Electronic Banking Models

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Q. How Do I Enroll for Online Banking? A. You May Access Our Website at and in the Top Right Corner There Is an Orange Box for Online Banking

Q. How do I enroll for Online Banking? A. You may access our website at www.guarantystate.com and in the top right corner there is an orange box for Online Banking. Under the User ID box there is a link that says “Enroll for Online Banking”. Clicking the link will open a new webpage where you will be prompted to confirm your identity which must match what we have on file, create your sign-on and review your information. Should you have any problems, don’t hesitate to contact us at any of our locations. Q. Is there a fee for Online Banking? A. No, Online Banking is available free of charge to all Guaranty State Bank & Trust Company customers. Q. Is Online Banking safe? A. Guaranty State Bank & Trust Company uses state-of-the-art firewalls and security to protect client accounts and identities. We do this by: • Using Secured Socket Layer (SSL) data encryption. • Requiring clients to use a browser with 128-bit encryption. • Never displaying Social Security Numbers over the Internet. • Automatically disconnecting Online Banking sessions after 10 minutes of inactivity. • Requiring a unique Online Banking ID and password to be entered before access is granted to account information. • Utilizing a Password Security System. To keep unauthorized individuals from accessing client accounts by guessing their password, we have instituted a password lockout system. If a password is entered incorrectly three consecutive times, the user is “locked out” of the system. • “Out-of-band Authentication” which manages what computer you access your online banking from and should the IP address change, you will be required to enter a 5 digit code that will either be sent by phone call or text message. -

Word Files Coverted

About MasterCard International: MasterCard International is a leading global payments solutions company that provides a broad variety of innovative services in support of their global members' credit, deposit access, electronic cash, business-to-business and related payment programs. MasterCard international manages a family of well-known, widely accepted payment cards brands including MasterCard®, Maestro®, and Cirrus® and serves financial institutions, consumers and businesses in over 210 countries and territories. What is a Debit Card: Maestro® is the Global Debit Card cum ATM Card product of MasterCard International. This card can be used to make on-line bill payments through 49,000 Point of Sale (POS) terminals in India and 70,00,000 merchant establishments worldwide exhibiting “MAESTRO” logo. In other words the Debit Card holder can pay their bills, at shops exhibiting “Maestro” Logo, using this card instead by cash or cheque. The card holder need not carry cash in future when all the shops provide this facility. SIB's Debit Card can also be used as an ATM card within the ATM network of the Bank. People around the world prefer debit card over credit card since the spending can be restricted to what they have in their account. Since payment is effected only if there is available balance in the customer's account, it is absolutely risk-free for the banks. SIB plans to issue debit cards liberally as an added convenience to its customers which in turn reduces the pressure on cash transactions at the counters. How is CIRRUS relevant to other bank's Maestro Card holders: SIB has acquired “CIRRUS”, the product of MasterCard International. -

(Automated Teller Machine) and Debit Cards Is Rising. ATM Cards Have A

Consumer Decision Making Contest 2001-2002 Study Guide ATM/Debit Cards The popularity of ATM (automated teller machine) and debit cards is rising. ATM cards have a longer history than debit cards, but the National Consumers League estimates that two-thirds of American households are likely to have debit cards by the end of 2000. It is expected that debit cards will rival cash and checks as a form of payment. In the future, “smart cards” with embedded computer chips may replace ATM, debit and credit cards. Single-purpose smart cards can be used for one purpose, like making a phone call, or riding mass transit. The smart card keeps track of how much value is left on your card. Other smart cards have multiple functions - serve as an ATM card, a debit card, a credit card and an electronic cash card. While this Study Guide will not discuss smart cards, they are on the horizon. Future consumers who understand how to select and use ATM and debit cards will know how to evaluate the features and costs of smart cards. ATM and Debit Cards and How They Work Electronic banking transactions are now a part of the American landscape. ATM cards and debit cards play a major role in these transactions. While ATM cards allow us to withdraw cash to meet our needs, debit cards allow us to by-pass the use of cash in point-of-sale (POS) purchases. Debit cards can also be used to withdraw cash from ATM machines. Both types of plastic cards are tied to a basic transaction account, either a checking account or a savings account. -

