Report of the Comptroller and Auditor General of India on for The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

World Bank Document

h -- Public Disclosure Authorized gn,un,r- s' t .S *K t ' t~~~~~~~~~~-- i ll E il P \~~~t 4 1- ' Public Disclosure Authorized (na'g HS) zY Wm"y''''S.'f' ;', ', ''' '',''-' '~'0', t'' .SC:''''''''E 3'; , 'r' 6 ~ U Public Disclosure Authorized it ~ ~ ~ ~ ~ Public Disclosure Authorized OA 86b3 ' :~~~~~~~~~~~ TABLE OF CONTENTS 1. INTRODUCTORY BACKGROUND ................................................... 1-1 1.1. PROJECT BACKGROUND ................................................... 1-1 1.2. PROPOSED WORKS FOR BP1 -THE AIZAWL BYPASS . ..................................1-1 1.3. IMPACTS ENVISAGED AND THE CORRIDOR OF IMPACT . ..............................1-4 1.4. SCOPE OF ENVIRONMENTAL IMPACT ASSESSMENT ................................... 1-6 1.5. THE STUDY METHODOLOGY ................................................................... 1-6 1.6. STRUCTURE OF THE REPORT ................................................................... 1-7 2.' POLICY, LEGAL AND ADMINISTRATIVE FRAMEWORK . ..............................2-1 2.1. IMPLEMENTATION AND REGUALTORY AGENCIES .......................................................... 2-1 2.2. LEGAL FRAMEWORK AND THE ENVIRONMENTAL CLEARANCE STIPULATIONS ............ 2-1 2.3. GOI/GOM CLEARANCE REQUIREMENTS ..................................................................... 2-2 2.4. WORLD BANK REQUIREMENTS ..................................................................... 2-2 3. THE EXISTING ENVIRONMENT ..................................................................... 3-1 3.1. METEOROLOGICAL CONDITIONS -

Schedule-Ii: Village Profile (Khaw Dinhmun Tlangpui)

SCHEDULE-II: VILLAGE PROFILE (KHAW DINHMUN TLANGPUI) Khuaa Moto Highe Chung h r Naupang r Middl Prima PHE kaw APL BPL Lo nei High Sub_ electric kawn District Code Mipa Hmeichhia kum 14 Colle Secon e ry Hosp tui lak zawng SI No District Village/Veng hming Name of Block APL zat BPL zat mihring mihring chhungkaw Scho UHC CHC PHC Centr ity a gin Code No awm zat awm zat hnuai lam ge dary Schoo Scho ital a awm zawng awm zat awm zat awm zat ol e awm khua awm zat Schoo l ol em awm tawh a l zat em pawh 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 1 Kolasib 02 Bairabi N 01 Bilkhawthlir 806 103 0 0 1 6 6 0 0 0 1 0 yes yes yes 909 2 Kolasib 02 Bairabi South Bilkhawthlir 355 11 0 0 1 2 2 0 0 0 0 1 yes yes yes 366 3 Kolasib 02 Bilkhawthlir N 02 Bilkhawthlir 411 79 0 0 0 1 2 0 0 0 0 1 yes yes yes 490 4 Kolasib 02 Bilkhawthlir South 03 Bilkhawthlir 503 61 2610 234 1401 1443 118 767 0 1 1 2 3 0 0 0 1 1 yes yes yes 564 5 Kolasib 02 Buhchangphai 18 Bilkhawthlir 184 27 450 523 200 0 0 1 1 2 0 0 0 0 1 yes yes yes 221 6 Kolasib 02 Bukvannei 21 Bilkhawthlir 76 32 342 158 234 266 30 50 0 0 0 1 1 0 0 0 0 0 yes yes yes 118 7 Kolasib 02 College Veng, Kolasib Bilkhawthlir 238 48 1308 203 730 771 64 127 0 0 1 1 1 0 0 1 1 1 Yes Yes Yes 286 8 Kolasib 02 Diakkawn, Kolasib 08 Bilkhawthlir 964 62 0 0 0 2 3 0 0 0 0 0 yes yes yes 1026 9 Kolasib 02 Electric Veng, Kolasib Bilkhawthlir 244 26 270 26 538 601 10 0 0 0 0 0 0 0 0 0 0 Yes Yes Yes 270 10 Kolasib 02 Hmarveng, Kolasib 09 Bilkhawthlir 726 40 2527 160 1329 1358 30 757 0 0 1 4 5 0 0 0 0 1 Yes Yes Yes 766 11 Kolasib 02 Khuangpuilam, Kolasib Bilkhawthlir 293 8 1500 31 796 735 150 435 0 0 0 2 1 0 0 0 0 0 Yes Yes Yes 301 12 Kolasib 02 Meidum 19 Bilkhawthlir 205 18 0 0 1 1 1 0 0 0 0 1 yes yes yes 223 13 Kolasib 02 N. -

