PCA Case No. AA 227 in the MATTER of an ARBITRATION BEFORE a TRIBUNAL CONSTITUTED in ACCORDANCE with ARTICLE 26 of the ENERGY CH

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Harvard University

HARVARD UNIVERSITY ROBERT AND RENÉE BELFER CENTER FOR SCIENCE AND INTERNATIONAL AFFAIRS 2000-2001 ANNUAL REPORT 2 Robert and Renée Belfer Center for Science and International Affairs 2000-2001 Annual Report Director’s Foreword 5 Overview From the Executive Director 7 Environment and Natural Resources Program TABLE 8 OF Harvard Information Infrastructure Project 52 CONTENTS International Security Program 71 Science, Technology and Public Policy Program 109 Strengthening Democratic Institutions Project 155 WPF Program on Intrastate Conflict, Conflict Prevention, and Conflict Resolution 177 Events 188 Publications 219 Biographies 241 Robert and Renée Belfer Center for Science and International Affairs 3 2000-2001 Annual Report 4 Robert and Renée Belfer Center for Science and International Affairs 2000-2001 Annual Report Director’s Foreword —————————————♦ For the hub of the John F. Kennedy School’s research, teaching, and training in international security affairs, environmental and resource issues, conflict prevention and resolution, and science and technology policy, the first academic year of the new century has been bracing. According to our mission statement, The Belfer Center for Science and International Affairs strives to provide leadership in advancing policy-relevant knowledge about the most important challenges of international security and other critical issues where science, technology, and international affairs intersect. BCSIA’s leadership begins with the recognition of science and technology as driving forces transforming threats and opportunities in international affairs. The Center integrates insights of social scientists, technologists, and practitioners with experience in government, diplomacy, the military, and business to address critical issues. BCSIA involvement in both the Republican and Democratic campaigns. BCSIA was privileged to have senior advisors in both camps in one of the most unforgettable American elections in recent memory. -

The Russia You Never Met

The Russia You Never Met MATT BIVENS AND JONAS BERNSTEIN fter staggering to reelection in summer 1996, President Boris Yeltsin A announced what had long been obvious: that he had a bad heart and needed surgery. Then he disappeared from view, leaving his prime minister, Viktor Cher- nomyrdin, and his chief of staff, Anatoly Chubais, to mind the Kremlin. For the next few months, Russians would tune in the morning news to learn if the presi- dent was still alive. Evenings they would tune in Chubais and Chernomyrdin to hear about a national emergency—no one was paying their taxes. Summer turned to autumn, but as Yeltsin’s by-pass operation approached, strange things began to happen. Chubais and Chernomyrdin suddenly announced the creation of a new body, the Cheka, to help the government collect taxes. In Lenin’s day, the Cheka was the secret police force—the forerunner of the KGB— that, among other things, forcibly wrested food and money from the peasantry and drove some of them into collective farms or concentration camps. Chubais made no apologies, saying that he had chosen such a historically weighted name to communicate the seriousness of the tax emergency.1 Western governments nod- ded their collective heads in solemn agreement. The International Monetary Fund and the World Bank both confirmed that Russia was experiencing a tax collec- tion emergency and insisted that serious steps be taken.2 Never mind that the Russian government had been granting enormous tax breaks to the politically connected, including billions to Chernomyrdin’s favorite, Gazprom, the natural gas monopoly,3 and around $1 billion to Chubais’s favorite, Uneximbank,4 never mind the horrendous corruption that had been bleeding the treasury dry for years, or the nihilistic and pointless (and expensive) destruction of Chechnya. -

The North Caucasus: the Challenges of Integration (III), Governance, Elections, Rule of Law

