Annual Report and Accounts for the Year Ended 31 December 2017 CONTENTS

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Open Page 2017

Israel Aerospace Industries Ltd. 2017 Sustainability Report 20172016 in ina nutshella nutshell of procurement billion$ of procurement 3.6billion$in Sales 61% is local 3.5 in Sales 62% is local st in local patent 1 registration Record customer at 5.8 Backlog contracts billion$ Backlog of orders at 9 of billion$ of orders at 11 of billion$ Largest 14,857 high-tech company 15,359employees in Israel employees 18,23716,233 volunteeringvolunteering hours hours Sustaining over th 50,000 rankingth in the “best place to work” list households nationwide 9 6 ranking in the “best place to work” list 54%54% hazardoushazardous waste waste recycledrecycled or reused or reused 58%56% non-hazardousnon-hazardous waste waste recycledrecycled or reused or reused 435 500 GWh GWh Saved Savedsince 2007 since 2007 Message from our Board of Directors 102-14 IAIs 2017 sustainability report is a detailed record of our The very existence of IAI directly contributes to the strength and ongoing progress as a resilient, long-lasting, and extraordinary resilience of the local communities in which we operate across company. Our operations and products enable us not only to Israel. Our business model is built on identifying long term advance and achieve our business objectives, but also to fulll mega trends, and partnering with our customers to offer top our responsibilities towards our customers, employees, the quality technology excellence and innovations in every area communities in which we operate and society as a whole. they look to grow in. We report here in detail on the management of our environmental impact and the principles of We make this commitment actionable through specic pollution prevention and continual improvement integrated organizational mechanisms, starting with IAIs board of into our business. -

16.1.2020 Program | Cybertech Tel Aviv 2020 1/10 EXHIBITION OPENING HOURS 28.01.2020 |

16.1.2020 Program | Cybertech Tel Aviv 2020 EXHIBITION OPENING HOURS 28.01.2020 | 14:00-18:00 29-30.01.2020 | 08:00-18:00 28.01.2020 Tuesday \\ 28.01.2020 CyberMed | Hall I - P2 Hall M - P2 15:00–15:05 Opening Words By the host 15:05–15:15 Case Study: Editing X-Ray Images to Add or Remove Cancer 15:15–15:45 Med Tech: ML, AI and Big Data Implementation and Integration – Challenges and Opportunities I Panel 15:45–15:55 Bio Hacking 15:55–16:05 Tales From the Trenches - Lessons Learned from Ransomware and Other Incident Response Engagements 16:05–16:25 Protecting the Healthcare Industry 16:25–16:45 Data Privacy in the Age of Genomic Data – Access, Management, and Ownership 16:45–16:55 Medical Ethics in the Cyber Era 16:55–17:10 Investment in Cyber: the Latest Market Trends and Strategies 17:10–17:25 Open Questions Open questions to and from attendees followed by a discussion. 17:25–17:30 Closing Remarks: Hospitals Recognized as Critical Infrastructure - Yes or No By the host Frontier Tech | Hall I - P2 Hall I - P2 09:00–09:30 Gathering and Registration Moderator: Renana Ashkanzi, Principle, Grove Ventures 09:30–09:50 Keynote Dr. Orna Berry, Scientist, entrepreneur and executive 09:50–10:00 New Society with Frontier Tech and New Risk Management Okuya Toshikazu, Director, Ministry of Economy, Trade and Industry, Japan 10:00–10:30 Panel: Quantum Computing Moderator: Oded Melamed, Formerly Co-founder & CEO, Altair Semiconductor Prof. Roee Ozeri, VP Resource Development & Public Axairs, Weizmann Institute of Science Dr. -

2019 Sustainability Report 2 Our Sustainability

Israel Aerospace Industries Ltd. 2019 Sustainability Report 2 Our sustainability “IAI is a leader in the development, production and export of advanced commercial and military systems, in the air, at sea, on the ground, in space and cyber. As a large Israeli governmental company, IAI operates from a vision of growth and risk management, expressed by extensive investments, in order to ensure business strength alongside sustainable practice in Strategy........................8 environmental and social aspects, for the benefit of Integrity and ethics this generation and for the future ones.” ....26 Value creation .............36 An excerpt from IAI’s sustainability policy Innovation ...................48 Employees and community ..................54 Environment ...............70 GRI Content index ......86 Link to full policy https://www.iai.co.il/about/sustainability 3 From the Chairman of the board 102-14 | 102-15 Our long-standing contribution to Israel’s defense and economy, This report has been prepared according to the GRI standards, and has alongside our business in international markets, had positioned IAI as been reviewed externally for the fourth consecutive time. In addition, a leading Aerospace and Defense Company. Our solid results in 2019 as we aim to keep our stakeholders well informed in a timely manner, reflect the good performance of the business, following the outset of we are now publishing this report in full in both English and Hebrew, the company's new 2030 business strategy. and coinciding with our annual financial statements. We continue to deliver exceptional solutions in aviation, space, As we publish this report, the global community experiences cyber, land, and sea, while promoting inclusive and nurturing unprecedented times of turmoil due to the outbreak of the Coronavirus. -

