Global League Tables Introduction

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Crowdfunding in Asia

Crowdfunding in Asia May 2018 Introducing the first free directory of crowdfunding platforms across Asia. The data is based on the AlliedCrowds Capital Finder, a database of over 7,000 alternative finance capital providers across emerging markets. Our data has been used by organizations like FSD Asia, UNDP, World Green Economy Organization, GIZ, World Bank, and others in order to provide unique, actionable insights into the world of emerging market alternative finance. This is the latest of our regular reports on alternative finance in emerging markets; you can find all previous reports here. Crowdfunding rose in prominence in the post-financial crisis years (starting in 2012), and for good reason: a global credit crunch limited the amount of funding available to entrepreneurs and small businesses. Since then, crowdfunding has grown rapidly around the world. Crowdfunding is especially consequential in countries where SMEs find it difficult to raise capital to start or grow their businesses. This is the case in many Asian countries; according to the SME Finance Forum, there is a $2.3 trillion MSME credit gap in East Asia and the Pacific. Crowdfunding can help to fill this gap by offering individuals and small businesses an alternative source of capital. This can come in the form of donation-based as well as lending-based (peer-to-peer or peer-to-business) crowdfunding. In order to help entrepreneurs and small business owners to find the crowdfunding platform that’s right for them, we are releasing the first publicly available list of all crowdfunding platforms across Asia. The report is split into two key sections: the first one is an overview of crowdfunding platforms, and how active they are across the largest markets on the continent. -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

Bankrupt Subsidiaries: the Challenges to the Parent of Legal Separation

ERENSFRIEDMAN&MAYERFELD GALLEYSFINAL 1/27/2009 10:25:46 AM BANKRUPT SUBSIDIARIES: THE CHALLENGES TO THE PARENT OF LEGAL SEPARATION ∗ Brad B. Erens ∗∗ Scott J. Friedman ∗∗∗ Kelly M. Mayerfeld The financial distress of a subsidiary can be a difficult event for its parent company. When the subsidiary faces the prospect of a bankruptcy filing, the parent likely will need to address many more issues than simply its lost investment in the subsidiary. Unpaid creditors of the subsidiary instinctively may look to the parent as a target to recover on their claims under any number of legal theories, including piercing the corporate veil, breach of fiduciary duty, and deepening insolvency. The parent also may find that it has exposure to the subsidiary’s creditors under various state and federal statutes, or under contracts among the parties. In addition, untangling the affairs of the parent and subsidiary, if the latter is going to reorganize under chapter 11 and be owned by its creditors, can be difficult. All of these issues may, in fact, lead to financial challenges for the parent itself. Parent companies thus are well advised to consider their potential exposure to a subsidiary’s creditors not only once the subsidiary actually faces financial distress, but well in advance as a matter of prudent corporate planning. If a subsidiary ultimately is forced to file for chapter 11, however, the bankruptcy laws do provide unique procedures to resolve any existing or potential litigation between the parent and the subsidiary’s creditors and to permit the parent to obtain a clean break from the subsidiary’s financial problems. -