The North Caucasus: The Challenges of Integration (III), Governance, Elections, Rule of Law Europe Report N°226 | 6 September 2013 International Crisis Group Headquarters Avenue Louise 149 1050 Brussels, Belgium Tel: +32 2 502 90 38 Fax: +32 2 502 50 38 [email protected] Table of Contents Executive Summary ................................................................................................................... i Recommendations..................................................................................................................... iii I. Introduction ..................................................................................................................... 1 II. Russia between Decentralisation and the “Vertical of Power” ....................................... 3 A. Federative Relations Today ....................................................................................... 4 B. Local Government ...................................................................................................... 6 C. Funding and budgets ................................................................................................. 6 III. Elections ........................................................................................................................... 9 A. State Duma Elections 2011 ........................................................................................ 9 B. Presidential Elections 2012 ...................................................................................... -

Observation of the Presidential Election in the Russian Federation (4 March 2012)

Parliamentary Assembly Assemblée parlementaire http://assembly.coe.int Doc. 12903 23 April 2012 Observation of the presidential election in the Russian Federation (4 March 2012) Election observation report Ad hoc Committee of the Bureau Rapporteur: Mr Tiny KOX, Netherlands, Group of the Unified European Left Contents Page 1. Introduction ............................................................................................................................................. 1 2. Political and legal context ....................................................................................................................... 2 3. Election administration and voter and candidate registration .................................................................3 4. The campaign period and the media environment.................................................................................. 4 5. Complaints and appeals ......................................................................................................................... 5 6. Election day ............................................................................................................................................ 5 7. Conclusions ............................................................................................................................................ 6 Appendix 1 – Composition of the ad hoc committee.................................................................................... 8 Appendix 2 – Programme of the pre-electoral mission (Moscow, -

OON31.P65 19.01.04, 14:04 1 Cyan

OON31.p65 1 19.01.04, 14:04 Cyan Visit of the UNESCO Director-General, Ko¿tiro Matsuura, to Russia The UNESCO Director- Art in the presence of minis- General visited the Russian ters, including ;irst Deputy ;ederation for the second Prime-Minister of R;, Ms. time 2526 November 2003 Karelova, Minister of ;oreign on the invitation of the Pres- Affairs, Mr. Ivanov, Minister ident of the Russian ;eder- of Culture, Mr. Shvydkoy, as ation, Mr. Vladimir Putin. well as Chairperson of the The programme of the visit Commission of the Russian included a meeting of Mr. ;ederation for UNESCO, Matsuura with Mr. Putin, Mr. ;ortov, Permanent Del- the participation of the egate of the Russian ;edera- UNESCO Director-General tion to UNESCO, Mr. Kala- in the meeting of the Presi- manov, Assistant to the dential Council for Culture UNESCO Director-General and Art, a meeting with the for Culture, Mr. Bouchenaki, ;irst Deputy Prime-Minister Director of the UNESCO of the Russian ;ederation, Mr. Vladimir Putin greets Mr. Ko¿tiro Matsuura Moscow Office, Mr. Quéau, Ms. Galina Karelova, and in the Kremlin and other representatives of participation at the ceremo- the UNESCO Headquarters. ny of awarding Mr. Matsuura with After the meeting with Mr. Putin in the Opening the meeting, President the title of Honorary Professor of Kremlin Ko¿tiro Matsuura made a Moscow State University. speech at the Council for Culture and (To be continued on p. 8) Contents: UNESCO UNA Visit of the UNESCO Director-General, Students and Journalists Discuss the Present Ko¿tiro Matsuura, to Russia ..................................... -