Annual Report and Accounts 2016 BATM Advanced Communications Ltd

Products include instruments Products includeand instruments reagents for small to and reagents formedium small to labs and hospitals medium labs and hospitals Bio-MeBdiioc-aMl edical Genomics and Bioinformatics Division Genomics and BioinformaticsServices Division Services BATM Advanced Communications Ltd Communications Advanced BATM 2016 Annual Report and Accounts Developer and manufacturer of Diagnostic Equipment Distribution Developer and manufacturerhigh quality sterilizers of and medical Diagnostic Equipment Distribution high quality sterilizerswaste managementand medical waste management International IVD manufacturer and International IVDdevelopper manufacturer of In-vitro and Diagnostic developper of In-vitroSystems Diagnostic and Reagents Systems and Reagents Cloud Networking Business Ethernet Cloud Networking Business Ethernet Cyber Security Solutions Mobile Cyber Security Solutions Mobile Backhaul Backhaul Surveillance Surveillance Solutions Solutions ATCA Solutions ATCA Solutions Cyber Cyber Real time Real time and embedded and embeddedoperating system operating system NetwoNrkeitnwgo r&k ing & Cyber CDyivbiesri oDnivision Automated testing - Automated testingplanning - and development planning and development Enterprise Cloud Enterprise Cloud Neve Ne’eman Ind. Area 4 Ha’harash Street, P.O.B. 7318 Annual Report and Accounts 4524075 Hod Hasharon Israel for the year ended 31 December 2016 CONTENTS Directors, Secretary & Advisors 2 Financial & Operational Summary 3 Strategic Report Chairman’s Statement 4 Chief Executive Officer’s -

'Precise' Strikes: Fractured Bodies, Fractured Lives

Israel’s drone wars: An update ‘Precise’ strikes: Fractured Bodies, Fractured Lives Front Cover image: Israel’s Heron TP drone at Tel Nof Air Force base, February 2010. Credit: UPI/Debbie Hill. Note: The term ‘drone’ is used interchangeably with ‘Unmanned Aerial Vehicle (UAV)’ Drone Wars UK is a small British NGO established in 2010 to undertake research and advocacy around the use of armed drones. We believe that the growing use of remotely-controlled, armed unmanned systems is encouraging and enabling a lowering of the threshold for the use of lethal force as well as eroding well established human rights norms. While some argue that the technology itself is neutral, we believe that drones are a danger to global peace and security. We have seen over the past decade that once these systems are in the armoury, the temptation to use them becomes great, even beyond the constraints of international law. As more countries develop or acquire this technology, the danger to global peace and security grows. Published by Drone Wars UK Drone Wars UK Written by Chloe Skinner Peace House, 19 Paradise Street November 2019 Oxford, OX1 1LD Designed: Chris Woodward www.dronewars.net www.chriswoodwarddesign.co.uk [email protected] ‘Precise Strikes’, Fractured Bodies, Fractured Lives | Israel’s drone wars: An update | 1 Contents 1 INTRODUCTION 3 2 “A RAPIDLY-GROWING DIVISION”: Israel’s drones and their operators 5 3 “ACCESS, PERSISTENCE, ACCURACY.” The humanitarian claims made for drone technology 8 4 “IN A MATTER OF SECONDS, THEY WERE CUT TO PIECES.” Life -

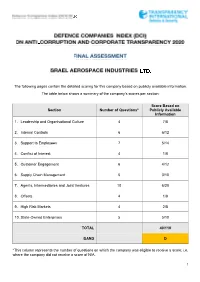

The Following Pages Contain the Detailed Scoring for This Company Based on Publicly Available Information

