Los Angeles 4Q17 Office Market

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Greater Los Aneles Office Q4 2020

M A R K E T B E AT GREATER LOS ANGELES Office Q4 2020 YoY 12-Mo. ECONOMIC OVERVIEW: Slow Recovery, Record Job Losses in 2020 and Vaccine Optimism Chg Forecast Although total nonfarm employment in Los Angeles County increased by 29,800 in November and has since made up 47.6% of the job deficit sustained in March and April, it remained below year-ago levels with every industry sector posting job reductions. With 17.9% the loss of 386,100 jobs in the last year (-8.3%), Los Angeles County’s unemployment rate rose from 4.3% in November 2019 to Vacancy Rate 11.0% in November 2020. Sectors that fuel the demand for office space posted significant declines with the professional and business services contracting by 47,000 jobs, the information sector losing 36,400 jobs and the educational and health services -4.5M sector posting the lost of 37,900 jobs. Net Abs. YTD, SF SUPPLY: Office Inventory Rises at Year-end and Asking Rental Rates Not Indicative of the Market The Greater Los Angeles’ (GLA) current office inventory of 205.9 million square feet (msf) has increased by 2.2 msf from this time last $3.62 year, with 27 office buildings added throughout 2020. There are more than 6.7 msf of new office projects (Under Construction/Under Asking Rent, PSF Renovation) still under way, LA Central and LA West lead the market with 2.0 msf and 2.9 msf respectively. While demand remains (Overall psf/mo, All PropertyClasses) uncertain in the near future and more available space hits the market, it is expected that most new developments would be on hold until later in 2021. -

Land Use Element Designates the General Distribution and Location Patterns of Such Uses As Housing, Business, Industry, and Open Space

CIRCULATION ELEMENT CITY OF HAWTHORNE GENERAL PLAN Adopted April, 1990 Prepared by: Cotton/Beland/Associates, Inc. 1028 North Lake Avenue, Suite 107 Pasadena, California 91104 Revision Table Date Case # Resolution # 07/23/2001 2001GP01 6675 06/28/2005 2005GP03 & 04 6967 12/09/2008 2008GP03 7221 06/26/2012 2012GP01 7466 12/04/2015 2015GP02 7751 TABLE OF CONTENTS Section Page I. Introduction to the Circulation Element 1 Purpose of this Element 1 Relation to Other General Plan Elements 1 II. Existing Conditions 2 Freeways 2 Local Vehicular Circulation and Street Classification 3 Transit Systems 4 Para-transit Systems 6 Transportation System Management 6 TSM Strategies 7 Non-motorized Circulation 7 Other Circulation Related Topics 8 III. Issues and Opportunities 10 IV. Circulation Element Goals and Policies 11 V. Crenshaw Station Active Transportation Plan 23 Circulation Element March 1989 LIST OF FIGURES Figure Page Figure1: Street Classification 17 Figure 2: Traffic Volume Map 18 Figure 3: Roadway Standards 19 Figure 4: Truck Routes 20 Figure 5: Level of Service 21 LIST OF TABLES Table 1: Definitions of Level-of-Service 22 Circulation Element March 1989 SECTION I - INTRODUCTION TO THE CIRCULATION ELEMENT Circulation and transportation systems are one of the most important of all urban systems in determining the overall structure and form of the areas they service. The basic purpose of a transportation network within the City of Hawthorne is the provision of an efficient, safe, and serviceable framework which enables people to move among various sections of the city in order to work, shop, or spend leisure hours. -

Los Angeles/Orange/Riverside/San Bernardino/Ventura Los Angeles County Cities

Southern California Regional Energy Network Los Angeles/Orange/Riverside/San Bernardino/Ventura Los Angeles County Cities Alhambra ...................................................................................................................................................... 9 Compton ...................................................................................................................................................... 9 Canoga Park ................................................................................................................................................. 9 Carson ........................................................................................................................................................... 9 Cerritos ......................................................................................................................................................... 9 Chatsworth ................................................................................................................................................... 9 Compton ...................................................................................................................................................... 9 Culver City ..................................................................................................................................................... 9 El Monte ...................................................................................................................................................... -