VI Europe–Russia Economic Forum

VI Europe–Russia Economic Forum Sejm of the Republic of Poland Warsaw, Poland ST OF MAY – ST OF JUNE Under the High Patronage of Grzegorz Schetyna, Marshal of the Sejm of the Republic of Poland Organizer Publisher Foundation Institute for Eastern Studies ul. Solec 85 00–382 Warsaw Tel.: + 48 22 583 11 00 Fax: + 48 22 583 11 50 e–mail: [email protected] www.forum–ekonomiczne.pl Layout BikerStudio www.biker.wns.pl Print Flexergis Sp. z o.o. (Drukarnia BAAD) Warsaw 2011 Contents Programme . 5 Speakers. 19 List of Participants . 55 Programme Programme 6 Programme Programme 7 May 31, 2011 Registration of participants 11:30–12:15 Presentation of the Economic Forum “Russia 2010. Report on Transformation”. Political and Economic 12:15–13:30 Situation in Russia in 2010 Break 13:30–13:45 Partnership for Modernization 13:45–15:15 Lunch 15:15–16:15 Russia in 21st Century. Expectations and Projects 16:15–17:45 Coffee break 17:45–18:00 European Union and Russia: Common Values 18:00–19:30 Reception 20:00 www.economic–forum.pl www.economic–forum.pl 6 Programme Programme 7 June 1, 2011 Energy Industry. Russian Resources and European Security 09:00–10:30 NATO–EU–Russia Relations after the Lisbon Summit 09:00–10:30 Coffee break 10:30–10:45 Europe and Russia in the Global Economy: Opportunities and Threats 10:45–12:15 EU and Russia – Foreign Policy Directions 10:45–12:15 Coffee break 12:15–12:30 EU–Russia. New Perspectives for Partnership and Cooperation 12:30–14:00 Regional Cooperation. -

DISCUSSION PAPER Public Disclosure Authorized

SOCIAL PROTECTION & JOBS DISCUSSION PAPER Public Disclosure Authorized No. 1931 | MAY 2019 Public Disclosure Authorized Can Local Participatory Programs Enhance Public Confidence: Insights from the Local Initiatives Support Program in Russia Public Disclosure Authorized Ivan Shulga, Lev Shilov, Anna Sukhova, and Peter Pojarski Public Disclosure Authorized © 2019 International Bank for Reconstruction and Development / The World Bank 1818 H Street NW Washington DC 20433 Telephone: +1 (202) 473 1000 Internet: www.worldbank.org This work is a product of the staff of The World Bank with external contributions. The findings, interpretations, and conclusions expressed in this work do not necessarily reflect the views of The World Bank, its Board of Executive Directors, or the governments they represent. The World Bank does not guarantee the accuracy of the data included in this work. The boundaries, colors, denominations, and other information shown on any map in this work do not imply any judgment on the part of The World Bank concerning the legal status of any territory or the endorsement or acceptance of such boundaries. RIGHTS AND PERMISSIONS The material in this work is subject to copyright. Because The World Bank encourages dissemination of its knowledge, this work may be reproduced, in whole or in part, for noncommercial purposes as long as full attribution to this work is given. Any queries on rights and licenses, including subsidiary rights, should be addressed to World Bank Publications, The World Bank Group, 1818 H Street NW, Washington, -

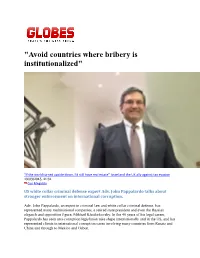

"Avoid Countries Where Bribery Is Institutionalized"

"Avoid countries where bribery is institutionalized" “If the world turned upside down, I’d still have real estate” Israel and the UK ally against tax evasion 19/03/2015, 11:31 Gur Megiddo US white collar criminal defense expert Adv. John Pappalardo talks about stronger enforcement on international corruption. Adv. John Pappalardo, an expert in criminal law and white collar criminal defense, has represented many multinational companies, a retired state president and even the Russian oligarch and opposition figure, Mikhail Khodorkovsky. In the 40 years of his legal career, Pappalardo has seen anti-corruption legislation take shape internationally and in the US, and has represented clients in international corruption cases involving many countries from Russia and China and through to Mexico and Gabon. Although the development of anti-corruption legislation internationally hugely influences the operations of multinational companies in developing countries, he says: “There is no law in the universe that will change human nature; there are countries where corruption is institutionalized as a tradition of centuries, where the demand for a bribe is so blatant and clear, you cannot conduct business there in a legal manner. In such cases I advise my clients to keep their distance.” Pappalardo heads the white-collar criminal defense department at law firm Greenberg Traurig, one of the most prominent firms in the US, and one of global renown, employing about 1,800 attorneys in 37 offices worldwide, including an office in Tel Aviv. Pappalardo began his career as a federal prosecutor in the field of white collar crime and advanced to the role of US Attorney for the District of Massachusetts. -