The following pages contain the detailed scoring for this company based on publicly available information. The table below shows a summary of the company’s scores per section: Score Based on Section Number of Questions* Publicly Available Information 1. Leadership and Organisational Culture 4 7/8 2. Internal Controls 6 6/12 3. Support to Employees 7 5/14 4. Conflict of Interest 4 1/8 5. Customer Engagement 6 4/12 6. Supply Chain Management 5 3/10 7. Agents, Intermediaries and Joint Ventures 10 6/20 8. Offsets 4 1/8 9. High Risk Markets 4 2/8 10. State-Owned Enterprises 5 5/10 TOTAL 40/110 BAND D *This column represents the number of questions on which the company was eligible to receive a score; i.e. where the company did not receive a score of N/A. 1 1. Leadership and Organisational Culture Question 1.1. Does the company have a publicly stated anti-bribery and corruption commitment, which is authorised by its leadership? Score 2 Comments There is evidence that the company has a publicly stated anti-bribery and corruption commitment, which details the company's stance against any form of corruption within the organisation. It is clear that this commitment was authorised and endorsed by the company's leadership. Evidence [6] President and CEO Letter (Document) Accessed 18/07/2019 https://www.iai.co.il/drupal/sites/default/files/2019-06/IAI%27s%20President%20and%20CEO%20Letter.pdf [p.1] Israel Aerospace Industries (IAI) is one of the world's leading companies in both the defense and commercial markets delivering state-of-the-art technologies and systems in all domains. -

Israeli Violations' Activities in the Opt 25 February 2015

Israeli Violations' Activities in the oPt 25 February 2015 The daily report highlights the violations behind Israeli home demolitions and demolition threats The Violations are based on in the occupied Palestinian territory, the reports provided by field workers confiscation and razing of lands, the uprooting and\or news sources. and destruction of fruit trees, the expansion of The text is not quoted directly settlements and erection of outposts, the brutality from the sources but is edited for of the Israeli Occupation Army, the Israeli settlers clarity. violence against Palestinian civilians and properties, the erection of checkpoints, the The daily report does not construction of the Israeli segregation wall and necessarily reflect ARIJ’s opinion. the issuance of military orders for the various Israeli purposes. Brutality of the Israeli Occupation Army Clashes erupted between Palestinians and the Israeli Occupation Army (IOA) in Al-Arroub refugee camp, north of Hebron city. The IOA fired rubber bullets, teargas and stun grenades at Palestinians, causing dozens of suffocation cases. (Pal Info 25 February 2015) Israeli Occupation Army (IOA) invaded and searched a Palestinian house in Kafr Sur village, south of Tulkarm city. The targeted house is located near the Israeli segregation wall. (Wattan 25 February 2015) 1 Israeli Occupation Army (IOA) fired teargas grenades at a Palestinian school in At-Tur/ Olive Mount neighborhood in Jerusalem city. As a result, dozens of Palestinians suffered gas inhalation. (RB2000 25 February 2015) Israeli Occupation Army (IOA) opened fire at Palestinian farmers while they were working in their land, east of Al-Maghazi refugee camp, east of Gaza strip. -

“South Africa's 800” by Henry Katzew

SOUTH AFRICA’S 800 The Story of South African Volunteers in Israel’s War of Birth by Henry Katzew Compiled and produced by Maurice and Marcia Ostroff from Henry Katzew’s original manuscript Edited by Joe Woolf Key to the Front Cover Top to bottom: • The famous Haganah immigrant ship S.S Exodus 1947, in which 4500 refugees were forcibly returned to Hamburg in September 1947. (See foreword & Palestine Post article page 23) • Boris Senior in a Spitfire constructed from bits and pieces. • A group of Machalniks, in the Tank Corps. • A column of the 9th Palmach, Commando Battalion. Revised and reprinted November 2003 COPYRIGHT© All rights reserved No part of this document may be reproduced by any means whatsoever, except with the prior express written permission of the South African Zionist Federation. Correspondence should be addressed to: Telfed, 19/1 Schwartz Street, Ra’anana, 43212 Israel Telephone +972 9-7446110 Fax + 972 9-7446112 E-mail: [email protected] About this book “South Africa’s 800” is about Machal, the collective Hebrew acronym for volunteers from abroad and about individual volunteers, colloquially known as Machalniks. The book reveals details never previously documented and provides a valuable new perspective on Israel’s birth and struggle for survival. It includes eye witness reports by active participants in the events. While written mainly through South African eyes, the book also contains gripping anecdotes about volunteers from the USA, Britain and other countries. It throws new light on important events and personalities of the time. In his engaging eloquent style, Henry Katzew takes the reader on a fascinating expedition through recent historical events including: • Adventures of 8 young South Africans in their ill-fated attempt to bypass British restrictions on immigration to Palestine, by travelling overland from Pretoria. -