Challenges in Privacy and Security in Banking Sector and Related Countermeasures

International Journal of Computer Applications (0975 – 8887) Volume 144 – No.3, June 2016 Challenges in Privacy and Security in Banking Sector and Related Countermeasures Zarka Zahoor Moin Ud-din Karuna Sunami Jamia Hamdard University Jamia Hamdard University Jamia Hamdard University Jamia Hamdard Jamia Hamdard Jamia Hamdard New Delhi 110062, India New Delhi 110062, India New Delhi 110062, India ABSTRACT Given the competitive nature of banking environment, along With the extensive use of technology particularly internet by with the significant value of the resources they manage, users, banking is becoming more dependent on technology. business and technology organizations must take all steps Unfortunately, with this the cyber-crimes related to banks are necessary to protect their assets. A compromise of these also increasing stupendously. The tendency of cyber security information assets could have a severe impact on the bank, attacks aimed at financial sector is much high than any other bank customers, form a violation of laws and regulations and sector. Some of the common cyber security attacks aimed at negatively affect the reputation and financial stability of the banks include Phishing, Cross site scripting, Cyber-squatting, bank. Botnets, Spoofing, etc. This causes a tremendous loss of The Banking industry has been exposed to a large number of money to the customer and bank, declines bank’s reputation cyber-attacks on their data privacy and security such as frauds and decreases the trust that users place in a bank. with online payments, ATM machines, electronic cards, net Banks are obligated to provide a safe online banking banking transactions, etc. The average number of attacks environment to its users. -

User Manual-Mobile Banking Service- SMS Banking Please Note

User Manual-Mobile Banking Service- SMS Banking Please note : The messages sent through this channel are stored in the sent items folder in the message box in the customer’s handset. To avoid a possible misuse, the customers are requested to delete such messages. Features Enquiry of balance in the account Mini Statement – last five transactions Transfer of Funds -Mobile to Mobile Money Transfer through IMPS Mobile Top up DTH Top up/ Recharge Top up of Mobile Wallet Registration for the Service (It may please be noted that the key words are not case sensitive) Get User ID Send SMS <MBSREG >to 9223440000 You will get a User ID and default MPIN. Change MPIN – It is mandatory for the customer to change the MPIN before visiting the ATM/Branch Send following SMS to 9223440000 for changing MPIN: <Smpin><UserId><Old Mpin><New Mpin> You will receive SMS – “Your MPIN is changed”. It is desirable to change MPIN at regular intervals or whenever there is an apprehension that secrecy has been lost. Register at ATM You will be required to register for the service on ATM or at your Branch. Please ensure that you have changed your MPIN before registering at the ATM. Go to ATM and after swiping your Debit Card choose Mobile Registration–Enter your ATM PIN- Mobile Banking – Registration – Enter your mobile number.- Choose yes after ensuring the correctness of the entry- Then the Mobile Number entered by you is displayed- Choose Confirm. You will get a SMS regarding successful registration. In this process of registration, the Primary Account linked to the ATM card is enabled for Mobile Banking Service. -

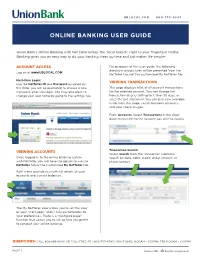

Online Banking User Guide

UBLOCAL.COM 800-753-4343 ONLINE BANKING USER GUIDE Union Bank’s Online Banking with Net Teller brings the “local branch” right to your fi ngertips! Online Banking gives you an easy way to do your banking, frees up time and just makes life simpler. ACCOUNT ACCESS For purposes of this user guide, the following directions and pictures will be presented from the Log on at www.UBLOCAL.COM NetTeller tab, not the customized My NetTeller tab. First-time Login: VIEWING TRANSACTIONS Use the NetTeller ID and Password assigned by the Bank; you will be prompted to choose a new This page displays a list of all account transactions Password after you login. You may also elect to for the selected account. You can change the change your user name by going to the settings tab. transaction display setting to 7, 15 or 30 days, or since the last statement. You can also view available funds from this page, switch between accounts, and view check images. From Accounts, Select Transactions in the drop- down menu next to the account you wish to access. VIEWING ACCOUNTS Transaction Search: Select Search from the Transaction submenu. Once logged-in to the online banking system Search by date, debit, credit, dollar amount, or with NetTeller, you will have the option to use the check number. NetTeller tab or the customized My NetTeller tab. Both views provide you with full details of your accounts and current balances. The My NetTeller view allows you to set this view as your “start page” and is fully customizable to your preferences. -

CSCIP Module 5 - Payments and Financial Transactions Final - Version 3 - October 8, 2010 1 for CSCIP Applicant Use Only