Berezovsky-Judgment.Pdf

Neutral Citation Number: [2012] EWHC 2463 (Comm) Royal Courts of Justice Rolls Building, 7 Rolls Buildings, London EC4A 1NL Date: 31st August 2012 IN THE HIGH COURT OF JUSTICE Case No: 2007 Folio 942 QUEEN’S BENCH DIVISION COMMERCIAL COURT IN THE HIGH COURT OF JUSTICE Claim Nos: HC08C03549; HC09C00494; CHANCERY DIVISION HC09C00711 Before: MRS JUSTICE GLOSTER, DBE - - - - - - - - - - - - - - - - - - - - - Between: Boris Abramovich Berezovsky Claimant - and - Roman Arkadievich Abramovich Defendant Boris Abramovich Berezovsky Claimant - and - Hine & Others Defendants - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - Laurence Rabinowitz Esq, QC, Richard Gillis Esq, QC, Roger Masefield Esq, Simon Colton Esq, Henry Forbes-Smith Esq, Sebastian Isaac Esq, Alexander Milner Esq, and Ms. Nehali Shah (instructed by Addleshaw Goddard LLP) for the Claimant Jonathan Sumption Esq, QC, Miss Helen Davies QC, Daniel Jowell Esq, QC, Andrew Henshaw Esq, Richard Eschwege Esq, Edward Harrison Esq and Craig Morrison Esq (instructed by Skadden, Arps, Slate, Meagher & Flom LLP) for the Defendant Ali Malek Esq, QC, Ms. Sonia Tolaney QC, and Ms. Anne Jeavons (instructed by Freshfields Bruckhaus Deringer LLP) appeared for the Anisimov Defendants to the Chancery Actions David Mumford Esq (instructed by Macfarlanes LLP) appeared for the Salford Defendants to the Chancery Actions Jonathan Adkin Esq and Watson Pringle Esq (instructed by Signature Litigation LLP) appeared for the Family Defendants to the Chancery Actions Hearing dates: 3rd – 7th October 2011; 10th – 13th October 2011; 17th – 19th October 2011; 24th & 28th October 2011; 31st October – 4th November 2011; 7th – 10th November 2011; 14th - 18th November 2011; 21st – 23 November 2011; 28th November – 2nd December 2011; 5th December 2011; 19th & 20th December 2011; 17th – 19th January 2012. -

Stress the Import Nce

stress the import nce 2009 Social REPoRT “ We believe that charitable programmes are even more important today than they were during the pre-crisis period. So in the future, as each year throughout the Bank’s history, we will continue to render comprehensive support and financial assistance to essential projects, reaffirming our reputation of a socially responsible company.” Rushan Khvesyuk Chairman of the Executive Board, Member of the Board of Directors Message from Alfa-Bank management As a biggest financial institution in Russia, Alfa-Bank has always attached great importance to social and charitable activities. We are pleased to present our social report telling about some of our most significant events and undertakings in 2009. Alfa-Bank has a profound respect for the cultural heritage of our great country and endeavours to contribute to preserving it. For instance, we financed restoration work on a number of unique books in the Orenburg Universal Scientific Library named after N. Krupskaya, including Decrees of Ekaterina Alexeevna and Peter II published as early as in 1743 and works of Mikhail Lomonosov. In Nizhniy Novgorod, we sponsored restoration of Nikolay Koshelev’s canvas The Burial of Christ which was the ver y fir st ar t work in the collection of the regional museum. Alfa-Bank also covered the costs of restoring two pictures of the globally recognised artist Ivan Shishkin — Evening in a Forest and Evening in a Pine Forest belonging to the Tatarstan State Museum of Fine Arts in Kazan. Having supported initiatives aimed at preserving memory of our past for many years running, we also prioritise care for the young and talented, since they are our future. -