BEACH CITIES SWIMMING Parent Handbook “Building World Class Character Through Excellence in Swimming”

BEACH CITIES SWIMMING Parent Handbook “Building World Class Character through Excellence in Swimming” TABLE OF CONTENTS ORGANIZATIONAL STRUCTURE OF BEACH CITIES SWIMMING ........................................................................ 3 TRYOUTS ......................................................................................................................................................................... 3 ABOUT OUR COACHES ................................................................................................................................................. 3 BCS FEES AND PAYMENT POLICIES ......................................................................................................................... 4 QUARTERLY DUES ...................................................................................................................................................... 4 ANNUAL REGISTRATION FEE ................................................................................................................................... 4 USA SWIMMING REGISTRATION FEE ..................................................................................................................... 4 SWIM MEET FEE .......................................................................................................................................................... 4 RELAY FEE ................................................................................................................................................................... -

Production Studio for Lease in Playa Vista

Production Studio For Lease in Playa Vista 5419 McConnell Avenue Mark Berman Les Small O: 310-785-2000 O: 310-785-2000 C: 310-713-1323 C: 310-785-2200 [email protected] [email protected] DRE 01013402 DRE 00692938 5419 McConnell Ave | Playa Vista PREMISES 30,010 SF (not divisible) USE Formerly used by a major motion picture production company, it has state-of-the-art soundstages, virtual production stage, two screening rooms, editing bays, sound booths, etc. RENT Negotiable, modified gross OCCUPANCY Immediate TERM 1 – 10 years PARKING 68 new restriped parking spaces outside your door at $150 per space, per month. Lot conducive for valet parking for additional spaces (Landlord may be able to provide up to 5:1000 parking) CEILING HEIGHT Up to 23’ LOADING 3 Dock High, 1 Ground Level 5419 McConnell Ave | Playa Vista Specs LARGE SCREENING ROOM • Size: 19’ 3 “ x 10’ 10” (1.78:1) • Precision White Screen 1.4 Gain SMALL SCREENING ROOM • Size: 12’ 6 “ x 7’ 1” (1.78:1) • Precision White Screen 1.4 Gain VIRTUAL PRODUCTION STAGE Size: 54’ x 69’ with 18’6” ceiling height POWER • 600 amps 3 phase service (equipped for 1200 amps electrical capability with city utility upgrade to building) • Additional 3 new transformers with conduit and feeders ready to be pulled down when new switchboard is installed, if needed • 14 new 277V and 120V electrical panels • 5 new 200A breakers in existing switch gear HVAC • Recent upgrade of existing units and addition of 12 units • Editorial, stage, and screening room areas utilize line ducting to reduce noise WIRING • Fiber and CAT6 throughout with enough conduit to add or remove additional runs • 10GB Sohonet Fiber with a 1GB Back-Up Sohonet Fiber 5419 McConnell Ave | Playa Vista 1st Floor Plan 5419 McConnell Ave | Playa Vista 2nd Floor Plan 5419 McConnell Ave | Playa Vista Location Marina del Rey Playa Vista Minutes away from the 405 and 90 freeways, and a 10-minute drive to LAX. -