Module 5: Smart Card Usage Models – Payments and Financial Transactions Smart Card Alliance Certified Smart Card Industry Professional Accreditation Program Smart Card Alliance © 2010 CSCIP Module 5 - Payments and Financial Transactions Final - Version 3 - October 8, 2010 1 For CSCIP Applicant Use Only About the Smart Card Alliance The Smart Card Alliance is a not-for-profit, multi-industry association working to stimulate the understanding, adoption, use and widespread application of smart card technology. Through specific projects such as education programs, market research, advocacy, industry relations and open forums, the Alliance keeps its members connected to industry leaders and innovative thought. The Alliance is the single industry voice for smart cards, leading industry discussion on the impact and value of smart cards in the U.S. and Latin America. For more information please visit http://www.smartcardalliance.org . Important note: The CSCIP training modules are only available to LEAP members who have applied and paid for CSCIP certification. The modules are for CSCIP applicants ONLY for use in preparing for the CSCIP exam. These documents may be downloaded and printed by the CSCIP applicant. Further reproduction or distribution of these modules in any form is forbidden. Copyright © 2010 Smart Card Alliance, Inc. All rights reserved. Reproduction or distribution of this publication in any form is forbidden without prior permission from the Smart Card Alliance. The Smart Card Alliance has used best efforts to ensure, but cannot guarantee, that the information described in this report is accurate as of the publication date. The Smart Card Alliance disclaims all warranties as to the accuracy, completeness or adequacy of information in this report. -

Fees and Limits Guide Information About the Fees, Charges and Transaction Limits That Apply to Heritage Deposit, Credit Card and Lending Products

Fees and Limits Guide Information about the fees, charges and transaction limits that apply to Heritage Deposit, Credit Card and Lending Products. Talk to us today. Effective 1 June 2021 HERITAGE BANK - FEES AND LIMITS GUIDE Issue Date: 1 June 2021 This booklet: • sets out the fees, charges and transaction limits that apply to Heritage Deposit Products; and • sets out the transaction limits that apply to the following Heritage Credit Card and Lending Products and forms part of the Credit Contract for each product: • Credit Card Products; • Mortgage Loans; • Personal Loans; • Line of Credit Facilities; and • Business Overdrafts. • sets out fees and charges that may become payable to Heritage Credit Card Products. The fees and charges that apply to Heritage’s Credit Card and Lending Products are contained in other documents applicable to the product. For more information about which documents make up the terms and conditions for the products contained in this booklet, please see the Guide to Heritage Deposit Products (Deposit Products), the Guide to Heritage Credit Card Products (Credit Cards) or the Heritage Lending Terms and Conditions (Mortgage Loans, Personal Loans, Line of Credit Facilities and Business Overdrafts) as applicable. 2 Fees and Limits Guide HERITAGE DEPOSIT PRODUCTS We do not charge account keeping fees. TRANSACTION FEES Simply Access (S1), Cash Management (S8) – no longer available for sale, Loan Offset (S9) – no longer available for sale, Mortgage Crusher (S10), Money Manager (S24) – no longer available for sale, Pension -

Unit V: Different Modes of Online Banking (11 Hours) Different Means of Remittances Demand Draft, Mail Transfer, Telegraphic and Telephonic Transfer Credit Card-A.T.M

Unit V: Different modes of online banking (11 Hours) Different means of remittances demand draft, Mail transfer, Telegraphic and Telephonic transfer Credit card-A.T.M. (Automated teller machine) Mobile banking -Home Banking- Inter linked branches banking –Online banking-computerization in banking field. Remittance Business Apart from accepting deposits and lending money, Banks also carry out, on behalf of their customers the act of transfer of money - both domestic and foreign.- from one place to another. This activity is known as "remittance business" . Banks issue Demand Drafts, Banker's Cheques, Money Orders etc. for transferring the money. Banks also have the facility of quick transfer of money also know as Telegraphic Transfer or Tele Cash Orders. In Remittance business, Bank 'A' at a place 'a' accepts money from customer 'C' and makes arrangement for payment of the same amount of money to either the customer 'C' or his "order" i.e. a person or entity, designated by 'C' as the recipient, through either a Branch of Bank 'A' or any other entity at place 'b'. In return for having rendered this service, the Banks charge a pre-decided sum known as exchange or commission or service charge. This sum can differ from bank to bank. This also differs depending upon the mode of transfer and the time available for effecting the transfer of money. Faster the mode of transfer, higher the charges. Demand Draft A demand draft or "DD" is an instrument most banks in India use for effecting transfer of money. It is a Negotiable Instrument. To buy a "DD" from a Bank, you are required to fill an application form which asks the following information : Type of instrument needed Name of the recipient Name of the sender Amount to be transferred Place where the transferred money is to be paid Mode in which money is to be paid i.e. -