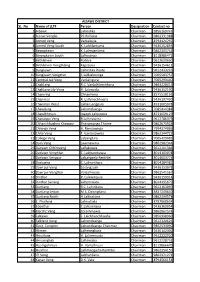

SL. No Name of LLTF Person Designation Contact No 1 Aibawk

AIZAWL DISTRICT SL. No Name of LLTF Person Designation Contact no 1 Aibawk Lalrindika Chairman 9856169747 2 Aizawl Venglai PC Ralliana Chairman 9862331988 3 Armed Veng Vanlalbula Chairman 8794424292 4 Armed Veng South K. Lalthlantuma Chairman 9436152893 5 Bawngkawn K. Lalmuankima Chairman 9862305744 6 Bawngkawn South Lalrosanga Chairman 8118986473 7 Bethlehem Rohlira Chairman 9612629630 8 Bethlehem Vengthlang Kapzauva Chairman 9436154611 9 Bungkawn Lalrindika Royte Chairman 9612433243 10 Bungkawn Vengthar C.Lalbiaknunga Chairman 7005583757 11 Centtral Jail Veng Vanlalngura Chairman 7005293440 12 Chaltlang R.C. Vanlalhlimchhana Chairman 9863228015 13 Chaltlang Lily Veng H. Lalenvela Chairman 9436152190 14 Chamring Chhanhima Chairman 8575518166 15 Chanmari R. Lalhmachhuana Chairman 9436197490 16 Chanmari West Lalliansangpuia Chairman 8731005978 17 Chawilung Lalnuntluanga Chairman 7085414388 18 Chawlhhmun Joseph Lalnunzira Chairman 8731059129 19 Chawnpui Veng R.Lalrinawma Chairman 9612786379 20 Chhanchhuahna Khawpui Thangmanga Thome Chairman 9862673924 21 Chhinga Veng H. Ramzawnga Chairman 7994374886 22 Chite Veng F. Vanlalsawma Chairman 9862344723 23 College Veng Lalsanglura Chairman 7005429082 24 Dam Veng Lawmawma Chairman 9862982344 25 Darlawn Chhimveng Lalfakzuala Chairman 9612201386 26 Darlawn Venghlun C. Lalchanmawia Chairman 8014103078 27 Darlawn Vengpui Lalsangzela Renthlei Chairman 8014603774 28 Darlawng C. Lalnunthara Chairman 8014184382 29 Dawrpui Veng Zosangzuali Chairman 9436153078 30 Dawrpui Vengthar Vanlalhruaia Chairman 9862541567 31 Dinthar R. Lalawmpuia Chairman 9436159914 32 Dinthar Sairang Lalremruata Chairman 8014195679 33 Durtlang R.C. Lalrinliana Chairman 9612163099 34 Durtlang Leitan M.S. Dawngliana Chairman 8837209640 35 Durtlang North H.Lalthakima Chairman 9862399578 36 E. Phaileng Lalruatzela Chairman 8787868634 37 Edenthar C.Lalramliana Chairman 9436360954 38 Electric Veng Zorammawia Chairman 9862867574 39 Falkawn F. Lalchhanchhuaha Chairman 9856998960 40 Falkland Veng Lalnuntluanga Chairman 9612320626 41 Govt. -

List of Eklavya Model Residential Schools in India (As on 20.11.2020)