PCA Case No. AA 228 in the MATTER of an ARBITRATION BEFORE a TRIBUNAL CONSTITUTED in ACCORDANCE with ARTICLE 26 of the ENERGY CH

PCA Case No. AA 228 IN THE MATTER OF AN ARBITRATION BEFORE A TRIBUNAL CONSTITUTED IN ACCORDANCE WITH ARTICLE 26 OF THE ENERGY CHARTER TREATY AND THE 1976 UNCITRAL ARBITRATION RULES - between - VETERAN PETROLEUM LIMITED (CYPRUS) - and - THE RUSSIAN FEDERATION FINAL AWARD 18 July 2014 Tribunal The Hon. L. Yves Fortier PC CC OQ QC, Chairman Dr. Charles Poncet Judge Stephen M. Schwebel Mr. Martin J. Valasek, Assistant to the Tribunal Mr. Brooks W. Daly, Secretary to the Tribunal Ms. Judith Levine, Assistant Secretary to the Tribunal Registry Permanent Court of Arbitration Representing Claimant: Representing Respondent: Professor Emmanuel Gaillard Dr. Claudia Annacker Dr. Yas Banifatemi Mr. Lawrence B. Friedman Ms. Jennifer Younan Mr. David G. Sabel SHEARMAN & STERLING LLP Mr. Matthew D. Slater Mr. William B. McGurn Mr. J. Cameron Murphy CLEARY GOTTLIEB STEEN & HAMILTON LLP Mr. Michael S. Goldberg Mr. Jay L. Alexander Dr. Johannes Koepp Mr. Alejandro A. Escobar BAKER BOTTS LLP TABLE OF CONTENTS LIST OF DEFINED TERMS ..................................................................................................................... xiii INTRODUCTION ........................................................................................................................................ 1 I. PROCEDURAL HISTORY ................................................................................................................ 2 A. COMMENCEMENT OF THE ARBITRATION ................................................................................... 2 -

Russia and the World: the View from Moscow

International Journal of Security Studies Volume 2 Issue 1 Article 1 2020 Russia and the World: The View from Moscow Daniel S. Papp Retired, [email protected] Follow this and additional works at: https://digitalcommons.northgeorgia.edu/ijoss Part of the Defense and Security Studies Commons, Military and Veterans Studies Commons, and the Peace and Conflict Studies Commons Recommended Citation Papp, Daniel S. (2020) "Russia and the World: The View from Moscow," International Journal of Security Studies: Vol. 2 : Iss. 1 , Article 1. Available at: https://digitalcommons.northgeorgia.edu/ijoss/vol2/iss1/1 This Article is brought to you for free and open access by Nighthawks Open Institutional Repository. It has been accepted for inclusion in International Journal of Security Studies by an authorized editor of Nighthawks Open Institutional Repository. Russia and the World: The View from Moscow Cover Page Footnote None This article is available in International Journal of Security Studies: https://digitalcommons.northgeorgia.edu/ijoss/ vol2/iss1/1 Introduction In 1939, British Prime Minister Winston Churchill famously observed that Russia was “a riddle wrapped in a mystery inside an enigma.” Less remembered but equally significant is what Churchill said next: “Perhaps there is a key. That key is Russian national interest."1 Much has changed in Russia and the world since 1939, but in many ways, Churchill’s observation is as valid today as it was then. What is Russia’s national interest? How do Russia’s leaders, especially Russian President Vladimir Putin, view their country’s national interest? And how can their viewpoints be determined? This is a challenging but not impossible task.