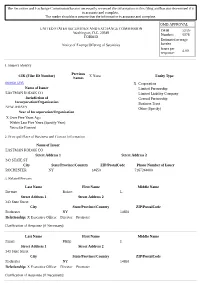

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W. -

Funds Raised in Q2 2016

www.buyoutsnews.com July 11, 2016 | BUYOUTS | 59 FUNDS RAISED IN Q2 2016 The following list represents funds raised by U.S.-based LBO and mezzanine firms in 2016. The list is compiled by Buyouts’ staff from a variety of sources, including news reports, press releases, Securities and Exchange Commission filings, and conversations with general and limited partners. Buyouts attempted to contact firms on the list. The amounts below are the most current figures we could obtain at press time. Funds in black are closed. Funds in red remain open, to our knowledge. If you have any questions or comments about this list, please send them to Paul Centopani, at [email protected]. Sponsor Name of Fund Fund Type Amount Amount Target ($M) Placement Agent Legal Counsel Raised Raised- in 2015 to-Date ($M) ($M) Aberdeen Asset Aberdeen Energy & Resources Acquisitions/Buyouts (Industry 225 Management Partners IV, L.P. Focus: Energy/Power) ACON Investments ACON Equity Partners IV, L.P. Acquisitions/Buyouts 578.2 1,070 Evercore Advent International Advent Global Private Equity VIII Acquisitions/Buyouts 12,100.0 13,000.0 12,000 AE Industrial Partners AE Industrials Partners Fund I, L.P. Growth Equity (Industry Focus: 680.0 680.0 600 Eaton Partners Gibson Dunn & Industrials) (Debut Fund) Crutcher LLP Alliance Consumer Alliance Consumer Growth Fund Growth Equity (Industry Focus: 210.8 210.8 Kramer Levin Growth III LP Consumer Products/Services) Naftalis & Frankel Altaris Capital Partners Altaris Health Partners III LP Acquisitions/Buyouts 425 Alvarez -

Powering the Crowd Into the Future

POWERING THE CROWD INTO THE FUTURE KEY LEARNINGS & RECOMMENDATIONS Davinia Cogan, Peter Weston POWERING THE CROWD INTO THE FUTURE KEY LEARNINGS & RECOMMENDATIONS FOR ENERGY ACCESS CROWDFUNDING AND P2P LENDING CONTENTS BIOS 3 EXECUTIVE SUMMARY 4 INTRODUCTION 6 1 STATE OF THE MARKET 8 2 THE 6 CAMPAIGN ARCHETYPES 12 1. PARTNERSHIP MODELS 15 CASE STUDY: TAHUDE FOUNDATION 16 2. ONE-OFF FUNDRAISERS 17 CASE STUDY: RAFODE 19 CASE STUDY: SOLARIS OFFGRID 20 3. MEGA-CAMPAIGNS 22 4. P2P MICROLENDING 23 CASE STUDY: EMERGING COOKING SOLUTIONS 24 5. ONLINE DEBT-BASED SECURITIES 26 CASE STUDY: SIMUSOLAR 27 CASE STUDY: AZURI TECHNOLOGIES 29 5.EQUITY CROWDFUNDING 31 CASE STUDY: TRINE 32 3 INTERVENTIONS TO CATALYSE FUNDING 34 4 CROWD POWER UPDATE 37 CONCLUSION 39 REFERENCES 41 This material has been funded by UK aid from the UK government; however the views expressed do not necessarily reflect the UK government’s official policies. Published December 2018 Design: www.dougdawson.co.uk Front cover by C.Schubert BIOS Davinia Cogan Peter Weston Davinia Cogan is the Programme Peter Weston is the Director of Manager of Crowd Power at Energy Advisory Services at Energy 4 Impact. 4 Impact. She runs the UK aid He manages a team of consultants funded programme, which explores that advises off-grid SMEs in Sub the role of incentives to stimulate Saharan Africa and helps them to donation, reward, debt and equity implement new business models crowdfunding in the off-grid energy and technologies. He is an expert sector in Sub- Saharan Africa and in power, renewables and off- South Asia. -

DENVER CAPITAL MATRIX Funding Sources for Entrepreneurs and Small Business

DENVER CAPITAL MATRIX Funding sources for entrepreneurs and small business. Introduction The Denver Office of Economic Development is pleased to release this fifth annual edition of the Denver Capital Matrix. This publication is designed as a tool to assist business owners and entrepreneurs with discovering the myriad of capital sources in and around the Mile High City. As a strategic initiative of the Denver Office of Economic Development’s JumpStart strategic plan, the Denver Capital Matrix provides a comprehensive directory of financing Definitions sources, from traditional bank lending, to venture capital firms, private Venture Capital – Venture capital is capital provided by investors to small businesses and start-up firms that demonstrate possible high- equity firms, angel investors, mezzanine sources and more. growth opportunities. Venture capital investments have a potential for considerable loss or profit and are generally designated for new and Small businesses provide the greatest opportunity for job creation speculative enterprises that seek to generate a return through a potential today. Yet, a lack of needed financing often prevents businesses from initial public offering or sale of the company. implementing expansion plans and adding payroll. Through this updated resource, we’re striving to help connect businesses to start-up Angel Investor – An angel investor is a high net worth individual active in and expansion capital so that they can thrive in Denver. venture financing, typically participating at an early stage of growth. Private Equity – Private equity is an individual or consortium of investors and funds that make investments directly into private companies or initiate buyouts of public companies. Private equity is ownership in private companies that is not listed or traded on public exchanges. -