2018 Press Release

5th Annual Digital Entertainment World Features Speakers from Facebook, Apple, Netflix, YouTube, Microsoft & Disney Digital Media Wire’s annual event includes 2,000 decision-makers across video, music, games and advertising, startups, innovators, technologists and press at 2018 DEW, Feb. 5-6. LOS ANGELES, CA--(Marketwired - January 24, 2018) - Recognized by Hollywood insiders, digital influencers and industry leaders throughout the world as a "must-attend" event, now in its 5th year Digital Entertainment World (DEW) is where you want to be if you are in the business of creating or monetizing digital entertainment content. DEW 2018 focuses on "The FUTURE of..." and will cover topics from OTT to Innovation to eSports to Content Marketing to VR/AR to Music Rights to Startups, etc., as this theme guides the talks, discussions, meetings and presentations over the two days. This year's event will be held in the hip and modern Marina del Rey Marriott just steps from the beach and located in the heart of LA's thriving Silicon Beach with easy access to Santa Monica, Venice and Playa Vista. The event includes keynotes, fireside chats, presentations, panel discussions, tech demos, startup competition, innovative exhibitions, daily DJ music and performers and the best networking in the hotel's Sinder Lounge. "2018 DEW focuses on the most important developments shaping entertainment and media today from media consolidation to cord cutting to the challenges facing digital publishers," said Ned Sherman, DEW Chair and Counsel & Director of Manatt Digital. "By bringing together the key stakeholders at the intersection of content and technology, we provide a first-class platform for deal making and partnership development." DEW includes more than 75 unique sessions and 200 speakers on topics essential to the future of video, music, brands, marketing, gaming, AR/VR, and AI. -

Ocean Front Walk Creative Office Investment Opportunity in the Heart of Venice Beach

1007-1017 OCEAN FRONT WALK CREATIVE OFFICE INVESTMENT OPPORTUNITY IN THE HEART OF VENICE BEACH Holliday Fenoglio Fowler, L.P., acting by and through Holliday GP Corp., a real estate broker licensed with the California Department of Real Estate, License Number 01385740 PROPERTY SUMMARY HFF has been engaged as the Exclusive Advisor to extend to 1011-1017 qualified investors the opportunity to acquire the fee simple and leasehold interests in 1007-1017 Ocean Front Walk, Venice, California (the “Property” or “Ocean Front Walk”). The Property is comprised of a two-story, 10,778 square foot creative office and retail building that is owned fee simple, and an adjacent one story 2,811 square foot building and 24 surface parking space lot (leasehold). This location offers beach front views, an excellent live-work environment, extensive local amenities, strong economic fundamentals driven by the tech explosion in Silicon Beach and ample executive housing along the coast of the Westside. PROPERTY OVERVIEW PROPERTY OVERVIEW 1007-1009 Ocean Front Walk 1011-1017 Ocean Front Walk Address Venice, CA 90291 Address Venice, CA 90291 Building Size 2,811 SF Building Size 10,8778 SF Year Built 1987 Year Built 1921 Stories 1 Stories 2 Leased % 100% Leased % 73% Parking 24 Surface Spaces Parking 0 Surface Spaces “Silicon Beach” is now one of the heaviest concentrations of technology Interest Owned Leasehold (18 Years Remaining) Interest Owned Fee Simple and startup companies in the world. THE OPPORTUNITY INVESTMENT HIGHLIGHTS Ocean Front Walk represents the rare HIGH-TECH opportunity to acquire a truly creative office HIGHLY DESIRABLE opportunity in the heart of Venice Beach, one OFFICE LOCATION TENANT DEMAND of the top performing markets in Southern Rivaled only by submarkets within San Francisco Venice is synonymous with “new economy” California. -