List of Eklavya Model Residential Schools in India (as on 20.11.2020) Sl. Year of State District Block/ Taluka Village/ Habitation Name of the School Status No. sanction 1 Andhra Pradesh East Godavari Y. Ramavaram P. Yerragonda EMRS Y Ramavaram 1998-99 Functional 2 Andhra Pradesh SPS Nellore Kodavalur Kodavalur EMRS Kodavalur 2003-04 Functional 3 Andhra Pradesh Prakasam Dornala Dornala EMRS Dornala 2010-11 Functional 4 Andhra Pradesh Visakhapatanam Gudem Kotha Veedhi Gudem Kotha Veedhi EMRS GK Veedhi 2010-11 Functional 5 Andhra Pradesh Chittoor Buchinaidu Kandriga Kanamanambedu EMRS Kandriga 2014-15 Functional 6 Andhra Pradesh East Godavari Maredumilli Maredumilli EMRS Maredumilli 2014-15 Functional 7 Andhra Pradesh SPS Nellore Ozili Ojili EMRS Ozili 2014-15 Functional 8 Andhra Pradesh Srikakulam Meliaputti Meliaputti EMRS Meliaputti 2014-15 Functional 9 Andhra Pradesh Srikakulam Bhamini Bhamini EMRS Bhamini 2014-15 Functional 10 Andhra Pradesh Visakhapatanam Munchingi Puttu Munchingiputtu EMRS Munchigaput 2014-15 Functional 11 Andhra Pradesh Visakhapatanam Dumbriguda Dumbriguda EMRS Dumbriguda 2014-15 Functional 12 Andhra Pradesh Vizianagaram Makkuva Panasabhadra EMRS Anasabhadra 2014-15 Functional 13 Andhra Pradesh Vizianagaram Kurupam Kurupam EMRS Kurupam 2014-15 Functional 14 Andhra Pradesh Vizianagaram Pachipenta Guruvinaidupeta EMRS Kotikapenta 2014-15 Functional 15 Andhra Pradesh West Godavari Buttayagudem Buttayagudem EMRS Buttayagudem 2018-19 Functional 16 Andhra Pradesh East Godavari Chintur Kunduru EMRS Chintoor 2018-19 Functional -

Schedule for Selection of Below Poverty Line (Bpl) Families

SCHEDULE-I: SCHEDULE FOR SELECTION OF BELOW POVERTY LINE (BPL) FAMILIES STATE & STATE CODE : MIZORAM 15 NAME OF DISTRICT : CHAMPHAI DISTRICT CODE : 04 NAME OF BLOCK : NGOPA BLOCK CODE : 03 In Thlakhat awmdan Chhungkaw a ST/ Bank RUS Nu/ Village/ Village/ (katcha/ Voter ID Ration hotu chawhruala SC/ Account NO Pa hming Veng Veng Code No semi Card No Card No House in luah# hming pawisa nei/miIn Others No Chhungkaw pucca/ member zat lakluh zat pucca)@ 1 2 3 4 5 6 7 8 9 10 11 12 13 14 1967 Thangliana Khuala (L) 5 1700 Changzawl 10 22 01 11 FDV0198457 10097 ST 97009514505 1968 Lalzamlova Thanliana (L) 3 1700 Changzawl 10 24 01 11 FDV0219915 10068 ST 97000951035 1969 K Lalbiaksanga Lalbiaknunga (L) 2 1700 Changzawl 10 70 01 11 SSZ0022897 10019 ST 97003297000 1970 Lalnunhlima K Zabuanga (L) 7 3500 Changzawl 10 71 01 11 FDV0044826 10046 ST 25034017704 1971 Lalchhanhima Lalduhawma 5 2000 Changzawl 10 72 01 11 FDV0045047 10028 ST 97002524591 1972 Laldanga Ralkapa (L) 2 1700 Changzawl 10 75 01 11 FDV0049297 10030 ST 97002159377 1973 Hrangkima Tlanglawma (L) 6 2000 Changzawl 10 16 01 11 FDV0045039 10011 ST 97003793802 1974 Biakthangsanga Lalchhana 4 3000 Changzawl 10 80 01 11 FDV0062950 10003 ST 25034016438 1975 Lalsawmzuala Sapkhuma 1 2000 Changzawl 10 29 01 10 FDV0044545 10057 ST 97004199294 1976 Lalhmangaiha KT Hranga (L) 1 1500 Changzawl 10 60 01 11 FDV0044776 10034 ST 97004232030 1977 Sapkhuma Vanlalliana (L) 5 1700 Changzawl 10 7 01 11 FDV0045161 10093 ST 25034019553 1978 C Kapmawia Tlanglawma (L) 4 2500 Changzawl 10 16 01 11 FDV0044479 10104 -