Private Equity Confidence Survey Central Europe Winter 2018 This Publication Contains General Information Only

Caution returns Private Equity Confidence Survey Central Europe Winter 2018 This publication contains general information only. The publication has been prepared on the basis of information and forecasts in the public domain. None of the information on which the publication is based has been independently verified by Deloitte and none of Deloitte Touche Tohmatsu Limited, any of its member firms or any of the foregoing’s affiliates (collectively the “Deloitte Network”) take any responsibility for the content thereof. No entity in the Deloitte Network nor any of their affiliates nor their respective members, directors, employees and agents accept any liability with respect to the accuracy or completeness, or in relation to the use by any recipient, of the information, projections or opinions contained in the publication and no entity in Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies thereon. Caution returns | Private Equity Confidence Survey Central Europe Introduction The Central European (CE) private equity (PE) market Croatia and Lithuania are all expected to grow at second fund on €21m, putting it well on its way to its may be reverting to its usual pace of activity following under 3.0%. €55m target after launching in January. A new fund a prolonged period of large exits and fundraisings as has been launched for the Baltics, with Lithuanian well as strong levels of deal-doing. While we remain Exit activity continues apace, with the headline-hitting asset manager Invalda INVL seeking €200m for its confident conditions remain conducive to transacting, homeruns of 2017 giving way to a steadier flow of INVL Baltic Sea Growth Fund to back Baltic businesses respondents are hinting at some caution as we enter mid-market exits dominated by local players. -

Midwest M&A Quarterly Update

Midwest M&A Quarterly Update Second Quarter 2012 Bridgepoint Merchant Banking is a division of Bridgepoint Holdings, LLC. Securities offered through an unaffiliated entity, M&A Securities Group, Inc., member FINRA/SIPC Second Quarter 2012 Midwest M&A Quarterly Update Bridgepoint Midwest M&A Index Bridgepoint Midwest M&A Index Increased To All-Time High in Q2-12 . Index Summary: The Bridgepoint Midwest M&A Index, a measure of corporate merger and acquisition activity in the U.S. Midwest region, increased 3.3% in Q2-12 after increasing 18.7% in Q1-12. On a year-over-year basis, the index increased 22.0% from Q2-11. The latest increase put the index at an all-time high of 119.5 (Q3-06 = 100), up from the previous high reached in Q1-12 of 116.3 . Perspective: Index reflects continued healthy growth of Midwest M&A deal volumes in the face of a relatively stable local economy. Current index level of 119.5 reflects a continued rally from the . Deal volumes previous quarter, which was the highest index level What the Index Means for You: have continued to grow, with increased attention on since its inception. Q2-12 deal volume was also companies with strong performance. The current very strong on a seasonal basis as the year-over- environment represents an attractive opportunity for year index increase of 22.0% represented the Midwest companies and business owners to: highest change since Q3-10. Besides deal volume growth, median Midwest M&A deal size and Evaluate strategic options & your company valuation (on a TEV/EBITDA basis) also increased value – Midwest companies are receiving from $12.00mm and 5.4x in Q1-12 to $14.9mm and strong M&A interest from both sponsors 8.5x in Q2-12, respectively and other corporates with performing companies garnering premium valuations . -