Flood Insurance Study Number 06037Cv001b

VOLUME 1 OF 4 LOS ANGELES COUNTY, CALIFORNIA AND INCORPORATED AREAS Community Community Community Community Community Community Community Community Name Number Name Number Name Number Name Number LOS ANGELES COUNTY, UNINCORPORATED 065043 DIAMOND BAR, CITY OF 060741 LAWNDALE, CITY OF* 060134 SAN DIMAS, CITY OF 060154 AREAS SAN FERNANDO, CITY AGOURA HILLS, CITY OF 065072 DOWNEY, CITY OF 060645 LOMITA, CITY OF* 060135 060628 OF* ALHAMBRA, CITY OF* 060095 DUARTE, CITY OF 065026 LONG BEACH, CITY OF 060136 SAN GABRIEL, CITY OF* 065055 ARCADIA, CITY OF 065014 EL MONTE, CITY OF* 060658 LOS ANGELES, CITY OF 060137 SAN MARINO, CITY OF* 065057 ARTESIA, CITY OF* 060097 EL SEGUNDO, CITY OF 060118 LYNWOOD, CITY OF 060635 SANTA CLARITA, CITY OF 060729 SANTA FE SPRINGS, CITY AVALON, CITY OF 060098 GARDENA, CITY OF 060119 MALIBU, CITY OF 060745 060158 OF MANHATTAN BEACH, CITY AZUSA, CITY OF 065015 GLENDALE, CITY OF 065030 060138 SANTA MONICA, CITY OF 060159 OF BALDWIN PARK, CITY OF* 060100 GLENDORA, CITY OF 065031 MAYWOOD, CITY OF* 060651 SIERRA MADRE, CITY OF 065059 HAWAIIAN GARDENS, BELL GARDENS, CITY OF 060656 065032 MONROVIA, CITY OF 065046 SIGNAL HILL, CITY OF* 060161 CITY OF* SOUTH EL MONTE, CITY BELL, CITY OF* 060101 HAWTHORNE, CITY OF* 060123 MONTEBELLO, CITY OF 060141 060162 OF* HERMOSA BEACH, CITY BELLFLOWER, CITY OF 060102 060124 MONTEREY PARK, CITY OF* 065047 SOUTH GATE, CITY OF 060163 OF SOUTH PASADENA, CITY BEVERLY HILLS, CITY OF* 060655 HIDDEN HILLS, CITY OF 060125 NORWALK, CITY OF 060652 065061 OF* HUNTINGTON PARK, CITY BRADBURY, CITY -

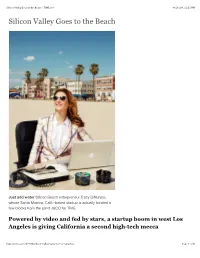

Silicon Valley Goes to the Beach | TIME.Com 4/16/14, 12:35 PM

Silicon Valley Goes to the Beach | TIME.com 4/16/14, 12:35 PM Silicon Valley Goes to the Beach Just add water Silicon Beach entrepreneur Tracy DiNunzio, whose Santa Monica, Calif.–based startup is actually located a few blocks from the sand JUCO for TIME Powered by video and fed by stars, a startup boom in west Los Angeles is giving California a second high-tech mecca http://time.com/57159/silicon-valley-goes-to-los-angeles/ Page 1 of 6 Silicon Valley Goes to the Beach | TIME.com 4/16/14, 12:35 PM The second-floor office of Tradesy, a 16-month-old online consignment shop, has all the requisite trappings of a digital startup. Inside an open, loftlike space, seven 20- somethings work at a central pod of desks near an L-shaped kitchen stocked with free snacks and drinks. Employees’ dogs scamper beneath their feet while a team of programmers, eyes glued to computer screens, huddles in a separate room. But there is a giveaway clue that Tradesy isn’t based in Silicon Valley or one of the dozens of other tech hubs that have taken root from Austin to Omaha: a deck off the kitchen is piled with surfboards. From there, the Pacific Ocean and the wide white- sand beach of Santa Monica, Calif., is about 300 yards away–easy walking distance when the waves are breaking. “We have two things we hold dear here,” says Tradesy co-founder and CEO Tracy DiNunzio, 35. “Catered food delivered for all meals and being close to the ocean.” Such is life in Silicon Beach, a stretch of roughly four miles from Venice to Santa Monica that has become the heart of Los Angeles’ fast-growing tech scene. -

