and E. C. Lathrop. Mod. Plastics 27(2): 111-112, 169-170, 172, 174. 1949. Hop vines for paper. By H. -

Emerging Vegetable Oils in Europe

CBI Product Factsheet: Emerging vegetable oils in Europe CBI | Market Intelligence Product Factsheet Cloves in Germany | 1 Introduction The drive for innovation in the European food industry leads companies to adopt new ingredients in order to remain competitive. The introduction of new vegetable oils (emerging oils), either as ingredients or as final consumer products, is a form of innovation, differentiation and marketing used by food companies to articulate their competitive edge. On the other side of the coin, exporters of emerging oils still face a number of challenges to access the European market successfully. Whereas the Novel Food Regulation imposes marketing restrictions on a number of innovative products, some barriers to suppliers are often related to issues such as supply sufficiency and stability. At the same time, emerging oils also provide opportunities in terms of niche marketing and value adding propositions. Understanding the European market for emerging vegetable oils Innovation is high on the agenda of food manufacturers in Europe, significantly in North-Western Europe. In order to remain competitive, companies invest heavily in Research & Development (R&D), with the goal of adapting products to ever-changing consumer preferences, food health and safety requirements and introducing novelty into the food market. A large part of this strategy consists in finding new ingredient solutions. Vegetable oils are an integral part of several food products and, as such, are an interesting basis for product development. The introduction of new vegetable oils, either as ingredients or as final consumer products, is a form of innovation, differentiation and marketing used by food companies to articulate their competitive edge.