Including League Tables of Financial Advisors

An Acuris Company Finding the opportunities in mergers and acquisitions Global & Regional M&A Report 2019 Including League Tables of Financial Advisors mergermarket.com An Acuris Company Content Overview 03 Global 04 Global Private Equity 09 Europe 14 US 19 Latin America 24 Asia Pacific (excl. Japan) 29 Japan 34 Middle East & Africa 39 M&A and PE League Tables 44 Criteria & Contacts 81 mergermarket.com Mergermarket Global & Regional Global Overview 3 M&A Report 2019 Global Overview Regional M&A Comparison North America USD 1.69tn 1.5% vs. 2018 Inbound USD 295.8bn 24.4% Outbound USD 335.3bn -2.9% PMB USD 264.4bn 2.2x Latin America USD 85.9bn 12.5% vs. 2018 Inbound USD 56.9bn 61.5% Outbound USD 8.9bn 46.9% EMU USD 30.6bn 37.4% 23.1% Europe USD 770.5bn -21.9% vs. 2018 50.8% 2.3% Inbound USD 316.5bn -30.3% Outbound USD 272.1bn 28.3% PMB USD 163.6bn 8.9% MEA USD 141.2bn 102% vs. 2018 Inbound USD 49.2bn 29% Outbound USD 22.3bn -15.3% Ind. & Chem. USD 72.5bn 5.2x 4.2% 17% 2.6% APAC (ex. Japan) USD 565.3bn -22.5% vs. 2018 Inbound USD 105.7bn -14.8% Outbound USD 98.9bn -24.5% Ind. & Chem. USD 111.9bn -5.3% Japan USD 75.4bn 59.5% vs. 2018 Inbound USD 12.4bn 88.7% Global M&A USD 3.33tn -6.9% vs. 2018 Outbound USD 98.8bn -43.6% Technology USD 21.5bn 2.8x Cross-border USD 1.27tn -6.2% vs. -

BC Partners London Paris Milan Hamburg Geneva New York AGENDA

GREECE: The Ne w Reform Agenda Investment & Business Opportunities in Greece A Global Investor’s Perspective Nikos Stathopoulos 30th October, 2008 New York City BC Partners London Paris Milan Hamburg Geneva New York AGENDA Greece as an investment destination Case Studies Conclusions BC Partners London Paris Milan Hamburg Geneva New York Private Equity is a Major Player in European M&A European LBO Activity as a % of all European M&A value 2007 BC Partners London Paris Milan Hamburg Geneva New York BC Partners: a Leading Global Private Equity Fund – 1 BC Funds Investments by Sector Investment in 67 companies since foundation in 1986 ̶ Total transaction value of US$100bn Automotive Health 6% Retail ̶ Invested in 13 countries in Europe, US and Asia 8% 23% ̶ Current portfolio companies representing an aggregate turnover Media/Telecom of US$30bn and employing 81,000 employees 11% Service Consumer 14% goods Over US$17bn ra ise d in e ig ht f un ds 19% ̶ Fund VIII with US$9.3bn of equity Industry 19% ̶ Up to US$2.4bn equity for single transaction available plus International Presence additional equity from BC funds co-investors ̶ Average transaction value of investments of US$3.1bn since 2000 New York/ (from US$141m to US$29.9bn) London London Presence in Europe and the US Hamburg ̶ Offices in London, Paris, Milan, Geneva, Hamburg, and New York Paris ̶ 50 investment professionals with broad individual experience Geneva Milan BC Partners London Paris Milan Hamburg Geneva New York BC Partners: a Leading Global Private Equity Fund – 2 Selected -

LIFE at KKR We Are Investors

LIFE AT KKR We are investors. But we're more than that. IT'S IN OUR DNA We're collaborative team players who are curious communities. We often measure success over about the world around us. We're passionate about years, not quarters. We value integrity in all that we always learning more and pushing to be better. do, whether it's presenting numbers accurately or Here, we're never finished growing or discovering being open and honest with a portfolio company new ideas. executive. People want to do business with those they like and trust. It's a mantra instilled in all of us People want to do business from the top down. with those they like and trust As a firm we manage investments across multiple asset classes and as individuals we are encouraged to think creatively to solve problems, explore opportunities, take on new responsibilities and challenges, put our clients first and contribute to our LIFE AT KKR | 2 We are investors. But we're more than that. Culture & Work Environment For over 40 years, our At KKR, you'll find a team of curious, driven, dedicated and intelligent professionals who enjoy working together. We all work collaborative approach hard to create a friendly environment that encourages asking continues to drive our culture questions and reaching out to others. Teamwork Entrepreneurial Spirit Integrity No matter where you sit in the Some of our best ideas come from It's at the heart of everything we do organization, you have the full giving people the time to explore, from our internal interactions to resources, network, skills and research and have conversations.