Issue No : 28 Time : 12Th May, 2020 @ 7:00 PM SARS-Cov-2 (COVID-19

ation please visit the following link : For latest COVID-19 related information in Mizoram, pleaseclick the following links : https://twitter.com/dipr_mizoram?s=09 https://instagram.com/dipr_mizoram?igshid=1akqtv09bst7c https://www.facebook.com/Department-of-Information-Public-Relations-Govt-of-Mizoram- 113605006752434/ Issue No : 28 Time : 12th May, 2020 @ 7:00 PM 1. May ni 12, 2020 tlai dar 5:30 a Khawvel COVID-19 dinhmun (source: World Health Organization) Confirmed cases - 40,58,252 Confirmed deaths - 2,81,736 Countries, areas or - 213 territories with cases COVID-19 natna vei hmuhchhuah tamna ram te : USA – 12,98,287 Russia – 2,32,243 Spain - 2,27,436 United Kingdom – 2,23,064 Italy – 2,19,814 Germany – 1,70,508 Brazil-1,62,699 Turkey – 1,39,771 France – 1,37,491 Iran – 1,09,286 China – 84,451 India – 70,756 *darkar 24 chhungin Russia in Spain a lehpel a, a vawikhat nan India chu a sang zual ram 12 zingah a tel 2. May ni 12, 2020 zing dar 8:00 a India ram COVID-19 dinhmun (source : MoHFW, GOI) COVID-19 positive case confirm tawh zawng zawng zat - 70,756 SARS-CoV-2 (COVID-19) vanga thi awmna State/ UT (22) : Andhra Pradesh - 45, Assam - 2, Bihar - 6, Chandigarh- 2, Delhi - 73, Gujarat - 513, Haryana-11, Himachal Pradesh - 2, Jammu & Kashmir-10, Jharkhand - 3, Karnataka - 31, Kerala - 4, Madhya Pradesh - 221, Maharashtra –868, Meghalaya - 1, Odisha - 3, Punjab - 31, Rajasthan-113, Tamil Nadu-53, Telengana-30, Uttarakhand – 1, Uttar Pradesh - 80, West Bengal – 190 India ram State/UT 33 ah SARS-CoV-2 (COVID-19) vei hmuhchhuah tawh a ni * Darkar 24 chhungin sample 85,891 test niin positive case thar 3604 hmuh a ni a, mi 1538 dam (cured) a puan niin 87 in an thihpui a ni. -