An Integrated Approach for SMS Based Secure Mobile Banking in India Neetesh Saxena, Narendra S

An Integrated Approach for SMS Based Secure Mobile Banking in India Neetesh Saxena, Narendra S. Chaudhari Department of CSE, Indian Institute of Technology Indore, India Introduction: M-banking can be executed using various channels like SMS, USSD, GPRS, WAP and phone based Application. Most of the people (70% of the population) living in rural areas of India don’t have java enabled cell phones and Internet facility is also very limited through which WAP/GPRS based applications work. Nowadays, SMS is very popular and frequently used worldwide, however traditional SMS service does not provide any security to the transmitted message information. SMS based m-banking can be extended as a secure channel for users by enhancing the security of SMS. This concept of providing a secure channel can be implemented on a separate SIM. In India, most of the banks provide information retrieval services only and they don’t permit to do transaction using SMS banking. Only banks can provide the facility of m-banking in India while in some other countries like Kenya and Philippines non-bank organizations can also provide such facilities. Apart from this, some banks provide change password through SMS which is a threat as SMS is not encrypted while transmitted to bank server. Problem Statement: The main objective is to provide a secure mobile banking using SMS for the people who are living in the rural part of India and don’t have java support cellular phones and Internet facility. Presently, SMS is not secure and is in clear text without any ciphering mode while transmitting. -

OTP Encryption Techniques in Mobiles for Authentication and Transaction Security

ISSN(Online): 2320-9801 ISSN (Print): 2320-9798 International Journal of Innovative Research in Computer and Communication Engineering (An ISO 3297: 2007 Certified Organization) Vol. 2, Issue 10, October 2014 OTP Encryption Techniques in Mobiles for Authentication and Transaction Security Dr.AnanthiShesashaayee, D. Sumathy Associate Professor & Head, Department of Computer Science, Quaid E Millath Government College for Women, Chennai, Tamil Nadu, India Research Scholar, Department of Computer Science, Quaid E Millath Government College for Women, Chennai, Tamil Nadu, India ABSTRACT: The improvement and advancement in technology makes the modern day smart phones and PDAs moresophisticated .It has drastically changed the way in which we perform our m-banking transactions. When a client initiates a bank transaction, he is provided with an OTP which is sent to his registeredmobile number via SMS. The client sends back the OTP within a short period to complete the transaction. The OTP SMS is generated by the bank server and is handed over to the client’s mobile operator. To avoid any possible attacks like phishing, man-in-the- middle attack, malware Trojans, the OTP must be secured. In order to provide a reliable and secure mode of online transactions without any compromise to convenience, a reliable m-banking authentication scheme that combines the secret PIN with encryption of the one-time password (OTP) has been developed in this paper. The secret PIN known only between the client and the bank is used for encrypting the OTP. After the encrypted OTP SMS reaches the client’s mobile, the PIN is used again used for decrypting. -

Billing Service Code Consolidation Guide | Effective August 2016

Billing Service Code Consolidation Guide | Effective August 2016 Starting with your August 2016 statement, we are changing some of the service codes and service descriptions displayed on your Treasury Services Billing statement to provide consistent billing standards for all of your Treasury Services accounts. In addition, some services will appear under a different product category. A complete listing of these changes is provided in the table below. Changes are highlighted in red for easier identification. Please share this information with your technical team to determine if system updates are required. Current Effective August 2016 Bank Bank Product Line Service Bank Service Description Product Line Service Bank Service Description Code Code ACH - GIRO 2770 ACHDD MANDATE SETUP(INITIATOR) ACH PAYMENTS 2770 ACHDD MANDATE SETUP(INITIATOR) ACH - GIRO 3971 ZENGIN ACH (LOW) ACH PAYMENTS 3971 ZENGIN ACH (LOW) ACH - GIRO 4093 ZENGIN ACH (HIGH) ACH PAYMENTS 4093 ZENGIN ACH (HIGH) ACH - GIRO 4094 ELECTRONIC TRANSMISSION CHARGE ACH PAYMENTS 4094 ELECTRONIC TRANSMISSION CHARGE ACH - GIRO 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH PAYMENTS 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH - GIRO 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH PAYMENTS 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH - GIRO 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH PAYMENTS 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH - GIRO 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH PAYMENTS 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH - GIRO 4174 OUTWARD PYMT - GIRO (URGENT) 5 ACH PAYMENTS 4174 OUTWARD PYMT - GIRO (URGENT)