Beach Bluffs Restoration Project Master Plan

Beach Bluffs Restoration Project Master Plan April 2005 Beach Bluffs Restoration Project Steering Committee Ann Dalkey and Travis Longcore, Co-Chairs Editor’s Note This document includes text prepared by several authors. Julie Stephenson and Dr. Antony Orme completed research and text on geomorphology (Appendix A). Dr. Ronald Davidson researched and reported South Bay history (Appendix B). Sarah Casia and Leann Ortmann completed biological fieldwork, supervised by Dr. Rudi Mattoni. All photographs © Travis Longcore. GreenInfo Network prepared maps under the direction of Aubrey Dugger (http://www.greeninfo.org). You may download a copy of this plan from: http://www.urbanwildlands.org/bbrp.html This plan was prepared with funding from California Proposition 12, administered by the California Coastal Conservancy and the Santa Monica Bay Restoration Commission through a grant to the Los Angeles Conservation Corps and The Urban Wildlands Group. Significant additional funding was provided by a grant from the City of Redondo Beach. Preferred Citation Longcore, T. (ed.). 2005. Beach Bluffs Restoration Project Master Plan. Beach Bluffs Restoration Project Steering Committee, Redondo Beach, California. 2 Beach Bluffs Restoration Project Table of Contents Executive Summary .......................................................................................................... iii Introduction .........................................................................................................................5 Goals.....................................................................................................................................6 -

Why Silicon Beach Bros Are Buying in Brentwood 6:30 AM PDT 11/4/2017 by Peter Kiefer

Why Silicon Beach Bros Are Buying in Brentwood 6:30 AM PDT 11/4/2017 by Peter Kiefer Courtesy of HILTON & HYLAND This $38.5 million South Burlingame estate is listed by Hilton & Hyland's Drew Fenton. L.A.'s digital jet set migrates north for space, privacy and a respite from anti-tech sentiment: "No one wants to be picketed." The borders of Silicon Beach loosely extend to Venice Beach, Santa Monica and Playa del Rey, where the L.A. area's largest tech employers — Google, Yahoo, Snap and Riot Games — have set up shop the past decade. But when Snap founder Evan Spiegel put down personal roots, the Silicon Beach wunderkind (credited with either transforming or destroying Venice, where Snap is headquartered, depending on whom you ask) settled on a ZIP code that struck many observers as counterintuitive. With wife Miranda Kerr, the 27-year-old plunked down $12 million last year for a Gerard Colcord-designed estate just below the Getty Museum in Brentwood. With the Silicon Beach tech community now in its adolescence (Google announced its move to Venice seven years ago) and adjacent real estate surging to record per-square-foot highs amid dwindling inventory, a trend has taken hold: Tech titans are leaving Santa Monica condos and Venice bungalows in the rearview mirror of their Teslas as they head to the quiet calm offered by Brentwood. "My prediction all along was that they would end up coming to Brentwood," says the Agency's Santiago Arana, who has brokered multiple deals in the neighborhood for tech moguls. -

Rossi Offering Memorandum

1026 Manhattan Beach Blvd, Manhattan Beach CA 90266 Manhattan Beach For more information: Mike Rossi BRE: 01089100 Commercial Investments Cell: 310.849.9601 [email protected] ©2015, NW Real Estate, Inc. We obtained the information above from sources we believe to be reliable. However, we have not verified its accuracy and make no guarantee, warranty, or representation about it. It is submitted subject to the possibility of errors, omissions, change of price, rental or other condition, prior sale, lease or financing or withdrawal without notice. We include projections, opinions, assumptions or estimates for example only, and they may not represent current or future performance of the property. You and your tax and legal advisors should conduct your own investigation of the property and transaction. Offering Memorandum Commercial Opportunity NW Real Estate Brokers Offered at $2,299,000.00 This beautiful mid-century commercial building Offering is an exceptional opportunity to purchase and enjoy as an owner/user, passive investment, or start over and construct your own new building. The property is located on popular Manhattan Beach Blvd which experiences approximately 22,600 cars per day traveling in and out of downtown Manhattan Beach and is just west of Sepulveda Blvd. The property’s two current tenants are on month to month tenancies and 2 - 3 units are vacant and the ground floor space is configured to easily divide the space into two separate units. The rear of the property lies a large private parking lot with direct access off Manhattan Beach Blvd with a southern exposure. Please contact the City of Manhattan Beach for information regarding zoning or any other development/use questions.