SDEO W.PHAILENG Sl

SELECTED CANDIDATES FOR TEMPORARY ENGAGEMENT OF MIDDLE SCHOOL HINDI TEACHERS UNDER CSS WITH PLACE OF POSTING,2020-2021 UNDER SDEO W.PHAILENG Sl. Name of Name and Address Qualification Remarks Name Of School Place of Posting No Training Hindi General Lalfakawmi Praveen Hindi Shikshak 1 D/o Lalrinliana B.A Govt Lallen M/S SDEO W.Phaileng (Mizoram) Diploma Lallen Lalhmunmawii D/o Khawvelthanga Praveen Hindi Shiksahak 2 SSSE Chhippui UPS SDEO W.Phaileng Kawnmawi Veng,Chhippui (Mizoram) Diploma Mamit Dist. PC Lalkhumtiri Praveen Hindi Shikshak 3 D/o PC Sangtawna HSSLC Govt Khawhnai M/S SDEO W.Phaileng (Mizoram) Diploma Chhinga Veng Zarzoliana Fanai Hindi Shikshak 4 S/o F.Laldawngliana B.A with Hindi Govt NM M/S,Marpara SDEO W.Phaileng Diploma Tuikual 'N', Aizawl Lalbiakkimi Praveen Hindi Shikshak 5 D/o C.Lalruala HSSLC W Phulpui UPS SDEO W.Phaileng (Mizoram) Diploma W.Phaileng, Dinthar, Mamit Lalrinmawii Praveen 6 D/o Laikunga HSSLC D.El.Ed W.Phaileng UPS SDEO W.Phaileng (Mizoram) Chhippui I,Kawnmawi Veng Nimai Chakma Praveen Hindi Shikshak 7 S/o Sukro Sen Chakma HSSLC Hruiduk UPS SDEO W.Phaileng (Mizoram) Diploma Hruiduk,W.Phaileng, Mamit Lalbiakmawia Ratna Hindi Shikshan 8 S/o Lalbiaknunga HSSLC Govt Parvatui M/S SDEO W.Phaileng (Wardha) Praveen Ramhlun North Rosy Lalhmahruaii Praveen Hindi Shikshan 9 D/o Lalhmingmawia Ralte HSSLC L.M Phuldungsei M/S (GIA) SDEO W.Phaileng (Mizoram) Praveen Tuahzawl, Mamit PC Vanlalnghaki Praveen Hindi Shikshak Govt.T.M.M/S Chhippui 10 D/o PC Lalchuailova B.A SDEO W.Phaileng (Mizoram) Diploma Kawnmawi. -

Project Staff

Project Staff Thanhlupuia : Research Officer Ruth Lalrinsangi : Inspector of Statistics Lalrinawma : Inspector of Statistics Zorammawii Colney : Software i/c Lalrintluanga : Software i/c Vanlalruati : Statistical Cell Contents Page No. 1. Foreword - (i) 2. Preface - (ii) 3. Message - (iii) 4. Notification - (iv) Part-A (Abstract) 1. Dept. of School Education, Mizoram 2009-2010 at a Glance - 1 2. Number of schools by management - 2 3. Enrolment of students by management-wise - 3 4. Number of teachers by management-wise - 4 5. Abstract of Primary Schools under Educational Sub-Divisions - 5-9 6. Abstract of Middle Schools under Educational Sub-Divisions - 10-16 7. Abstract of High Schools under Educational Districts - 17-18 8. Abstract of Higher Secondary Schools under Educational Districts - 19-23 Part-B (List of Schools with number of teachers and enrolment of students) PRIMARY SCHOOLS: Aizawl District 1.SDEO, AizawlEast - 25-30 2.SDEO, AizawlSouth - 31-33 3.SDEO, AizawlWest - 34-38 4. SDEO, Darlawn - 39-41 5.SDEO, Saitual - 42-43 Champhai District 6.SDEO, Champhai - 44-47 7. SDEO, Khawzawl - 48-50 Kolasib District 8. SDEO, Kolasib - 51-53 9. SDEO, Kawnpui - 54-55 Lawngtlai District 10. EO, CADC - 56-59 11. EO, LADC - 60-64 Lunglei District 12.SDEO, LungleiNorth - 65-67 13.SDEO, LungleiSouth - 68-70 14.SDEO, Lungsen - 71-74 15. SDEO, Hnahthial - 75-76 Mamit District 16. SDEO, Mamit - 77-78 17. SDEO, Kawrthah - 79-80 18.SDEO, WestPhaileng - 81-83 Saiha District 19. EO, MADC - 84-87 Serchhip District 20. SDEO, Serchhip - 88-89 21. SDEO, North Vanlaiphai - 90 22.SDEO, Thenzawl - 91 MIDDLE SCHOOLS: Aizawl District 23.SDEO, Aizawl East - 93-97 24.SDEO, AizawlSouth - 98-99 25. -