Israeli Missions Around the World

ISRAEL INNOVATION NATION Israel INNOVATION NATION SECTION I Report in Foreign Affairs magazine, September-October 2014...................................... pages 1-3 SECTION II Extended report available online at www.countrystrategic.com............................................. pages 5-21 Sponsored Section INNOVATION NATION Company Highlight ISRAEL StraUSS’ mISSION In the past twenty-years, Israel has “In Israel, we have our own DNA of earned the nickname “start-up nation” policy innovation” explains the Ministry TURNINg ISRAEL exporting solutions to global human of Economy’s Chief Scientist, Avi into THE fOODtecH challenges in the field of water and Hasson. His office supervises twenty nation food technologies, healthcare and life incubators for early stage projects. Along- Started in 1936 with two cows in sciences, ICT, cybersecurity and en- side private venture capital, Israel provides Northern Israel, the Strauss Group ergy. Since the state was established in its entrepreneurs with the necessary has grown to become a significant 1948, kibbutz and moshav (communal backing to turn their innovative ideas into global player. Ofra Strauss, third and cooperative agricultural commu- profitable businesses. The country has the generation to lead the company, nities), then state companies and start- highest density of start-ups per capita, and the head of the Israel-US ups have led the way. which aim high and global with more Is- Chamber of Commerce, explains raeli companies listed on the NASDAQ the recipe for her group’s national than the entire European continent. and international success: carefully Harel Locker, Director General of selected partners and an insatiable the Prime Minister’s Office, wants quest for better products. Israel to further open to the world. -

University of London Thesis

2809076477 REFERENCE ONLY UNIVERSITY OF LONDON THESIS Name of Author COPYRIGHT This is a thesis accepted for a Higher Degree of the University of London. It is an unpublished typescript and the copyright is held by the author. All persons consulting the thesis must read and abide by the Copyright Declaration below. COPYRIGHT DECLARATION I recognise that the copyright of the above-described thesis rests with the author and that no quotation from it or information derived from it may be published without the prior written consent of the author. LOAN Theses may not be lent to individuals, but the University Library may lend a copy to approved libraries within the United Kingdom, for consultation solely on the premises of those libraries. Application should be made to: The Theses Section, University of London Library, Senate House, Malet Street, London WC1E 7HU. REPRODUCTION University of London theses may not be reproduced without explicit written perjnission from the University of London Library. Enquiries should be addressed to the Theses Section of the Library. Regulations concerning reproduction vary according to the date of acceptance of the thesis and are listed below as guidelines. A. Before 1962. Permission granted only upon the prior written consent of the author. (The University Library will provide addresses where possible). B. 1962 - 1974. In many cases the author has agreed to permit copying upon completion of a Copyright Declaration. C. 1975 - 1988. Most theses may be copied upon completion of a Copyright Declaration. D. 1989 onwards. Most theses may be copied. This thesis comes within category D. This copy has been deposited in the Library______ of £A..C* ^ This copy has been deposited in the University of London Library, Senate House, Malet Street, London WC1E 7HU. -

The Global Political Economy of Israel

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Nitzan, Jonathan; Bichler, Shimshon Book The Global Political Economy of Israel Provided in Cooperation with: The Bichler & Nitzan Archives Suggested Citation: Nitzan, Jonathan; Bichler, Shimshon (2002) : The Global Political Economy of Israel, ISBN 0-7453-1676-X, Pluto Press, London, http://bnarchives.yorku.ca/8/ This Version is available at: http://hdl.handle.net/10419/157972 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified -

122242340.Pdf

Contents Introduction Chapter One – The End of Inside Israel Chapter Two – The Conspirators Can’t Stop Conspiring Chapter Three – Netanyahu Is Dead, Long Live Deri Chapter Four – It’s the Same Old Song But With a Different Beast Since Rabin’s Been Gone Chapter Five - The CFR Takes Over Israel Chapter Six – Why Rabin Was Murdered Chapter Seven – The Shabak’s Patsies Chapter Eight – Israel Will Not Learn From Its History Chapter Nine – The NWO Closes In Chapter Ten – Will Israel Overcome? 3 INTRODUCTION Recently, a reader commented, “With Netanyahu, Sharon and Arens on top, the Likud is in good hands again.” I was discouraged. Had he soaked in nothing of my message? Israel’s primary enemy is not the Arabs, some of whom still express their hostility openly, though others have learned that keeping it under wraps for now is the better strategy. Our greatest threat comes from a little think tank in New York called the Council on Foreign Relations. The Arabs are merely their means to our end. In my 1997 book, Traitors and Carpetbaggers in the Promised Land, I detailed Netanyahu and Sharon’s corruption by the CFR. I warned that they are no less under CFR control than Rabin was or Barak is. Since then, we have found a new name on the CFR list. Moshe Arens is a member of the CFR’s foreign advisory team, sharing the Middle East desk with the PLO’s Hanan Ashrawi. In this book, I detail the CFR’s plan for Israel, right from the months of its leadership.