The Mizoram Gazette EXTRA ORDINARY Published by Authority RNI No

The Mizoram Gazette EXTRA ORDINARY Published by Authority RNI No. 27009/1973 Postal Regn. No. NE-313(MZ) 2006-2008 Re. 1/- per page VOL - XLII Aizawl, Wednesday 6.3.2013 Phalguna 15, S.E. 1934, Issue No. 109 ORDER No.H.11018/2/2007-PW, the 22nd February,2013. In supersession of this Department’s Notification of even No. dated 29th November, 2007 and in exercise of power conferred by section 3 under chapter 11 of the Mizoram Highway Act, 2002, the Governor of Mizoram is pleased to declare roads mentioned in Statement 1, 11, 111 & 1V as - 1) State Highways (SH) 2) Major District Road (MDR) 3) Other District Road (ODR) 4) Village Road (VR) respectively with immediate effect. Enclo : Statement 1, 11, 111 & 1V. Lalram Thanga, Principal Secretary to the Govt. of Mizoram, Public Works Department. Ex-109/2013 - 2 - STATEMENT - 1 STATE HIGHWAYS (SH) SI.No Name of Road Length in Km Remark 1. Aizawl - Thenzawl - Lunglei 164.00 SH - 1 2. Lunglei - Tlabung 91.00 SH - 2 3. Rengtekawn - NH ‘154’ 6.000 SH - 3 4. Champhai - Zokhawthar 29.000 SH - 4 Total of State Highways (SH) 290.000 STATEMENT - 11 MAJOR DISTRICT ROADS (MDR) SI.No Name of Road Length in Km Remark 1. Tuilutkawn-Kawrtethawveng-Kanhmun(Formerly known as Katamani-Demagiri road) 96.000 2. Bairabi-Zamuang Road 28.000 3. Tuipuibari W. Kawnpui 18.000 4. Mamit- Bairabi 36.000 5. Buhchang - Phaisen 9.000 6. Serkhan - Bagha 117.000 7. Bilkhawthlir- Saiphai-Natasura 17.000 8. Serchhip-Thenzawl-Buarpui-Bunghmun 126.000 9. -

State Finances Audit Report of the Comptroller and Auditor General of India

State Finances Audit Report of the Comptroller and Auditor General of India for the year ended 31 March 2019 Government of Mizoram TABLE OF CONTENTS Para No. Title Page Preface v Executive Summary vii CHAPTER-I Finances of the State 1.1 Profile of the State 1 1.2 Basis for State Finances Audit Report 1 1.3 Budgetary Processes 2 1.4 Structure of Government Accounts 3 1.5 Gross State Domestic Product 4 1.6 Fiscal Correction Path 6 1.7 Trends in key Fiscal Parameters 7 1.8 Major changes in key fiscal aggregates vis‑à‑vis 2017‑18 9 1.9 Sources and Application of Funds 10 1.10 Summary of Current Year Fiscal Transactions 10 1.11 Budget Estimates and Actuals 12 1.12 Buoyancy Ratios 13 1.13 Major policy initiatives in Budget Speech 14 1.14 Resources of the State 14 1.15 Revenue Receipts 16 1.16 Capital Receipts 22 1.17 Public Account Receipts 23 1.18 Reserve Funds 24 1.19 Application of Resources 26 1.20 Quality of Expenditure 34 1.21 Financial Analysis of Expenditure and Investments 37 1.22 Assets and Liabilities 41 1.23 Debt Management and Sustainability 43 1.24 Conclusion 47 1.25 Recommendations 47 State Finances Audit Report 2018-19 i Page Para No. Title Page CHAPTER-II Budgetary Management 2.1 Introduction 49 2.2 Budget preparation process 49 2.3 Financial Accountability and Budget Review 49 2.4 Sub-optimal utilisation of budgeted funds 51 2.5 Missing/Incomplete Explanation for Variation from Budget 51 2.6 Large and Persistent Savings in Grants/Appropriation 53 2.7 Appropriation vis‑à‑vis Allocative Priorities 54 2.8 Financial Accountability -

The Mizoram Gazette Published by Authority

The Mizoram Gazette EXTRA ·ORDINARY Published by Authority REGN. NO. N.E.-313 (MZ) Rs. 2/- per Issue VOL. XXX" Aizawl. Wednesday, 26.4.2006, Valsakha 6, S.E. 1928, Issue No. 103 NOTfCATION No. B. 14016/3/02-LAD/VC, the 18th April, 2006. In exercise of the powers co nferred by Section 7(1 )(2), Section 15 and Section 22(1) of the Lusbai Hills District (Village Councils) Act, 1953, as amended from time to time, the Gover- nor of Mizoram is pleased to approve Executive Body of the following Village Councils as shown in the enclosed Annexure within Cha mphai District. R. Sangliankhuma, Addl. Secretary, Local Administration Department. ANNEXURE CHAMPHAI DISTRICT -........------;-------- ----- 1 2 3 4 I4-KHAWBUNG Ale 1. Buang 1. Tinlinga· President 2. Thangchhinga Vice President & Treasurer 3. K. Lalzawngliana Secretary 4. ParlaV\oma Crier Ex-103/20C6 2 1 2 3 4 2. Bungzung J. Lalringzuala President 2. Lalpianfa Vice Pr�sider.t 3. La]zapa Trt:asurer 4. Lalhmingliana Secretary 5. Sangkhuma Crier 3. Bulfekzawl 1. Vanlalrin ga President 2. Chhunkhuma Vice Presifient 3. Chh un tb angvunga Treasurer 4. Laltums2nga Seer etary 5. I. F. }.'Iallga Crier 4. Chawngtui -E' Not yet formed Executive Body 5. Dungtlang 1. H. Laldin gliana President ., .. C. Zalawma Vice President 3. K. LaIthlamuana Treasurer 4. C. Lalzama Secretary 5. Kaprothanga Crier l 6. Farkawn 1. Lalslama President 2. Manghupa Vice President 3. Engm av. ia Treasurer 4. Ljansailova Secretary 5. Lalrawna Crier 7. Hruaikawn 1. C. Hranghleikapa President 2. Sangtinkulha Vice President 3. Sa ngtha n gpuia Treasurer 4 . -

Mizoram Education (Transfer and Posting of School Teachers) Rules

The Mizoral111~Gazette~' EXTRA ORDINARY, ' ' •.. ,- '. ,I Published by Authoritv' REGN. NO. N.E.-313 (MZ) Rs. 2/- per Issue Vol. XXXV Aizawl, W~dnesday, 26.4.2006, Vaihsakha 6, S.E. 1928, Issue No. 104 No .A. 23022/5/2006 EDN, the 12th April, 2006. In exercise of th,e power con• erred by clause (xxxv) of sub-section (2) of sectidh 30 of the Mizoram Educa• tion Act, 2e03 (Act No. 5 of .2003), the Governor of Mizoram" is pleased to make the [allowing rules, namely :- . 1. SnORT TITLE? EXTENT AND COMMENCEMENT : (1) These Rules may be called the Mizoram Education (Transfer and . Posting of School Teachers) Rules, 2006, (2) It shall extend to the whole of Mizoram in respect of Elementary ,Educdtion and Secondary£ducation, except Chakllla Autonomous District, Lai Autonomou3 District and Mara Autohomous Dis• trict in respect of Elementary Education 'only. (3) These rul es shall com::: into force from til~ date of notificati on in the Mizoram Gazette. 2. IN THESE RULES, UNLESS THE CONTEXT OTHERWISE REQUIRES : ;- (1')' "Act" means MizoramEducati~n Act, 2003 (Act No. 5 of 2003) (2) ""Appropriate AuthoJity" shall mean the authority.as specified in Rule 9; (3) "District" means the jurisdiction area prescribed by tb.e Government of District Education Officer; (4) "Elementary School" means Primary Schools and Middle Schools~ (5) "Government" means the Government of Mizoram. (€i) "Sanctioned strellgth'>"me'<lDSth.t' number of posts 'of teachers as a 'particular School as Sanctiolled by the Government., -', , (-7) "Schedule" m6anl~a Schedul~ appended .,to these Rule·s; -l"fl' Ex-l04/2006 2 (8) "Secondary School" means High Schools and Higher Secondary Schools.